The markets were truly surprised

As yesterday’s Minutes advised

That higher for longer

Intent was much stronger

Than prior belief emphasized

The market response was to sell

Risk assets and thus, prices fell

But after the close

Nvidia rose

And now everything is just swell!

It turns out that Chairman Powell’s press conference had a distinctly more dovish feel to it than the tone of the FOMC meeting at the beginning of the month. At least that appears to be the situation based on the Minutes of the meeting that were released yesterday afternoon. In truth, it is somewhat surprising that given all the comments we have heard by virtually every member of the FOMC in the intervening three weeks, a reading of the Minutes resulted in altered opinions of how policy would evolve going forward.

While every Fed speaker has maintained the view that higher for longer remains the baseline, at the press conference, Powell essentially ruled out further rate hikes. But in the Minutes, it turns out “various” members indicated a willingness to raise rates if necessary. In addition, “a few” members would have supported continuing the QT process at the previous $60 billion/month runoff rather than adjusting it lower. Finally, “many” questioned just how restrictive current monetary policy actually is, and whether it is sufficient to drive inflation back to their target. Net, it appears there was quite a lively discussion in the room and the hawks are not willing to be ignored.

With this more hawkish stance now more widely understood, it cannot be surprising that risk assets sold off yesterday afternoon. While I grant that the equity declines were modest, between -0.2% and -0.5% in the US, the tone of conversation clearly changed. Meanwhile, the real damage occurred in the commodity markets where the recent sharp rise in metals prices ran into a proverbial buzzsaw and all of them fell sharply. For instance, gold fell -1.5% yesterday and is lower by another -0.7% this morning. Silver was a bit more volatile, losing -3.0% yesterday and down a further -1.25% today and the king of this move was copper, which tumbled more than -4% yesterday although it seems to be basing for now.

While there are several pundits who are describing these commodity price moves as a reaction to the dollar’s rebound, I actually see it more as a response to the idea that the Fed may be willing to fight inflation more aggressively than previously thought. Remember, a key to the metals markets’ rally is the idea that the Fed is going to allow inflation to run hotter than target going forward, with 3% as the new 2%, and the widely mooted rate cuts would simply hasten that outcome. In that scenario, ‘real’ stuff will retain its value better than paper assets and metals are as real as it gets. However, if the Fed is truly going to stay the course and is willing to raise rates further to achieve their 2% goal, that is a very different stance which will support the dollar and paper assets far better.

Of course, none of this really mattered because the most important news yesterday was after the equity market close when Nvidia reported even stronger than expected results and also split their stock 10:1. And, so, all is now right in the universe because…AI!

Alas, this poet is not an equity analyst and has no useful opinion on the merits of the current valuations of AI stocks, so I will continue to focus on the macroeconomic story and try to interpret how things may evolve going forward.

Keeping in mind that the Fed may well be more hawkish than previously thought, that is quite a change in mindset compared to most other central banks where rate cuts appear far more likely as the summer progresses. For instance, yesterday Madame Lagarde explained, “I’m really confident that we have inflation under control. The forecast that we have for next year and the year after that is really getting very, very close to target, if not at target. So, I am confident that we’ve gone to a control phase.” This is her rationale for essentially promising, once again, that the ECB will cut rates next month. However, we continue to get pushback from the ECB hawks that a June cut does not mean a July cut or any other cuts afterwards. Now, I am inclined to believe that while they may skip July, they will cut again in September and probably consistently after that.

Of course, this is a very different stance than what was indicated by the FOMC Minutes, and I expect that there should be a greater divergence between European and US markets going forward because of this. In fact, I am quite surprised that the FX market has not taken this to heart and that the euro remains as well bid as it is. While the single currency has slipped about 2% since the beginning of the year, it is higher this morning by 0.2% and well above the lows seen back in mid-April. Today’s price action has been driven by slightly better than expected Flash PMI data, but the big picture strikes me that there is more room for the euro to fall than rise.

And really, isn’t that the entire discussion overall, relative policy stances by the main central banks? I continue to see that as the key driving force in markets at this time, and the macro data helps inform what those stances are likely to be. If the US growth story is accelerating vs. other G7 countries, then we should expect to see continued outperformance by US assets and the dollar. However, if the rest of the G7 is catching up, perhaps those tables will turn. While PMI data has not been a particularly good indicator lately, the fact that European data (and Japanese data overnight) were slightly better than forecast may be an indication that things are changing. Later this morning we will see the US version (exp 50.0 Manufacturing, 51.3 Services, 51.1 Composite) so it will be interesting to see if the market responds to any surprises there.

As to the rest of the overnight session, markets in Asia were mixed with more gainers (Japan, India, South Korea, Taiwan) than laggards (China, Hong Kong, Australia) with the gainers generally benefitting from somewhat better than expected PMI data and the laggards the opposite. European bourses are mostly higher on the back of that better data as well. As to US futures, at this hour (7:30) Nvidia has pulled the entire complex higher with the NASDAQ (+1.1%) leading the way.

In the bond markets, most major countries have seen essentially zero movement this morning with the UK (-3bps) the one exception as the PMI data there was a touch softer than expected. Of course, you may recall that yields rose sharply in the UK yesterday after the hotter than expected CPI data, so this is a bit of a give-back. JGB yields, interestingly, slipped back 1bp and are now back below 1.00% despite a modestly better than expected PMI reading.

Oil prices (+0.7%) are bouncing slightly after a string of down days and despite slightly larger than expected inventory builds in the US. But for now, it seems clear there is ample supply. And, of course, we already discussed the metals markets.

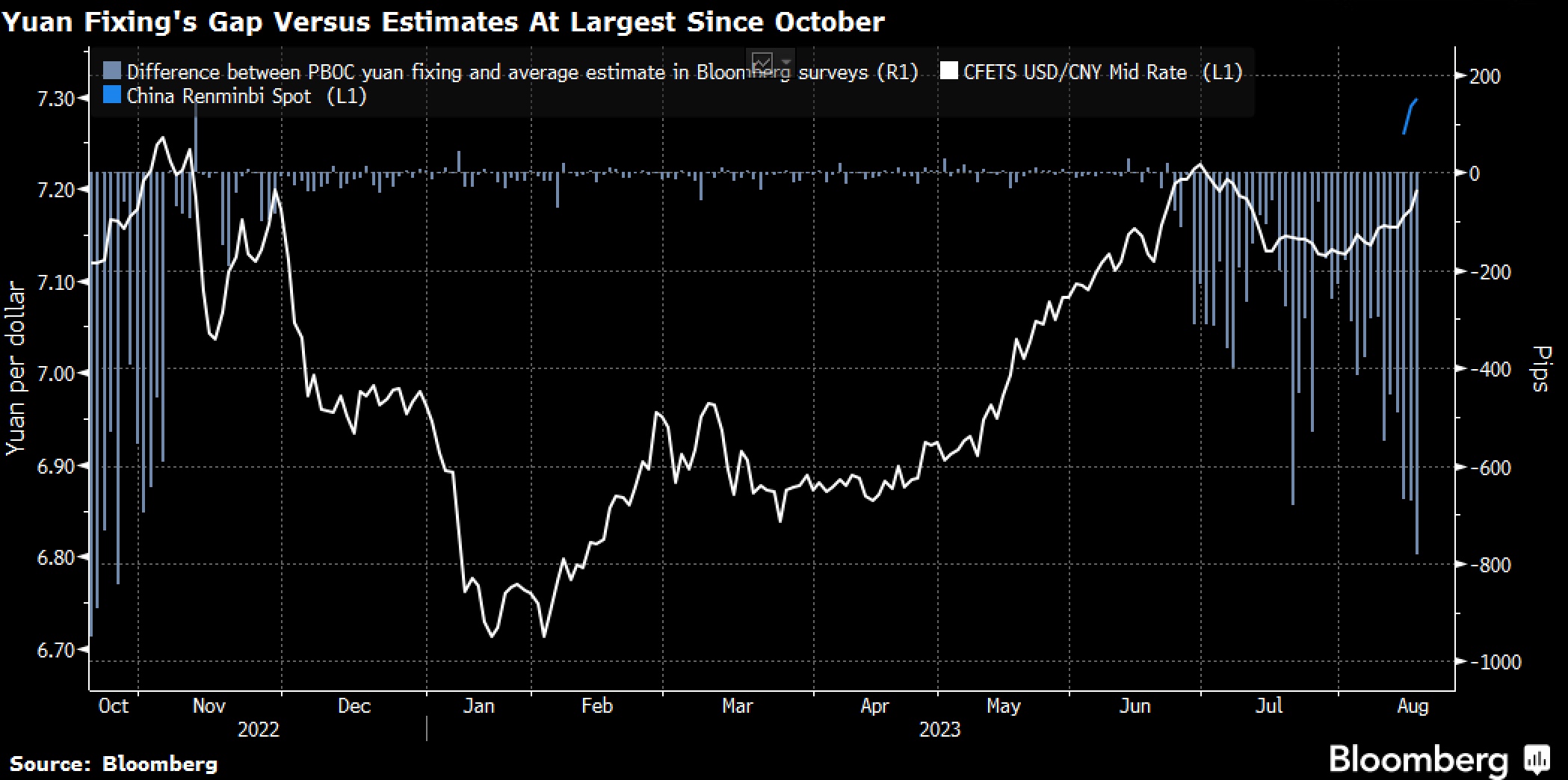

Finally, the dollar is a touch softer overall this morning with most of the movement as you might expect. For instance, NOK (+0.7%) is rallying alongside oil and adding to the dollar’s broad weakness. However, ZAR (-0.5%) remains beholden to the metals complex and is still under pressure. Of minor note is the fact that the CNY fixing last night at 7.1098 was the weakest renminbi fix since January and some are claiming this is a harbinger of the PBOC relaxing its control of the currency. While that may be true, I suspect it will be extremely gradual. And the yen continues to tend weaker, not stronger, as the interest rate differential is too wide for traders and investors to ignore. As well, it is fair to ask if Japan is really concerned about the level of the yen, or if they truly are only concerned with a slow and steady movement.

Before the PMI data, we see Initial (exp 220K) and Continuing (1799K) Claims and the Chicago Fed National Activity Index (0.16). Then, at 10:00 we see New Home Sales (680K) which are following yesterday’s much softer than expected Existing Home Sales data. It seems clear that there is an ongoing problem in the housing market. Finally, this afternoon, Atlanta Fed president Rafael Bostic speaks, and it will be quite interesting to hear his views now in the wake of the Minutes.

While actions speak louder than words, yesterday’s FOMC Minutes certainly have given me pause regarding my view that they were going to ease policy more quickly than inflation data may warrant. That should help support the dollar and keep pressure on risk assets. Of course, given the ongoing euphoria over AI and the Nvidia earnings, I don’t expect equity traders to care much about that at all.

Good luck

Adf