Hormuz is blockaded once more

The latest response in the war

So, crude prices rose

While both sides expose

Their relative views of the score

Now after a month of some peace

Seems tensions are set to increase

So, what about stocks?

The sales are in blocks

While buyers, few bids will release

After a brief respite for markets, where oil had seemed to be drifting out of the headlines, the events of the past weekend plus the US reimposition of the blockade of the Strait of Hormuz has changed the narrative dramatically, and rightly so. The benign attitude of an eventual conclusion to this situation has been tossed aside and the oil bulls and war hawks are both back in the ascendancy. Yesterday ultimately saw oil prices rise 9.4% and this morning they are a further 3.2% higher, and perhaps more importantly, back above the psychological level of $80/bbl.

Source: tradingeconomics.com

There doesn’t seem to be any short-term solution to this situation. There are clearly enough hard-liners still with power in Iran to prevent any move toward a negotiated solution. As long as this maintains, the outlook for oil will tilt higher. However, as I have written before, and is very clear now, the effort to reroute oil shipments from the Gulf nations away from the Strait is intensifying and will continue to do so. As well, alternative sources of supply including additional US production, Brazil, Argentina, Guyana, Venezuela and Canada are satisfying demand. While uncertainty remains high, especially in the short run, by the end of next year, my take is less than 8% – 10% of the world’s oil will need to transit the Strait. However, in the meantime, given that everybody who was long oil as the war initially ramped up has sold out, there are few sellers left to cap the price. I imagine a move toward $90/bbl is quite possible in the next weeks.

As well as the story on crude

Two other themes will be pursued

First CPI’s print

Will offer a hint

Then Warsh will discuss why he’s screwed

If we turn our attention away from the oil market now, the two main events today are the CPI release at 8:30 this morning followed by Chairman Warsh testifying to the House Financial Services committee in his semi-annual trip to Congress. Starting with CPI, expectations are for a decline from last month as headline (exp -0.1% M/M, 3.8% Y/Y) and core (0.2% M/M, 2.8% Y/Y) are due. From what I can tell, there are a number of analysts who are calling for a relatively hotter number, although I’m not sure on what basis they believe that. Certainly, oil prices, and energy prices across the board, declined significantly in June and that will be reflected in the reading. Looking at the home price data, that doesn’t appear to have risen dramatically, and other commodity prices have also slipped. I don’t’ rule out any outcome, but on the surface, expectations seem reasonable.

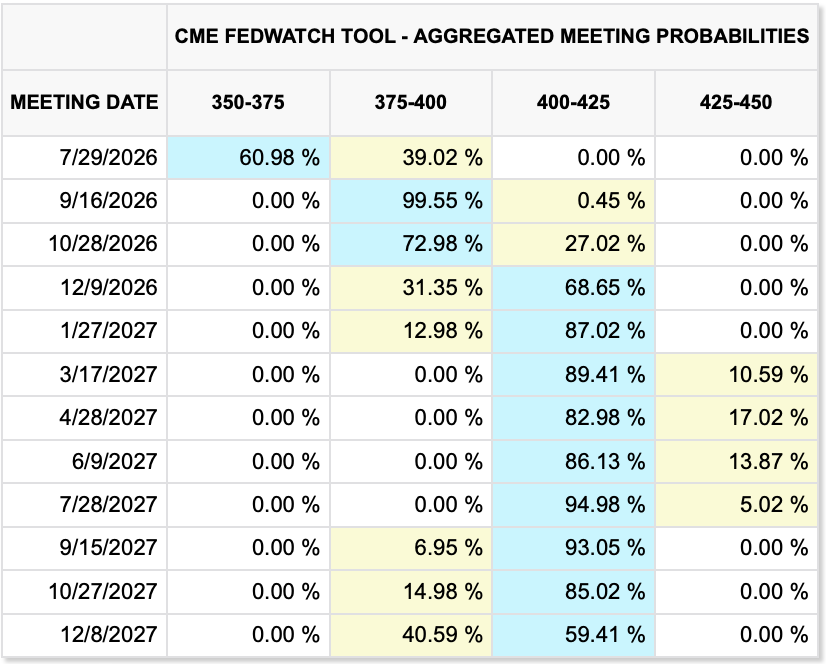

Of course, with oil prices rising, talk of more rate hikes is all the rage and according to the Fed funds futures market, as per the below CME table, you can see that expectations have risen to a 40% probability of a hike this month and a two-thirds probability of two hikes before the end of the year. My personal view, FWIW, remains that there will be no hikes this year, although with the resumption of hostilities in the Gulf, I think a cut is off the table as well. Remember, too, that if oil prices remain elevated that will negatively impact economic activity, so hiking rates into that scenario doesn’t seem to make much sense. But then, I’m not on the FOMC.

Now, I have long maintained that FOMC members should shut up, but it seems Mr Warsh will have a hard time getting them to do so. I’m not sure if they think they are helping, or they are just enamored with their own voices. But yesterday, Governor Waller spoke and explained that if the CPI data was hot, a rate hike would be an appropriate response. And remember, we hear from another 7 or 8 of these folks just this week, four today!

While I expect that Warsh’s testimony will be dry, and that most of the questioning will be either long-winded preening by some idiot member, or an attempt at a gotcha question, I am confident that Chairman Warsh will continue to avoid discussing his views of where policy should go and reiterate forcefully that the Fed’s goal is to reduce inflation, full stop. I am also confident that he will not be dragged into any discussions of other issues like global warming or DEI and simply repeat that ending inflation is the only job he has. We shall all find out shortly.

On to the markets. It should be no surprise that equity markets were under pressure yesterday in the US with the jump in oil prices. This added to the chorus of those who believe the AI bubble is popping as the NASDAQ led the way lower, falling -1.5%. But a funny thing happened in Asia. Despite the jump in oil prices and declines in US equity markets, Tokyo (+0.75%), HK (+0.5%) and China (+2.15%) all rallied nicely last night. In fact, so did Korea (+0.7%) and Malaysia (+1.3%) although we did see declines in India (-0.7%) and Taiwan (-1.4%) with the rest of the region moving far less. This is a surprising outcome to me, especially as Asia is the region most negatively impacted by rising oil prices.

Europe though is trading true to form with declines across the board ranging from Spain (-1.1%) to the UK (-0.4%) and everywhere in between. There has been precious little data overnight to drive things, and this appears to be entirely oil related. Of course, Europe’s suicidal energy policy, notably the UK’s ban on drilling for oil in the North Sea, remains one of the key reasons that the area will continue to struggle. As to US futures, this morning DJIA futures are lower (-0.8%) but the other two major markets are little changed at this hour (7:25).

In the bond market, 10-year Treasury yields jumped 6bps yesterday although are little changed this morning. However, as you can see from the chart below, they are pushing back up toward the highs seen in late May.

Source: tradingeconomics.com

There is a lot of talk about how Warsh should hike rates aggressively this month to gain bond market credibility in his fight against inflation, but I sense that is a lot of people talking their books. I continue to believe that there will be no Fed action ahead of task force reports. As to other nations, yields are generally firmer in Europe today, ranging between +1bp (Germany) and +3bps (Italy) with the UK worst of all (+4bps) as 10-year Gilts now yield more than 5.0% again, also pushing back to late-May highs. The one exception is Japan (JGBs -5bps) where the latest ploy by Katayama-san is to propose JGBs be allowed to be invested in tax-free accounts for individuals in Japan. Given the long history of zero rates there, a tax-free return of 2.7% with no currency risk could well be quite attractive, I think.

In the metals markets, it is no surprise that both gold and silver fell yesterday with the jump in oil prices, but despite oil’s continued rally this morning, both gold (+0.7%) and silver (+0.7%) are finding support, with gold seeming to hold the $4000/oz level for now. Copper (+1.6%) is also holding up well, but its relation to the precious sector seems to be waning. Perhaps the precious metals story is less about oil and more about the dollar.

Turning to the dollar, yesterday it put in a strong performance with the DXY rallying about 0.3% from Friday’s closing levels as you can see in the chart below.

Source: tradingeconomics.com

However, as you can also see in the chart, this morning the greenback is under pressure despite the rise in oil prices and yesterday’s increase in yields. The biggest outlier is NZD (+0.9%) as the RBNZ continues to make hawkish statements about the need for further rate hikes. And of course, NOK (+0.7%) is benefitting from the oil price rise. But the rest of the G10 are all firmer, and so is most of the EMG bloc with only INR (-0.5%) standing out as underperforming. That story appears to be based on higher oil prices and concerns, or thoughts at least, that the RBI will not be aggressively hiking rates to protect the rupee. Otherwise, most currencies have moved higher vs. the dollar on the order of +0.15% to +0.25%.

And that’s really it today with CPI the only data release other than the already released NFIB Small Business Optimism index (97.4, exp 95.8), but that predates the change in the Gulf. Chairman Warsh has his work cut out for him to get his colleagues to shut up. I wonder if he can fine them if they speak.

We are in a narrative transition right now, but longer term, I remain bullish the US and the dollar.

Good luck

Adf