The Techquity rally has stumbled

Though oil has once again crumbled

But pundits don’t care

As they’ll still declare

They’re right. They can never be humbled

Some days are simply less interesting than others, and based on the number of new stories, it seems today is falling into that category. That’s not to say that some markets haven’t moved, there has been some significant movement, it’s just that the movement is based on the same rehashed story lines we’ve heard for the past several weeks.

For instance, the below chart of the NASDAQ, with daily candles, shows just how choppy the tech sector has been this month.

Source: tradingeconomics.com

For the market technicians, if you are inherently bearish, this will read as a double top and the next leg is lower, targeting something with a 26000 handle. However, if you are bullish, you will make the case that this is the end of the “c” wave and we are ready to break to new highs above 31000.

That’s the thing about market technicals, they remain in the eye of the beholder. If you ask about new news, arguably the Micron Technology earnings were the biggest story of the week, but despite a tremendous outcome, tech stocks could not hold any early gains. The flipside is that OpenAI has postponed their IPO until next year, a clear sign that they are concerned with sufficient investor capacity. Again, spin it as you see fit, since there is no right or wrong here, but there are conflicting sentiments.

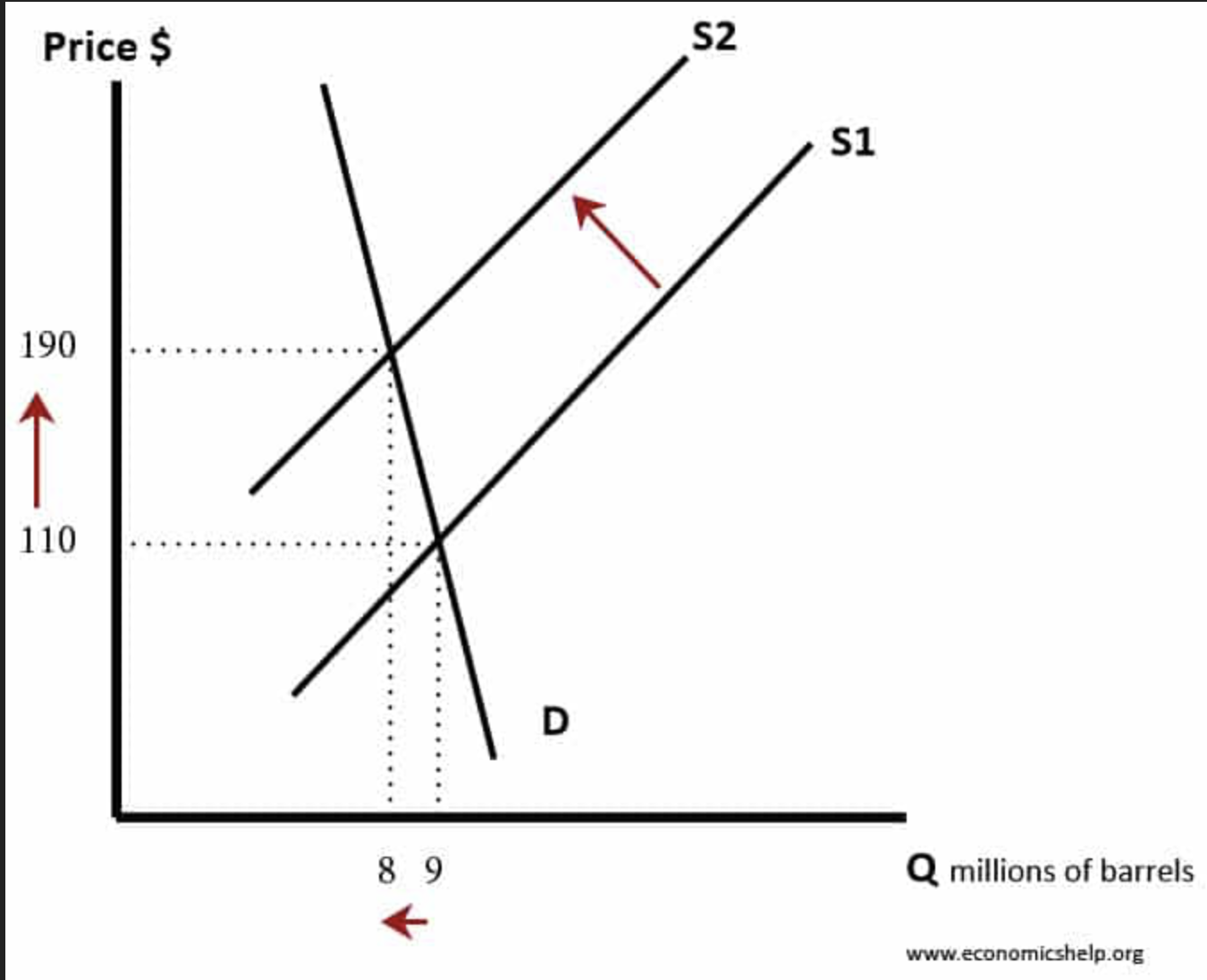

My point is that while there have been headlines, there hasn’t been any news. Or consider oil (-3.1% this morning), which as you can see from the chart below has fallen back to prewar levels.

Source: tradingeconomics.com

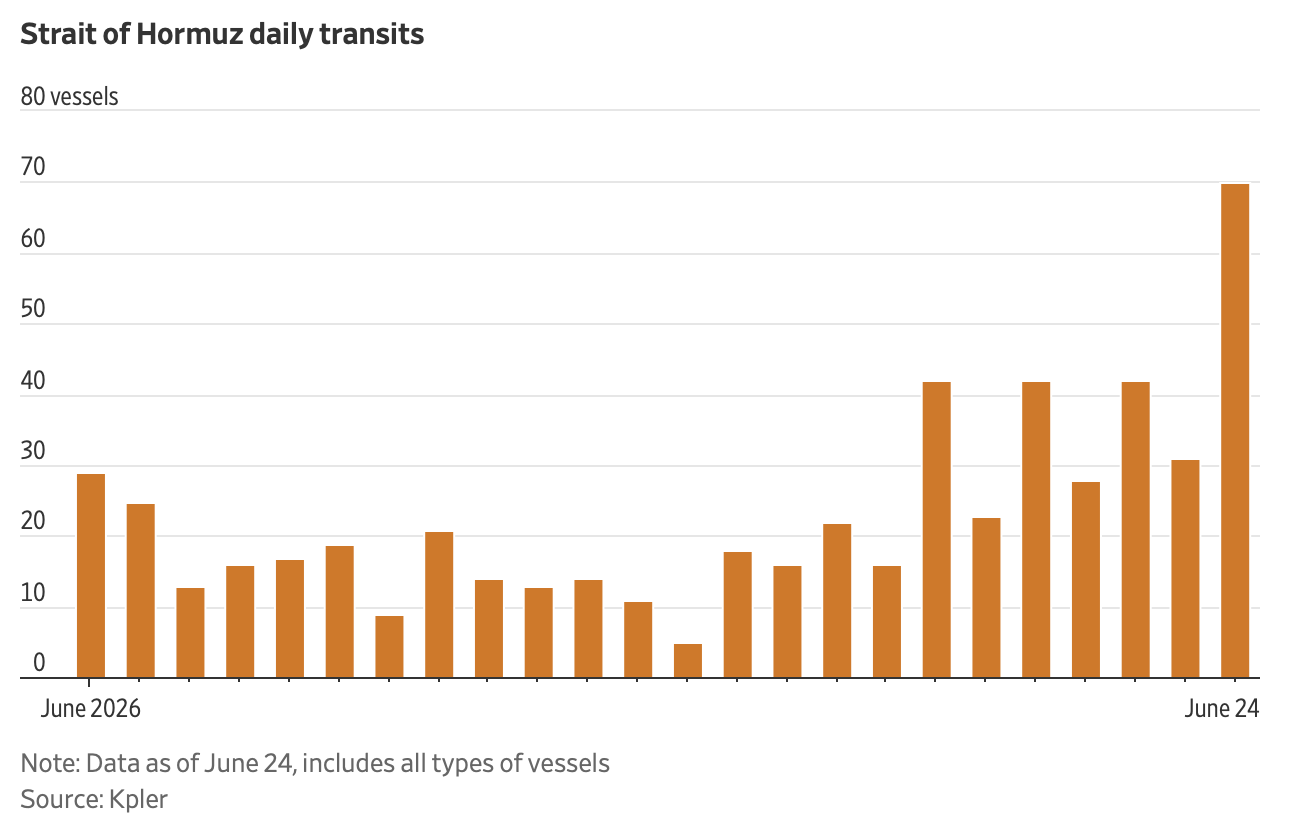

Yes, there was an incident with some freighter being hit by an unidentified object in the SOH, and that jangled a few nerves yesterday, but apparently fully laden VLCCs carrying 2mm barrels of oil, are fleeing the Gulf in ever larger numbers. I read that 78 ships transited yesterday and as you can see from the chart below from the WSJ this morning, the trend is higher.

All of the stories about tank bottoms and a sudden spike higher in the price of oil continue to be nothing more than fear porn. As Alyosha from Market Vibes notes, the likely reason for less inventory is the oil companies are expecting a huge influx of oil from the Gulf and they need some place to put it. Again, these are warmed over stories and not new news.

By all accounts, we are continuing along the recent path where oil prices continue to normalize while other markets search for the next big thing. For stocks, the AI debate continues to rage on as to its impact on the future, while resource companies continue to be seen as a place to hang out given the needs of the economy as it grows, and that is a global comment. For bonds, is inflation fading or persistent and setting to move higher? The recent view is fading, but obviously that is subject to change. And the dollar? It’s had a nice rally, but is it about to break to much higher levels or reverse course? Over time I see it higher, but for now, not so much.

Ok, let’s review the overnight session. Tech stocks in Asia had a rough go of it, reversing yesterday’s gains as Japan (-4.15%), China (-3.0%), HK (-1.8%), Taiwan (-3.6%) and Korea (-5.8%) all reversed yesterday’s rallies. The below chart from finance.Yahoo.com of the KOSPI gives an excellent sense for the magnitude of the moves this week.

Elsewhere in the region, there was far more red than green, but those were the standouts. In Europe, everything is lower this morning as well, with Germany (-1.2%) the laggard, although there is no news that would lead you to believe things are worse there than in the UK (-0.8%), France (-0.7%) or Spain (-0.4%). It’s a soft day. US futures are on this same path with NASDAQ (-1.2%) leading the way lower.

In the bond market, yields are little changed to slightly softer this morning with Treasuries (-2bps) actually leading while European sovereign yields have edged lower by -1bp across the board. Interestingly, JGB yields (-3bps) are slipping and some pundits are making the case we have seen the highs in 10-year JGBs, at least for quite a while. Certainly, looking at the chart below, the case that the uptrend has been broken is viable. Last night, Tokyo CPI data was released there at 1.6%, as expected and well below the 2.0% target. Is it possible that inflation pressure there is abating as well?

Source: tradingeconomics.com

In the metals markets, it appears that the rout is on hold, at least for now, as gold (+0.5%), silver (+0.7%) and copper (+0.6%) all seem to have found recent support with gold holding the $4000/oz level and copper the $6.00/lb level. We saw a massive bubble in these that has deflated, but real demand remains in place. China continues to hoover up gold, and the electrification narrative has not disappeared, nor the data center one, both of which require massive amounts of copper.

Finally, the dollar is softer this morning, slipping somewhere between -0.1% and -0.3% vs. almost all its counterparts. NOK (-0.4%) is an outlier as oil slides but otherwise, it is hard to get excited here at all. JPY did not make another new low last night, so it has that going for it.

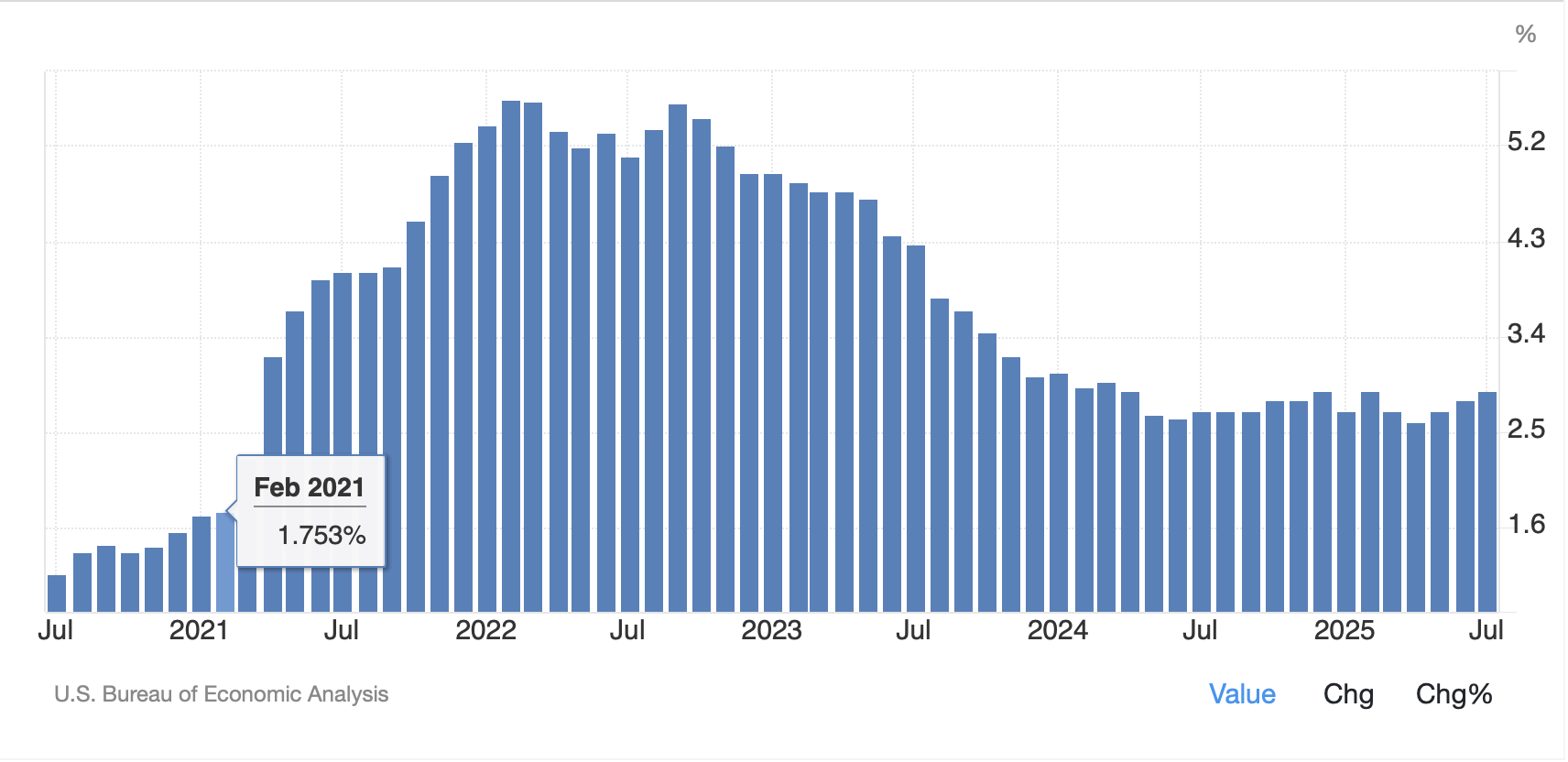

On the data front, this morning brings the Goods Trade Balance (exp -$85.0B) and then Michigan Sentiment (50.0). Yesterday’s PCE data is a perfect example of the narrative, and how there is a real attempt to write a story from nothing. While GDP rose more than expected, as did Personal Income and Spending, the PCE data was right on expectations, or even a tick low in the headline monthly number. So, this was clearly priced into markets. Yet virtually every headline I saw was how these were the highest prints since 2023, which as you can see in the chart below, is absolutely true, but hardly newsworthy. But it makes for good headlines if you are trying to tell a story of rampant inflation.

Source: tradingeconomics.com

At any rate, that’s all I’ve got today. My take is oil is still heading lower although Techquity prices just might follow for now. However, I’m not in the collapse camp there. And the dollar? Softer for a bit, but I have a feeling all we’ve done is widen the range, not really broken out.

Good luck and good weekend

Adf