A line has been drawn

Is it steel reinforced? Or

Just dust in the wind?

Shortly after 9:30 yesterday morning, the BOJ entered the FX market aggressively selling dollars as you can see in the chart below. While the amount sold is unknown at this time, it was likely pretty large, ~$10 billion – $15 billion would be my guess. In addition to the sales, though, apparently the Fed called around the Street “checking rates”, although my understanding is the Treasury didn’t actually sell any dollars.

Source: tradingeconomics.com

Regardless, the signal of an approved, if not joint, intervention is powerful and I expect that the market will take some time before pushing the dollar back higher again. Now, one of the themes yesterday was that the BOJ would also raise interest rates at their meeting last night in a surprise move as a way to reinforce this action. I believe if they had done so, it could have been quite effective and we would have seen another sharp leg lower, as well as an overall reduction in pressure on the yen. But they did nothing with their base rate remaining at 1.0% and, as you can see from the chart, the drift has already begun for the yen to weaken once more.

As I have maintained throughout this process, absent policy changes of substance, and at this point in Japan that includes fiscal as well as monetary, pressure on the yen is very likely going to be the norm. Of course, if the Fed really does begin to ease policy at some point, that will alter opinions and I imagine soften the dollar universally.

The pundits are still really pissed

That Warsh, their concerns, has dismissed

Get ready to hear

That Doomsday is near

If Warsh keeps ignoring their gist

Since we seem to be in an interlude in the war in Iran and the Middle East, so oil markets remain quiet and there has been little news from the White House, the punditry has continued its focus on Fed Chair Warsh and all the things they hate that he is doing. This is well summed up in this morning’s WSJ article titled, ”Kevin Warsh’s Honeymoon with the Bond Market Is Already Over” interestingly, this was not written by Nick Timiraos, but rather by Sam Goldfarb, their bond market guy. Personally, I think he is completely wrong, but the punditry is consistent in their desperate desire for Warsh to tell them what the Fed is going to do so they can report it and seem smart.

However, my read on the bond market response is quite different, especially when put in context with other markets, notably inflation markets. The fact that the 2-year yield has backed off, and we have already seen a modest pull-back in the 10-year tells me that there is limited fear of rampant inflation. While the pundits, and many other central bankers (see Lagarde, Christine) think that hiking rates into an energy price shock is the right move, it has historically been a key policy error. And what we have learned from financial history is that it is NEVER different this time. And the folks who trade inflation have breakevens (the difference between nominal Treasury yields and TIPS yields of the same maturity) trading at very ordinary levels of 2.27% in the 10-year and 2.22% in the 30-year. I thought that Alexandru Stefan Goghiedid an excellent job of describing the situation in his Substack article this morning.

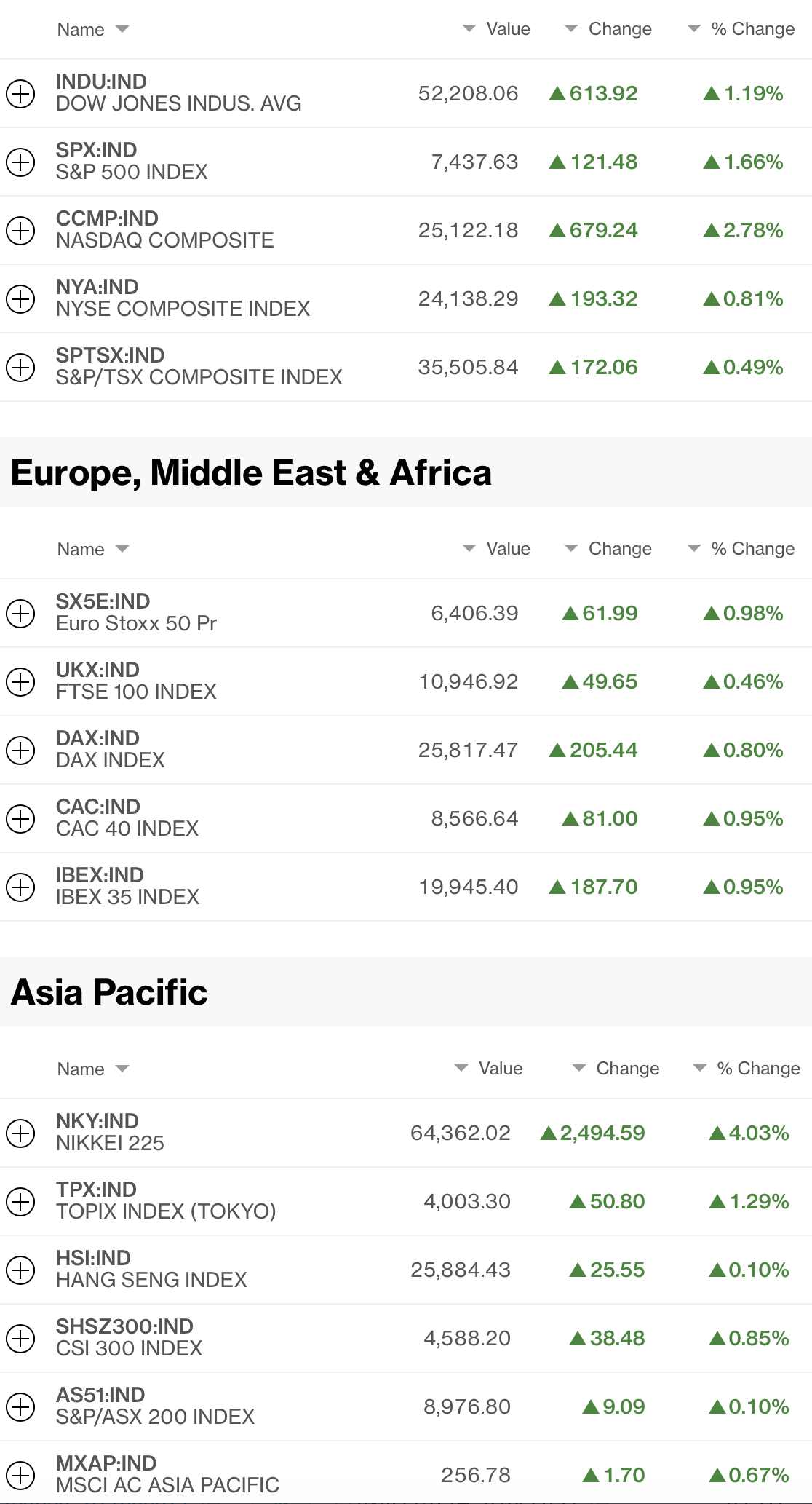

In the meantime, you know who else isn’t really worried about this? Equity investors. Broadly speaking, green is today’s color in that asset class, with some of the real movers not even shown in this Bloomberg Screenshot.

For instance, the KOSPI rallied 17.9% last night after Amazon and Microsoft’s earnings got everybody reconvinced that the AI trade was not over. This is the market that I had been highlighting as collapsing and it just did a major reversal. Last night’s candle, on the right-hand side of the chart, is one of the largest you will ever see in a major equity market!

Source: finance.yahoo.com

So, we have made it through the major tech earnings releases and spirits are still high. While the Fed funds futures markets are still pricing a two-thirds probability of a hike in September and the certainty of one by October, the recent cooler than expected CPI and PCE data will continue to give ammunition to remain on hold. To me the real question is, will Chairman Warsh be able to convince the committee that reducing the balance sheet is the right thing to do (it is) as that will have a much stronger impact on inflation than raising rates into the energy price shock.

In an aside, lately I have been wondering if every Fed governor should be fired for ‘cause’. After all, according to legal precedent, cause can mean:

- Inefficiency – persistent inability or incompetence in performing the role’s administrative or official functions

- Neglect of duty

- Malfeasance in office

Now, I would not accuse them of the latter two, but let’s face it, they have completely failed in their official functions as evidence by the fact that even on their own terms of stable prices, it has been more than 5 years since they have achieved their goal. That seems pretty inefficient or incompetent to me!

Ok, let’s run through the other markets. Bond yields are higher by 1 tick around the world, and we have discussed them already. JGB yields, have slipped -2bps, so maybe they are not as worried with the yen strength from yesterday.

Commodity markets are dull with oil (+1.5%) having rallied in the past hour but still hanging around the $85/bbl level with no new news on the war. At the same time both gold (-1.2%) and silver (-2.0%) are under pressure this morning, although that doesn’t make a huge amount of sense to me given the dollar’s broad weakness. Perhaps the fact that it is month end is driving flows there, but I am not close enough to those markets to know.

Finally, the dollar is softer, having fallen sharply yesterday although bouncing somewhat this morning. As you can see in the DXY chart below, we are back within the 96.50/100.50 range that has prevailed for most of the past year and have traded below 100.00 several times yesterday and early this morning.

Source: tradingeconomics.com

To me, this is very interesting as FX traders seem to be taking different signals from the Fed than the short-term interest rate guys. This does not feel like a market that is anticipating rate hikes in the US. Now, historically, when it comes to opinion differences across markets, FX traders are the worst of the worst. And, of course, I am an FX guy at heart, but I have a feeling they are correct here and I still see no rate hikes this year despite the Fed funds futures markets relative certainty. So, right now, the dollar is broadly firmer by 0.3% across the board with the biggest outlier KRW (-1.35%) seeming to follow the KOSPI.

I think the really important thing to remember here is that the dollar has just not done very much, at least against the G10 currencies, for more than a year. Certainly, LATAM currencies have performed well this year, but it remains difficult for me to look at the rest of the G10, a group with weak economic activity, and get excited about owning any of them.

On the data front, the PCE data was as expected to softer, but the real key yesterday was the GDP data which showed nominal GDP rose 7.9%, although the inflation adjusted number was just 1.5%. But this is the very essence of running it hot, high nominal growth, which consisted of significant consumption and investment, while allowing inflation to run as well. From a debt management perspective for the US, the debt/GDP ratio fell accordingly by about 1%. While this trend remains higher, I expect we will see more of this type of outcome going forward.

As to today’s releases, Chicago PMI (ep 56.0) and Michigan Sentiment (54.0) are what we see, neither of which seems likely to matter to markets. The equity bulls are back and that is going to be today’s story. If those rallies fail, it will portend larger problems I believe, but my take is that is not going to happen. I guess we shall see.

Good luck and good weekend

Adf