This evening the president speaks

And pundits have many critiques

Meanwhile in Iran

There’s no clear game plan

As havoc, the president wreaks

But right now, seems traders don’t care

‘Bout Persia or any warfare

Instead, soft inflation

Has changed the narration

So, pundits, high rates now foreswear

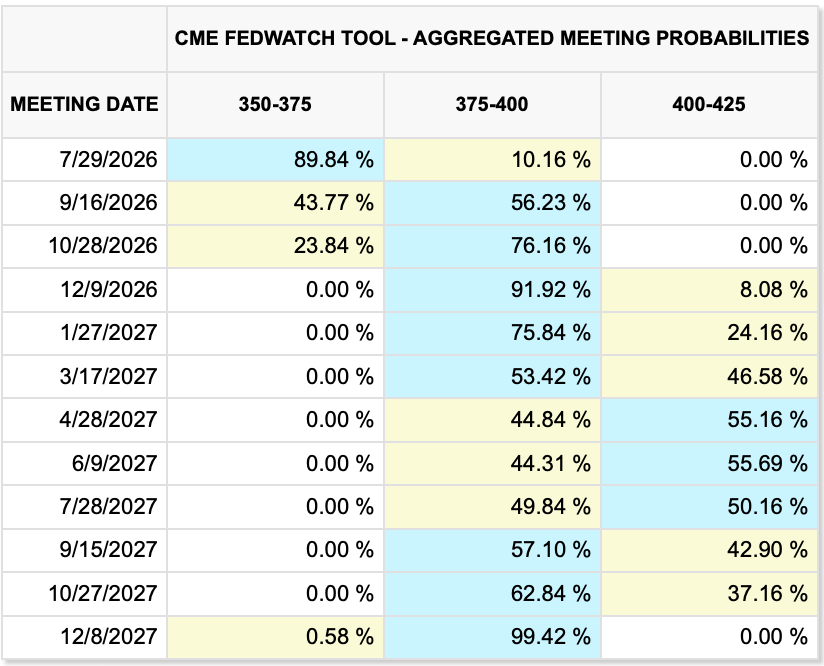

Some days, it’s simply more difficult to find stories that bring coherence to the narrative. But let me try. Yesterday’s PPI data was also much cooler than forecast, although still clearly quite high on a year over year basis, but it certainly added to Tuesday’s CPI result and has changed a lot of views regarding the Fed’s future actions. For instance, if we look at my favorite CME table for current probabilities of future rate moves, we see that there is now just a 10% probability of a hike in two weeks’ time, and just one hike priced in for the next 18 months.

Remember, Monday, there was a 40% probability of a hike priced for the July meeting and two+ hikes priced through 2027. (As I recall, I was an advocate of fading that price action.) I expect that this will alter the narrative as calls for an immediate rate hike to burnish Warsh’s, and the Fed’s, credibility are likely to fade away. In the meantime, he didn’t say anything new at the Senate testimony and the rest of the Fed talking heads continue to reiterate that they would be comfortable raising rates if inflation pressures rise. Remarkably, they didn’t seem to notice the recent numbers.

Turning to the Strait of Hormuz, the US blockade of Iranian vessels is back in force and there have been a significant number of new US attacks on Iranian military sites. As well, the IRGC has fired drones/missiles at several tankers trying to exit the Strait on the Omani side. I read this morning that the president is considering whether to escalate things by attacking Kharg or Qeshm Islands, two key Iranian strongholds, and my guess is if that were to be the case, the oil market would likely take a turn higher. But right now, WTI is effectively unchanged on the day, and has been since Monday’s rise. I guess $80/bbl +/- is the new home.

Source: tradingeconomics.com

As to the President’s speech tonight, the word is it is going to involve election related issues, seemingly regarding the integrity of elections, the SAVE Act and the results of the 2020 elections. Recall, Tulsi Gabbard, before she resigned to care for her husband, declassified a great deal of information and some portion apparently was election related. Alas, this will simply further stoke partisan feelings as there is very little evidence that showing proof of something political has the ability to change the opposing viewpoints of partisans.

So, away from oil, we are now into earnings season, and the big banks all had monster quarters while there is growing angst over the AI sector and whether the main players will be able to make the money that was assumed for so long. So, while yesterday saw US indices trade higher, the overnight session has been far less positive.

Starting in Asia, Tokyo (-2.8%), China (-1.9%) and Korea (-6.4%) all felt the pain of semiconductor weakness although HK (+1.3%) bucked the trend with most of the rest of the region showing far less movement in either direction. There was precious little data to drive things, so this clearly seemed to be tech sector woes. In Europe, broad, but modest, weakness is today’s theme with both France and Germany lower by -0.65% with Spain (-0.5%) also under pressure and the UK (-0.3%) the best of the bunch after GDP data was mildly better than the last reading at 1.3% Y/Y in May. While the Trade Balance improved a bit, IP was weak and although it has been spun as a positive report, it hardly quickens the pulse. Meanwhile, at 7:20 this morning, NASDAQ futures are lower by -1.1% although the other two major indices are little changed. Tech is definitely under pressure here.

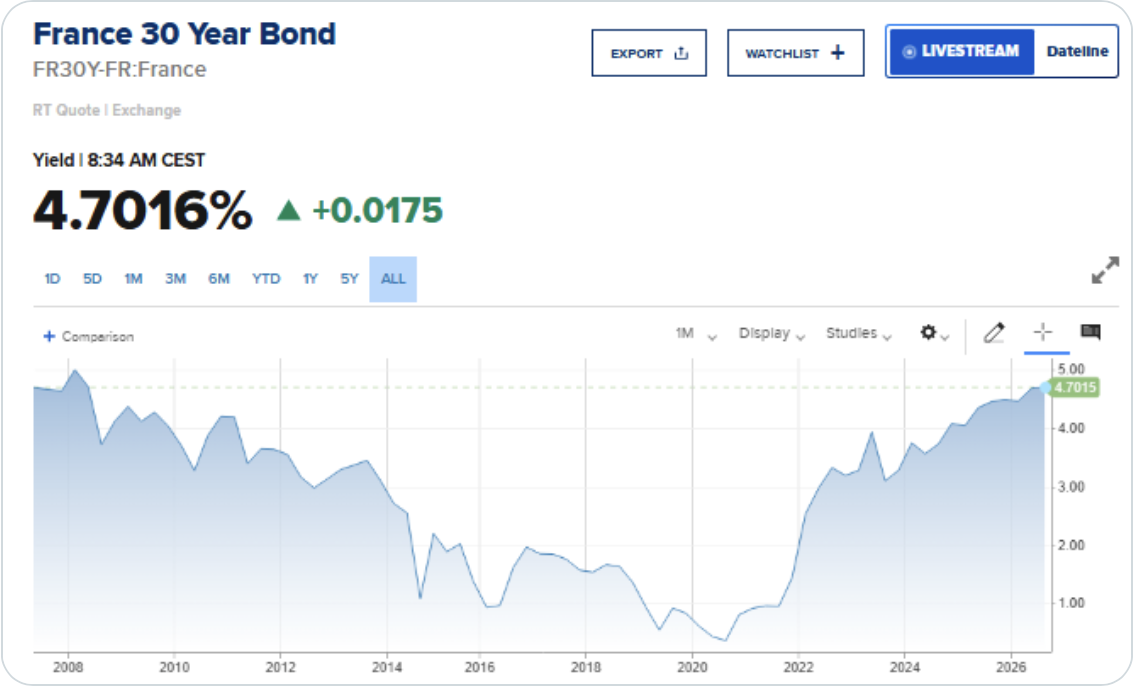

In the bond market, this morning we are seeing yields higher by basically 2bps across the board in Treasuries and European sovereigns. Much is being made of the French OAT 30-year yield this morning as it trades to its highest level since the GFC as per the below from barchart.com.

While this headline of the highest rate in X years is splashy, what we have been seeing consistently, across all nations, is that debt issuance continues to rise and central banks have not been absorbing nearly as much as they had in the more recent past. This means that the private sector needs to buy bonds, and they are demanding higher yields. Someone made the point (and I cannot remember where I first read it, but it is valid) that bond yields appear to be less about inflation concerns, per se, and more about the ability for markets to absorb the ever-increasing amount of debt being issued by governments…and companies. Just look at how much debt is being issued by the hyperscalers to fund their AI buildout. Regardless of what happens to the front end of the curve and central bank rate activities, it does feel like the back end of the curve is where the signal is going to be found going forward.

Precious metals continue to bat about, rallying and then giving those gains back, but net remain under pressure as gold (-0.75%) and silver (-1.9%) are both softer this morning although copper (+0.7%) continues to find support. It is difficult to look at the gold chart and be optimistic about a reversal of fortune in the near-term.

Source: tradingeconomics.com

However, as per the discussion above regarding the increasing issuance of government debt around the world, at some point, the larger fiat vs. physical stores of value question is going to reassert itself and gold will be one of the main beneficiaries of that story. Alas, it has a history of doing nothing from a price perspective for years on end.

Finally, the dollar, which suffered yesterday, with the DXY slipping -0.5%, is not very interesting this morning. the pound, interestingly, has slipped -0.3% despite what many are trying to spin as a positive GDP report. The other noteworthy mover is KRW (+0.4%) on the back of the BOK raising interest rates by 25bps to 2.75% last night. While this was widely expected, the rhetoric about faster growth driving the need for higher rates has been a boon to the won. (And remember, this was despite the KOSPI getting crushed last night on weakness in the two big semiconductor firms.)

On the data front, this morning brings the weekly Initial (exp 217K) and Continuing (1820K) Claims as well as Retail Sales (0.2%, -0.1% ex autos) and the Philly Fed (13.0). With the recent surprises in CPI and PPI, I’m sure there will be a lot of focus on this morning’s Retail Sales data. Certainly, a weak number will feed into the new, growing narrative, that the economy is slowing and rate hikes are slipping from view. But yesterday’s Empire Mfg number was quite strong. There are still many inconsistencies in the data, which if nothing else, allows every analyst to point to something and claim they are right.

Ultimately, to me the great concern is an escalation of US activity in Iran, especially bringing troops into play. In that case, I think things would change a lot, and we could well see another jump in oil prices. But absent that, right now there is a lot of noise, but not much signal. I don’t think the big picture has changed, i.e. investment into the US remains strong and that is going to support both the economy and the dollar. But there will be many twists and turns.

Good luck

Adf