The ceasefire seemed to be crumbling

And stocks all around started tumbling

Then late in the morning

Trump issued a warning

To Bibi that clearly was humbling

So, Lebanese fighting decreased

Though, so far, it has not yet ceased

The door’s now ajar

For peace near Qatar

Thus, risk appetite rose like yeast

Which takes us to data today

With March CPI on the way

It surely will show

That prices did grow

But how long will increases stay?

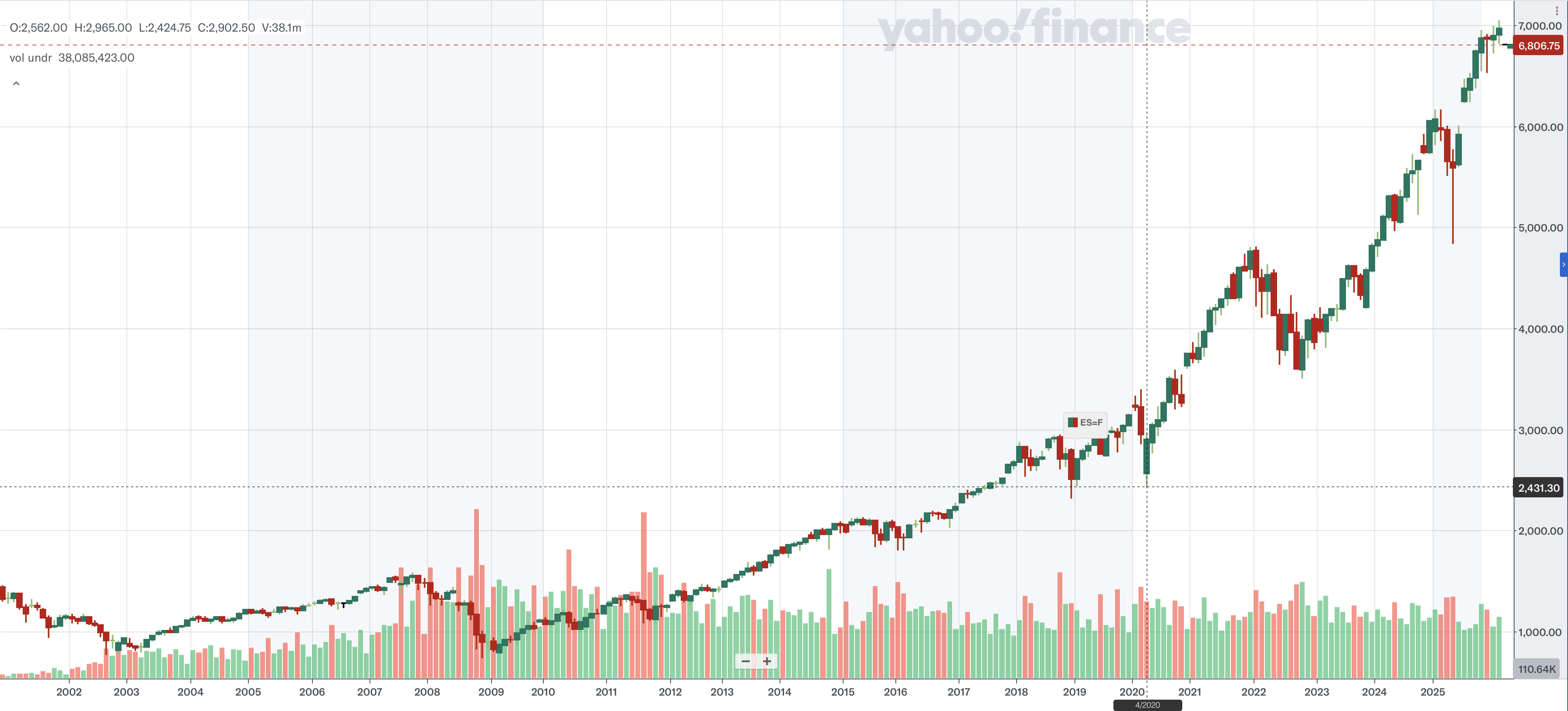

As you can see from the below chart showing oil (inverted) and the S&P 500, about 11:00 yesterday morning, the news hit that Israel was going to stop its ongoing fighting against Hezbollah in Lebanon, which the Iranians claimed was a violation of the ceasefire and had undermined general, and market, belief that the ceasefire would hold at all. The impact was instant with a substantial rally in the S&P, 1% within an hour, while oil prices tumbled about 6% in the same span (given oil’s volatility is so much higher, that discrepancy is not surprising at all.)

Source: tradingeconomics.com

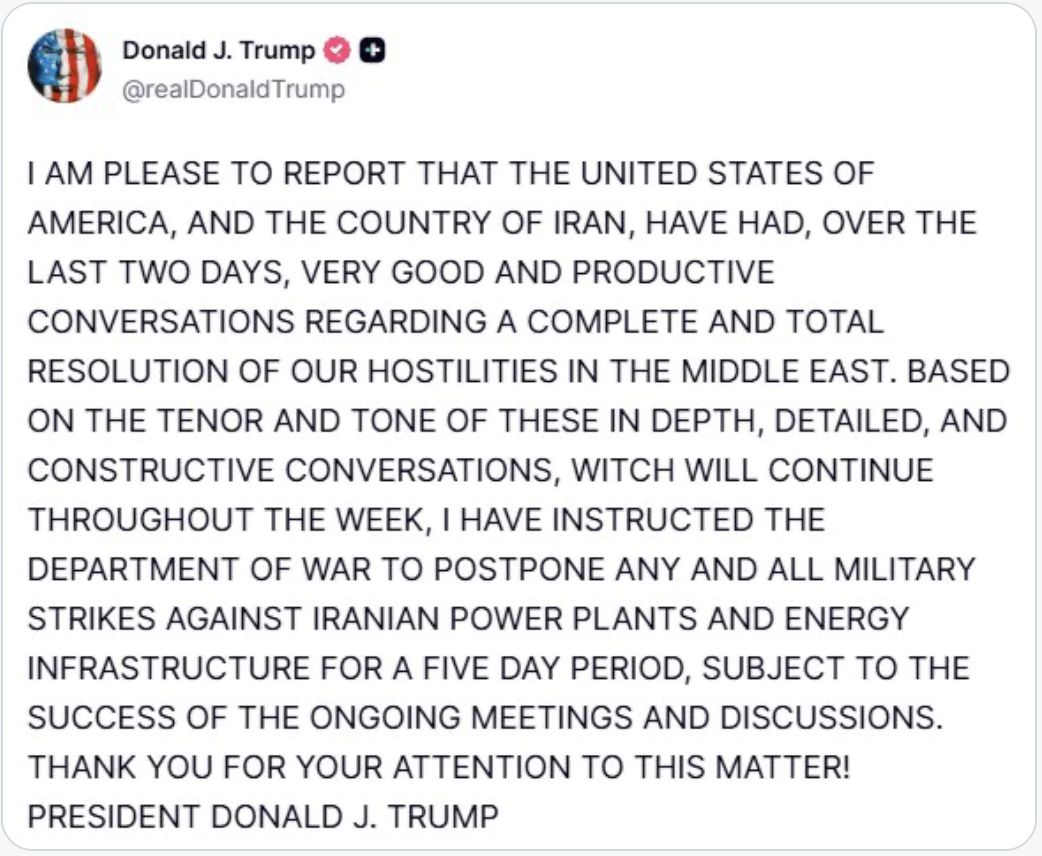

This is the lead-in to the first face-to-face talks between the US and Iran that are due to occur today in Karachi, Pakistan. Hopefully, they will lead to a lasting peace with the upshot that Iran will no longer be a sponsor of terrorism, but I must admit, I’m not holding my breath for that outcome. The overnight market reaction was pretty much exactly what you would have expected with a generally positive view of risk almost everywhere in the world. Obviously, if the talks lead to a peace and a reopening of the Strait of Hormuz, the strong belief is that things will eventually revert to the prewar stance, at least from an energy and economic perspective. We shall see.

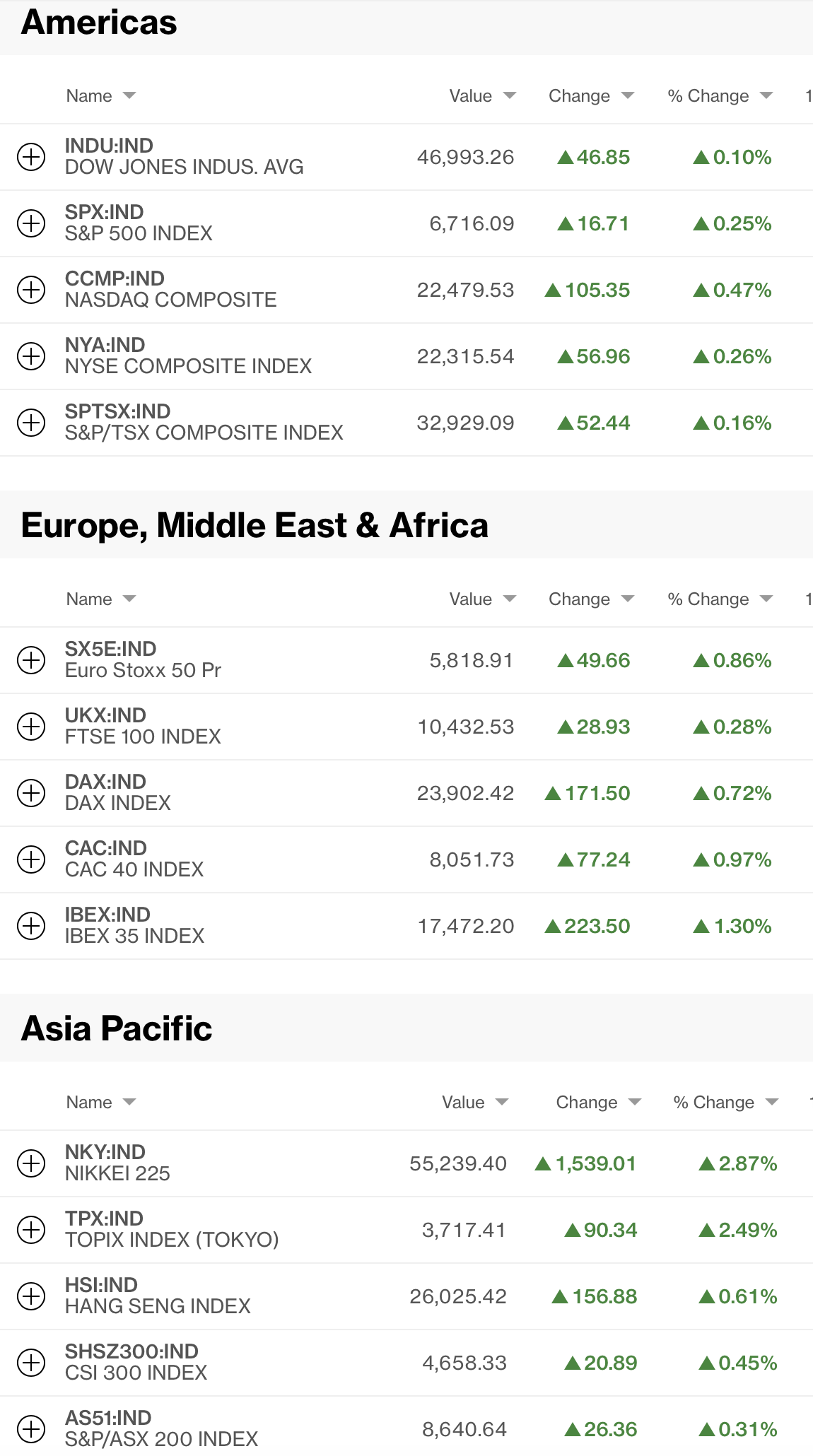

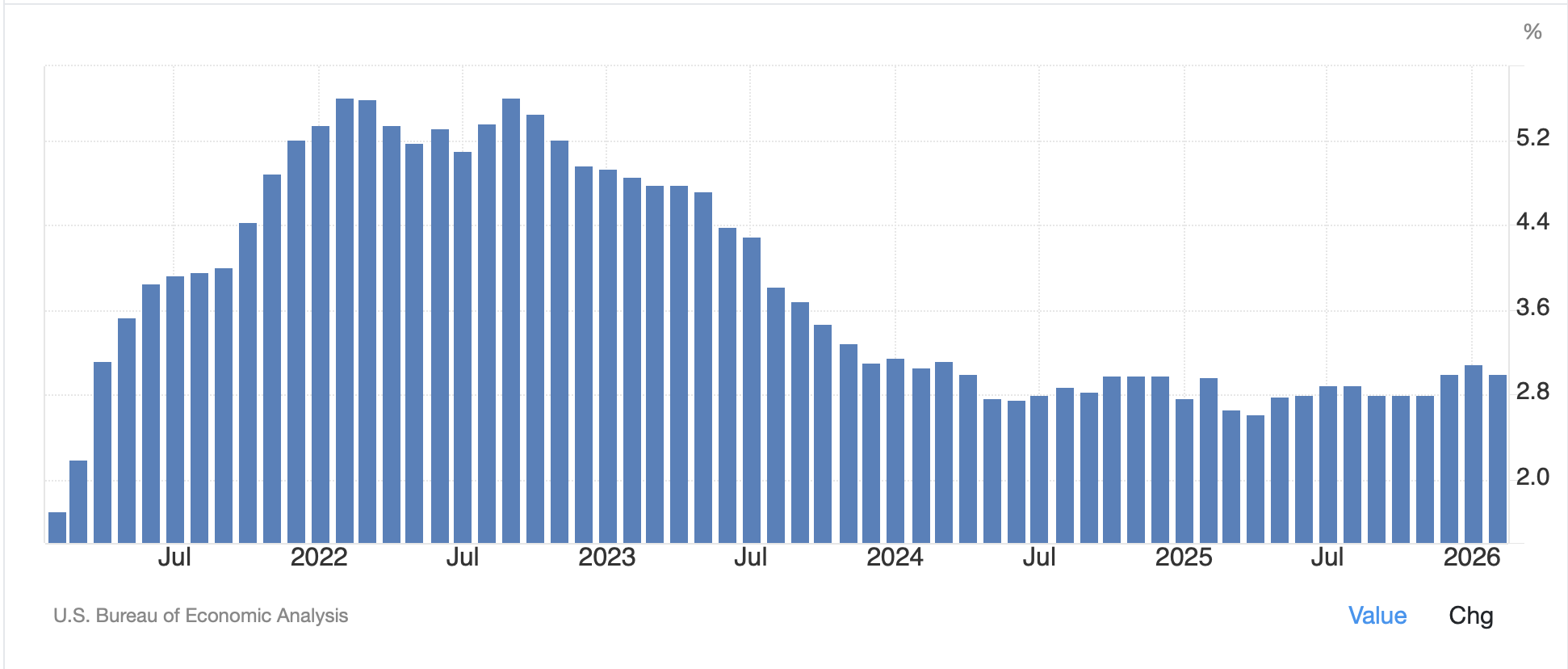

Which takes us to the other piece of news that markets are going to need to absorb this morning, the March CPI data. Yesterday we saw the February PCE data and while it was released at expected levels, those levels (2.8% Headline, 3.0% Core) are already far above the Fed’s 2.0% target. In fact, as you can see from the chart below, it has been a full five years since Core PCE was at or below their target.

Source: tradingeconomics.com

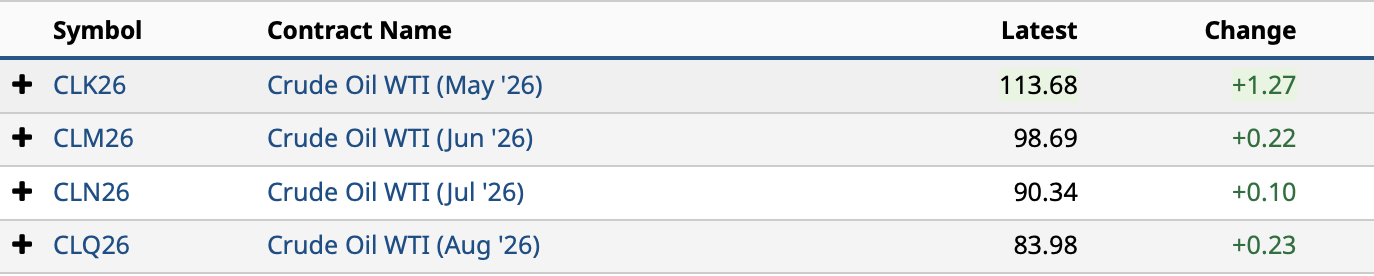

And now, we get March CPI this morning which will include a substantial rise in oil prices as the average in February was $64.51/bbl vs. March’s $93.58/bbl. Obviously, that is going to have a major impact on headline CPI, but the question is just how much of an impact will it have on core? Expectations are for Headline to rise 0.9% M/M and 3.3% Y/Y, while the Core rises just 0.3% M/M and 2.7% Y/Y. Now, we are coming halfway through April and oil prices have not retreated yet, so we are likely going to see continued upward pressure on core prices going forward as those high oil prices feed their way into other things. But that is for the future. For today, all eyes are on the data to see if it will be enough to concern central bankers.

In fact, next week is World Bank / IMF week in Washington DC and Kristalina Georgieva, the IMF’s Managing Director, expressed concern that the global economy is going to slow down because of the impact of higher oil prices, but implored central bankers around the world to be patient and not hike rates right away, while asking governments not to subsidize fuels and increase demand. It is, of course, much easier for her to make these comments as she doesn’t face an electorate that is angry about rising prices.

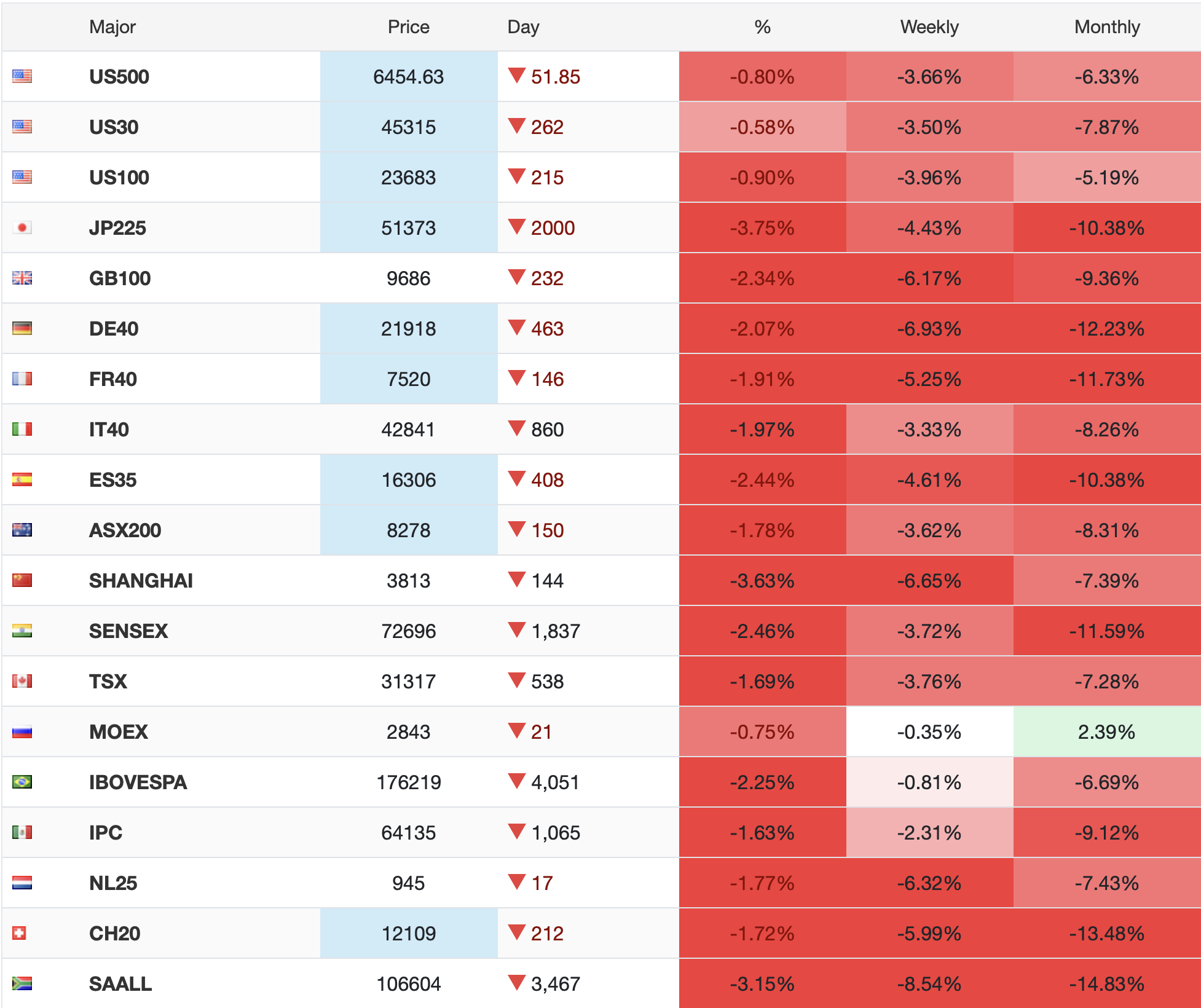

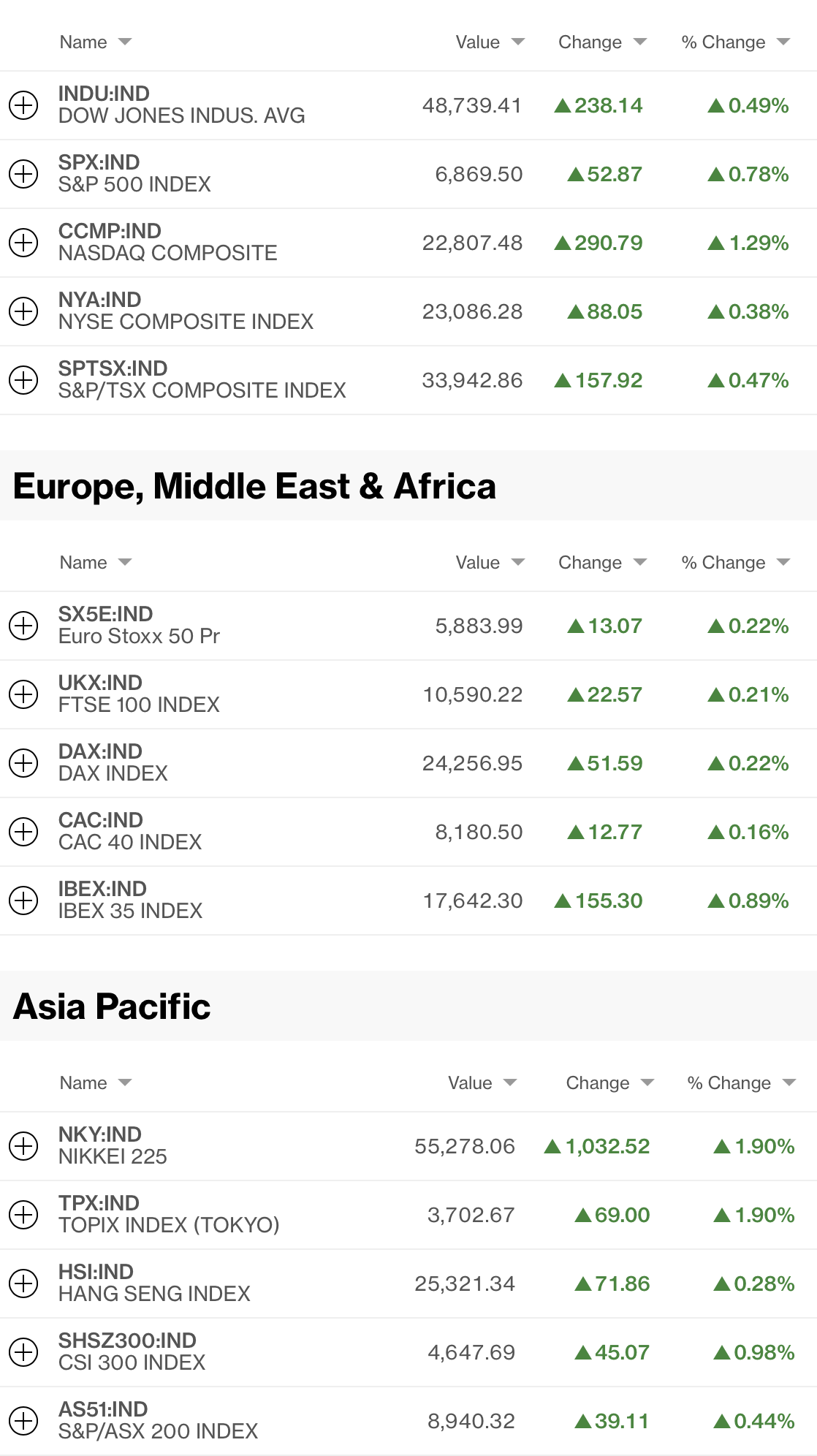

At any rate, other than the virtually infinite number of takes on the Iran war and the CPI data, there’s not much else to discuss, so let’s see how markets have responded to the latest and where they sit ahead of the data.

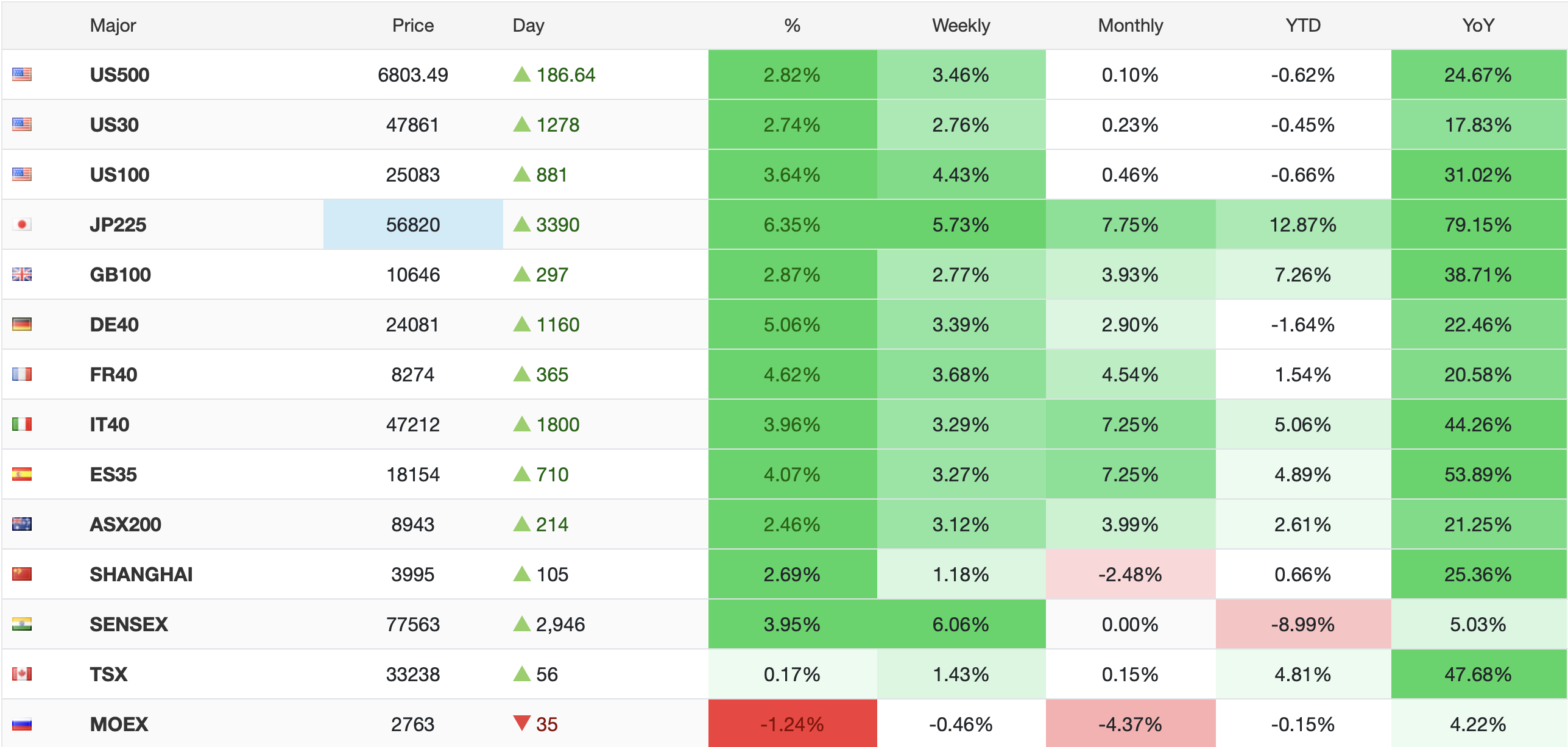

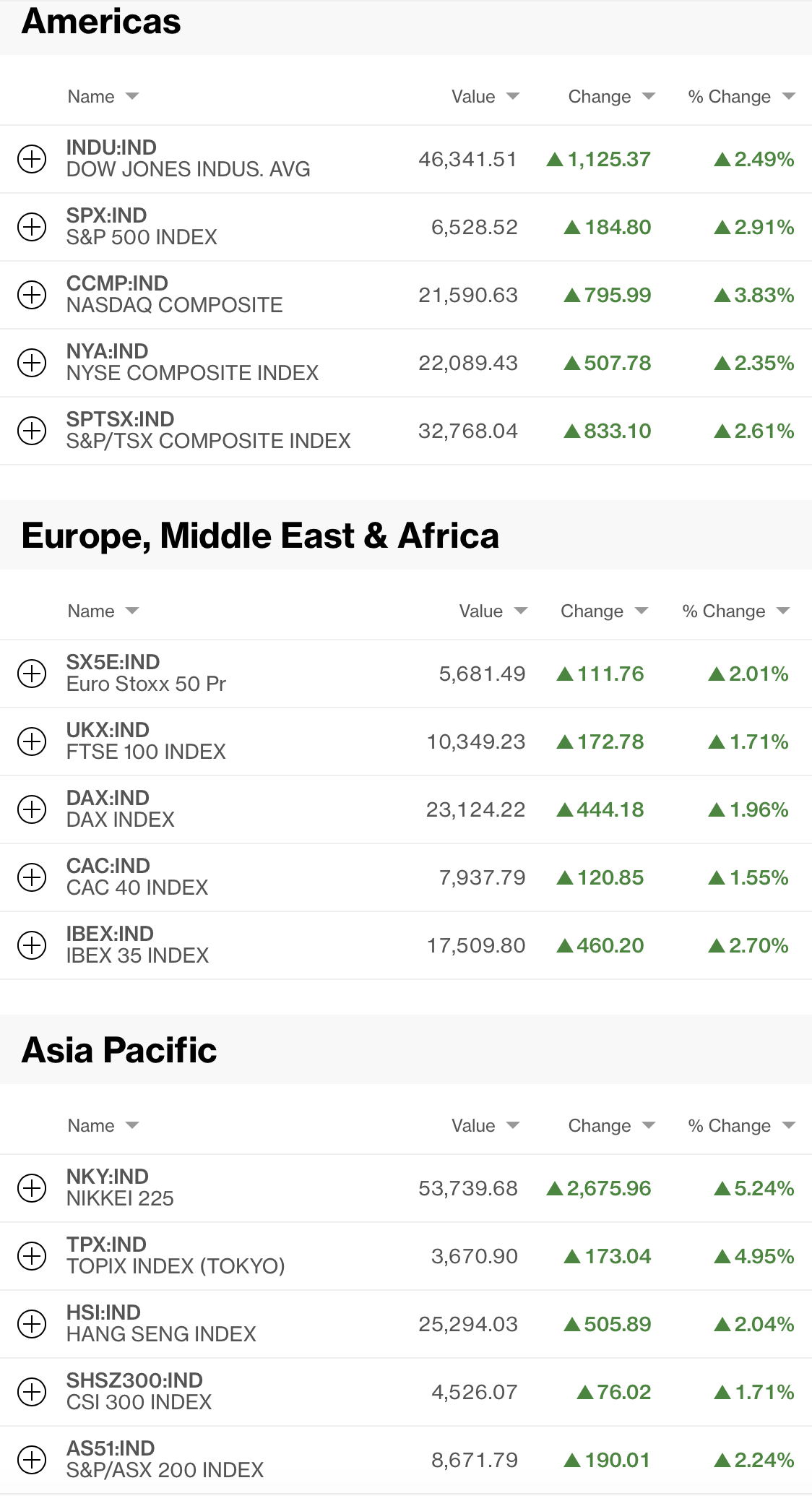

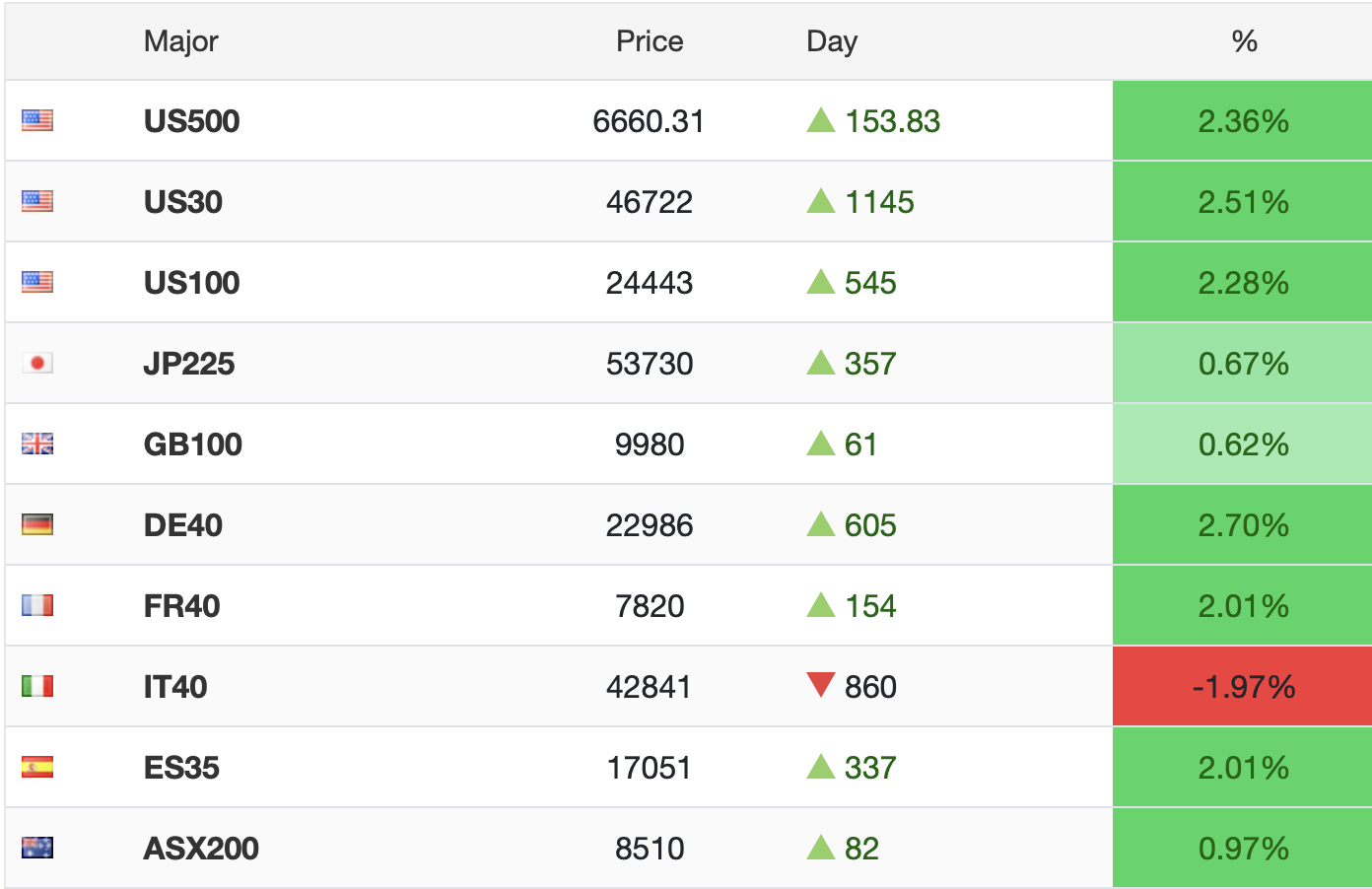

Yesterday’s early declines in the US were reversed, as per the chart at the top with all three major indices rallying more than 0.6%. in Asia, weirdly just Australia (-0.15%) and New Zealand (-0.7%) were the outliers on the downside with the rest of the region all in the green, some substantially so. Tokyo (+1.8%), China (+1.5%), Korea (+1.4%), Taiwan (+1.6%) and India (+1.2%) all had very strong sessions. Arguably, the weakness Down Under may be a reflection of their energy policies heading into the Iran war as neither nation has a substantial reserve (fossil fuels were deemed bad so their governments didn’t want to buy them) and both economies could suffer far worse than anyone else because of those decisions.

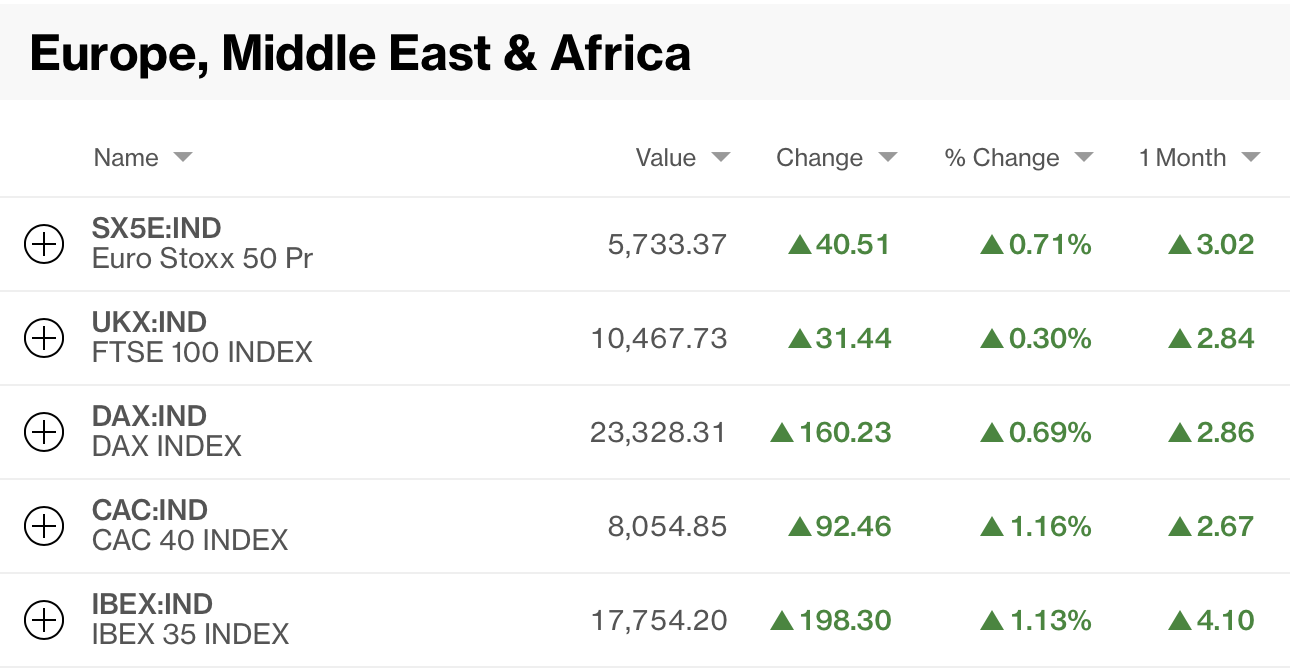

In Europe, markets are higher across the board although the gains are far more muted with France (+0.5%) the leader followed by Germany (+0.4%) and Italy (+0.4%) then the UK (+0.2%). While, certainly better than losses, they are hardly inspirational. As to US futures, at this hour (7:15), they are also pointing slightly higher, about 0.2% or so.

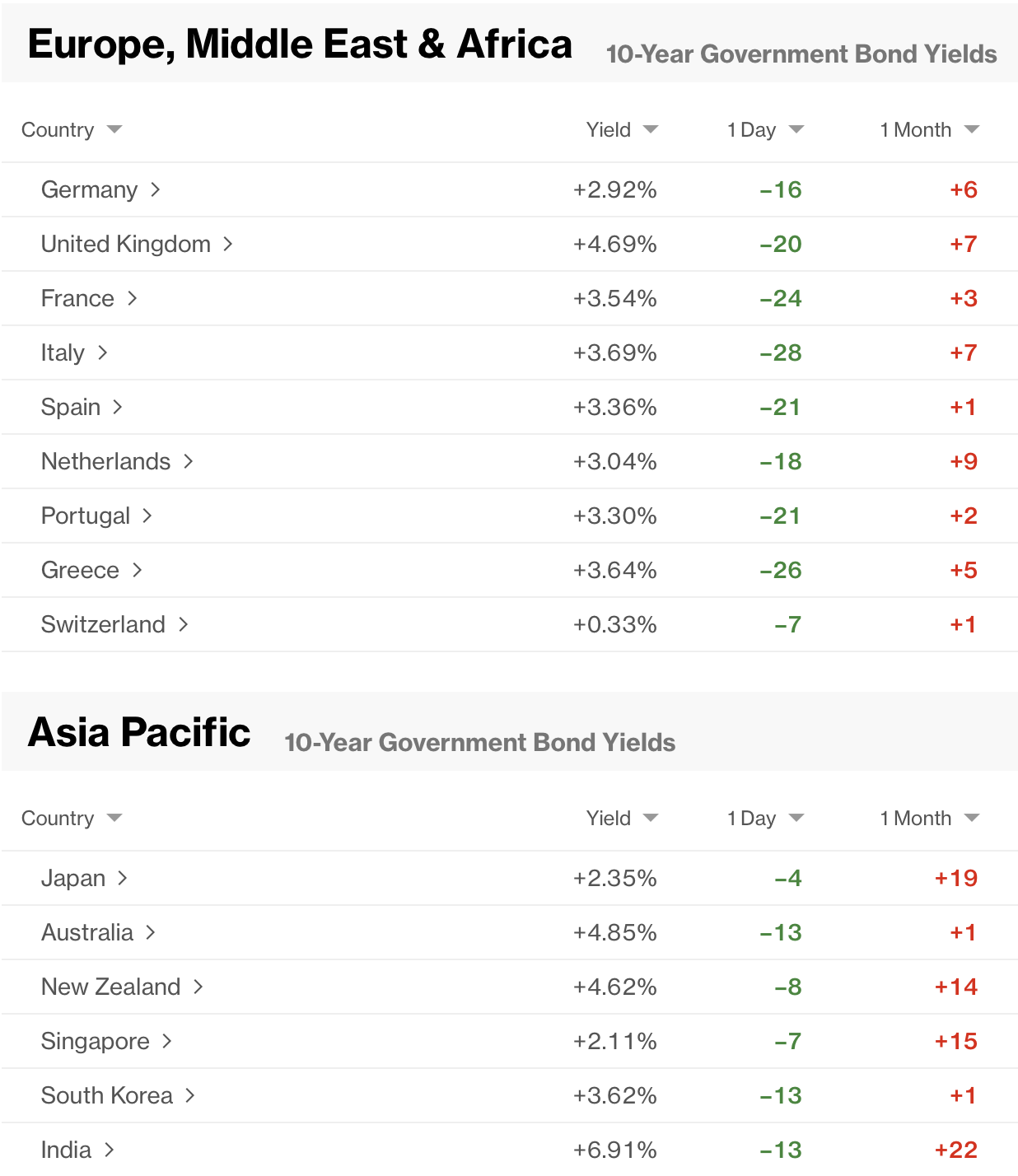

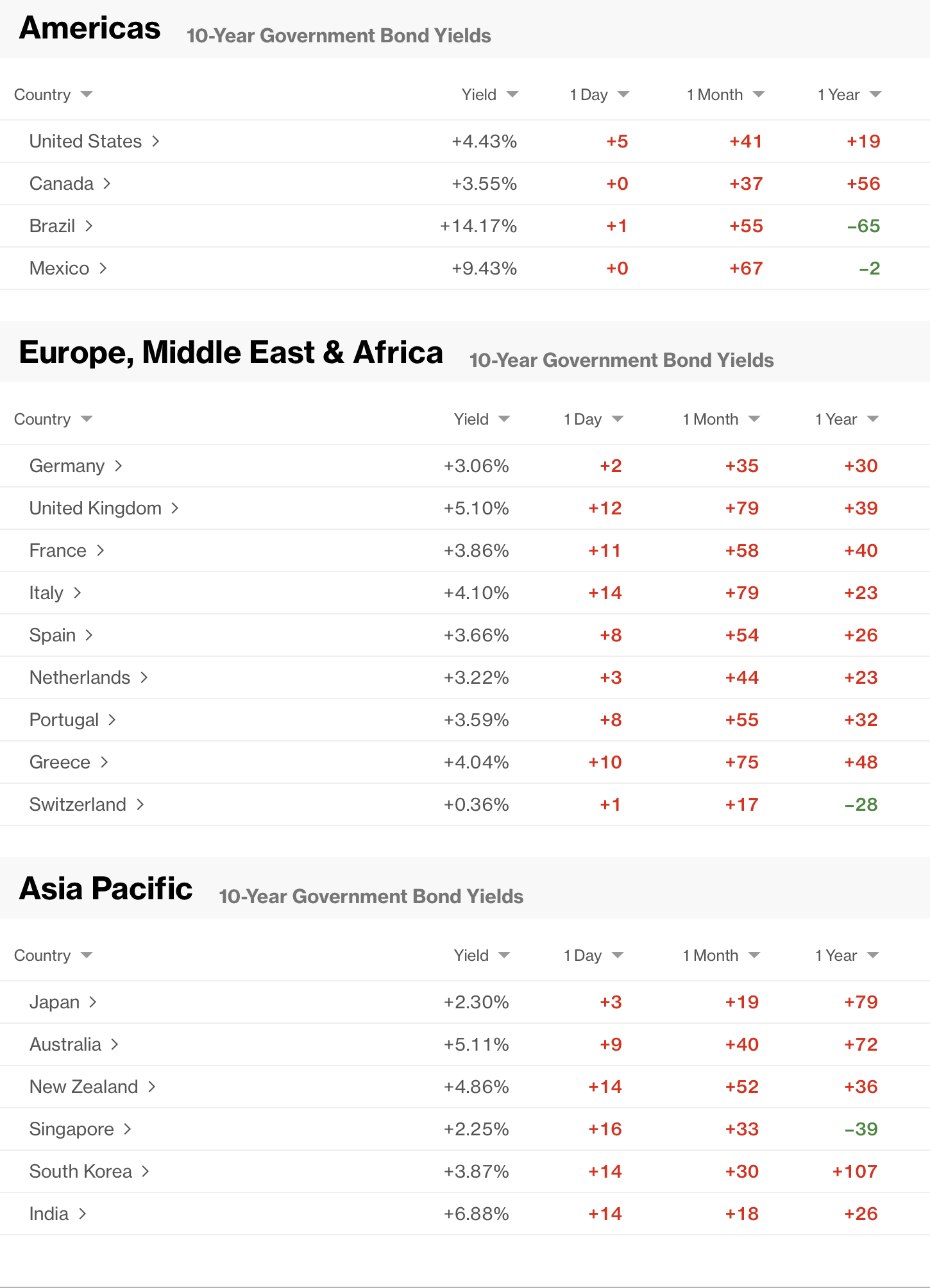

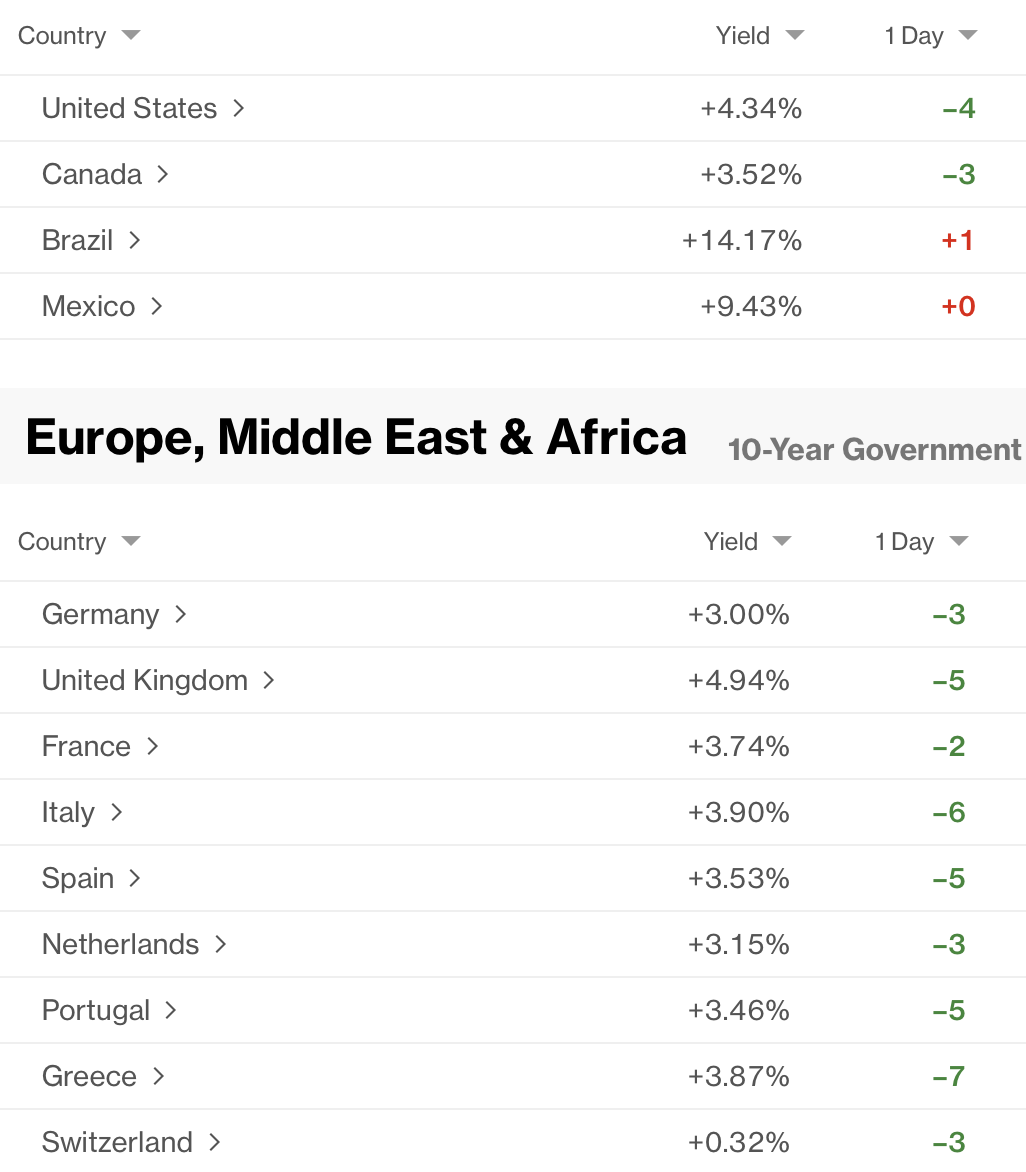

In the bond market, yields are backing up this morning with Treasuries (+2bps) the least impacted while European sovereign yields are higher between 5bps (Germany) and 8bps (Italy) with the rest of the continent somewhere in between. It is difficult to ascribe a particular story here other than rising concerns about general inflation being higher due to elevated energy costs. The market is pricing about 59bps of rate hikes by the ECB this year, perhaps a sign that investors don’t believe energy prices in Europe are going to decline as much as they will elsewhere. Given the continent-wide energy policies they have in place, I believe they are correct.

Turning to commodities, oil (0.0%) is unchanged this morning after sliding on the Lebanon news yesterday morning. The truly interesting thing is to watch NatGas (-0.6%) which continues to slide. Back toward its multi-year lows as it continues to be produced as an associated product alongside all the oil drilling that is ongoing.

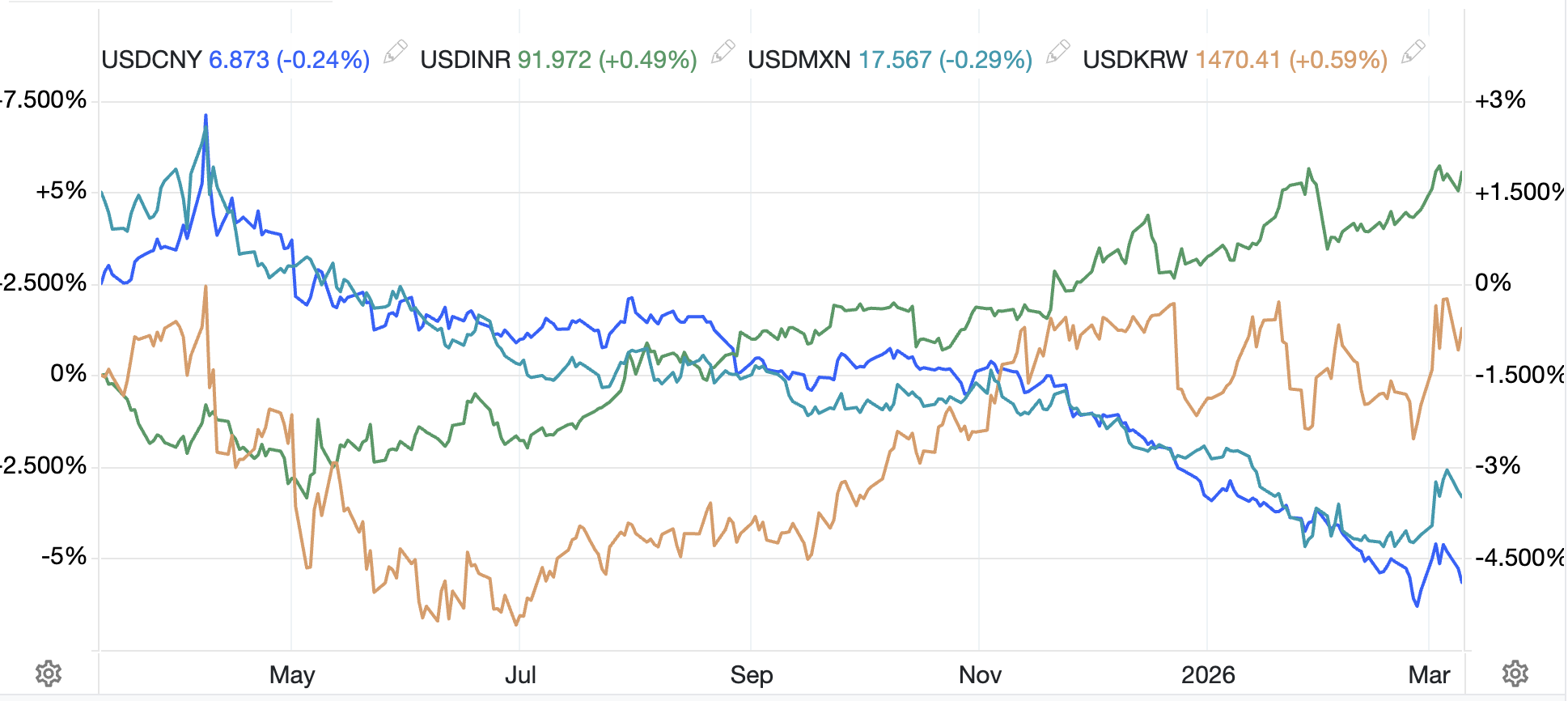

Source: tradingeconomics.com

I cannot look at the above chart and reconcile the massive energy advantage the US has with basically the rest of the world and conclude that the US economy is going to be at any disadvantage with other economies going forward, and hence the dollar seems very likely to remain in good stead going forward. Meanwhile, metals, too, are little changed this morning (gold 0.0%, silver +0.4%, copper +1.3%) with the latter a bit of a surprise after Argentina just passed legislation that will allow for more drilling in the Andes where Chile’s major copper deposits lie. That is a long-term prospect though, I must admit.

Finally, the dollar is mixed this morning, with very few significant movers in either direction. In the G10, +/-0.2% is the name of the game with the most noteworthy thing, I think, the yen (-0.25%) which is back above 159 this morning, although not yet threatening the perceived line in the sand of 160. In the EMG bloc, KRW (-0.6%) and ZAR (-0.4%) are the laggards although it is hard to ascribe specific news to either move. Rather, looking at the recent trading action, where both currencies have been rebounding sharply, these moves look like position squaring ahead of the weekend.

In addition to CPI, we also see Michigan Sentiment (exp 52.0) and Factory Orders (-0.2%) at 10:00. There are no Fed speakers so today is shaping up to be data dependent unless we hear something from the talks in Pakistan. However, it seems far too early for anything of substance there. I imagine if core CPI is firm, that could be an equity negative as that would encourage more thought of the Fed hiking, but I have a feeling that despite the broader importance of the number, markets are not going to do much today.

Good luck

Adf