While Friday, the world was on edge

And everyone wanted to hedge

This morning it seems

That Trump and his schemes

Have backed us away from the ledge

So, while Asian stocks mostly fell

In Europe, there’s been no death knell

And futures at home

Though not quite with foam

Are bubbling up, doing well

The bond market, though, is confused

With some analysts quite enthused

Recession is near

So, bond buys they cheer

Though holders, so far, have been bruised

The counter to this contestation

Is, soon we will feel more inflation

So, bonds are a sale

As Jay can’t curtail

That outcome, so short long-duration

Let me start by saying, we are still in a situation where nobody knows exactly what is happening in Iran and the Persian Gulf, although we continue to hear lots of propaganda from both sides. It does appear that Iran’s military has absorbed a significant beating, but they continue to fire missiles in retaliation, albeit at a reduced pace. It seems there are the beginnings of some discussions regarding ending the conflict, ostensibly with Pakistan taking the lead in speaking to both sides, but there have been no direct talks yet. Time is still a critical issue as every day the Strait of Hormuz is closed, that adds further pressure to the global economy, especially in Asia and Europe which are the two areas most reliant on energy flowing through the Strait.

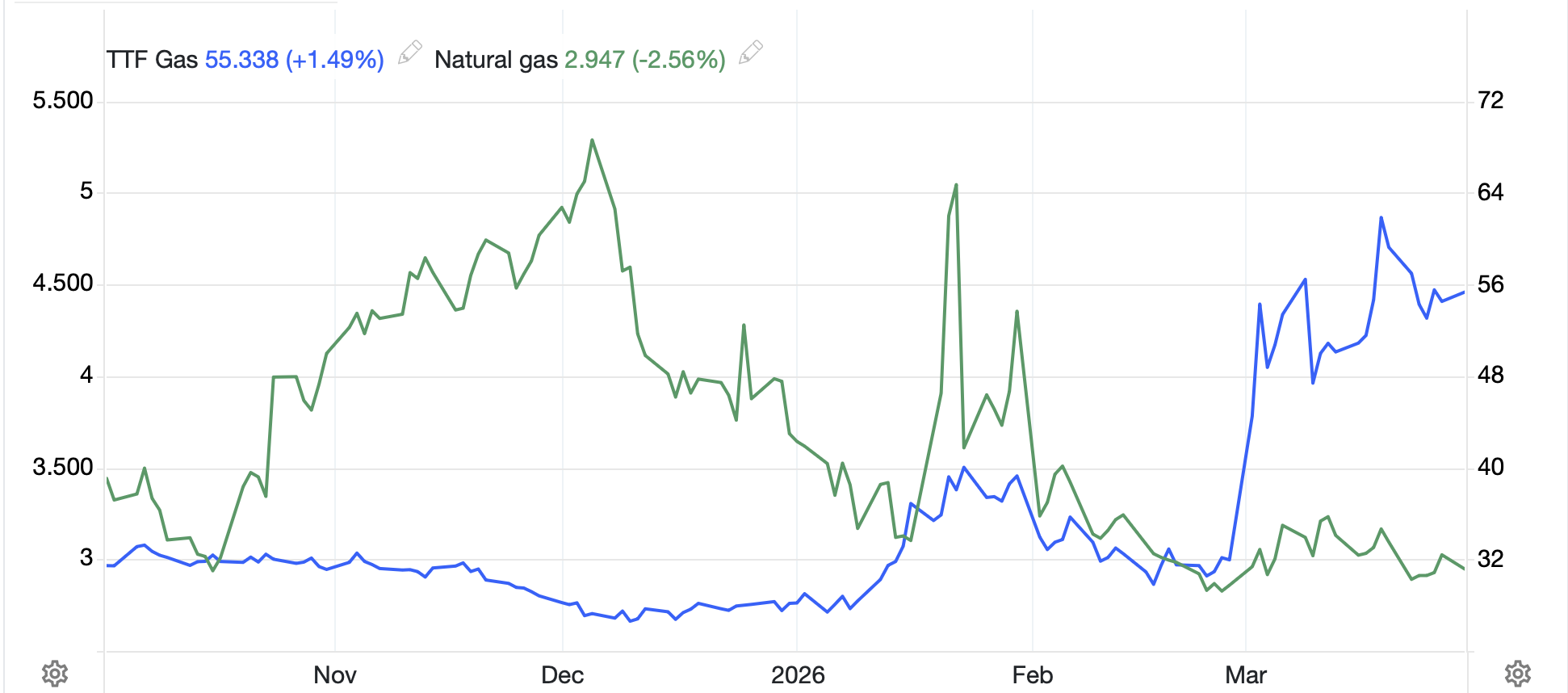

As I was considering the implications of oil prices at $100/bbl in the US, I realized that every fracking well in the US is going to be pumping at maximum capacity, and given how quickly DUC (drilled but uncompleted) wells can be brought on line, I expect that we will see US oil production rise from its recent 13.7 million bbls/day. But alongside that, many, if not most, of these wells will be producing associated gas, i.e. natural gas that comes up with the oil, which is one reason, I believe, that Natural Gas prices in the US (-2.5% today) are essentially unchanged since the war began a month ago (green line). Meanwhile, as you can see with the blue line on the chart, European Natural Gas prices have exploded higher. In fact, this morning, US prices are just below $3.00/MMBtu while European prices are about $18.65/MMBtu. (European gas is quoted in EUR/MWh, which is why the price looks so different.). Europe needs this war to end a lot sooner than the US from a pure economic perspective.

Source: tradingeconomics.com

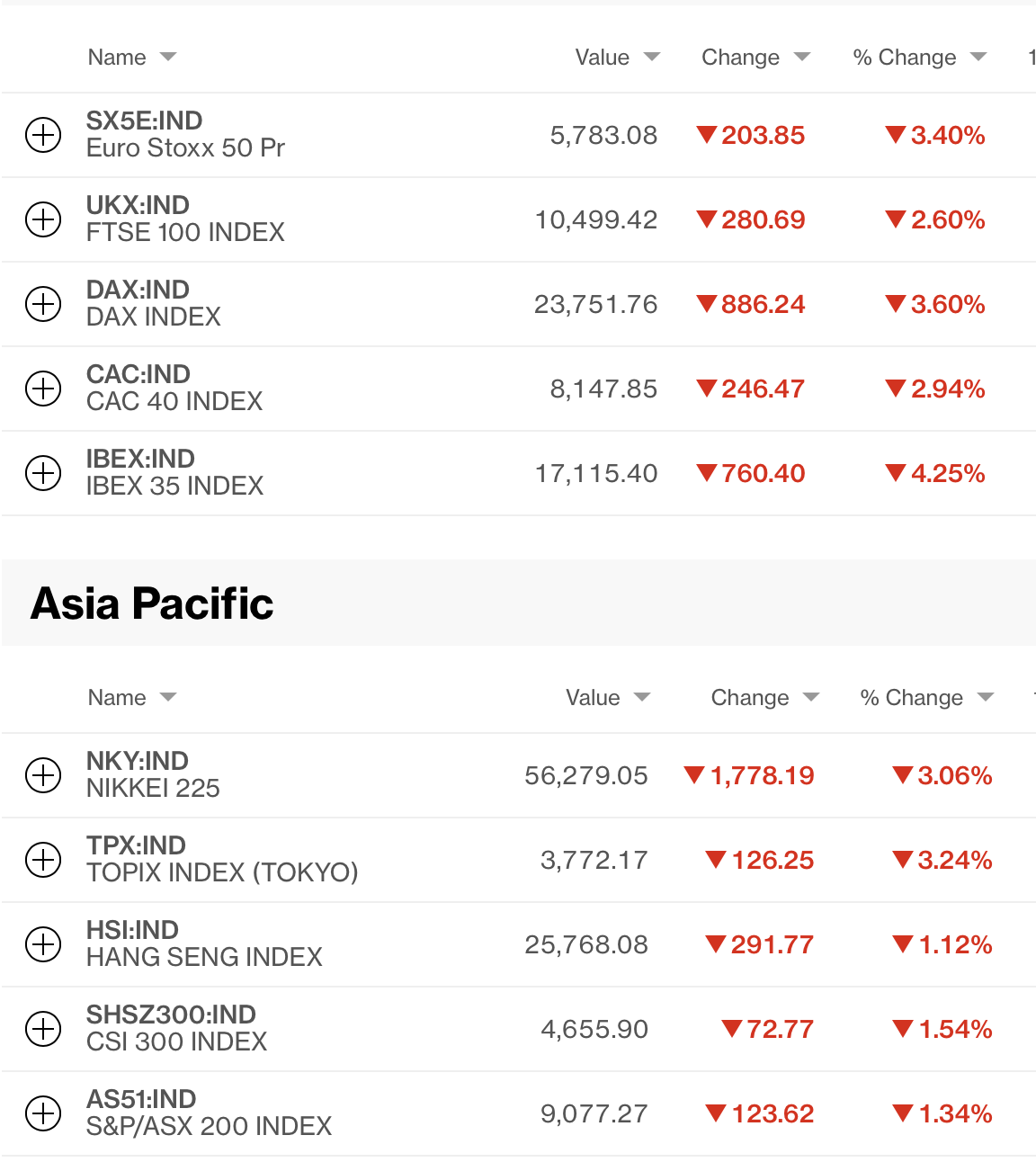

Away from that stray thought, if we look at equity markets, you can see there has been a real turn. Friday felt dreadful with every index falling and closing on its lows. And Asia followed through with that thesis as virtually all bourses there were under real pressure. Japan (-2.8%), Korea (-3.0%), India (-2.2%) and Taiwan (-1.8%) all fell sharply following the US lower. Both China (-0.25%) and HK (-0.8%) also slipped, but not quite as aggressively. The issue here is all these nations rely on energy transiting the Strait and are suffering accordingly. My take is that not only will these equity markets have issues, but so, too, will their currencies until things in the Gulf are settled.

As to European equities, the story there is less dramatic this morning with a mixed picture as the UK (+0.5%) is higher along with Spain (+0.3%) and Italy (+0.3%), although Germany (-0.2%) and France (-0.1%) are slipping. The big winner here, not surprisingly, is Norway (+2.0%). We also saw the first March inflation data from anywhere in the world this morning from Germany, and not surprisingly, it was higher. While the nationwide number has not yet been released, the individual Landers all show something between 2.5% and 2.9%, generally higher by 0.7% or more. The market is looking for a 2.7% national reading, up from 1.9% February print. US futures, meanwhile, are higher by 0.6% across the board at this hour (7:15).

In the bond market, though, inflation fears, which were all the rage on Friday, have abated somewhat with Treasuries (-4bps) seeing demand and European sovereign yields all softer by between -1bps and -3bps. Even JGB yields (-2bps) have slipped, although the latter appears to be on the back of stories the BOJ is getting ready to hike rates in April and the question is how much, not if. So, despite oil prices continuing to rise, and adding inflation pressure around the world, bond investors are relatively sanguine this morning.

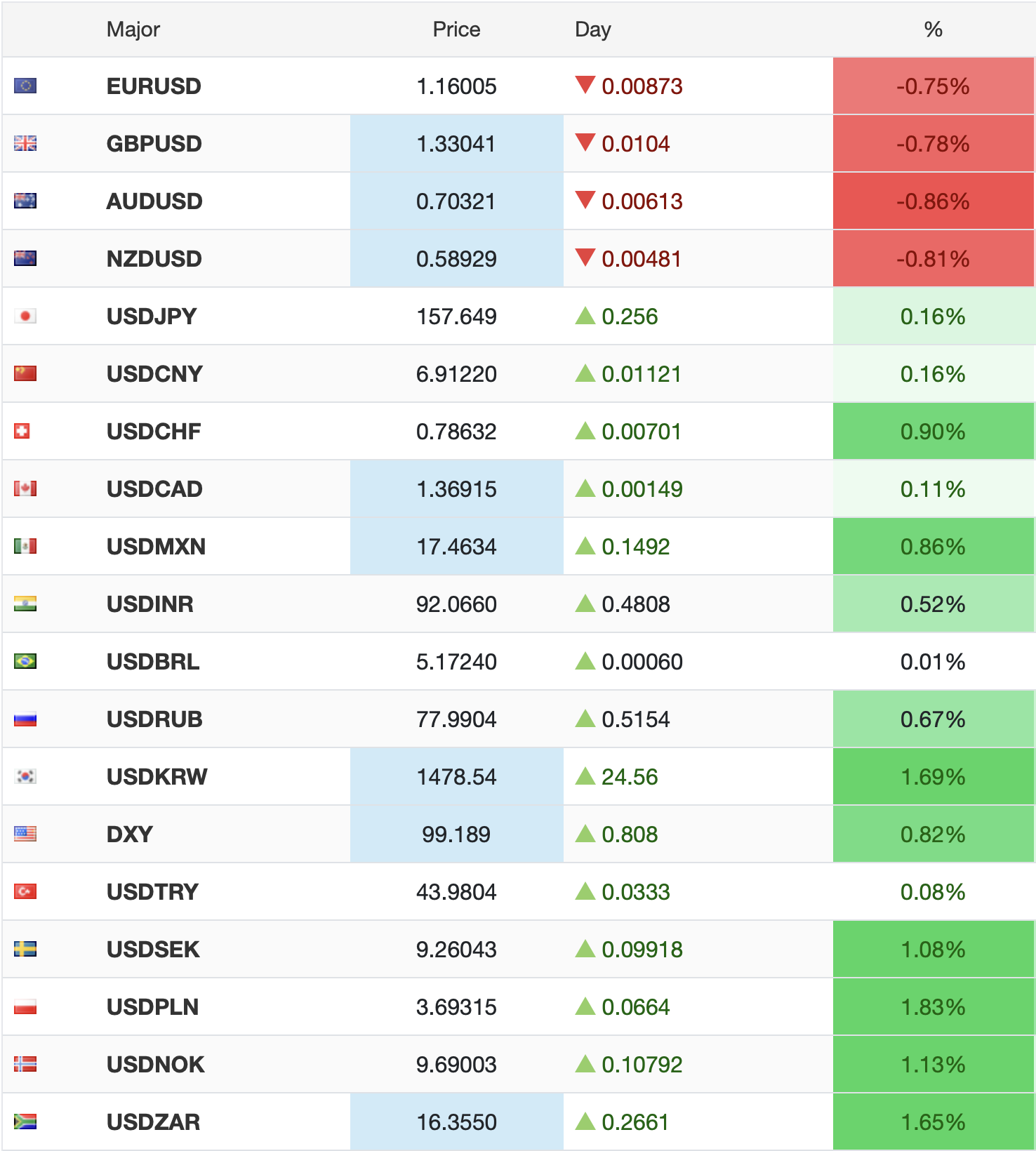

In the FX markets, the story has been more mixed this morning with the dollar broadly firmer, but not universally so. In the G10, the yen (+0.5%) is the outlier as having traded above the 160.00 level Friday, we heard more from Japanese authorities, specifically, the current Mr Yen, Mimura-san, that they did not welcome speculative trading and would address it if they believed that was driving the yen weaker than it should be. Given the dollar is firmer vs. all its other G10 counterparts over the past month, it is surprising that is the case they are trying to make, but I guess they need to say something. Otherwise, this bloc is mostly softer by about -0.2% or so across the board. In the EMG bloc, INR had a little hiccup last night as per the chart below.

Source: tradingeconomics.com

It seems that the RBI reduced the size of positions that Indian banks are allowed to hold regarding short rupees every day, which forced a serious appreciation of the currency. However, as you can see, it was relatively short lived and compared to Friday’s close, the rupee is weaker by -0.2% despite the new regulations. Otherwise, ZAR (-0.3%) and KRW (-0.6%) are the weakest in the bloc with one outlier, MXN (+0.3%) rallying back from its close on Friday as it closed then at its lowest level since December. In fact, this morning’s price action seems more like a trading reaction than a fundamental shift.

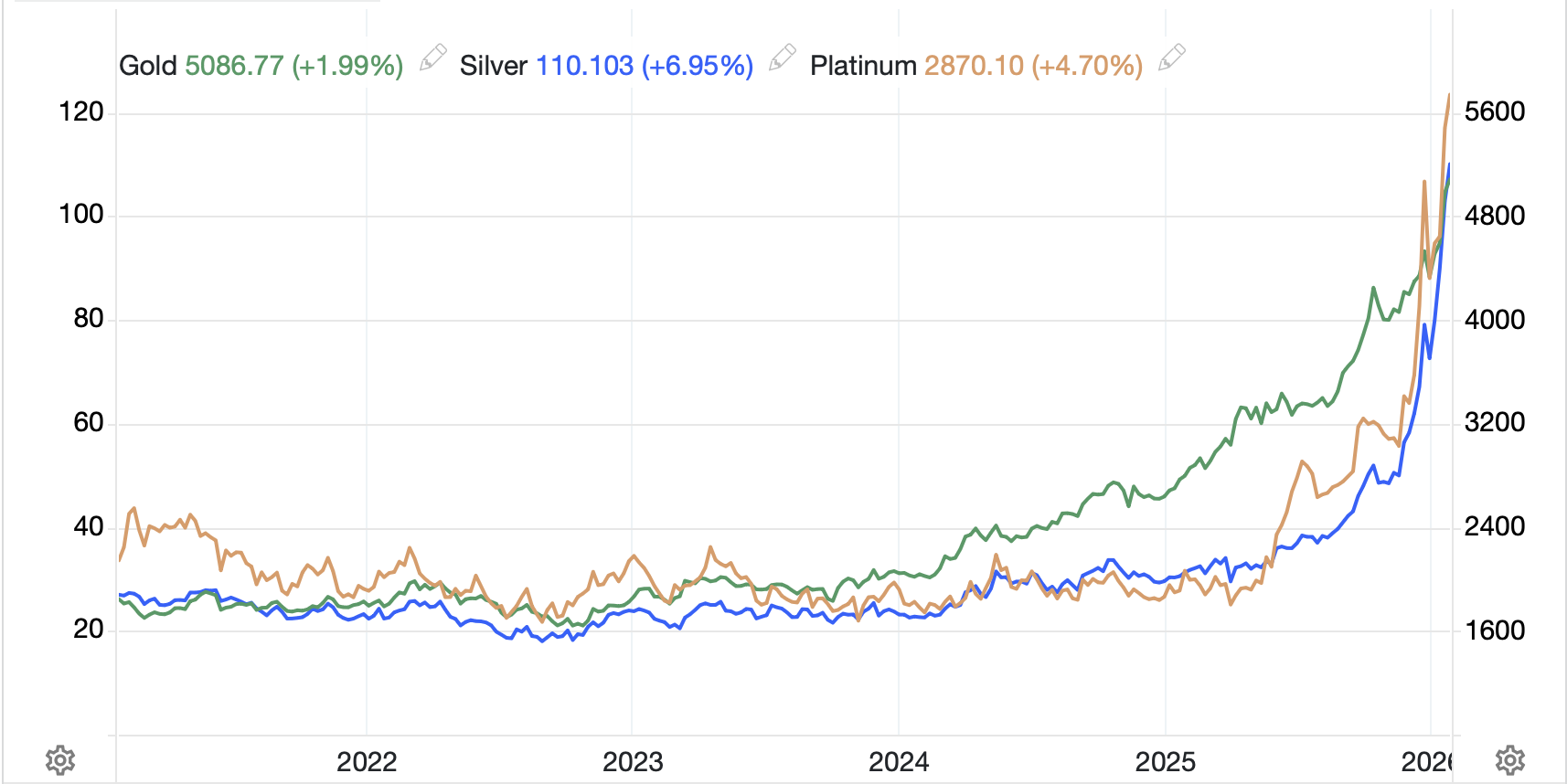

Finishing with commodities, oil (+1.1%) is back above $100/bbl in the US (above $115/bbl in Brent) although it is not really running away. Traders are clearly uncertain what to believe with respect to the potential opening of the Strait. We do get a lot of conflicting news from both sides, I must admit, and I find that reading either all the headlines or none of the headlines leaves you in exactly the same place, no idea what is reality. The biggest change in the commodity space is in gold (+1.7%) and silver (+2.6%) as the past two days they have both risen alongside oil, rather than their behavior during the first month of the conflict. It is easy to believe that the major downdraft in the precious metals was a result of liquidation during stress rather than gold’s loss of its haven status and I tend toward that view. While I am no market technician, the little I do know is that the blow-off low last Monday at $4100/oz may well have defined the bottom of this move.

Source: tradingeconomics.com

Again, 5000 years of history tell me that people will still want to hold the stuff in times of crisis as a way to retain the value of their assets.

Turning to the data this week, while we start slow today (although Chairman Powell speaks at 10:30), we finish the week, on Good Friday, with NFP.

| Tuesday | Case Shiller Home Prices | 1.3% |

| Chicago PMI | 55.8 | |

| JOLTs Job Openings | 6.897M | |

| Consumer Confidence | 88 | |

| Wednesday | ADP Employment | 40K |

| Retail Sales | 0.4% | |

| -ex autos | 0.2% | |

| ISM Manufacturing | 52.3 | |

| ISM Prices Paid | 73.5 | |

| Thursday | Trade Balance | -$59.2B |

| Initial Claims | 212K | |

| Continuing Claims | 1825K | |

| Friday | Nonfarm Payrolls | 55K |

| Private Payrolls | 55K | |

| Manufacturing Payrolls | 0K | |

| Unemployment Rate | 4.4% | |

| Average Hourly Earnings | 0.3% (3.8% Y/Y) | |

| Average Weekly Hours | 34.3 | |

| Participation Rate | 62.3% |

Source: tradingeconomics.com

So, plenty of information this week, but with a holiday weekend coming up next weekend as US equity markets will be closed Friday and European ones on Monday as well, it remains unclear just how important the data is these days. We are still headline driven although as the Marines make their way to the Persian Gulf, it has the potential to be a relatively quiet week ahead of any increase in military activity, maybe next weekend. We shall see. For now, the dollar continues to hold its own, and risk appetite is not collapsing in any meaningful way, yet. We have to see how long that can last if the war continues to drag on.

Good luck

Adf