This Friday is labeled as Good

And markets worldwide understood

That trading’s not right

So closed with no fight

If only the government could!

Instead, they’ll release NFP

Though traders won’t be there to see

And Monday, as well

There will be no bell

Let’s hope war’s not raised a degree

Philosophers ask, if a tree falls in the forest and nobody is there, does it make a sound? Today, investors will ask, if the NFP report is released and there are no markets to respond, does the data matter?

In a highly unusual circumstance, this morning’s NFP report is going to be released on Good Friday, the one day of the year when equity markets are closed but banks are open, as is the US government. As well, given the holiday, many international markets were closed overnight and essentially all of Europe is closed right now. Too, Monday is a holiday in many nations around the world, Easter Monday, so equity markets throughout Europe and all old Commonwealth nations will be closed for a very long weekend.

Which begs the question, does today’s data really matter? After all, we have a long weekend ahead of us and the possibility of an escalation of fighting in Iran, which if that occurs will make any data today moot. FWIW, here are the expectations for this morning:

| Nonfarm Payrolls | 60K |

| Private Payrolls | 70K |

| Manufacturing Payrolls | -5K |

| Unemployment Rate | 4.4% |

| Average Hourly Earnings | 0.3% (3.7% Y/Y) |

| Average Weekly Hours | 34.3 |

| Participation Rate | 62.3% |

Source: tradingeconomics.com

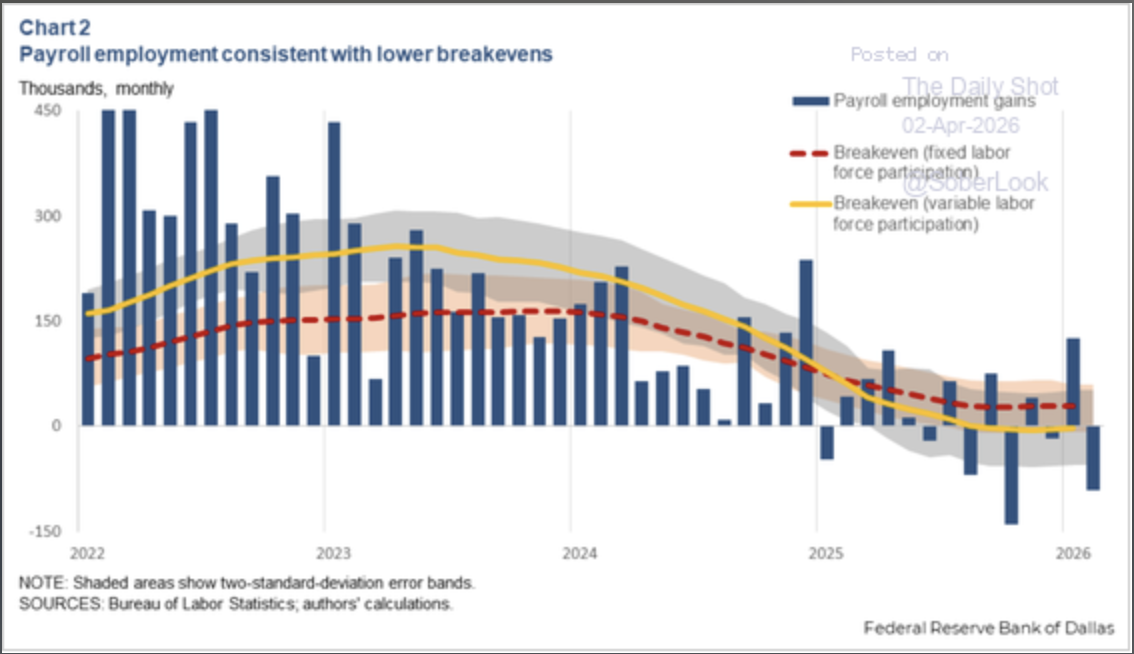

Remember, too, ADP Employment was a touch better than expected. As well, there is increasing evidence that the data with which we had become familiar regarding the number of new jobs necessary to maintain a stable employment market has fallen sharply. For the longest time, econometric estimates were that somewhere between 150K and 200K new jobs were needed each month to prevent the Unemployment Rate from rising. But the Dallas Fed just released a research report suggesting that is no longer the case. In fact, they estimate the number is basically zero.

Obviously, the big changes have come from immigration policy in the US, with the closing of the border, the deportation of between 350K and 650K (depending on your source) of illegal immigrants by the government as well as the self-deportation of somewhere on the order of 2 million more people. These actions have dramatically reduced the available work force and with that, the number of new jobs required to reach an employment equilibrium.

Despite these changes, arguably the data ought still to matter as it represents a key part of the FOMC mandate. But given the war has drowned out basically all economic data, it is not clear these numbers are going to be meaningful for a while yet. All those who trade via algorithm are the ones who are most impacted as payroll day was always a huge winner for them. And while US futures markets are open (currently -0.2% across the board at 7:25), there will be no arbitrage opportunities as the underlying markets won’t open until Monday in the US and Tuesday in Europe.

Which takes us to the other story, will there be an escalation of fighting in Iran over the long weekend? Every story I have read in the MSM has written, almost glowingly, about how the Iranians are completely prepared for any US invasion and will inflict serious damage and casualties on the Americans if one comes. Again, I am not a defense analyst, but to my understanding, the US does not yet have all its assets in theater which will preclude any opening salvos. The other thing I would say is historically, I wouldn’t bet against the USMC achieving their objective.

And that’s where we stand this morning, awaiting data to be released into a void with no opportunity to respond, really, until Monday, at least in the equity markets.

In fact, other than cryptocurrencies, which are always open, the only market of note that is open today is the FX market, and that is suffering from diminished liquidity because European centers are closed for the holiday, although US banks will be active. Or perhaps active is the wrong term, they will be open. With that in mind, it should not be surprising that the dollar is, overall, little changed from yesterday’s closing levels. In fact, every G10 currency is within 0.1% of yesterday’s close although we have seen a touch of weakness in ZAR (-0.6%) which is still suffering from gold’s -2.25% performance yesterday.

The only other currency that moved more than 10 basis points was INR (+0.3%) which continues to benefit from RBI efforts to prevent its complete collapse. You can see the performance of the rupee over the past five years and that spike near 100 was seen as a near-death experience by the RBI and drove them to respond. Alas, the war is not helping their cause at all and there are scant few reasons to buy the rupee for most traders these days.

Source: tradingeconomics.com

Otherwise, all I can offer is for you all to have a wonderful Easter/Passover weekend and we will pick up again Monday, but really it will take until Tuesday before we get a better sense of how the news will be absorbed, whatever it may be.

Good luck and good weekend

Adf