Though skeptics do not yet believe

That Trump, a peace deal, will achieve

The markets are saying

This sunshine they’re haying

And fading this move is naïve

So, oil continues to fall

And stocks are just having a ball

It’s peace in our time

And all quite sublime

To many, though, this tale is tall

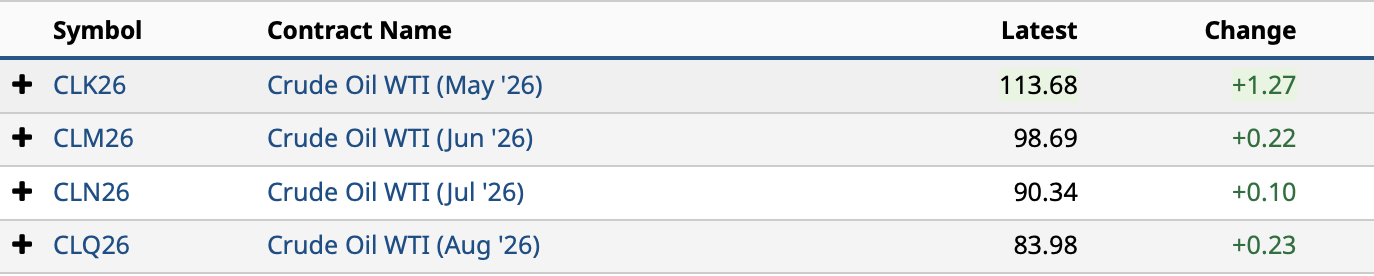

It is not clear what else to say about the current situation other than the markets are starting to believe that the Iran conflict is coming to a close. The headlines from the administration and news from Pakistan seem to indicate a deal is near, something we all should welcome. Certainly, the market is ready to accept this as gospel, at least based on the current risk appetite being demonstrated across all markets. So, this morning, oil (-2.8%) continues its rapid decline, down more than $18/bbl from its highs just one week ago.

Source: tradingeconomics.com

The commentariat refuses to accept that the conflict is ending and I cannot tell if that is because they hate President Trump so much, they cannot stand the idea of him concluding things having achieved objectives, or because if the conflict is over, they will need to find the next thing to prove their ‘expertise’ and they don’t know what that is yet (hantavirus anyone?) Regardless, markets are on board with this narrative as the moves we saw yesterday are simply extending this morning.

Meanwhile, the data from yesterday showing that ADP Employment was a stronger than expected 109K and the JOLTs quit numbers rose, meaning more people are willing to quit their jobs for a new one, indicating a growing confidence in the labor market, point to a continuation of the US equity rally, and by extension, the global rally. (As an aside, I chuckled at the article in the WSJ this morning about how the next target of taxes should be ‘compute’ since AI is going to replace human workers. My comment here, which has been confirmed by my time this week at the Consensus 2026 cryptocurrency conference, is that machines are great, but people still want to deal with people they can trust!)

Anyway, with the conflict ostensibly coming to a close, there is not much else to discuss outside actual market activity, so let’s see how things responded to this news.

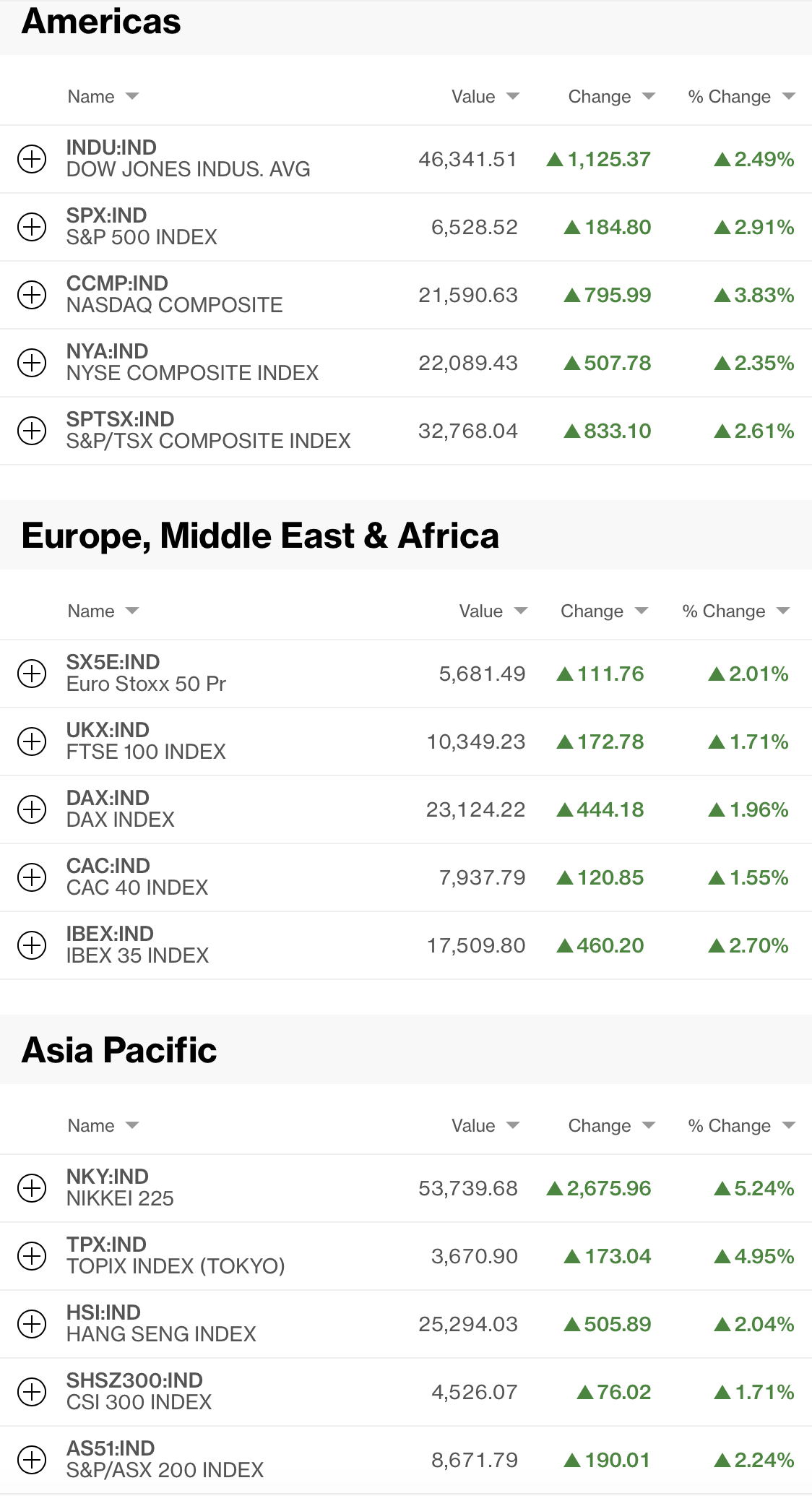

By this time, you have all checked your PA’s and saw the green from yesterday there. Overnight, Asian markets were also quite positive with Japan (+5.6%) exploding higher after their Golden Week holidays ended. Excitement on tech as well as a market that is looking forward to Treasury Secretary Bessent’s visit were the drivers. But we also saw strength in China (+0.5%), HK (+1.6%), Korea (+1.4%) and Taiwan (+1.9%). In fact, looking across the region, you are hard pressed to find a true laggard, as India (0.0%) was the worst performer of note. European markets, though, are not quite in as fine a fettle with most of them essentially unchanged this morning although the UK (-0.7%) is lagging after some underwhelming earnings reports as it appears profit taking is today’s motive. As to US futures, at this hour (6:45), they too, like Europe, are essentially unchanged

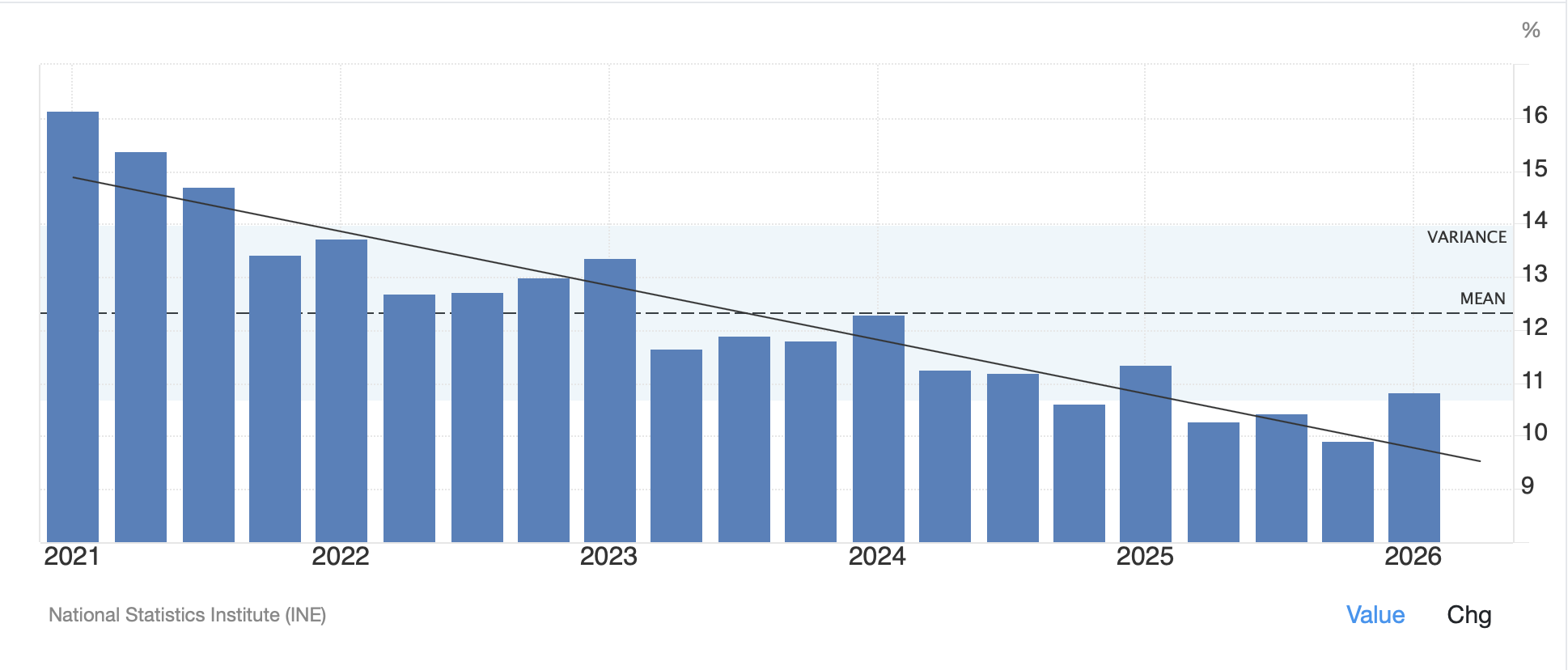

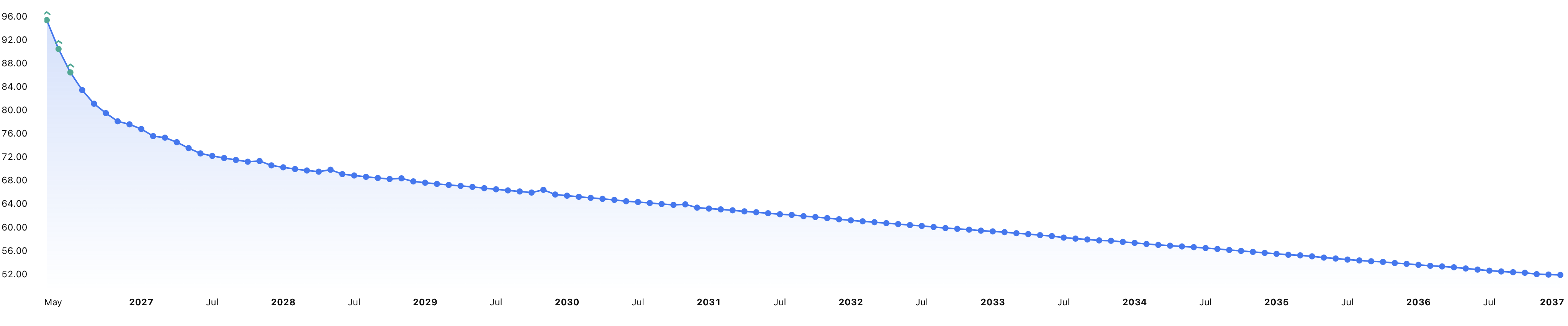

In the bond markets, yields continue to slide with Treasury yields lower by -2bps and virtually all European sovereign yields slipping -1bp. Overnight, JGB yields fell -3bps as markets there reopened and essentially all Asian government bonds saw yields decline as well. Apparently, fears over rampant inflation are ebbing. You may recall on Tuesday I discussed the 30-year Treasury as it traded above 5.0% on Monday and stayed there for about a minute. That had engendered a great deal of apocalyptic discussion. However, here we are this morning with 30-year yields slipping another -2bps, and now 10 bps below that little spike, and back below 5.0%. But I think it is worthwhile to offer a little perspective on the 30-year bond and the idea that 5.0% is deadly. Here is the chart of 30-year Treasury yields since 1985. Perhaps the anomaly was much lower yields, not 5.0%!

Source: finance.yahoo.com

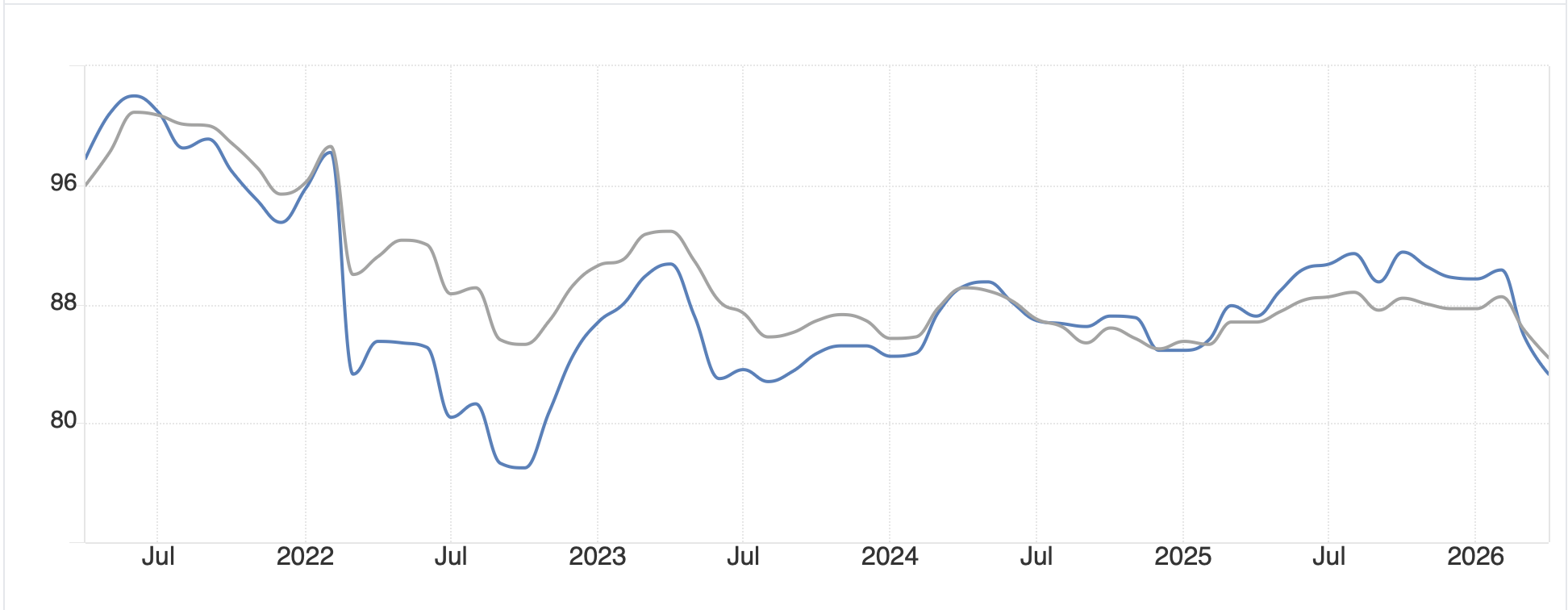

Precious metals are continuing to benefit from the peace initiative and oil’s delice with gold (+1.0%) and silver (+4.0%) both stronger again after big gains yesterday. In fact, I am starting to read more about why silver is set to make massive gains because of shortages, a narrative that was set aside for the past two months but seems to be reawakening. Now, I am no technician, but I am given to understand that if you look at this trend line in silver from its January peak, we have broken above the line and that portends a massive move higher. (full disclosure, I am long silver so would be happy to see that but have not spent the extra money yet!)

Source: tradingeconomics.com

Finally, the dollar is softer again this morning, which should be no surprise based on the overall market zeitgeist this morning. So, the DXY (-0.15%) is a pretty good approximation of what is happening, although we have seen some larger moves, notably NOK (+0.8%) which seems to be responding to the fact that the country is going to reopen some shuttered oil and gas drilling sites in the North Sea as Europe tries to figure out where to get energy from. As to the yen (0.0%) after a series of what appeared to be modest interventions by the BOJ during Golden Week, it appears the market may be explaining that the fundamentals are still pointing to yen weakness and while the BOJ may be able to cap the dollar for a short time, establishing real JPY strength will take a lot more effort, and real policy changes (i.e. much higher interest rates).

Source: tradingeconomics.com

Turning to the data this morning, we get the weekly Initial (exp 205K) and Continuing (1800K) Claims data, which continues to hover near historic lows despite the angst over the labor market. We also see Nonfarm Productivity (1.4%) and Unit Labor Costs (2.6%) and hear from several more Fed speakers, although most of their comments are back page news. Of course, tomorrow we will see the NFP report, and that will certainly garner all the attention. Personally, I will be focused on the Manufacturing Payrolls outcome as a proxy for the reshoring initiative and the potential for continued strong economic activity going forward.

And that’s really it. Despite the ongoing narrative of the dollar’s demise, it remains well within its recent trading range, and I keep reading about other nations issuing dollar debt as that is the market with the most liquidity. Over time, I continue to see the dollar as the best fiat around, although I still like stuff more than paper.

Good luck

Adf