The story today is the Fed

And whether, when looking ahead

Inflation they see

Stays well above three

Or if it just might fall instead

Meanwhile, every comment I’ve read

Discussing the ‘deal’ have all said

Too much was conceded

The US retreated

And look to the future with dread

Starting with the MOU with Iran, and having read the text of the agreement, at least the one published by Bloomberg, Iran has sworn to never have a nuclear weapon and then will effectively be readmitted to polite society, with sanctions and restrictions eventually removed. The several comments I have read on the deal highlight numerous potential loopholes and semantics regarding tolls and fees and are uniformly unhappy with the deal. But I’ve also read that many on Iran’s side are unhappy with the deal. Arguably, the best sign the deal is going to last is just that, neither side got everything they wanted, but both got some of the things they wanted. Time will tell how this all plays out, but certainly the oil market remains positive that the direction of travel is toward a normalization of flows through the Strait of Hormuz.

However, while the political pundits are going to continue to focus on that issue, markets have turned their focus to the FOMC meeting and how things play out under new Chairman Kevin Warsh. The previous Fed whisperer, Nick Timiraos at the WSJ, continues to push Governor Powell’s message as there is not yet a new Fed whisperer. My take is Timiraos will not be the one simply because his loyalties will not lie with Warsh.

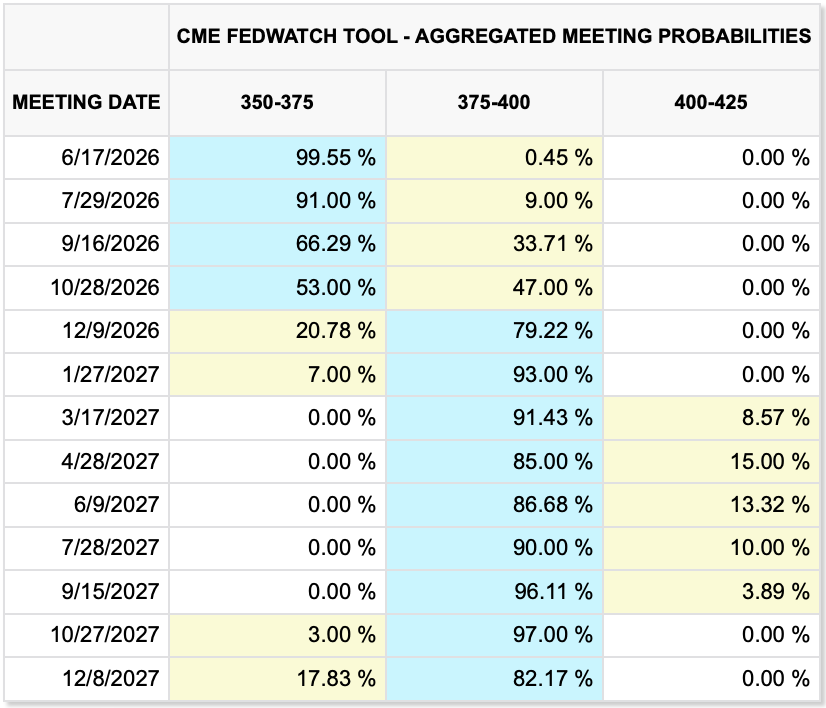

The thing in which we can be most confident is there will be no rate change at today’s meeting although the market continues to price a rate hike in December as per the below CME table.

All the drama will come with the release of the SEP (Summary of Economic Projections) which is the quarterly document the Fed publishes showing the range of economic forecasts by the individual FOMC members regarding GDP, Unemployment and interest rates. This document also includes the dot plot. It is important to note that the SEP only started to be released in 2007, so this is not a long-standing tradition, but part of Ben Bernanke’s changes to the institution.

And this is a key feature of what makes Kevin Warsh different. He has indicated that the Fed talks too much (I agree) and believes that some ambiguity in what is going on is a desired outcome. This is a controversial stance as Wall Street has minted money on the back of forward guidance, recognizing the Fed has their back whenever they blow up because they built up huge leverage and were wrong.

While I completely understand the idea that political discussions need to be in the open, I am far more suspect with respect to monetary policy discussions. Prior to forward guidance, market participants were far more cautious in their positioning as the probability of getting the direction of a trade wrong was far greater. But once the Fed says, ‘rates are going to stay low for a very long time’, traders can lever up positions massively relying on the fact that their funding costs are going to remain in check. And it is the massive leverage where the risks to the market lie, not the level of rates per se.

So, the question today is how Chairman Warsh will handle his desire to reduce communications compared to the previous actions of publishing the data and numerous FOMC members speeches. One thought is he may refuse to put his own forecasts into the document, a sign of what he wants going forward but I am confident he has other ways to move forward.

The other issue is the question of the tone of the statement, which had ostensibly been leaning dovish but seems now likely to be neutral. My sense is whatever he does, it will be incremental, at least at the beginning, but I anticipate that he is going to make substantial changes to the way the FOMC operates during his tenure as that is why he was put in the role.

So, with that as our backdrop, let’s see how markets have absorbed the text of the deal as we all await the FOMC this afternoon. Yesterday’s mixed US performance, with only the DJIA managing a gain while tech stocks dragged down both the NASDAQ and the S&P, was followed by more positivity than not in Asia with gains in Japan (+0.7%), China (+1.0%), Korea (+1.6%) and India (+0.5%) while HK (-0.75%) slipped a bit. It is always a bit of a surprise when HK and China move in opposite directions, and it seems today’s split arose from different interpretations from a policy conference regarding future PBOC activities as well as potential future government support for a clearly weakening consumer economy. Other regional exchanges had a mix of gainers and laggards as well, as the overall session was directionless.

In Europe, the picture is also mixed although the movement has been more muted than those in Asia. Both Germany and the UK are flat to slightly lower this morning with the former under pressure after BMW offered a terrible profit forecast while the latter, despite lower-than-expected inflation readings, is lagging on growth concerns. However, France (+0.2%) and Spain (+0.5%) have both managed to rally a bit on some slightly positive earnings news. As to US futures, at this hour (7:15), they are modestly higher across the board.

Bond yields are generally little changed this morning with only UK gilts (-5bps) and JGBs (-4bps) showing any movement at all. Gilts responded positively to the inflation data while JGBs seemed to take solace in the trade data showing Japan was back to a deficit.

In the commodity markets, oil (+0.7%) is having a very quiet session after several sharp declines in a row while metals markets are largely unchanged this morning. It appears even traders here are awaiting the FOMC outcome. One thing I have seen is a recent report from the World Gold Council showing 45% of central banks surveyed plan to buy the barbarous relic in the next 12 months.

And finally, the dollar is slightly stronger this morning, but like most other markets, not showing much movement at all. The below chart of the DXY for the past month shows just how lackluster price action has been with a total range of just 1.5%. The red line is the midpoint of that range showing there is just not a lot of pressure in either direction right now.

Source: tradingeconomics.com

Meanwhile, USDJPY has basically spent the past two weeks hovering just above 160.00 with nary a peep from the MOF or BOJ. Again, the situation there is the policy changes necessary to strengthen the yen are likely to have very negative economic consequences initially, and that is not something any government is likely to do.

On the data front, ahead of the Fed we see Retail Sales (exp +0.5%, +0.5% ex-autos) and then the EIA oil inventories with more draws expected. And that’s really all there is. I anticipate a very quiet session ahead of the Fed and then all will depend on how the market interprets Warsh’s signals.

Good luck

Adf

For a clear overview, your blog is now read daily. Excellent.

Thank you Elizabeth