The narrative right now is run

By hawks who think Warsh is the one

To raise short-term rates

Right out of the gates

And so, they’re long bucks by the ton

Thus, futures positions are huge

With no effort at subterfuge

But if they are wrong

About being long

The hawks will have all been the stooge

In an otherwise quiet session, this morning I am going to borrow from Ole Sloth Hansen, the futures maven at Saxo Bank. He publishes a Substack that is well worth reading if you are actively involved in the markets as he breaks down futures positions and offers context. This morning I am going to juxtapose those positions with my views, which are diametrically opposed to the way the market is currently positioned.

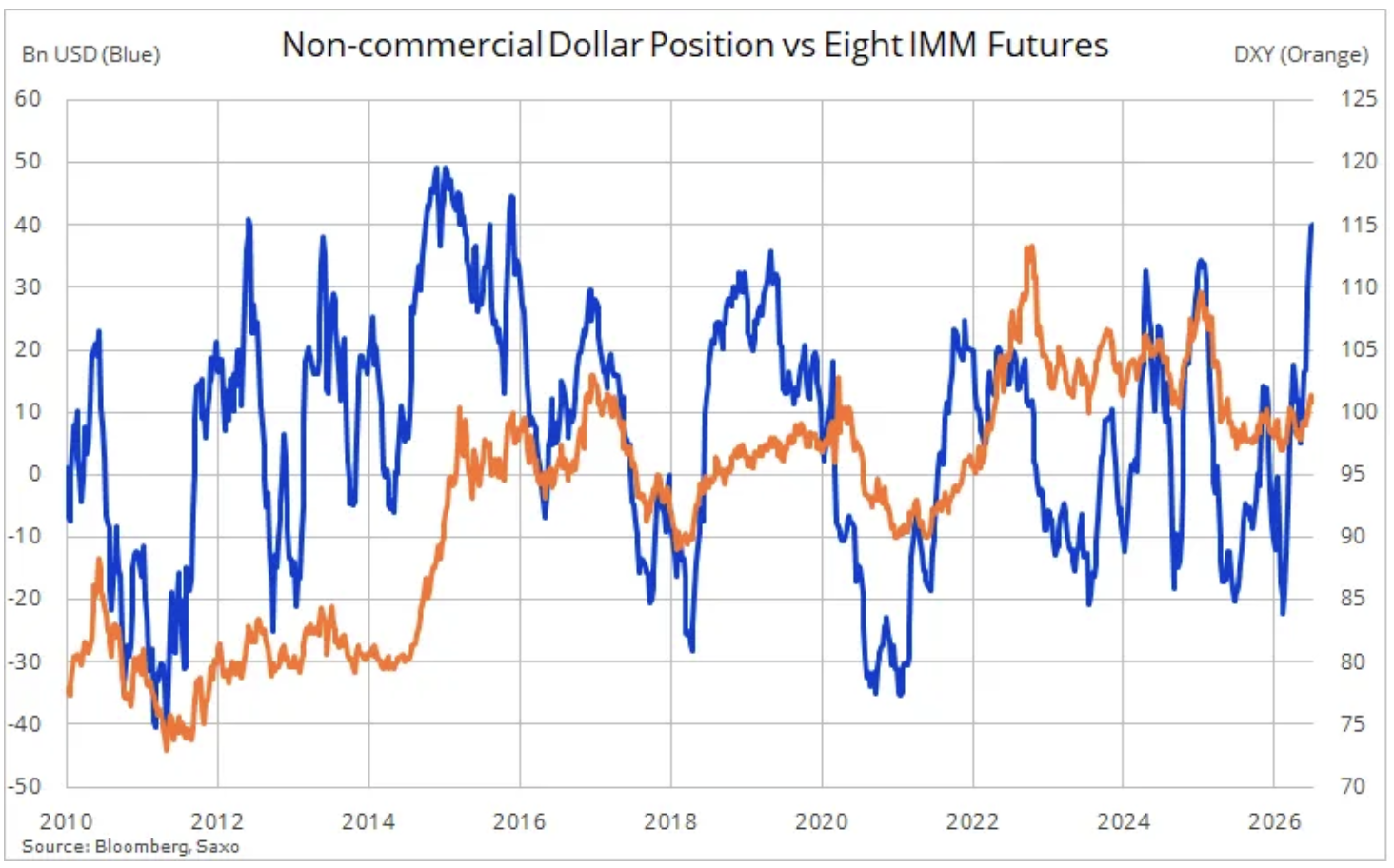

Starting with the FX market, he has created a wonderful chart showing that the net non-commercial long USD position against eight major currencies has reached 10-year highs. Interestingly, the DXY is not anywhere near those highs, although it appears that is the growing expectation of many traders.

Arguably, this is based on the idea that Chairman Warsh is Paul Volcker redux and will be quite hawkish going forward. Now, I cannot tell if this is the narrative because, absent forward guidance, narrative writers must now think on their own and are incapable of doing so, or if they truly believe that despite all the talk that rising oil prices were going to feed through to inflation readings, declining oil prices won’t have the same impact on the way down.

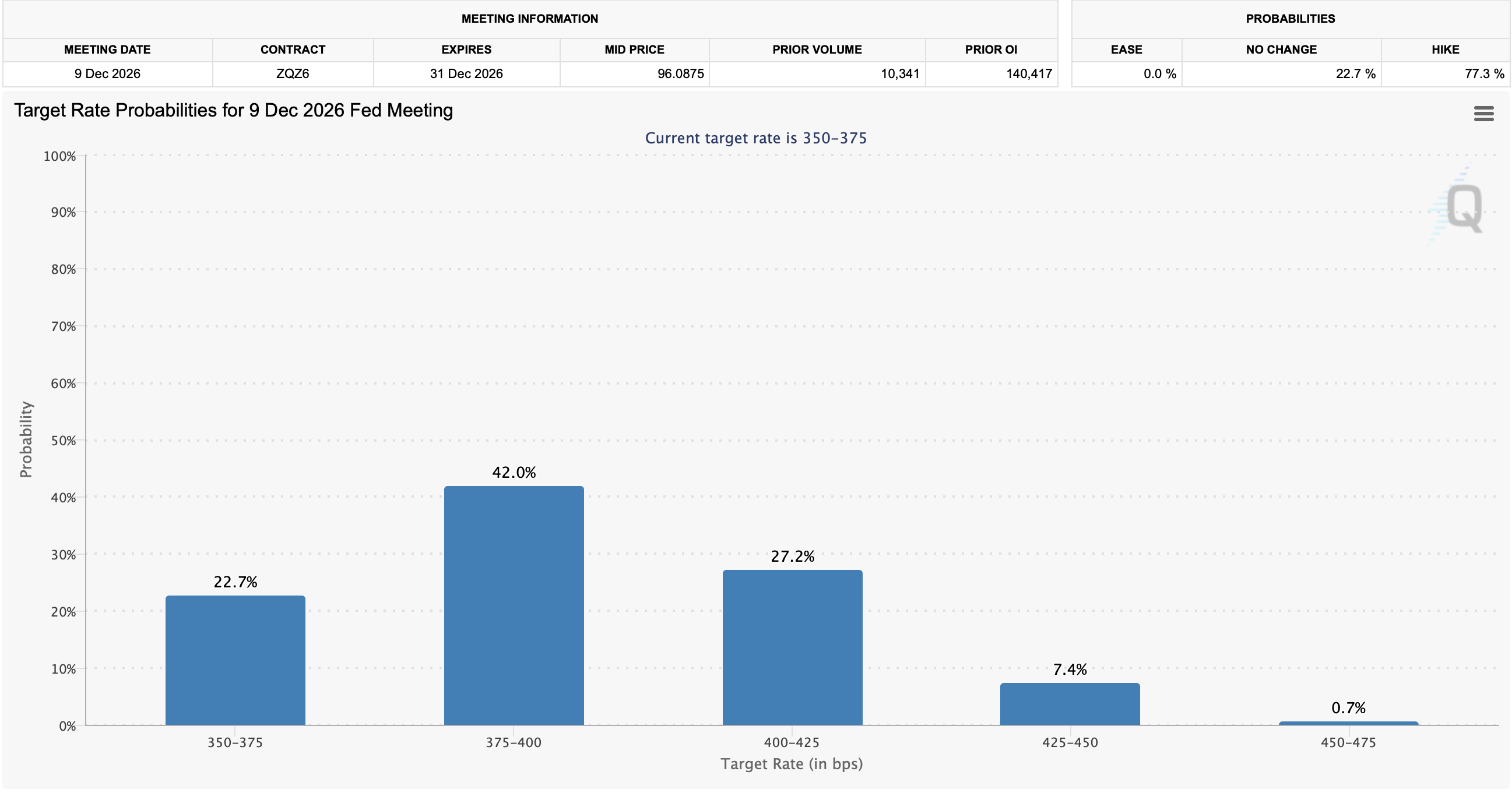

But it is not just the FX trading community that is on board with this story, so too is the short-term interest rate trading community. While LIBOR has been forced out of existence, SOFR (Secured Overnight Funding Rate) is the new benchmark in interest rate markets and, naturally, there is an active futures market there as well. As you can see from the below chart, also from Mr Hansen, the current positioning is strongly expecting higher short-term interest rates.

This is completely in accord with the Fed funds futures market where the market continues to price a 25% probability of a hike at the end of July and a virtual certainty of a hike by October. By my calculations, as per the chart from cmegroup.com below, the market is pricing about 30bps of rate hikes by the December meeting.

Or course, by now you know that my view is the Fed will not be hiking rates at all, and as measured inflation slides back (just look around the world and at oil prices) the narrative will belatedly shift to the need willingness to reduce rates on Warsh’s part and all these market positions will adjust.

My longer-term positive view of the dollar is based on the ongoing investment inflows into the US, for real investment, not merely equity market participation, and nothing has happened to change that view. In fact, the announcement yesterday by Toyota that they will be expanding their San Antonio truck and SUV plant with a $3.6 billion investment is just the latest in a series of these announcements. But that is not the carry trade driving things. In fact, ironically, we could easily see US rates slide a bit as the dollar rallies on natural investment demand rather than financial demand. As well, if I am correct, the Fed funds futures market is going to head back to pricing no rate hikes, perhaps as soon as next week after the CPI data is released.

I think the lesson is that the narrative writers need to bone up on their understanding of macroeconomics and international finance as the central bank policy driver may not be the future. Certainly, if Mr Warsh has anything to say about it, and he does, that will likely be the case.

Which takes us to the overnight session. The most excitement overnight was for Belgium as they completely outplayed the USMNT in a 4-1 victory in Seattle. But otherwise, the story that Iran fired two missiles at ships heading through Hormuz helped support oil prices, but as I type, they are higher by just 0.7% (~50¢/bbl) so not really very much. The interesting discussion in the oil market this morning is the fact that Iranian oil, which is no longer sanctioned, cannot seem to find any buyers with some 58 million barrels in floating storage and no takers. Meanwhile, despite ongoing buying by central banks around the world, gold (-0.5%) continues to struggle, although appears to be putting in a base and silver (-1.4%) is suffering as well.

In the bond market, yields are creeping higher with both Treasuries and European sovereigns all higher by 2bps this morning with a similar move by JGBs overnight. My take is this is less of an inflation concern than a supply concern. Certainly, there is no indication that the US, Europe or Japan are about to slow down their fiscal stimulus, with Europe now further ramping up its defense spending as the US pressures NATO further. To me, this is where the rubber will meet the road as if Warsh really does seek to reduce the Fed’s balance sheet, it is not clear where buyers are going to be found to replace them. I suspect we will see more regulatory freedom for banks and insurance companies to hold Treasuries without capital penalties, but that is a big hole to fill.

In the equity markets, yesterday’s US rally was followed by a reversal in Asia with Korea (-4.9%) leading the way lower on the back of weakness in SK Hynix stock despite stellar earnings. But that dragged down the entire region (Japan -2.1%, China -1.0%, HK -0.5%, Taiwan -2.3%) and various declines everywhere else except Singapore (+1.4%) although I can find no specific catalyst for that outlier move. In Europe, things are more mixed with Germany (-0.7%) under pressure although there is modest strength in the UK (+0.3%), France (+0.2%) and Spain (+0.1%). All the talk here is about defense spending, although one would have thought that would help Germany the most. As to US futures, at this hour (7:55), NASDAQ futures are following Asia lower, -1.3%, but the other indices are little changed.

Finally, the dollar is generally a bit stronger this morning, at least against its G10 counterparts, although JPY (+0.1%) is holding up. But the dollar’s gains are minimal, about 0.1% to 0.2%, so it is difficult to get too excited. In the EMG bloc KRW (+1.0%) is the clear leader after the country expanded trading hours in the currency markets, and there has been modest strength in BRL (+0.4%) and INR (+0.4%) although neither has seen any major policy changes.

On the data front, yesterday’s ISM Services data was right on the button at 54.0. This morning we see the Trade Balance (exp -$78.5B) and that’s it. The hawkish Fed story continues to be the most popular, and until we see some data that can undermine that story, I expect it will remain in place. Tomorrow’s FOMC Minutes should be interesting as there was obviously a lot of back and forth at the meeting, but since we have already heard further from Mr Warsh, and it is way too early to hear back from the task forces, I suspect we are in for more quiet markets for now.

Good luck

Adf