The market response was, at first

That things moved from bad to now worst

But by session’s end

The short-term downtrend

Was over, completely reversed

The narrative now making rounds

Is by starting naval lockdowns

Trump’s turned Iran’s table

And thus, may be able

To finish the goal he expounds

The irony, to me, of the entire Iranian situation is that, generically, the US shouldn’t need to care about Iran anymore. Back in 1979, when the US imported a majority of its oil, everything in the Middle East was critical for the economy as a whole, and therefore politically. But that is no longer the case, and if the Iranian leadership had simply wanted to repress its own people and espouse its Muslim fundamentalism, without sponsoring terrorism around the world, Iran would have faded from the view of the US establishment. While there would have undoubtedly been some who would say it was a terrible humanitarian crisis, and the US should do something about it, unfortunately those situations are rampant around the world.

Don’t get me wrong, I think the Iranian regime has been one of the cruelest and most repressive on the planet, I’m simply highlighting that to the US, it was an oil source throughout history. Now that it’s no longer a key oil source for the US, it has no political constituency in the US. And yet, here we are with 3 aircraft carrier groups in the vicinity doing incalculable damage to the nation because that leadership was not satisfied to simply repress its own people but felt it was their mission to destroy other nations, notably Israel and the US. That’s all I will say about the rationale for the current events.

But speaking of current events, it seems that President Trump’s decision to blockade the Strait of Hormuz has shown early signs of being quite effective. Two stories have made that point, first that the Chinese have suddenly made their first comments about the war, explaining that free navigation through the Strait is an imperative and second, that the Iranians appear to be quite interested in a second set of discussions after the ones last weekend fell apart.

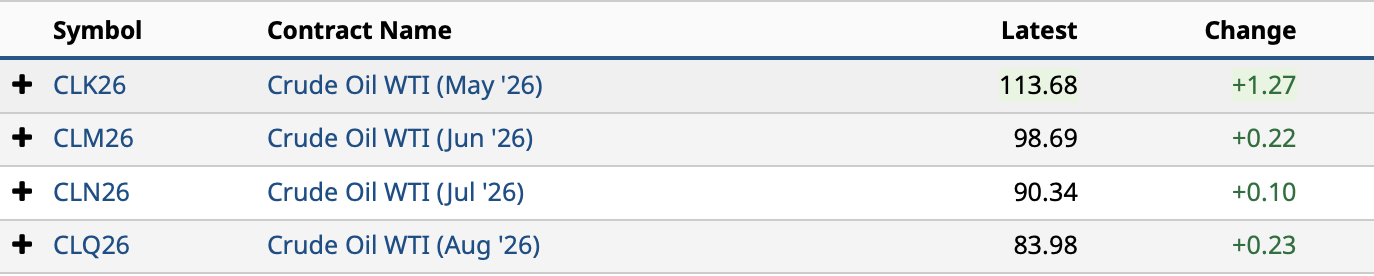

The interesting thing about markets is their ability to anticipate the way things work out, as despite the early panic over the weekend regarding the talks failing and the blockade being enforced, price action yesterday was entirely positive, reversing all the Sunday night fears. Once again, the oil chart for the past week shows the continued ups and downs, with the latest leg back down. This morning, WTI is lower by a further -2.3% and back well below $100/bbl.

Source: tradingeconomics.com

In truth, we cannot be surprised at either of these stories as the Iranian leadership knows it cannot live without its oil exports, nor the Chinese without its access to that oil. While it is still unclear how things will evolve from here, a successful conclusion of the war, with Iran giving up its enriched uranium and pledging to stop trying to go nuclear is seemingly closer to fruition than before all this started. Certainly, the market believes that is the case given the S&P 500 has traded back above its pre-war level and is now within 100 points of its all-time high just above 7000.

Source: tradingeconomics.com

And here’s the thing about the oil market. As we know, every shortage is followed by a glut. Every non-Gulf producer has been going full bore since this began and oil prices spiked, and this was alongside the massive releases from strategic petroleum reserves around the world. If you add up the amount of oil that is sitting in tankers in the Persian Gulf, along with the amount that is in storage there, and the amount of both Russian and Iranian oil that had been in transit and unsanctioned, the numbers are staggeringly high. The math I saw from Alyosha (Market Vibes) is somewhere around 600 million barrels are going to come flooding into the market in fairly short order once the Strait is reopened, and it will be reopened, of that I am certain. At the same time, the war has reduced revenues of the gulf nations for the past 6 weeks, and they will want to be pumping as much as possible, at any price (remember, in Saudi Arabia, the cost per barrel to pump oil is estimated to be between $3 and $6, so $30/bbl oil is still profitable.). While this is not an investment discussion nor advice of any type, I have exited all my oil focused positions at this point.

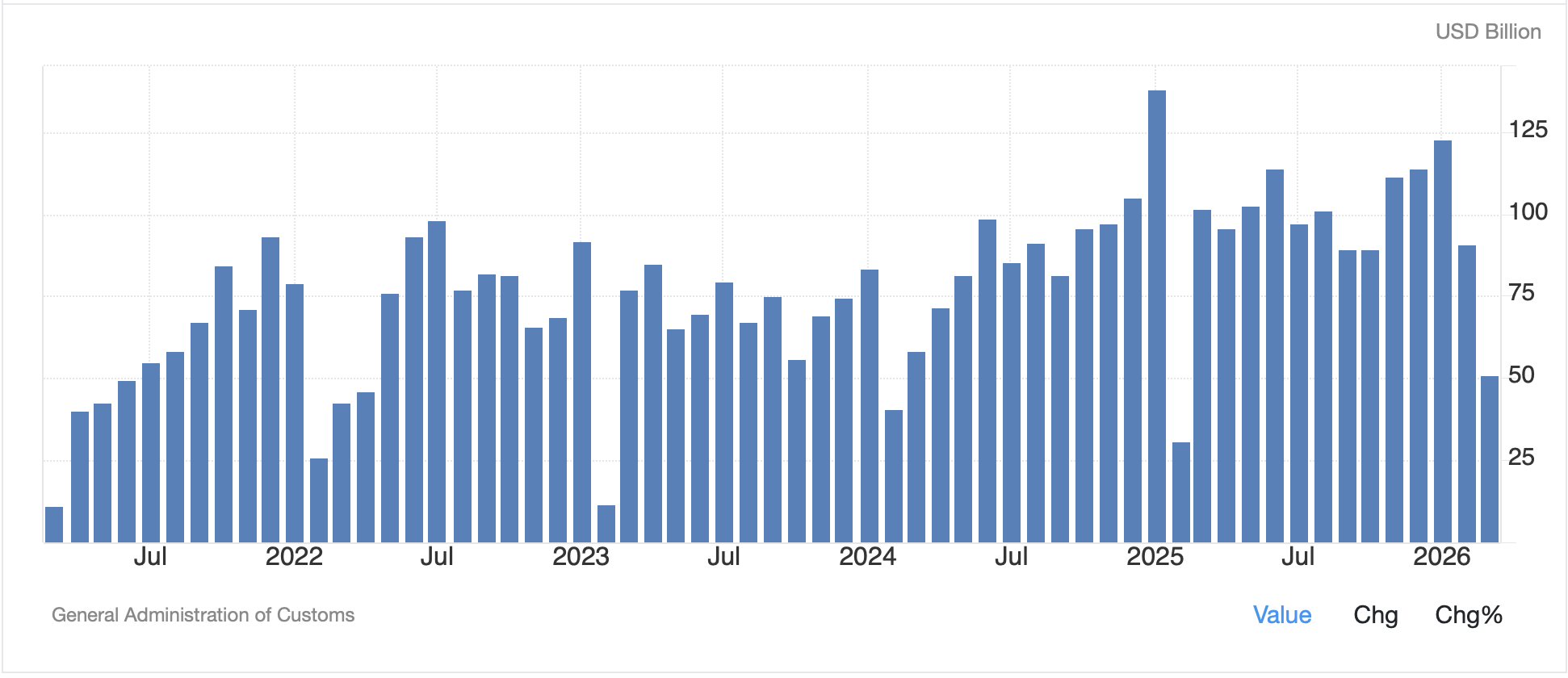

There is another related story here as well, this about the Chinese economy. Last night they released their trade data, and it was substantially worse than expected. As you can see from the chart below, the surplus barely topped $50 billion, compared to a consensus estimate of $112 billion with not only a massive increase in imports, 27.8% and likely highly energy related, but a significant decline in exports, just a 2.5% rise there. Again, if you wonder why suddenly President Xi is interested in reopening the Strait of Hormuz, the fact that it seems to be having a direct impact on the Chinese economy is one of the reasons.

Source: tradingeconomics.com

(A note about the data above shows that each February, the export numbers decline as a result of the Chinese New Year celebrations but always rebound strongly in March. And this was March data released that fell so sharply, a far more concerning outcome for Xi.)

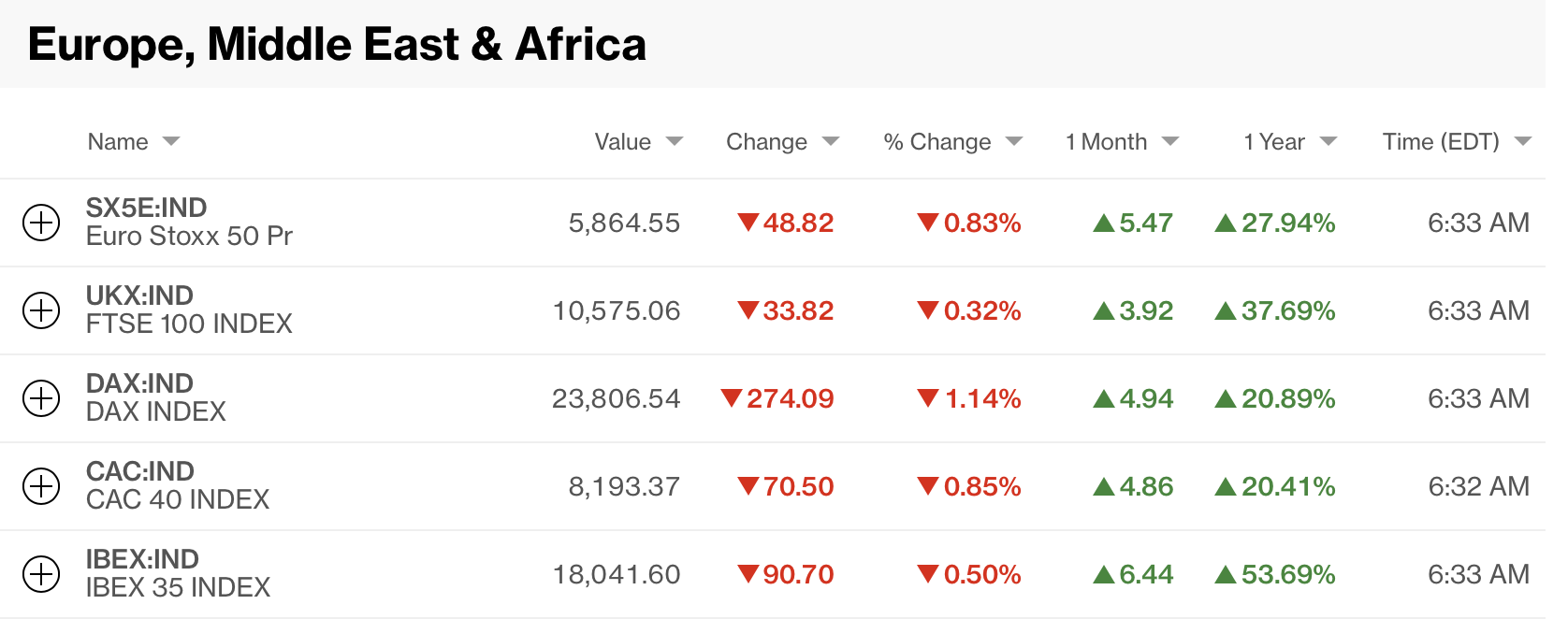

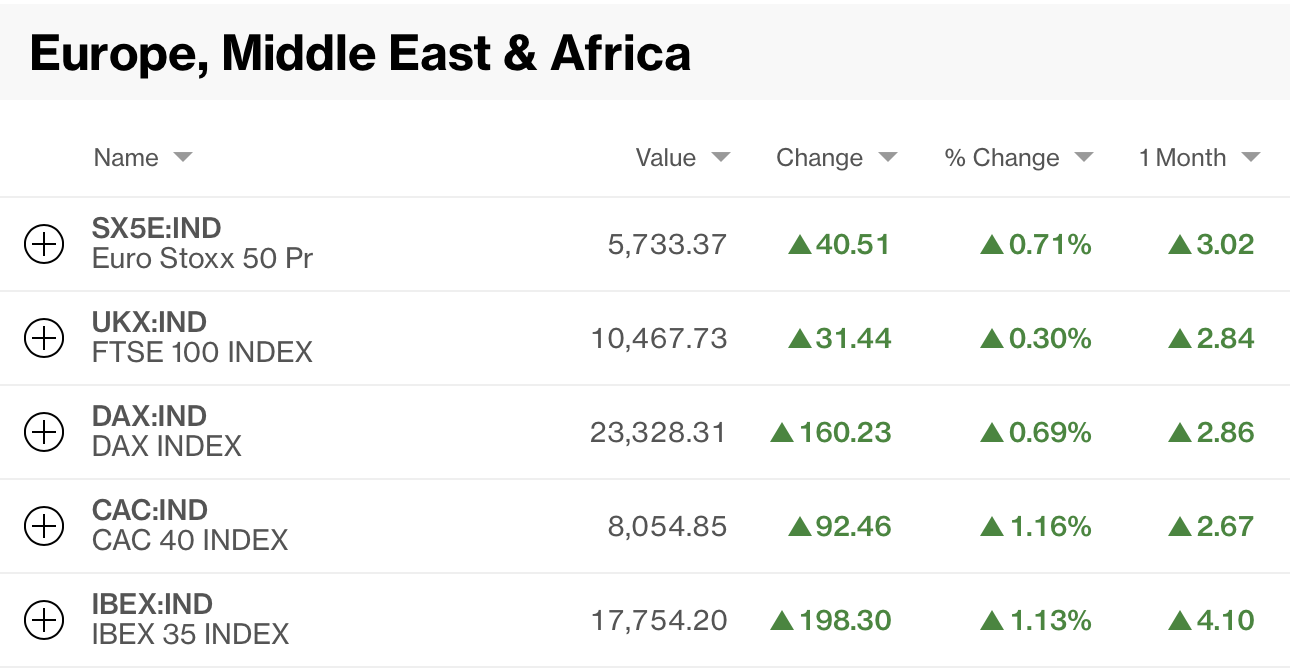

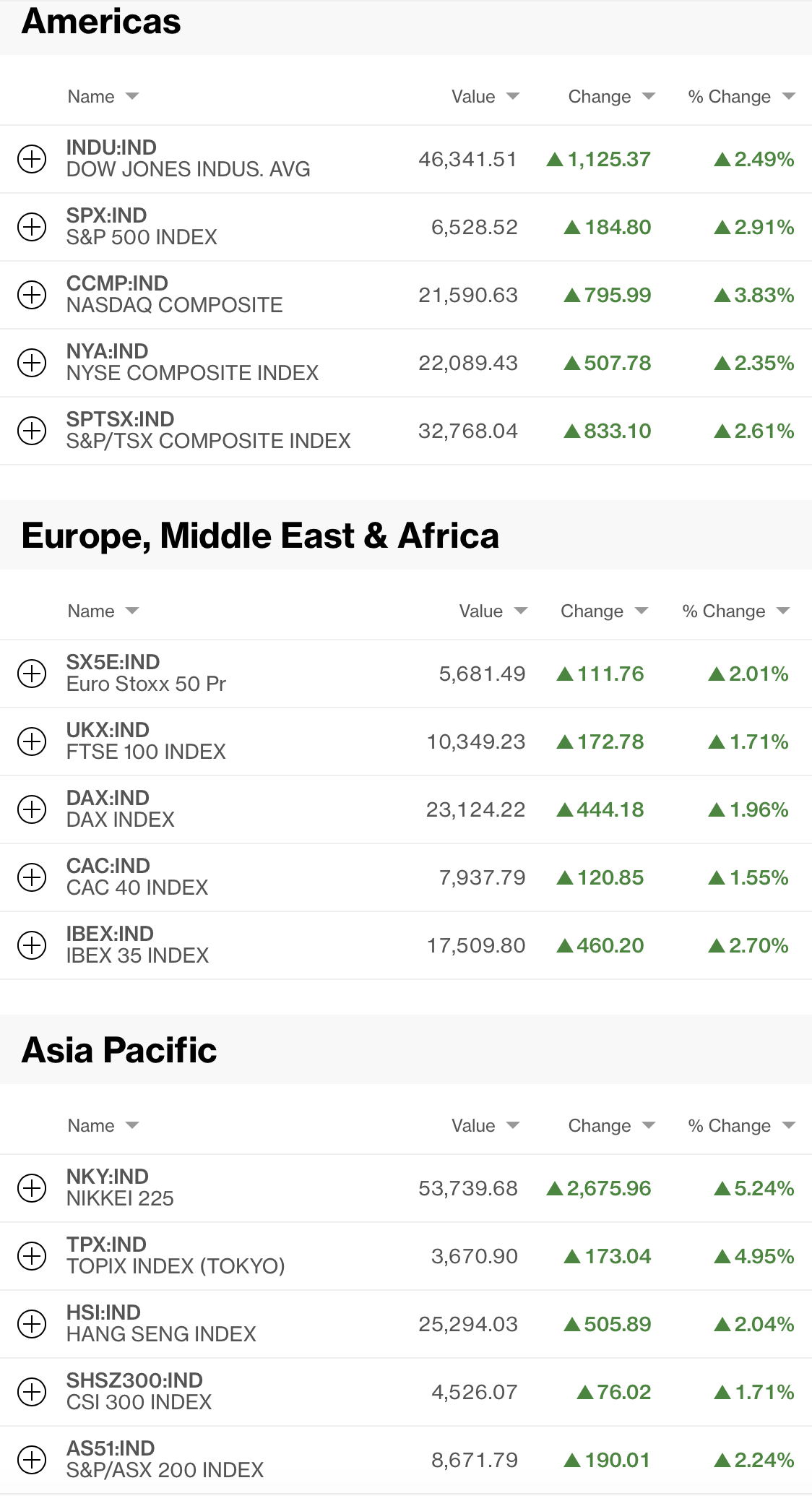

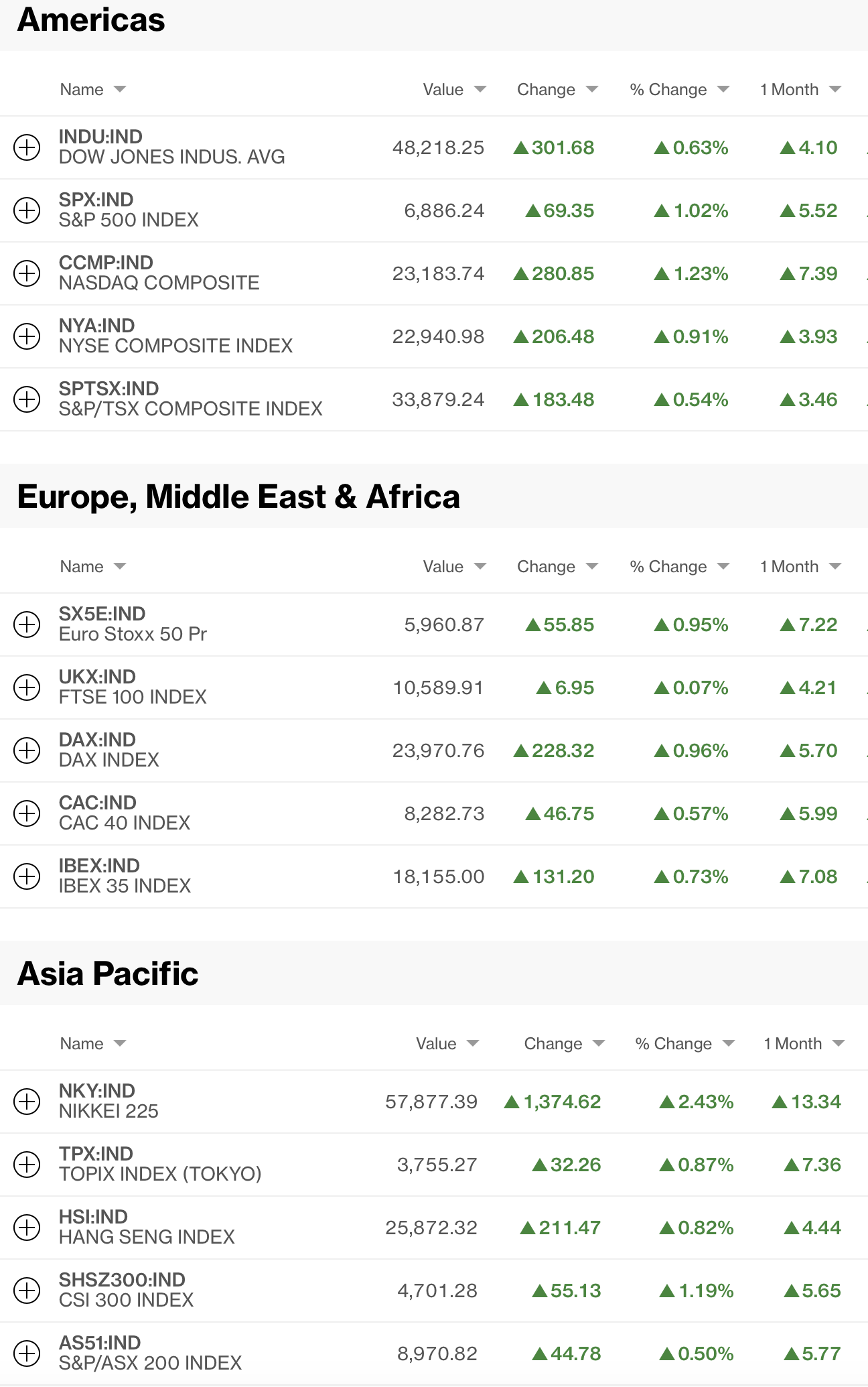

So, with all this in mind, how have other markets fared? Well, equity investors around the world are over the moon as you can see from the Bloomberg screen shot below. ‘Nuff said.

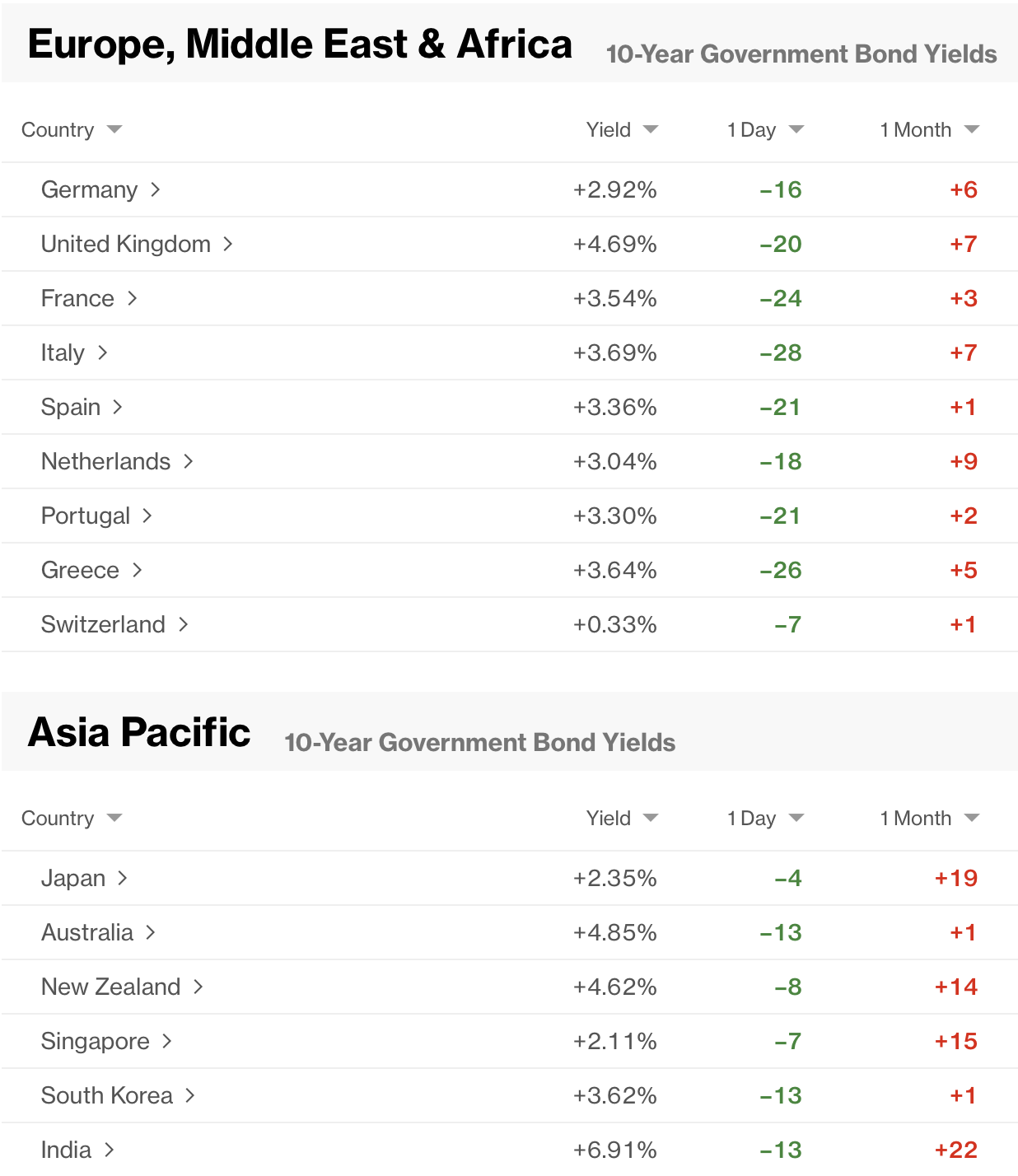

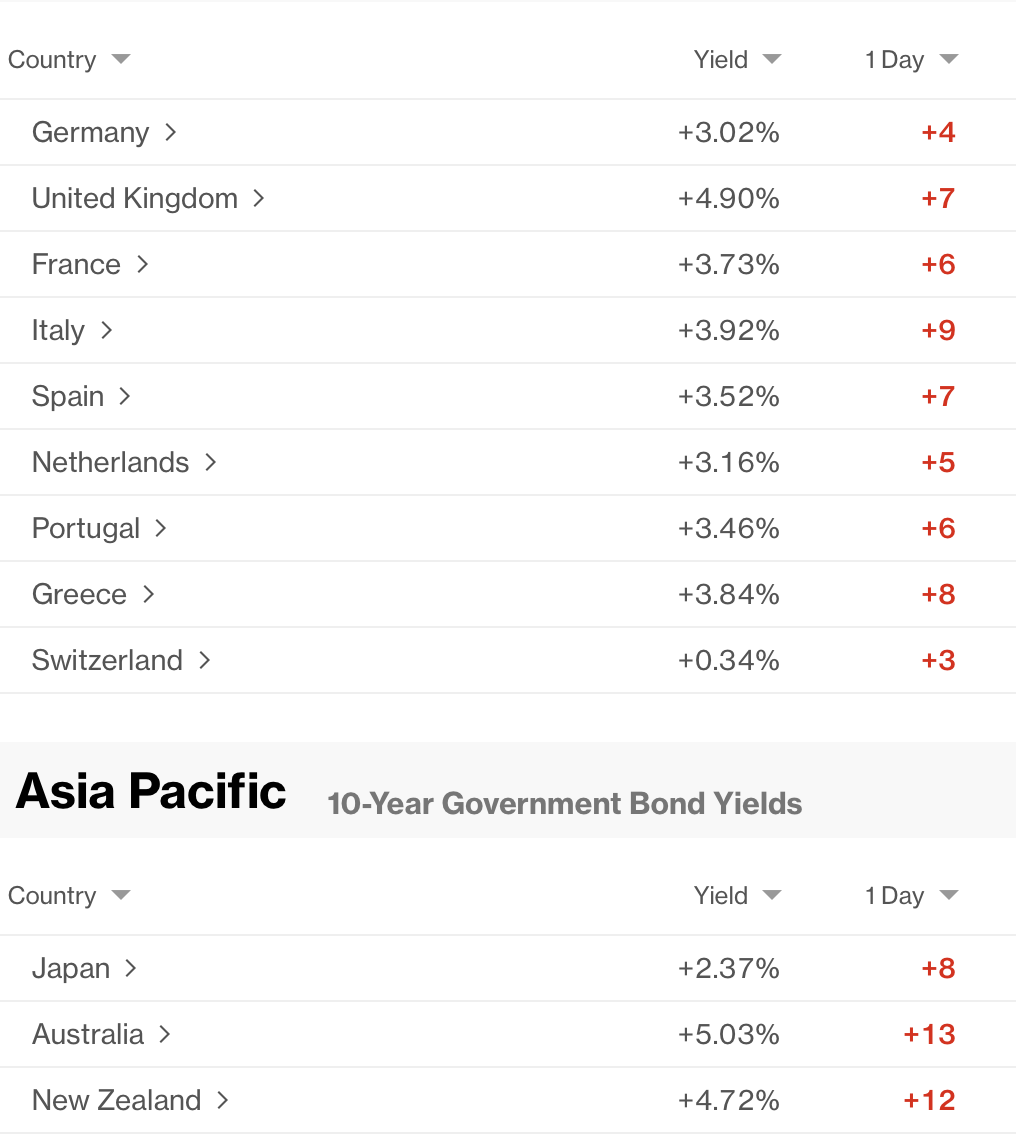

Bond yields have also fallen across the board as the decline in the price of oil, plus the idea that the war may end sooner than some had expected, thus reducing the inflationary pressures greatly, has bond investors grabbing for yield. Yesterday saw Treasury yields slip -2.5bps though this morning they are unchanged. In Europe, sovereign yields are all lower by between -3bps and -6bps while JGB yields fell -4bps overnight with even larger declines in the rest of Asia. Fear is clearly not a factor this morning.

It should not be surprising that precious metals prices have rallied as well, between lower yields and a growing belief that forced sales have stopped. So, gold (+0.5%), silver (+2.5%) and platinum (+0.5%) are all having a good day. But so are the base metals with copper (+0.8%) not only recouping its war-related losses, but actually back within spitting distance of its all-time highs set in January above $6.00/lb.

Source: tradingeconomics.com

Finally, the dollar is giving back more of its war-related gains and lower across the board this morning, with G10 currencies gaining on the order of 0.3% to 0.4% across the board, while EMG currencies show similar gains with one major outlier, INR (+1.4%) easily explained by the fact that India has been the hardest hit economy from the war, and so the prospects it is ending have had a very beneficial impact on the rupee. But to be clear regarding the dollar, all we have seen is that it has moved back to the middle of its yearlong trading range between 96.50 and 100.00 based on the DXY as per the below.

Source: tradingeconomics.com

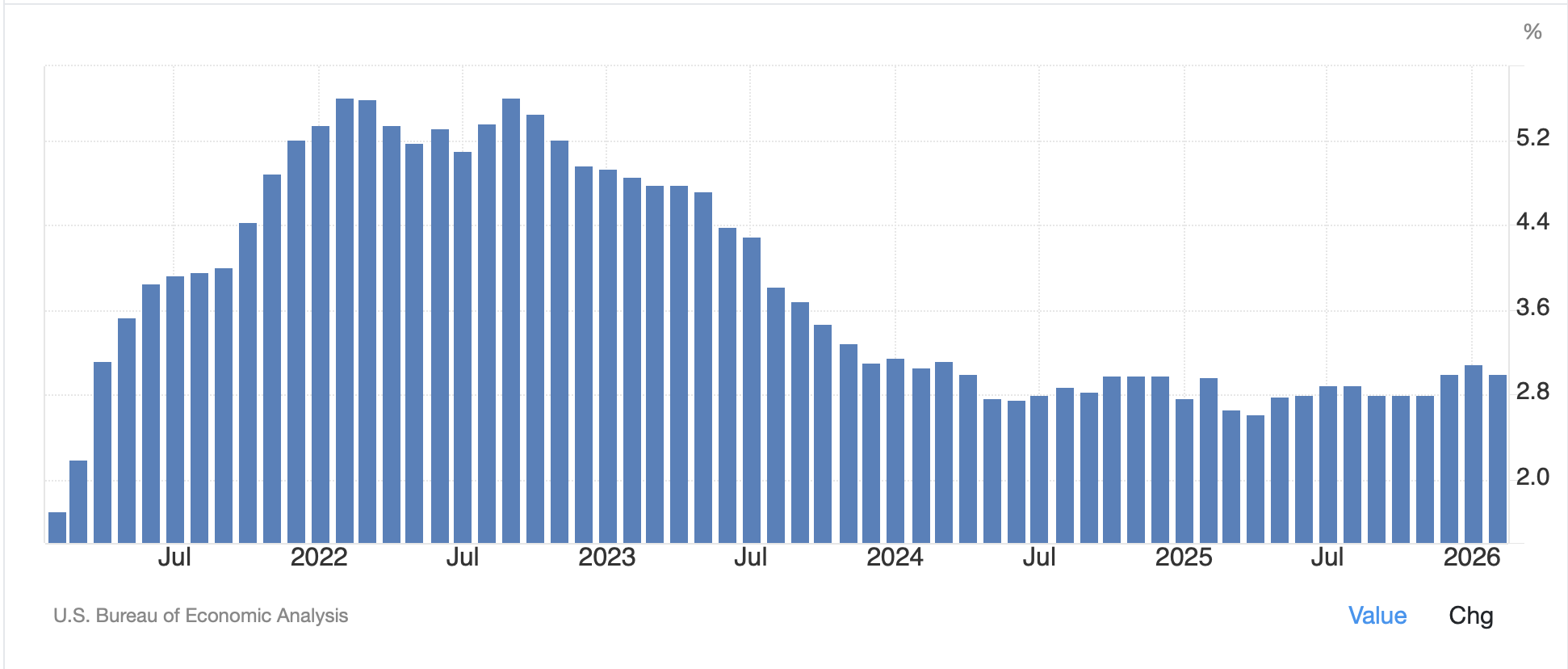

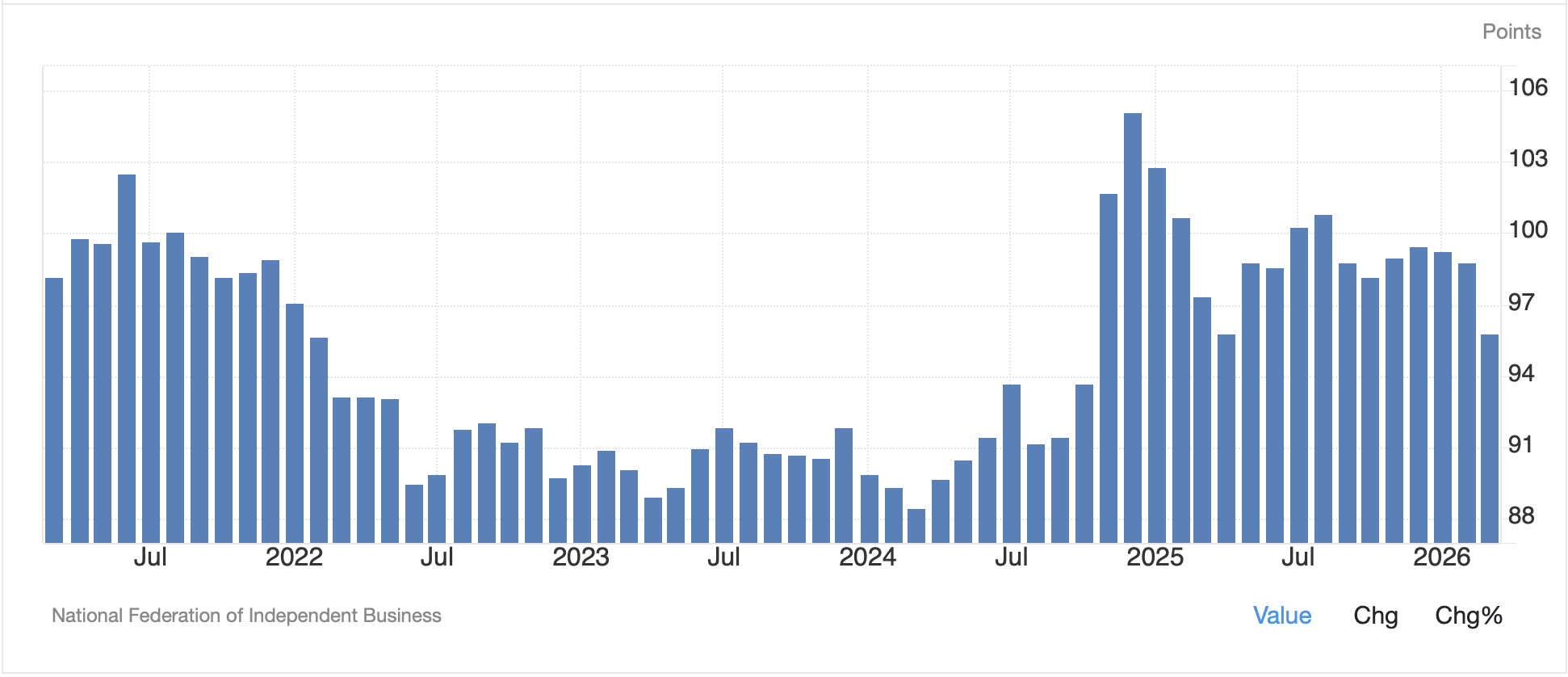

On the data front, yesterday’s Existing Home Sales numbers were weaker than forecast and many pundits have been claiming that as a signal of much greater economic weakness. We shall see. This morning we have already seen the NFIB Business Optimism Index released at a weaker than forecast 95.8, not a great sign, but as you can see below, still well above levels of a few years ago.

Source: tradingeconomics.com

We also get PPI (exp 1.1% M/M, 4.6% Y/Y headline, 0.5% M/M, 4.1% Y/Y core) and a few more Fed speakers. With CPI already having been released, PPI loses much of its luster, although it helps economists estimate PCE a bit better. One cannot be surprised that Governor Miran explained he expected to see inflation back to target by this time next year, but I am not holding my breath for that outcome.

Summing it all up this morning, risk is back baby!!! If ever you were curious about whether markets anticipate events, today is exhibit A. I certainly hope the market is correct and we are about to wind down the Iran war but be wary as it ain’t over til it’s over. If it has ended, look for previous narratives to be resurrected regarding markets, notably the dollar’s demise, but I am not holding my breath over that either.

Good luck

Adf