In England and Scotland and Wales

Without getting into details

The PM has lost

Support, and will be tossed

But Labour, so far’s, moved like snails

Until the time comes when he’s gone

And Keir reaches his denouement

Both gilts and the pound

Will fall toward the ground

But they’ve no one to settle on

While the stalemate in the Gulf continues, although there is clearly less optimism that things are going to end quickly according to the oil market (+3.0% and back to $101/bbl), there are a few other things that are ongoing in the world that are impacting markets. This morning, the most obvious is in the UK, where PM Keir Starmer, he of the <20% approval rating, is seeing his grip on power slip away, but like most politicians, he will hold on as tightly as possible for as long as possible regardless of the negative impact that has on his constituency, which in this case is the entire nation.

For instance, a quick look at the gilt market shows that yields there, this morning, have jumped 12bps in the 10-year, up to their highest level, at 5.11%, since April 2008, as per the below chart from marketwatch.com.

Perhaps, of more concern for the UK Treasury and the BOE is the fact that the spread between US Treasuries and UK Gilts has jumped 9bps this morning and, at 67bps, is now pushing back toward its upper quartile, also not seen since 2008 as per the below chart from worldgovernmentbonds.com.

The pound (-0.5%) is faring no better this morning, lagging the rest of the G10 while UK stocks suffer alongside with the FTSE 100 (-0.6%) adding to the overall pressure on Starmer.

Now, in fairness to poor Keir, he has failed in essentially every aspect of government, notably as to his promises when elected, so this cannot be a surprise. The question becomes; how much longer will he try to fight this very clear outcome to the detriment of his nation? From a fiscal perspective, I imagine he will be seeking to offer money to specific constituencies in an effort to buy more time, but my take is the die is cast here. For now, I expect UK assets and the pound are going to underperform and likely will until he is gone, regardless of his replacement.

However, aside from the war in Iran, where there is nothing new of note today, the next biggest stories are that President Trump is on his way to Beijing to meet with President Xi and this morning’s CPI report. Since I can offer nothing of note on the summit meeting, let’s turn to inflation.

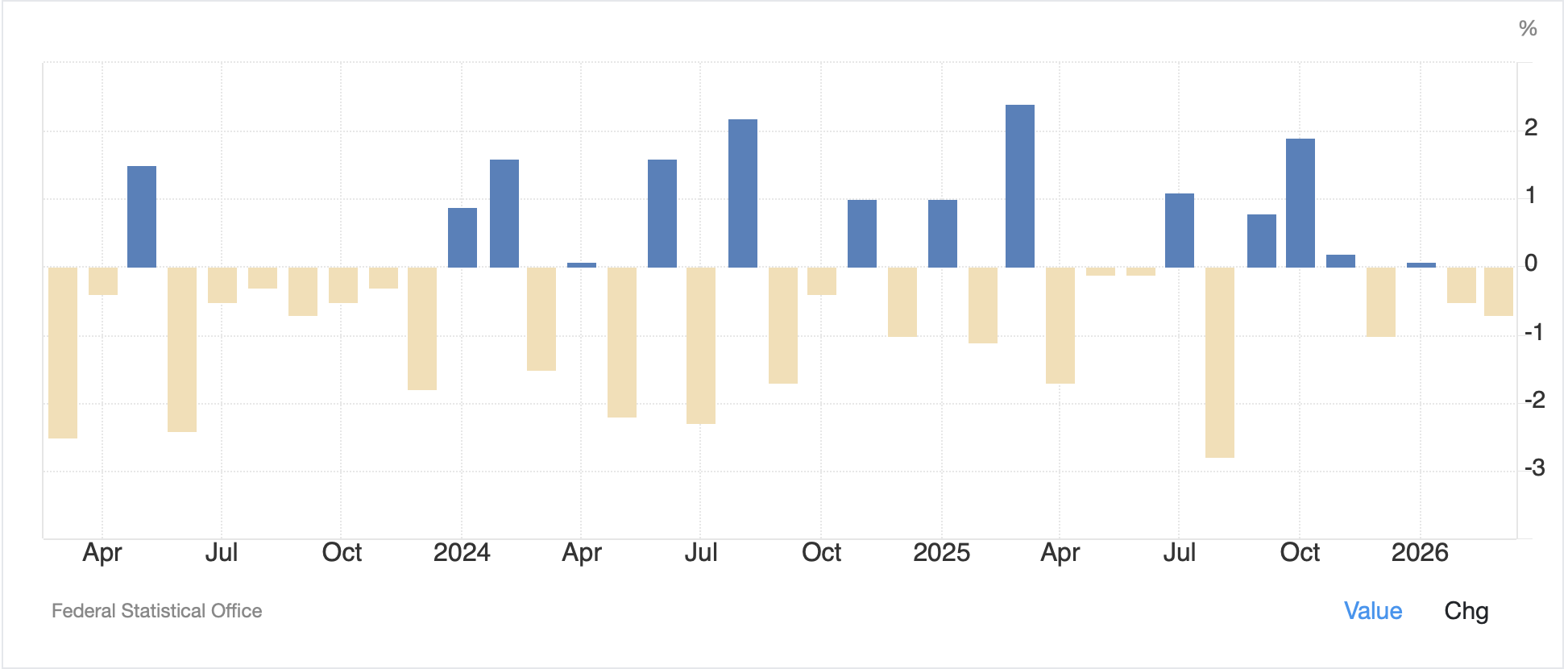

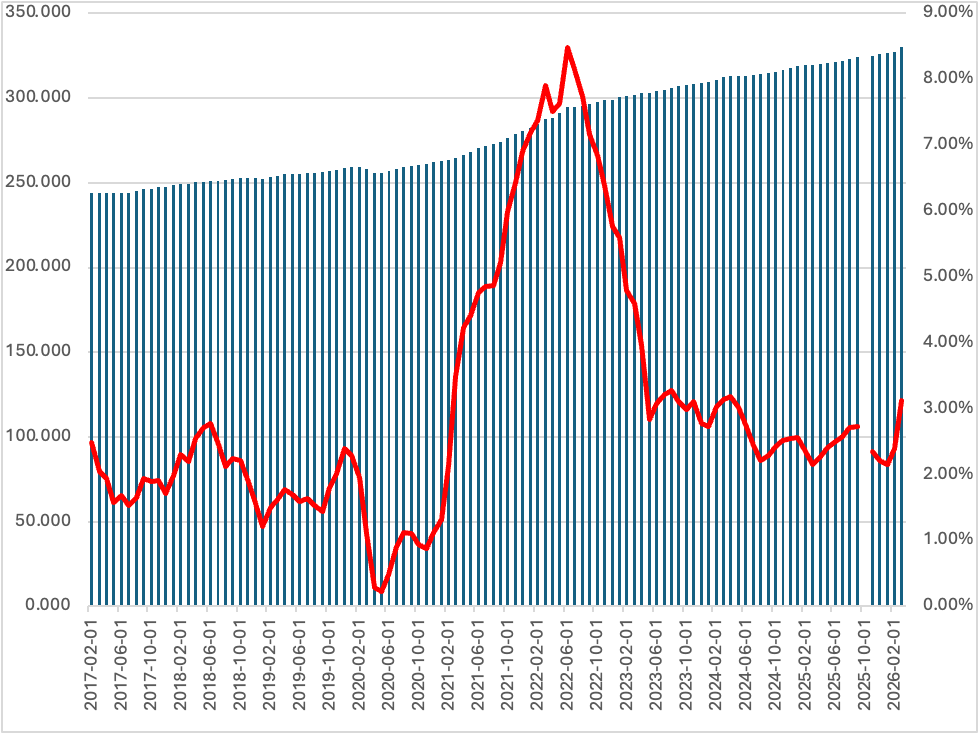

Expectations this morning are for the headline number to print 0.6% M/M and 3.7% Y/Y while the core (ex-food & energy) number is expected at 0.3% M/M and 2.7% Y/Y. Below is a chart showing headline CPI for the past 10 years, which I believe is informative of the national mood. In it, you can see both the annual rate of inflation (the red line, RH axis) and the steady growth of the underlying CPI index published by the BLS (blue bars, LH axis). To get the full sense of things, though, make sure you look at the index level on the left, which has grown, in aggregate, 38.7% over the past 10 years. It is this feature which drives the nation’s unhappiness with prices, I would contend, not the monthly data, but the cumulative nature of the problem.

Data: Fred, graphics: @fx_poet

All of us remember the peak inflation in the immediate post-Covid years. In addition, I’m sure we all remember the government shutdown and the missing data point because of the inability to collect data and the known assumption that if data were not collected, it would be assumed to be 0.0%. Well, not only is the Iran war having a direct impact on inflation, but that missing data is starting to leave the calculations, so the red line is going to continue to head higher. I must admit, that if I were to guess how things arise this morning, I would suspect the estimates to be on the low side, but we shall see in a few hours. The question here is; will the markets respond to this or are they focused on other issues? I also suspect that this depends on the outcome. If CPI is higher than forecast, it does not bode well for Treasury prices, nor likely stocks. But, if it is softer than forecast, I would look for the equity rally to continue.

Ok, let’s see how markets are behaving as we await the data. Yesterday’s nondescript and modest US rally was followed by a lot of nondescript trading in Asia (Tokyo +0.5%, HK -0.2%, China -0.1%), although both Korea (-2.3%) and India (-1.9%) had a bit more action with the former seeming a reaction to its recent moonshot rise while the latter continues to try to deal with a steadily weakening currency and the government’s efforts to address that without raising interest rates. Otherwise, in the region there were both winners and laggards but nothing else noteworthy.

In Europe, though, red is the only color I see with the DAX (-1.1%) leading the way down despite a better than expected, although still negative, ZEW report of -10.7. But Spain (-0.9%), Italy (-0.8%) and France (-0.6%) are all under pressure with only Norway (+0.6%) showing any life as its energy-centric market performs well with oil prices back up again this morning. As to US futures, they, too, are red with the NASDAQ (-1.1%) the worst of them at this hour (7:10).

We’ve already discussed Gilt yields but yields around the world are higher this morning with US Treasuries (+2bps) adding to yesterday’s 5bp rise. In Europe, and in Japan, yields are higher by 4bps to 5bps across the board. This appears to be a combination of concerns over both increased supply as nations spend more than they tax and rising inflation. It’s a pretty toxic combination for bonds.

Yesterday was a bit of an anomaly in the precious metals markets as despite the rise in oil prices we saw, gold, silver and copper all rally as well. Recently, we would have expected the metals to trade lower in that circumstance. And this morning, with oil (+3.0%) higher again, they are with gold (-0.9%) and silver (-3.3%) both under pressure although copper (+0.4%) continues to rise to new records. It turns out, the electrification of everything, and the massive power requirements for data centers along with rebuilding aging electricity grid infrastructure will require a lot of copper, likely more than will be mined at the current prices. It feels like this chart will continue to go higher.

Source: tradingeconomics.com

Finally, the dollar is back in form this morning against virtually all its counterparts in both the G10 and EMG blocs. In fact, it is easier to discuss the outliers which are NOK (+0.3%) and BRL (+0.4%) both benefitting from rising oil prices (as is the dollar!) while the rest of the world collectively suffers. The DXY (+0.35%) continues to ignore all the calls for its collapse and today’s weakest performers are KRW (-1.0%) and ZAR (-0.6%). The latter continues to be buffeted by the combination of higher oil and lower gold prices, although remains well above the lows (below dollar highs) seen at the beginning of the war that started this price action as per the below chart.

Source: tradingeconomics.com

KRW, though, is a bit more confusing to me as while weakness overnight alongside the KOSPI, makes sense, it has, in truth, performed terribly compared to the KOSPI’s remarkable rally. It would have made a great deal of sense to see significant foreign inflows to the won as investors jumped on that bandwagon, but I guess not.

There is nothing other than the CPI data released in the US this morning so that will be the driver for now. I would be remiss if I didn’t highlight, again, that the best way to manage inflation risk for us all is to own USDi, the fully backed, inflation-tracking cryptocurrency that is returning 12.588% annualized this month and depending on the exact CPI print this morning, set to return something on the order of 8% or so in June. Remember, Treasury bills return 3.6% annualized, so this is a way to keep up with prices. Check out www.usdicoin.com for more information and the ability to mint your own!

Good luck

Adf