Said Trump, come next Friday I’ll sign

A deal, and though many malign

The war with Iran

It’s all gone to plan

As they’ve lost their arms and their spine

Thus, oil has fallen in price

While gold and stocks rose in a trice

With bears in retreat

For Trump’s next great feat

Some midterm success would be nice

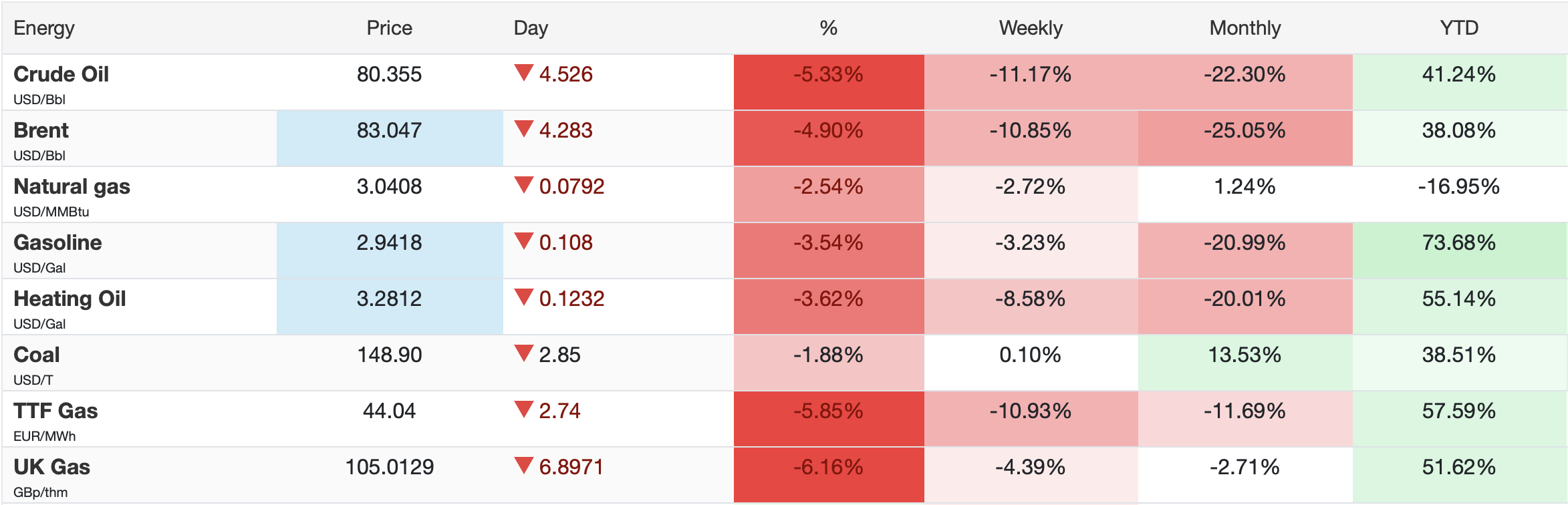

This is a look at the major energy futures markets according to tradingeconomics.com at 5:15 this morning

Sharp declines on the session in the wake of the announcement, confirmed by the Iranians, that a deal had been struck and that the Strait of Hormuz would be reopening by Friday after the mines are cleared. And while there has been much discussion over the past week, as you can see in the far-right column, energy prices are still largely higher year-to-date with only NatGas the exception.

To my mind, the question becomes, just how quickly prices continue to decline, and can gasoline prices, the one that matters most to the US consumer, slide back to the $2.00/gallon level that we saw prior to the war?

As you can see from that chart below, it still has a long way to fall, but if the Strait remains open, I suspect it will round trip by the end of the summer, just in time for people to start considering their voting habits.

Source: tradingeconomics.com

Remember this, as well, how much have you heard about Venezuela lately? Back in January, less than six months ago, the US captured and remanded Nicholas Maduro into custody and the world was up in arms. I would wager that most people don’t even remember it happened! Memories are very short for global events like this (consider the fact that the Russia – Ukraine war continues and it never even makes the proverbial papers anymore). For President Trump, the outcome of this situation will be a massively degraded Iranian military with pretty much the rest of the GCC aligned against everything they stood for, an economy that continues to demonstrate remarkable resilience, high stock prices and the likelihood that inflation, as oil prices slide, will be heading back closer to the theoretical 2% target.

There once was a time central banks Were saviors, and we would give thanks For all of their aid When, problems, they slayed And bankers, they all would close ranks But last week the ECB raised Tonight, Ueda-san will be praised For hiking rates too So, what will Warsh do? On Wednesday when his trail is blazed? Meanwhile, we are in the midst of the monthly central bank onslaught as last week, Madame Lagarde and the ECB raised their base rate by 25 basis points, blaming the ongoing rise in oil prices for leading to inflation. Of course, 96 hours later, with the announcement by both sides of a deal to end the Iran conflict, this is likely to be seen as an error, the full Trichet as it were.

Tonight, the BOJ meets and all signs are that they, too, are going to be hiking rates by 25bps tonight, to 1.00%, which you will have heard is the highest in more than 30 years. It’s funny, the official inflation data from Japan is showing a reading of 1.4%, below their target, and now that the prospect of oil prices falling more sharply has increased, it feels like they may be on the cusp of an error here as well. Consider that of all the governments around, the Japanese with a debt/GDP ratio of about 250% is the nation least able to absorb higher interest rates.

Which takes us to Wednesday’s FOMC meeting, the first under Chairman Warsh. There is a long Nick Timiraos article this morning in the WSJ ostensibly explaining that Warsh would like to see less Fed communication, including killing the dot plot, and have the cacophony of Fed speakers shut up. First, Timiraos has real skin in this game because while he was Powell’s go to, I doubt he will be Warsh’s, thus Timiraos’s status is about to be hit hard. In fact, the article read as though Powell was writing it to make it seem as though Warsh’s ideas are all wrong.

Personally, I am in favor of less communication by the Fed as policy uncertainty will result in significantly reduced positioning in the speculative community and that is a net benefit for the rest of the market. Plus, if there is a hiccup, there is less reason for a bailout. We shall see. It seems highly unlikely that they move on Wednesday, but we should at least get an inkling of how things may evolve going forward.

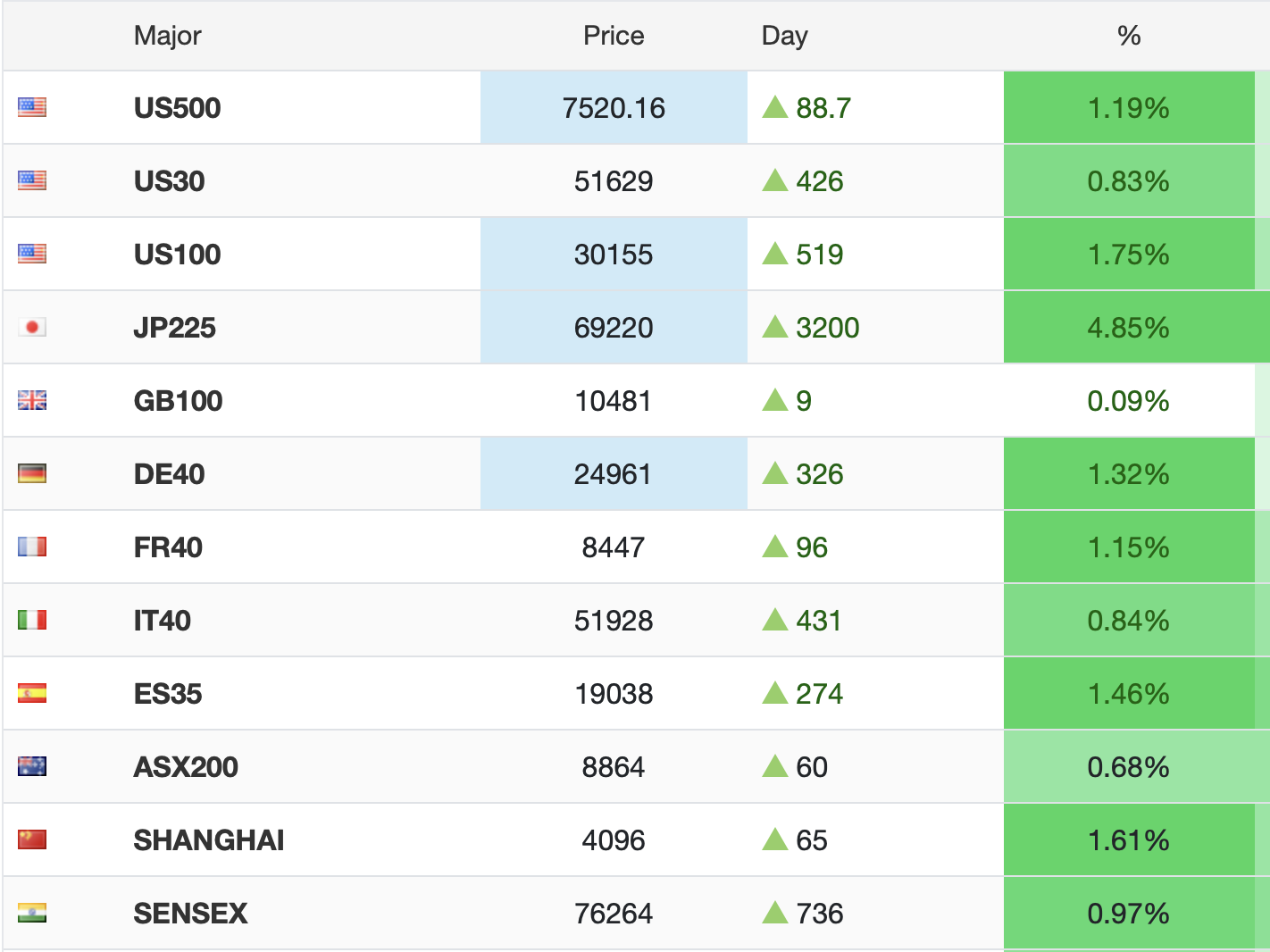

So, let’s turn to the markets. It is no surprise that risk is on everywhere this morning after the Trump announcement so briefly, here is a screenshot from 6:40 this morning showing equity futures markets higher across the board.

Source: tradingeconomics.com

While these are just the major markets, the reality is that markets are higher everywhere except Oslo, as the decline in oil prices hits the Norwegian stock market. But otherwise, it is universal.

Bond yields are lower across the board as well, with Treasuries (-4bps) leading the way and all of Europe seeing sovereign yields decline by between -4bps and -6bps as the inflation story follows oil lower. JGBs, too, slipped -4bps overnight and are down -17bps in the past week!

But oil remains the story because its movement is what is driving the narrative. And, interestingly, there is still strong support from one side of the argument that we are close to hitting tank bottoms and prices are going to shoot higher. We have heard from both Chevron and Exxon that it is a dangerous situation and even the reopening of the Strait may not happen in time to stop it. But consider if you are Exxon or Chevron, high oil prices are what you need as you sell your inventory rich and drilling is much more profitable. And one thing they have is a lot of inventory in their refinery systems. It hardly seems likely they would be out touting the deal as great and talking prices down. We have heard throughout the conflict that in a few weeks, prices would spike higher as shortages developed, but that has never happened. I go back to my view that ignoring market prices in favor of the narrative is a mistake. At this point, with WTI at $80/bbl, I will argue we will see $50 long before we ever see $100 again.

As to metals markets, based on recent price action, it should be no surprise that gold (+2.75%), silver (+4.3%) and copper. (+0.7%) are all rallying on the lower inflation => lower interest rates => increased commodity demand.

Finally, the dollar is under pressure generally as the DXY (-0.25%) is a pretty good proxy for most things. In truth, we are seeing some larger movements (INR +0.7%, SEK +0.8%, ZAR +0.6%, CHF +0.6%) all responding to the lower oil price, and in the case of the rand, the higher gold price. However, there are two outliers here. NOK (0.0%) is, not surprisingly, unable to show any traction, as like the Norwegian stock market, declining oil prices are a drag here, and JPY (+0.1% and still above 160.00). The latter must really be concerning to Ueda-san as in a broad dollar decline, if the yen can’t gain traction, that is a real problem.

On the data front, there is a bunch of stuff, but other than Retail Sales on Wednesday, all of it is second tier.

| Today | Empire State Manufacturing | 14.0 |

| IP | 0.3% | |

| Capacity Utilization | 76.2% | |

| Tuesday | RBA rate decision | 4.35% (unchanged) |

| Housing Starts | 1.44M | |

| Building Permits | 1.41M | |

| Wednesday | Retail Sales | 0.5% |

| -ex autos | 0.5% | |

| FOMC rate decision | 3.75% (unchanged) | |

| Thursday | Initial Claims | 232K |

| Continuing Claims | 1790K | |

| Philly Fed | 10.0 | |

| Leading Indicators | 0.1% |

Source: tradingeconomics.com

In addition to all that, the G7 meets this week, starting this evening in Evian, France with French President Macron leading the group.

As always there is a great deal of naysaying out there as the joint announcement of a deal between the US and Iran has upset the applecart for many narrative writers, and they are committed to their positions. Personally, I am very happy to see the deal, although it was early as I had anticipated a July 4th outcome, but in this case, a much better result. I guess it will take some time before it is clear if things are truly operating more normally again, but market pricing is demonstrating a willingness to believe.

With this in mind, the dollar should remain under some pressure for now, as prospects for a Fed rate hike are going to fade, although they haven’t yet according to the futures market, but if anything, that will simply mean that the US will suck in more global capital as the US economy continues to outperform elsewhere. Ultimately, that will benefit the greenback.

Good luck

Adf