For all of the angst that Iran

Has ended the talks and moved on

The market for oil

Has come off the boil

As risk takers see no black swan

So, stocks keep on making new highs

And it cannot be a surprise

That bond yields have slipped

While in today’s script

Elections will garner all eyes

Once again, I am having a hard time reconciling the narrative and the price action. Yesterday saw a sharp rally in oil as the talks between the US and whoever is representing Iran apparently collapsed. Yet, as you can see from the below chart, while that was worth nearly $5/bbl early in yesterday’s session, those gains dissipated over time and this morning, oil (-1.2%) continues that slide.

Source: tradingeconomics.com

One thing I saw on X this morning claimed Iran was done talking, had received a nuclear bomb from a third party (Pakistan? North Korea?) and was going to detonate it somewhere. Another was that the talks are still ongoing. I do find it interesting that so many are willing to take statements from the Iranian news agency, TASNIM, a body that has lied repeatedly for 47 years, and assume their claims are gospel. Propaganda is always an ongoing project on both sides (in truth from every government everywhere) and thus every claim must be seen for what it is, speaking to a specific audience to achieve a response, not an unbiased description of reality. Thus, it seems many folks see what they want to see to confirm their prior beliefs. I come back to the market as the most unbiased arbiter, and it continues to point to an end to the conflict on a relatively short timeline.

Which takes us to the other story today, US primary elections, notably in California where there is a gubernatorial primary and a mayoral one in LA that has garnered the most attention based on the seeming outstanding performance of former reality-TV star (?) Spencer Pratt running against the incumbent Karen Bass. This race seems like it may be quite important nationally as it would offer the possibility that the deepest blue of cities may finally have had enough incompetence in the mayor’s office and wants to change directions, at least a little bit. Of course, NY just elected an incompetent mayor, as did Seattle and Chicago before them, so maybe the people in these cities like the situation. I’m hopeful that is not the case.

But otherwise, it is hard to get too excited about much this morning. equity markets in the US made yet another set of new highs yesterday across the major indices as no matter the news, it appears there is a bullish spin. So, let’s turn to markets this morning. Asian equity markets were mixed overnight with Tokyo (-0.3%) slipping slightly although HK (+2.5%) and China (+1.5%) both rallied nicely on the back of the US tech rally. Net, there were far more winners in the region (Korea, India, Taiwan, Philippines, Thailand, Singapore, Indonesia), than laggards (Australia, New Zealand, Malaysia) with the laggards barely slipping at all. So, despite all the angst over Asian nations running out of oil and oil products, equity investors are all in there!

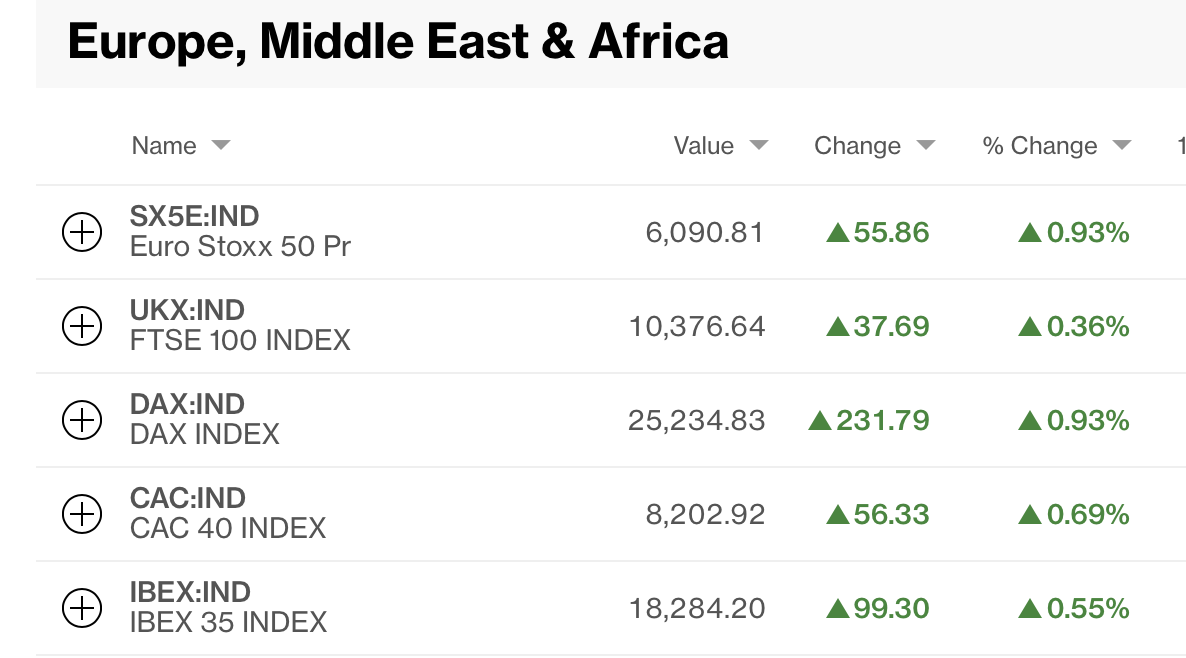

In Europe, it’s happy days as well as per the below Bloomberg screenshot.

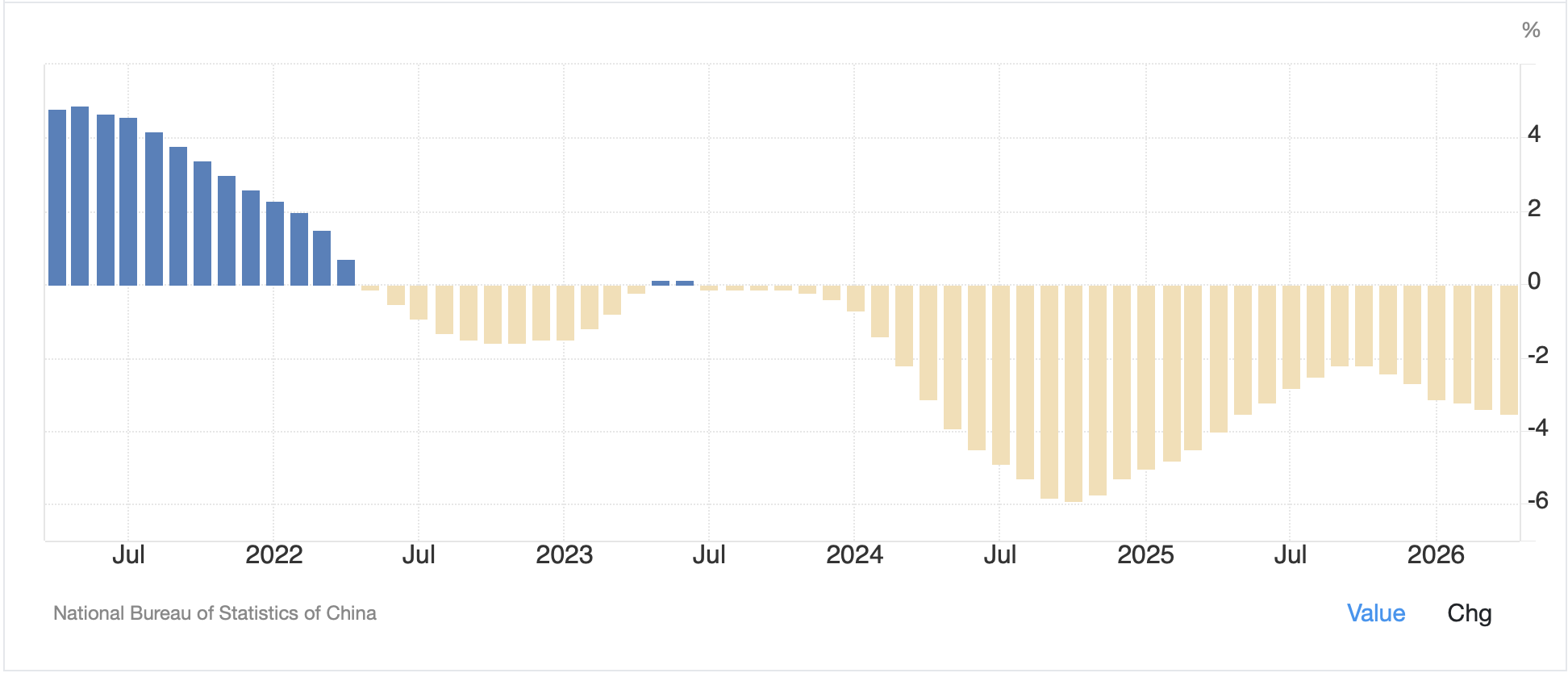

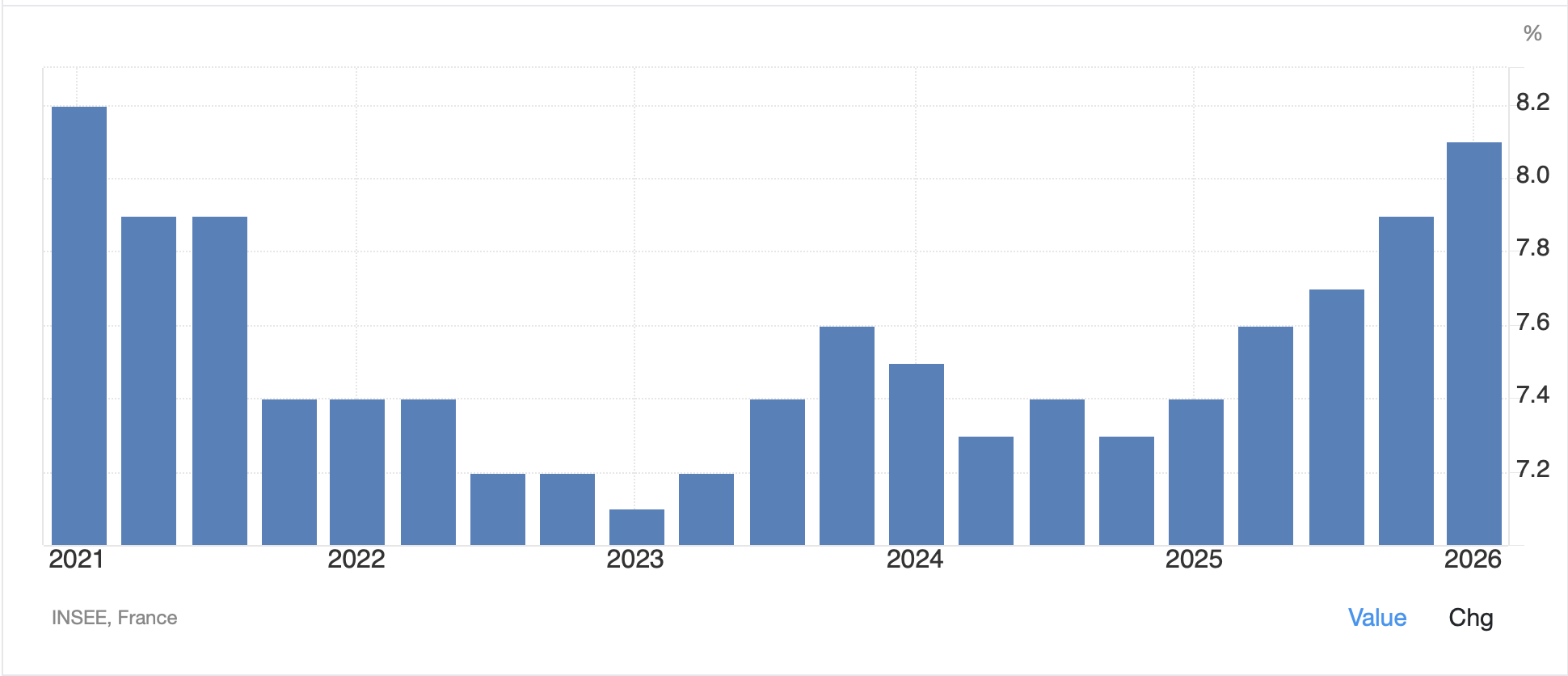

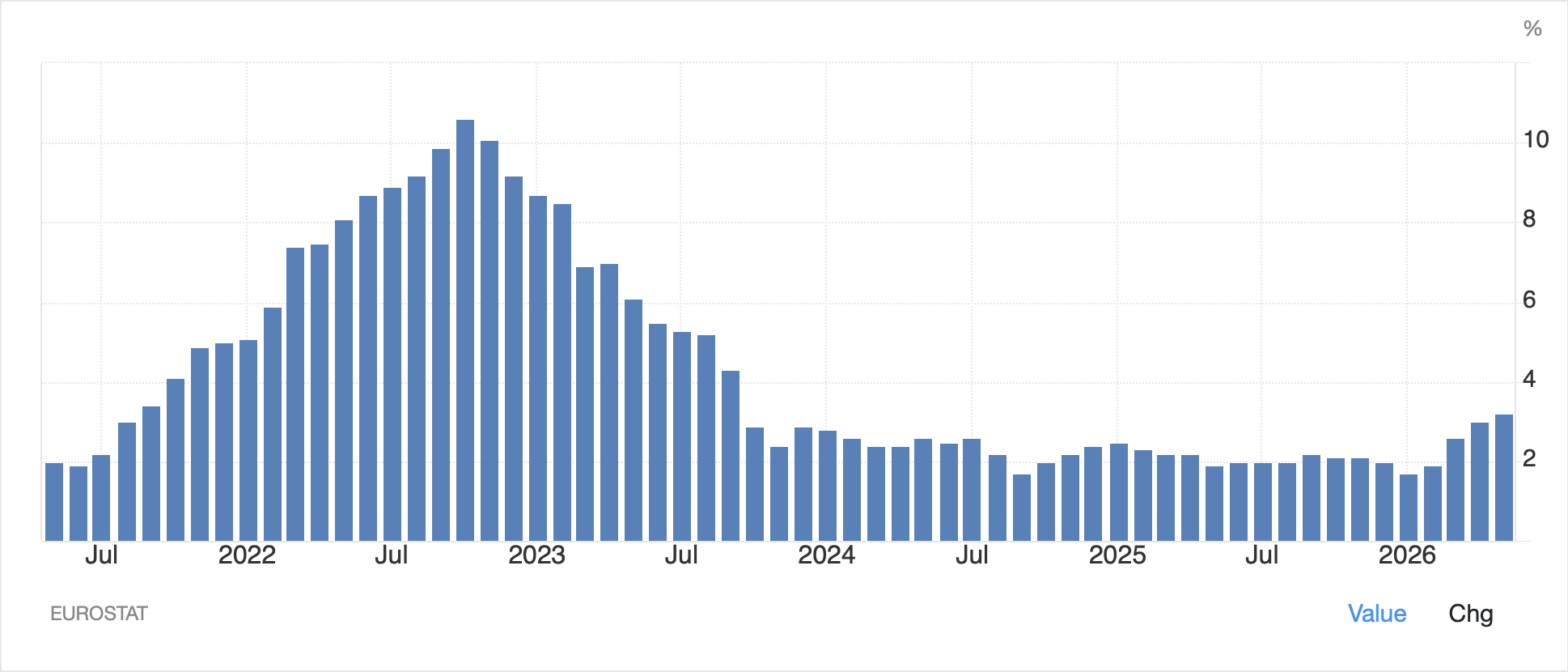

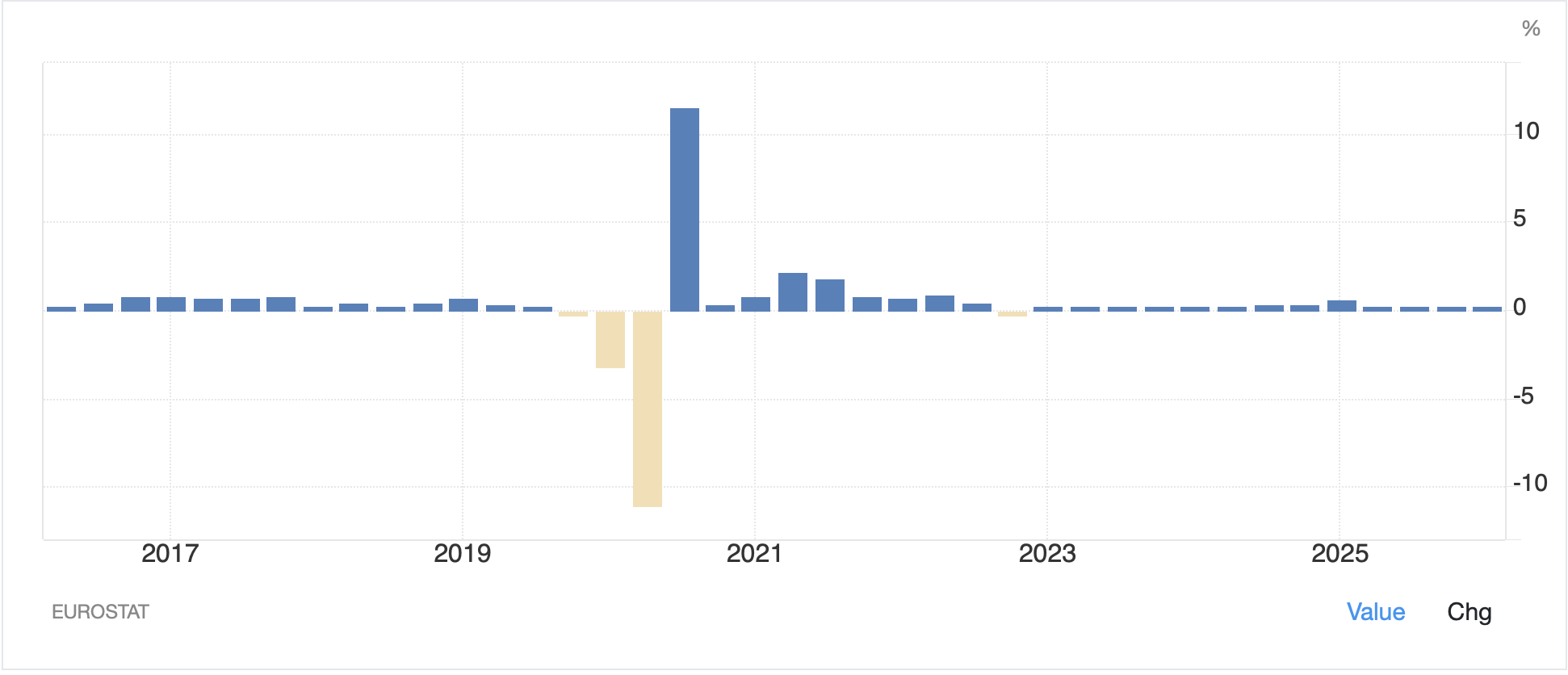

This is despite Eurozone inflation rising to 3.2%, its highest level since September 2023, and, as per the below chart, certainly looking like it is beginning to trend higher on the back of 3+ months of higher oil prices feeding through the entire economy.

Source: tradingeconomics.com

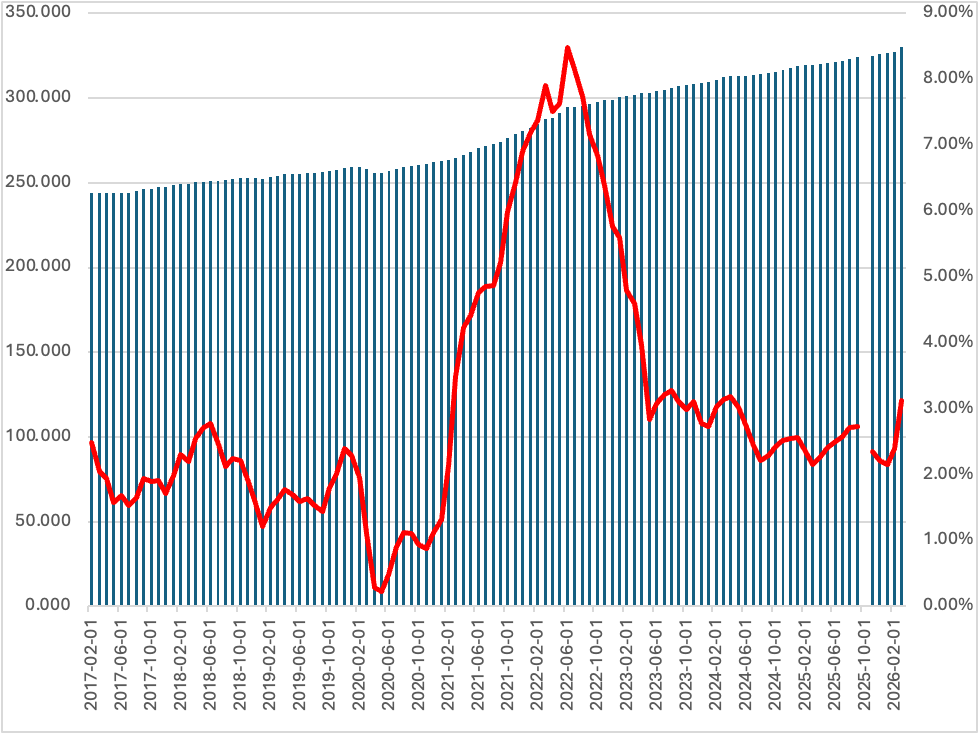

Of course, given Eurozone GDP is indistinguishable from zero (see below chart), and has been for 3 years, it is fair to wonder if this is setting up to be a particularly egregious central banking error by Madame Lagarde.

Source: tradingeconomics.com

Too, while short-term inflation expectations have unsurprisingly risen, a look at the 5-year result shows limited concern by consumers. As an aside, there is good reason to believe that inflation expectations are irrelevant in future inflation readings, at least according to the academic literature, but it is a driving force in current central banking models, so needs to be considered.

In the end, though, the ECB is going to hike rates next week, on that you can depend, and if when economic activity declines, they will blame Putin or Trump or Elon or anything but their own failed policies.

As to US futures at this hour (7:10), they are modestly lower, maybe -0.2% or so across the board.

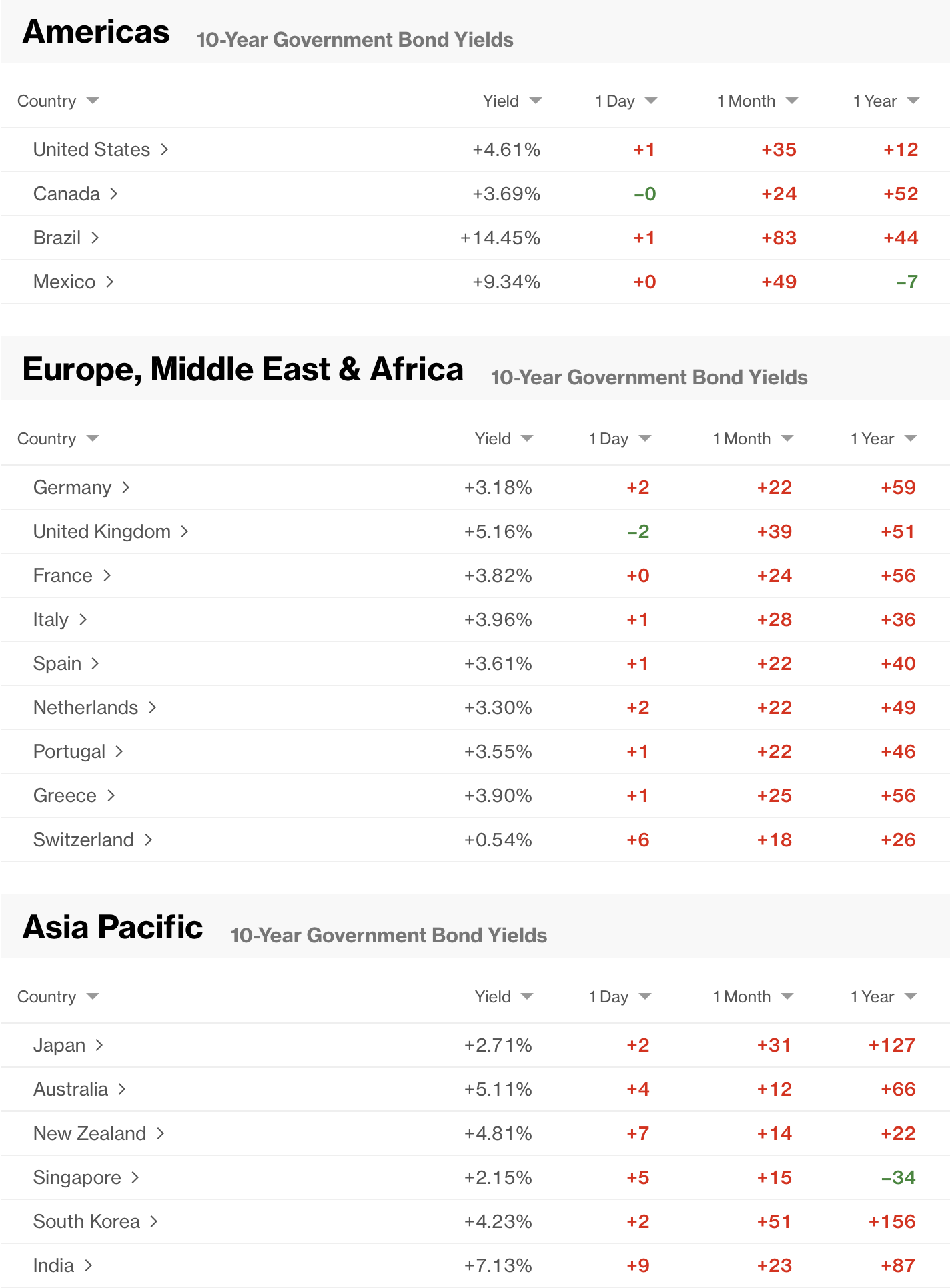

In the bond market, Treasury yields have fallen back -3bps this morning after round-tripping 5bps higher yesterday and finishing the day unchanged. European sovereign yields are having a better day, with declines of -6bps to -7bps across the continent and JGB yields (-11bps) are really falling. My conclusion is that investor concerns over runaway inflation simply do not exist despite the narrative pushing that story. The ostensible crises in May apparently never arrived, at least not yet.

In the commodity market, it can be no surprise that metals prices (Au +1.0%, Ag +1.8%, Cu +1.0%) are higher this morning given the overall risk environment. The negative correlation between metals and oil remains largely intact for now. The interesting thing to note, though, is that despite the daily gyrations, in reality, neither oil nor the precious metals have gone anywhere in a while. The same is not true for copper which is at new all-time highs.

Finally, the dollar is modestly softer this morning, on the order of 0.1% against its G10 counterparts with AUD (+0.3%) the best performer. In the EMG bloc, ZAR (+0.6%) is responding to the combination of lower oil and higher gold prices and MXN (+0.4%) is also having a pretty good session, but that seems more like beta vs. the dollar than anything else. I would be remiss if I didn’t spotlight JPY (0.0%) which continues to edge closer to the 160.00 level as per the below chart, but was also the subject of much discussion as FinMin Katayama was out explaining that, “As for foreign exchange, we continue to maintain our stance that we stand ready to take appropriate action at any time, as needed.” However, while the market expects a 25bp rate hike in two weeks, that is already in the price. In order to stop the yen’s slide, they will need to really change policy, something which I maintain is not in the cards for now.

Source: tradingeconomics.com

On the data front, this morning brings only the JOLTs Job Openings (exp 6.88M), essentially unchanged from last month. Yesterday’s ISM Manufacturing data was quite solid across the board except for the employment subindex, which remains lackluster as companies expand with more automation.

I think it is fair to say nobody knows what will happen in the Iran conflict nor the timing. While markets can be completely wrong, and forced to reprice suddenly, that is an extremely rare occurrence. Too, the one thing on which we can count is if something hugely negative occurs, central banks around the world will step in, add liquidity and cut rates, to ameliorate the slide. My point is, I will not bet against the market view that this will end sooner rather than later.

Good luck

Adf