Last night it appeared a reprieve

Was offered, though I don’t believe

That Trump will delay

Much more than a day

Ere US Marines, wins, achieve

But as of last night, markets think

That peace will come in an eye blink

Thus, futures have rallied

While bond prices dallied

And oil has started to sink

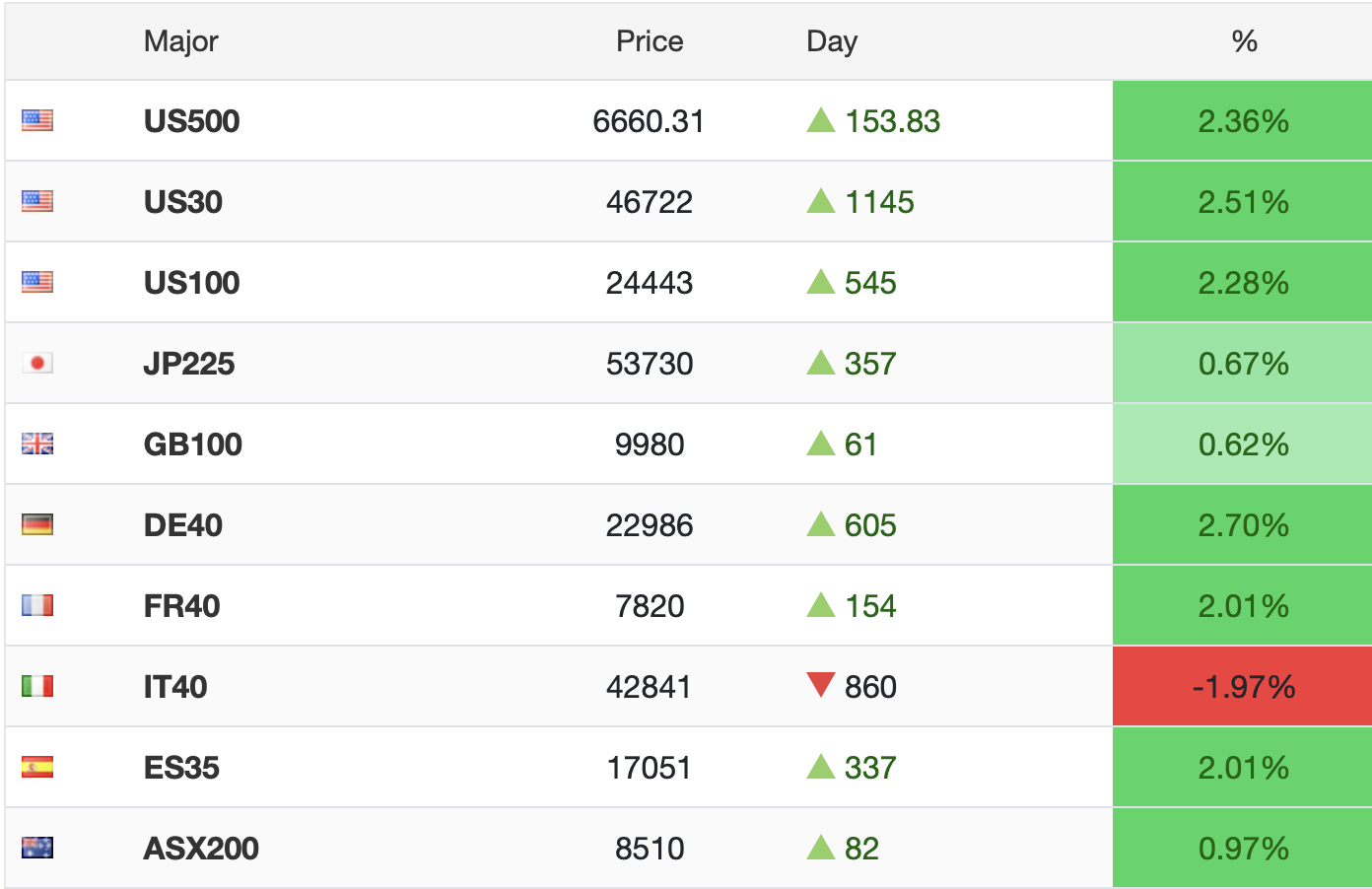

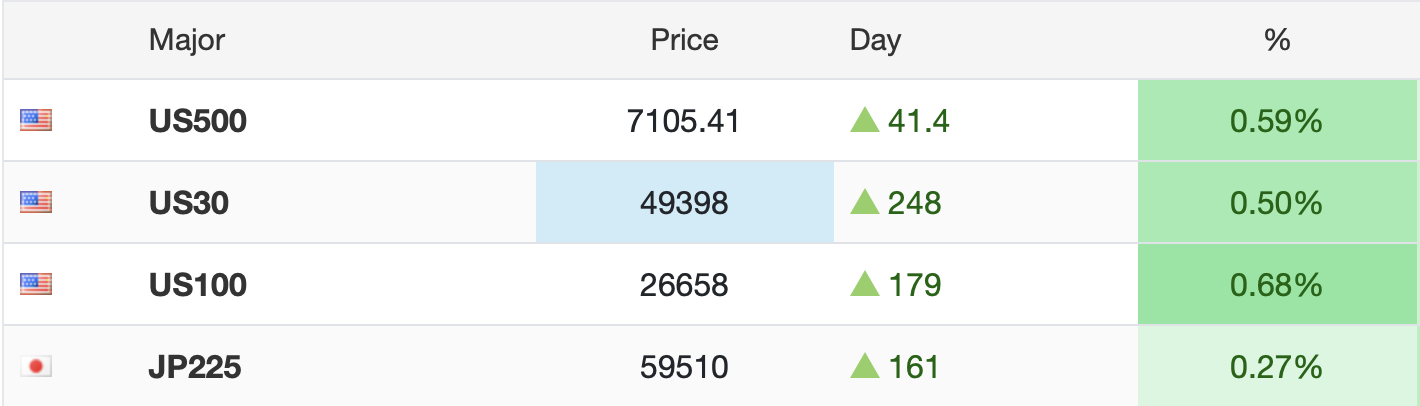

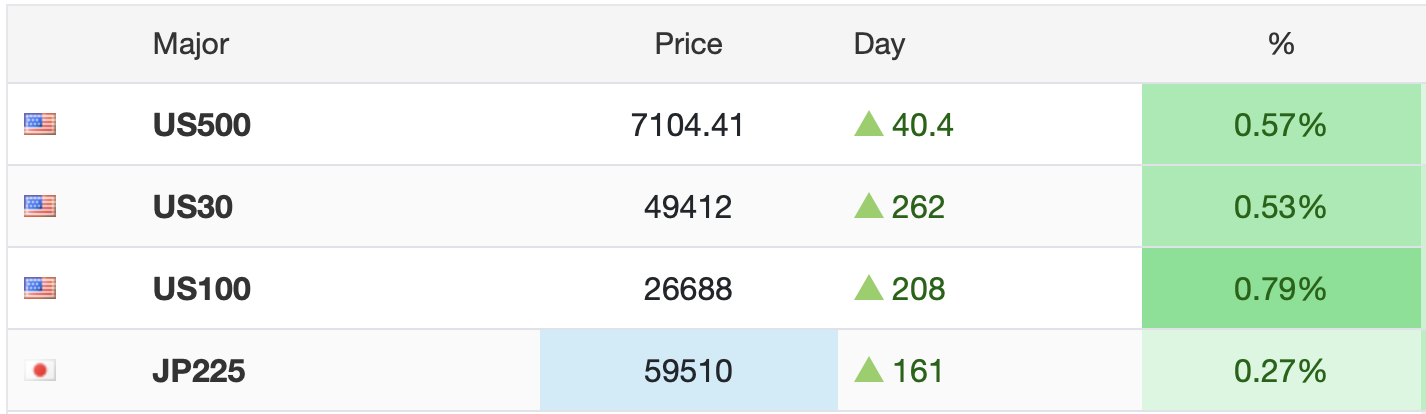

This is the Tuesday night look, which is subject to significant change by the time I wake up tomorrow morning. But here are the futures prices at 9:30pm:

Source: tradingeconomics.com

As you can see, US futures are higher and the Nikkei 225 is also modestly higher with no indication that there is concern over the US landing on Kharg Island and other Iranian key strongholds. All this comes after news has filtered out that Ahmad Vahidi, who appears to be the senior most IRGC leader left, has arrested the civilian government members who were scheduled to meet with the US and hammer out a deal. To my eyes, and from what I have read from what I believe is an excellent source, marines will be on Kharg Island before the week is out. It strikes me if that is the case, the current equity rally, which has been impressive, will get challenged.

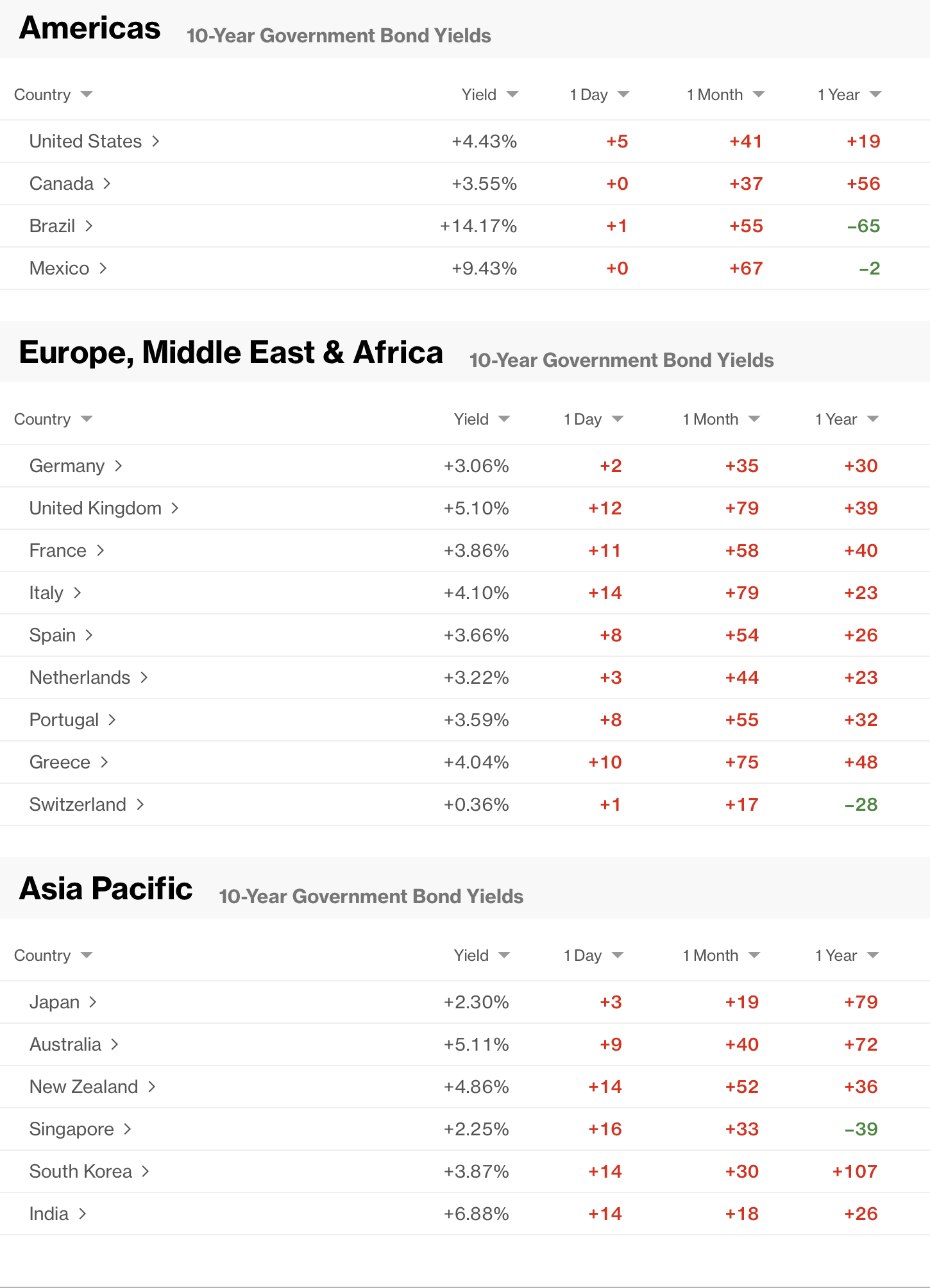

As to bonds, last night they were essentially unchanged with 10-year yields at 4.29%. Again, this is not the stuff of major concern. And oil? Modestly lower and back below $90/bbl.

The early results are confusing

With recent attacks Iran’s choosing

But elsewhere there’s hope

That peace is in scope

Despite lots of, others, accusing

As of 6:20 this morning, although there have been several ships fired upon by Iranian gunboats, the US has not escalated, and the President has indicated he is waiting for news today on the situation. One of the takes is that the Iranians are going to come to the table and seek a deal, although it is difficult for me to believe that Vahidi is ready to cede power. But like virtually everybody else, nobody really knows what is happening.

However, markets appear to have made up their mind that the worst is over and there is no reason to panic any further. In fact, it appears they are getting excited about the opportunities that will come about because of all the post-war reconstruction that will be necessary and will certainly be profitable for those companies engaged.

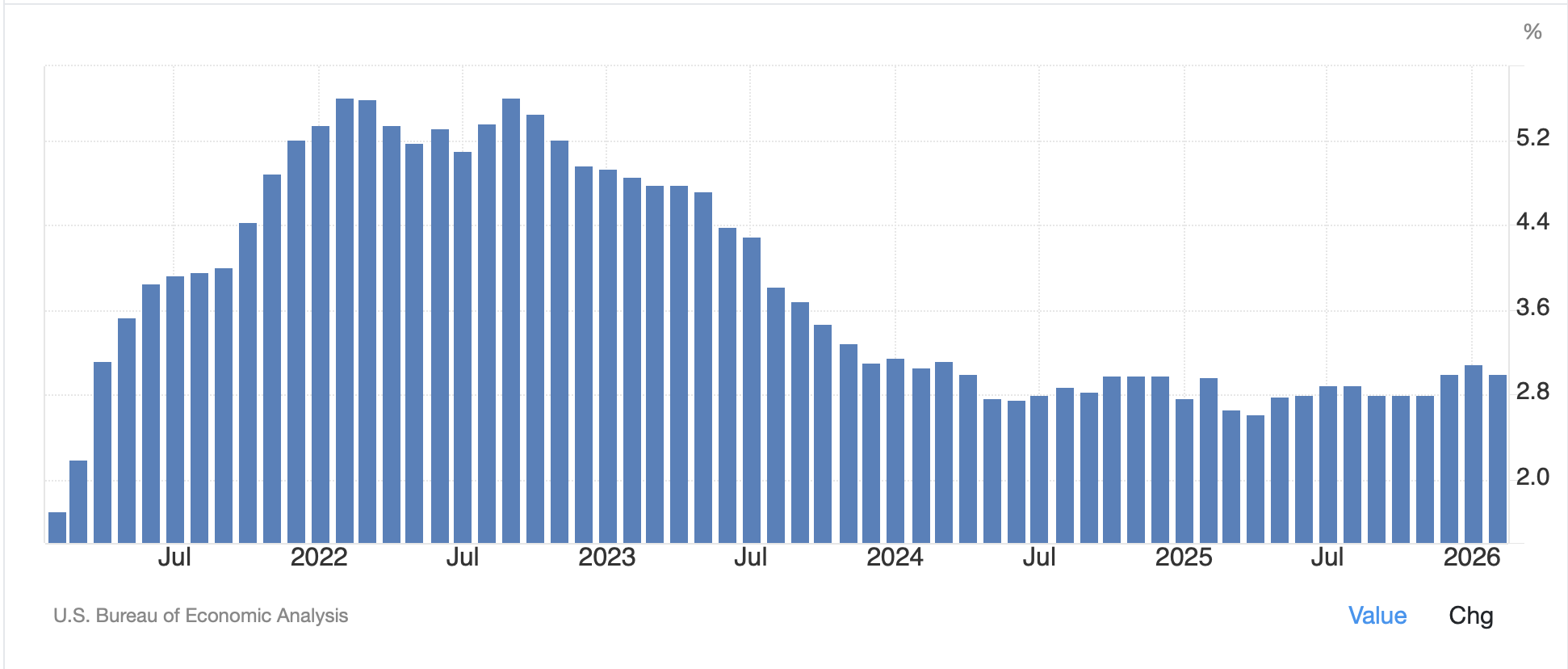

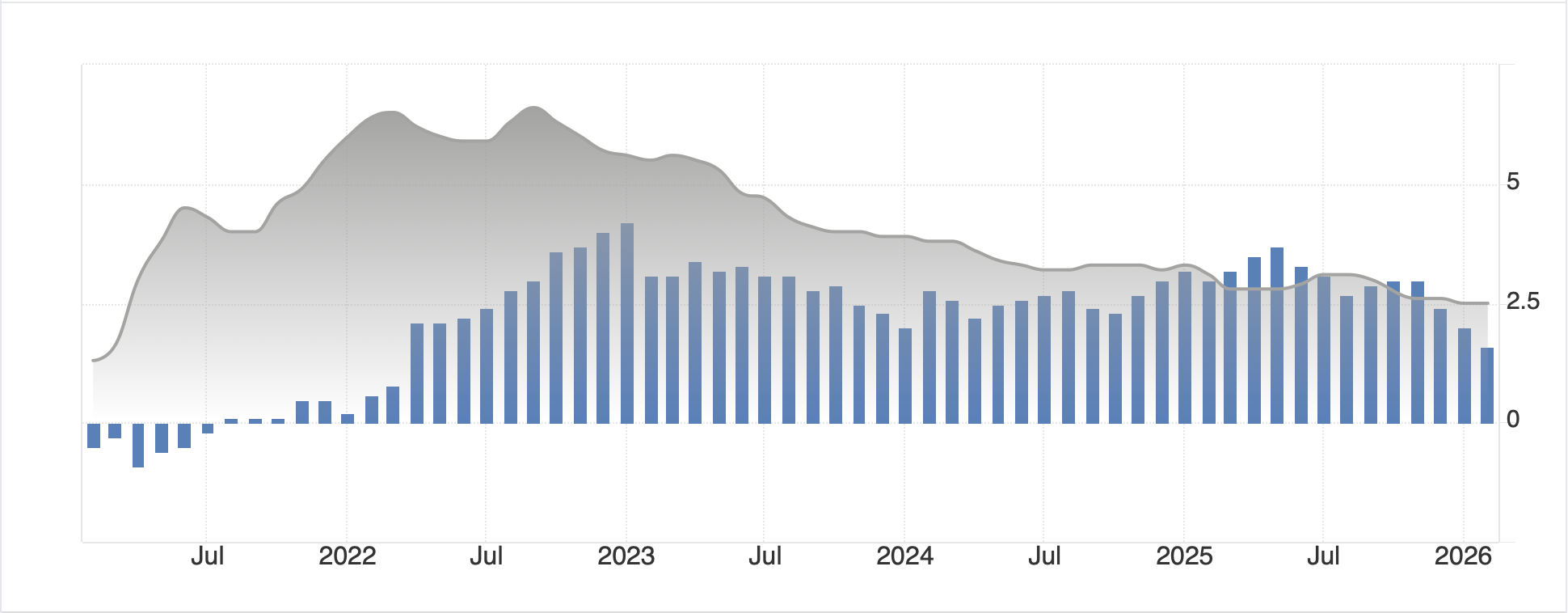

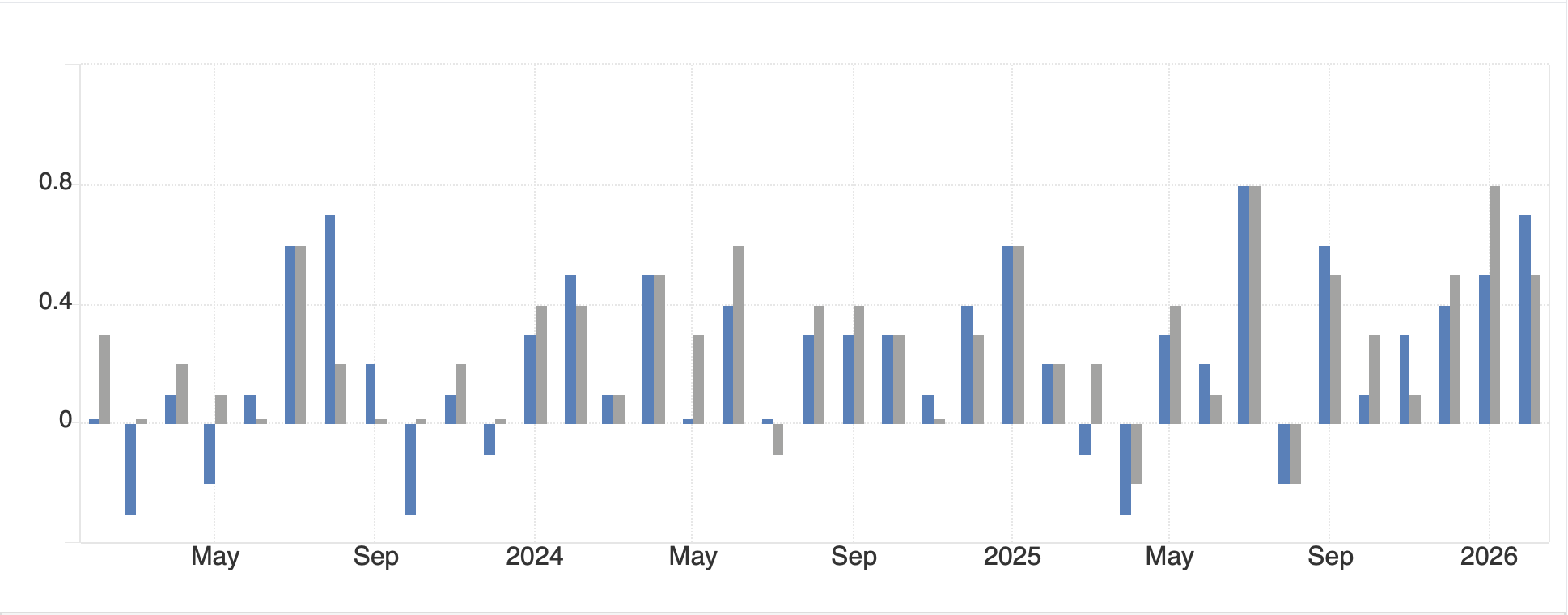

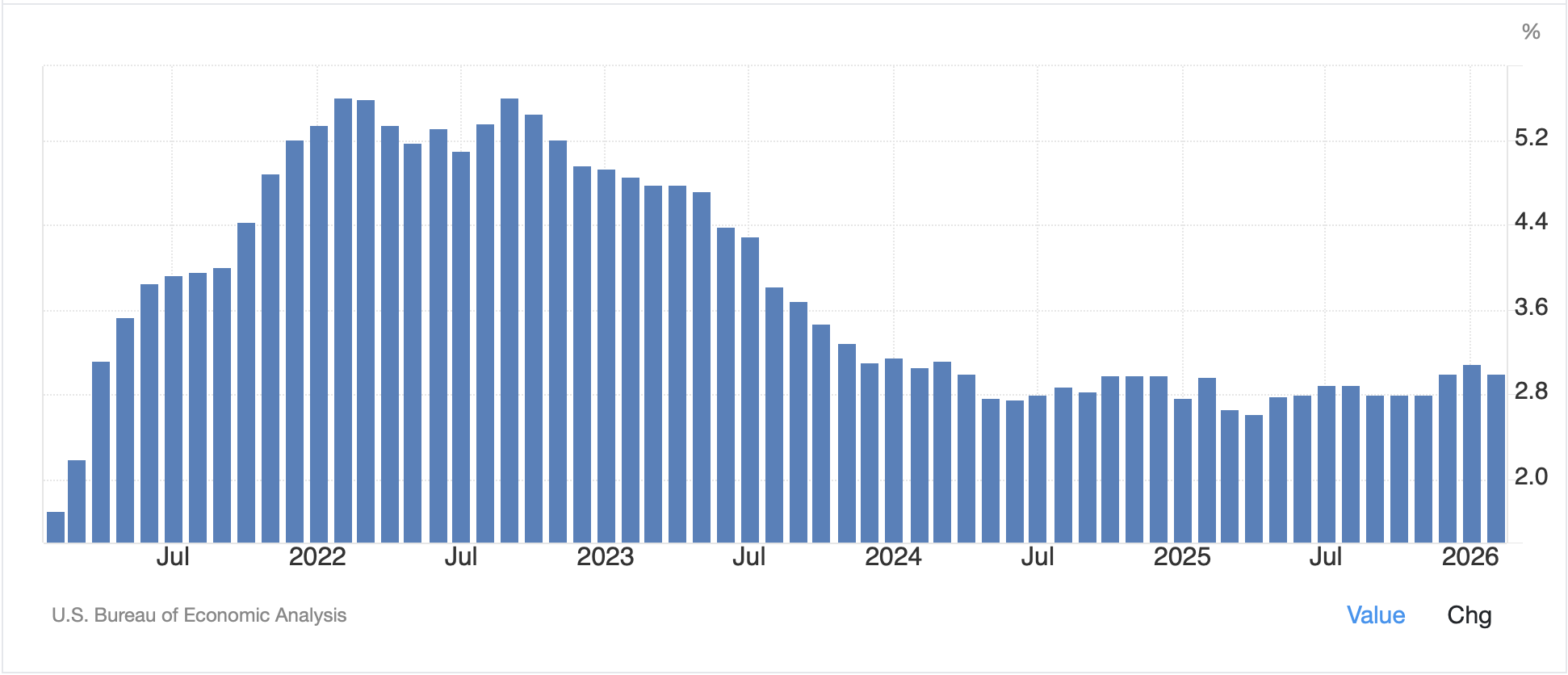

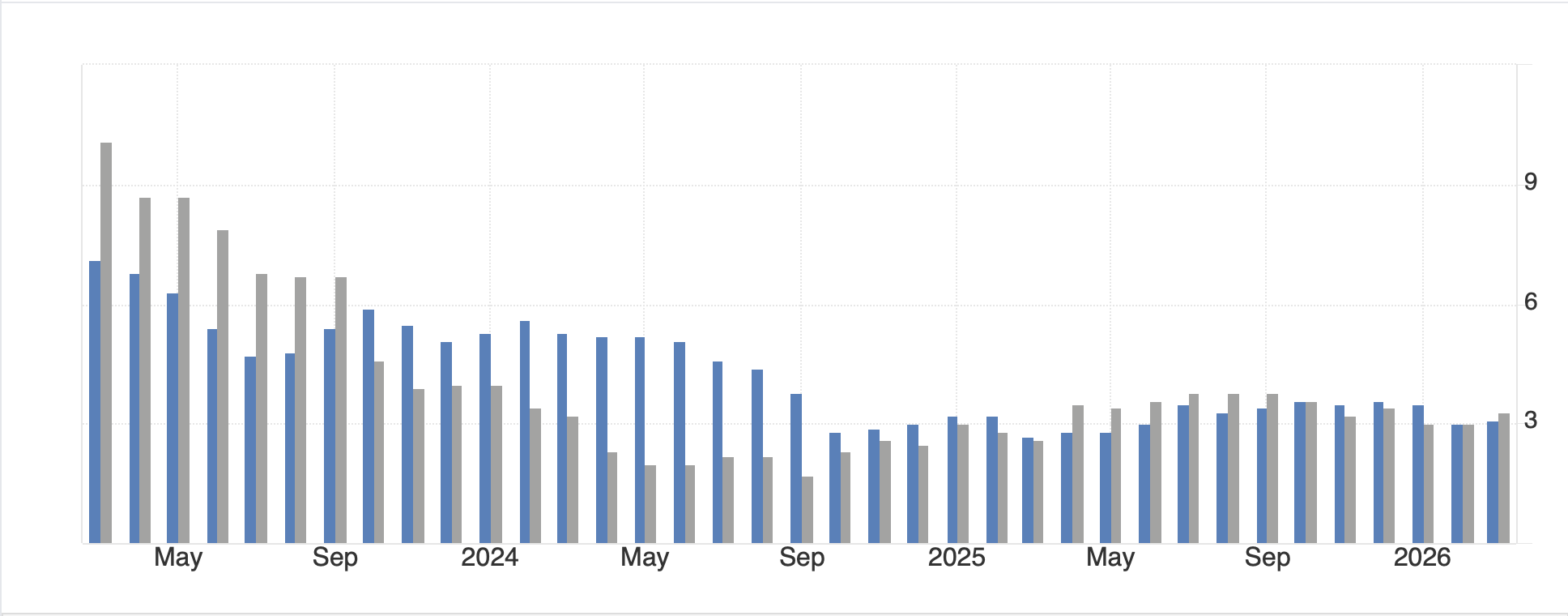

The other story from yesterday was the confirmation hearings for Fed Chair nominee Kevin Warsh. I imagine it went about as largely expected with every Democrat despising him and every Republican liking him, but until the DOJ case against Powell regarding the reconstruction of the Eccles Building is finished, Senator Thom Tillis has said he will not allow a floor vote. Warsh did consistently explain that the Fed has lost its way and has not achieved its goals so it is time to start thinking of new approaches. And it is certainly true, as the below chart shows, that the Fed has been a failure with respect to its inflation target of Core PCE at or below 2.0%, a number last seen in February 2022 (the left=most bar on the chart).

Source: tradingeconomics.com

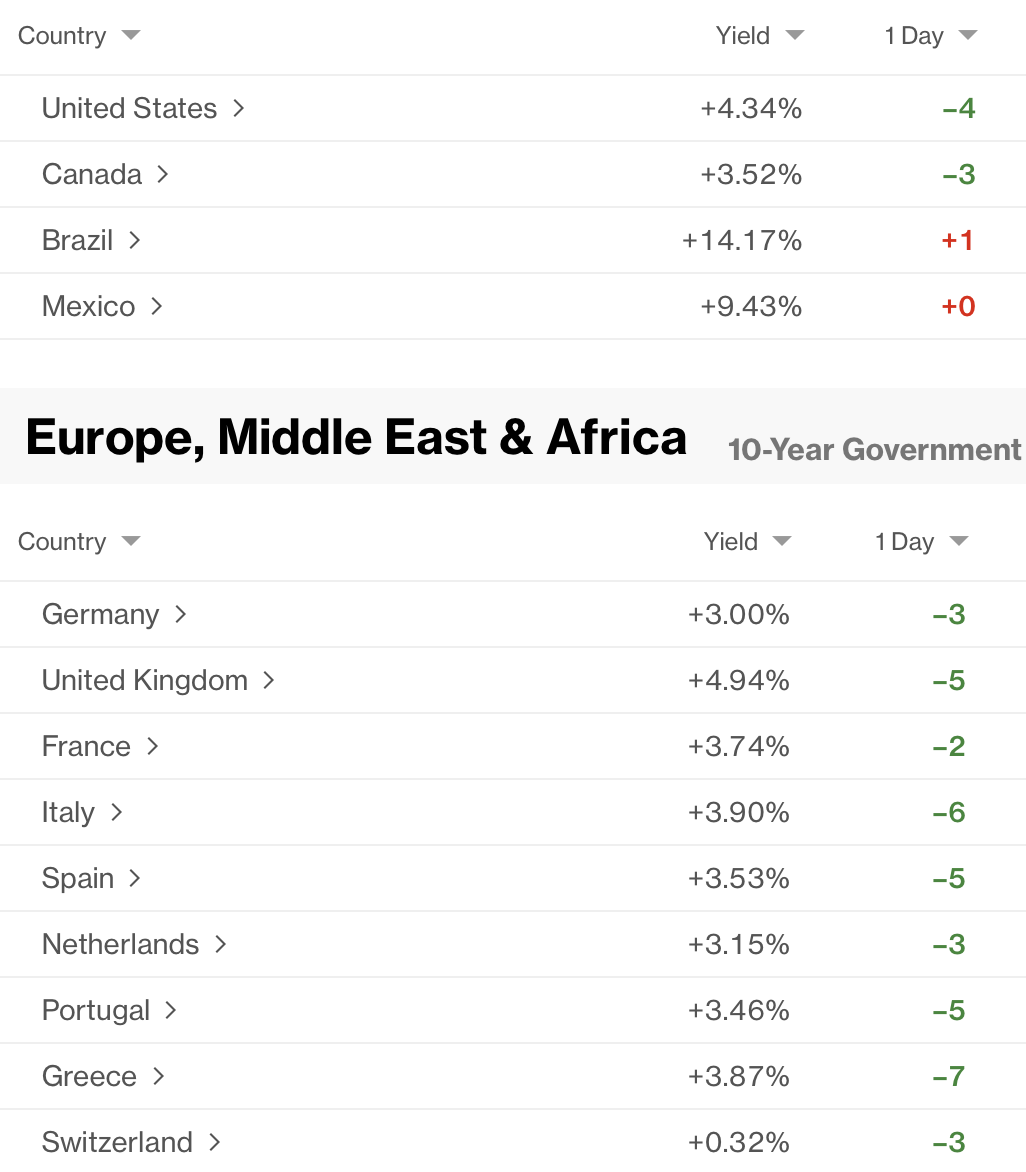

And with that in mind, let’s turn to markets this morning and see how things played out overnight and are evolving right now at 7:00. US futures are virtually in the same place they were last night as per the below screenshot from tradingeconomics.com

Asian markets were mixed overall with Tokyo (+0.4%), China (+0.7%) and Taiwan (+0.7%) all having a decent day while HK (-1.2%) and Australia (-1.2%) led the way lower for those regional exchanges that were under pressure. But in truth, it was about 50:50 with respect to gainers and losers. Certainly, there was no strong theme. Meanwhile, in Europe, markets have drifted a bit lower, but the CAC (-0.3%) and Spain’s IBEX (-0.3%) seem to be the worst of it. Net, it is hard to get too excited about anything in the equity space right now.

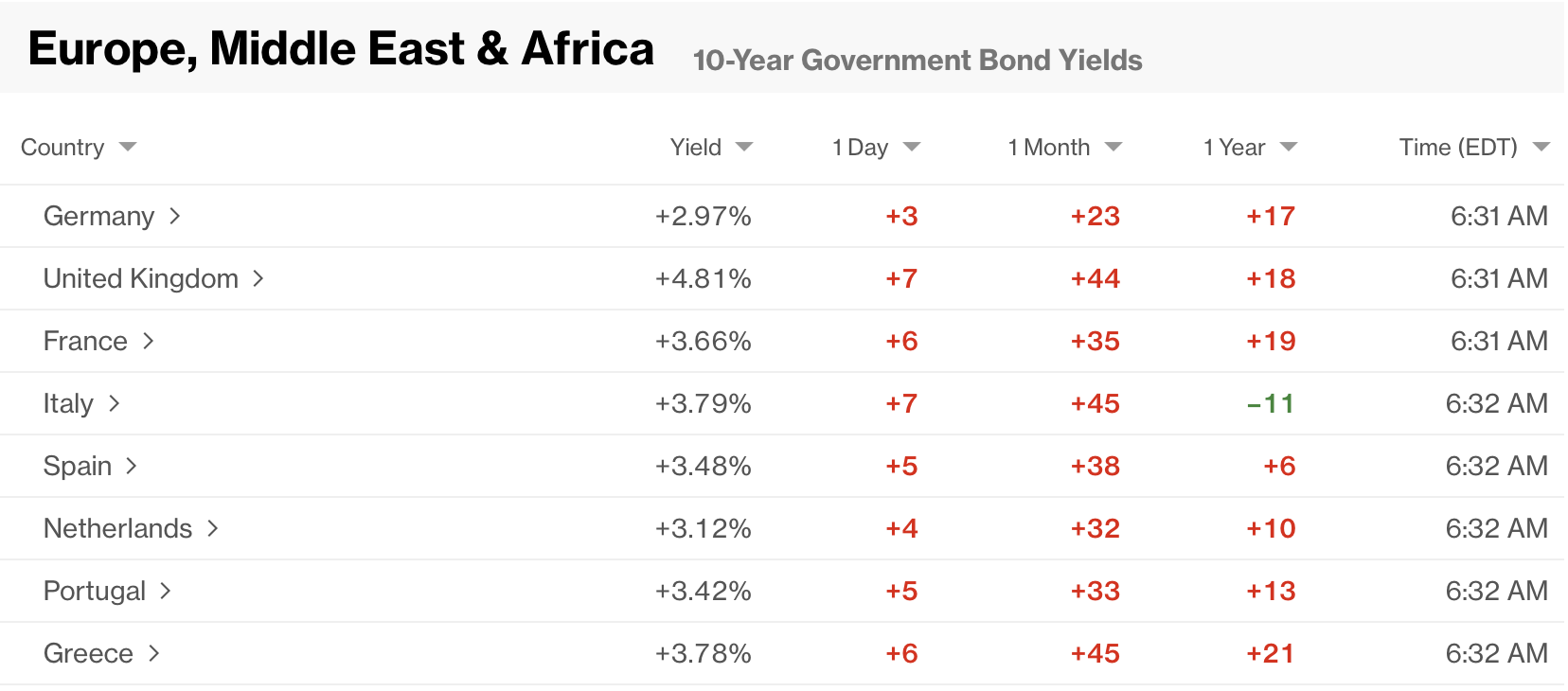

Similarly, bond markets are somnolent with Treasury yields edging lower by -1bp and similar price action in European sovereigns with the entire continent, and the UK, showing small yield declines of between 0bps and -2bps. Overnight, JGB yields were unchanged as well. While we continue to get inflation reads that include the war and the sharp rise in energy prices, there is no indication prices are running away yet. For example, the UK (3.3% headline, 3.1% core) released CPI this morning as did South Africa (3.1% headline, 3.2% core). Frankly, if you look at the chart below showing headline CPI for both nations (South Africa in blue, UK in grey), you would be hard-pressed to attribute any price pressure to the war given what has been going on in both places for the past three years.

Source: tradingeconomics.com

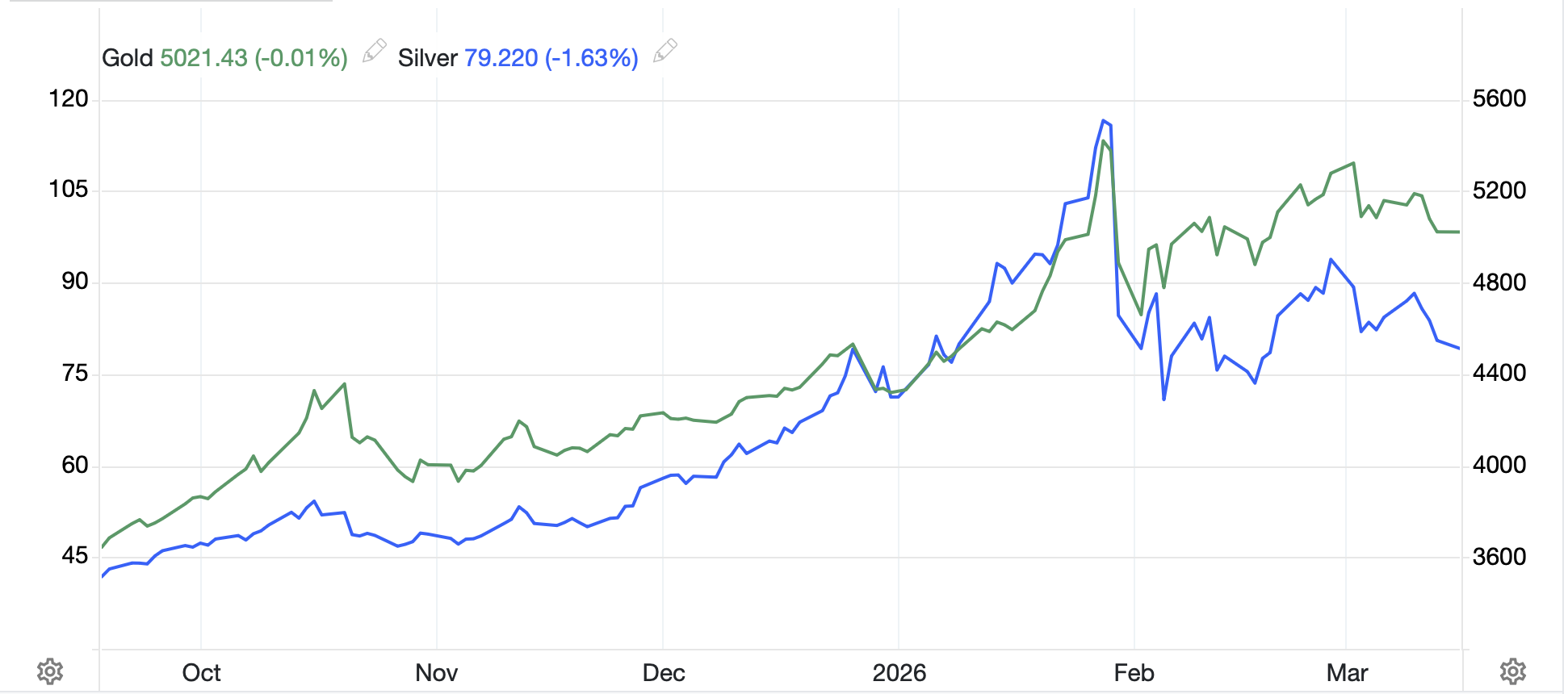

Turning to the commodity markets, oil (+0.8%) has rebounded from last night’s levels, but not that much, although WTI is back above $90/bbl, barely. NatGas (+1.15%) remains the absolute bargain in the energy world with US prices at $2.72/MMBtu, vastly cheaper than oil on a per unit basis of energy. Interestingly, in the metals markets, the recent negative correlation between gold and oil has broken down this morning with the shiny stuff rallying and taking all its friends along for the ride (Au +0.8%, Ag 2.0%, Pt +2.5%, Cu +0.7%).

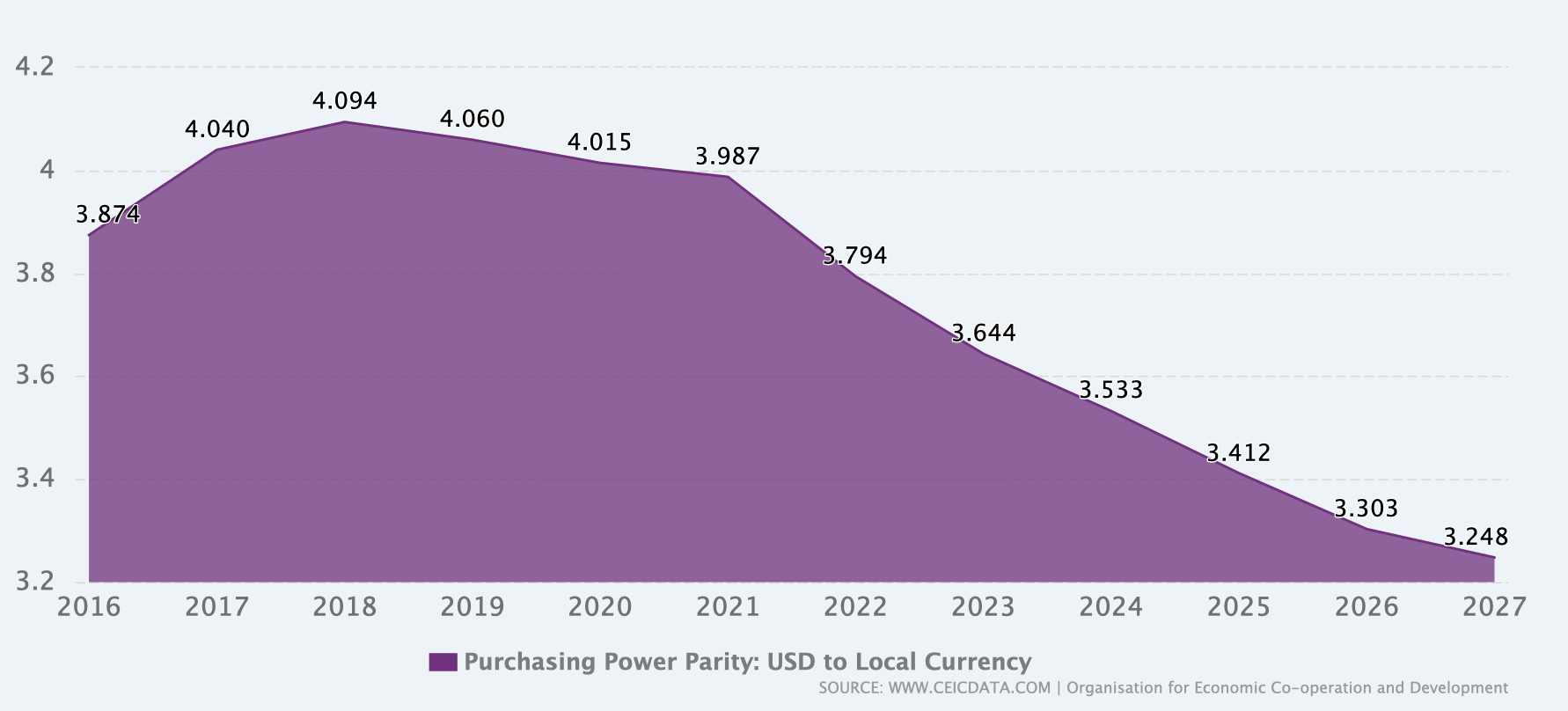

Finally, the dollar doesn’t really care about anything right now, virtually unchanged against most of its counterparts this morning. There are a few outliers, notably NOK (+0.9%) which continues to benefit from the oil story, CLP (+0.3%) which is higher on copper’s rally and NZD (+0.3%) which continues to gain on rising expectations of higher rates there. One other amusing thing was a story in Bloomberg this morning about CNY and how its recent strength, it has gained more than 6% over the past year as the below chart highlights, is causing problems for Chinese exporters.

Source: tradingeconomics.com

Of course, this has been a US (and global) complaint for a long time, that the renminbi has been manipulated to remain excessively weak to provide a competitive advantage for Chinese exporters. In fact, according to the OECD, the CNY’s PPP value is approximately 3.303 vs. its current level of 6.82, meaning it is trading in markets at half its appropriate value.

Source: ceicdata.com

My sense is that TEMU would not be able to sell all that sh*t so cheaply if that was the exchange rate, just saying. In fact, this is something President Trump has been bashing the Chinese on for years. But Bloomberg managed to offer a sympathetic tone for those “poor” Chinese companies who have seen the CNY gain 6% in a year.

Off the soap box and on to data where the only releases are the EIA oil inventories with a modest expected crude oil draw. This comes after the API indicated a 4.1-million-barrel draw last week. There are no Fed speakers on the docket with the FOMC meeting coming up next week, so my take is today will be all about the ongoing earnings releases, which thus far have been quite positive, and waiting for President Trump, who ostensibly will be speaking at 3:00pm this afternoon. It is hard to have a strong opinion in this market, that’s for sure. Unchanged seems to be the best bet absent a major headline announcement.

Good luck

Adf