The story today is the same

First China, then prices ain’t tame

The meeting twixt Xi

And Trump seemed to be

Successful as both sides will claim

But price data once again soared

Thus, PPI wasn’t ignored

But markets remain

Quite happy to feign

Indifference while traders are bored

China and prices remain the two dominant stories this morning, although despite much angst over yesterday’s MUCH hotter than expected PPI readings (Headline: 1.4% M/M, 6.0% Y/Y; Core 1.0% M/M, 5.2% Y/Y), markets did very little overall. For instance, Treasury yields edged up 1bp yesterday and this morning have reversed that tiny move. US equity markets were mixed with the DJIA slipping slightly while the NASDAQ (+1.2%) powered ahead oblivious to any potential negative issues with rising prices. Oil barely budged, and the same was true with metals and the dollar. In other words, despite a lot of analyst angst, and there was plenty regarding the data point, investors didn’t seem to care.

Now, while I am personally concerned over the trajectory of prices as I have seen nothing to indicate that governments anywhere are going to reduce their debt-financed spending nor are central banks going to stop supporting that activity, I clearly do not make up the majority view. With that in mind, I do have a suspicion that something will come along that will shake the investor community’s faith in higher forever equity prices, but I have no idea what it will be. After all, every other potential catalyst (e.g., oil at $100/bbl, 30-year Treasury yields at 5.00%, two hot wars involving nuclear powers) has been largely ignored. So, let’s move on to the other story of note, Nixon Trump in China.

It is always interesting to see the framing of a particular story from different news outlets which is obvious based on how they lede a story. But, trying to get through different versions of the same thing, it is clear that China’s primary concern is Taiwan and that there should be no US interference there. The US’s primary concern appears to be solving the Iran situation with President Trump looking to President Xi to use his influence to get Iran to see the light. Both nations agreed Iran should never have a nuke and that the Strait of Hormuz is an international waterway that should not be subject to blockage by one nation. (China really cares about this because half of their oil also transits the Strait of Malacca, and if the precedent is set in Hormuz that it is not a free waterway, that could easily be extended to Malacca which would be a real problem for Xi.).

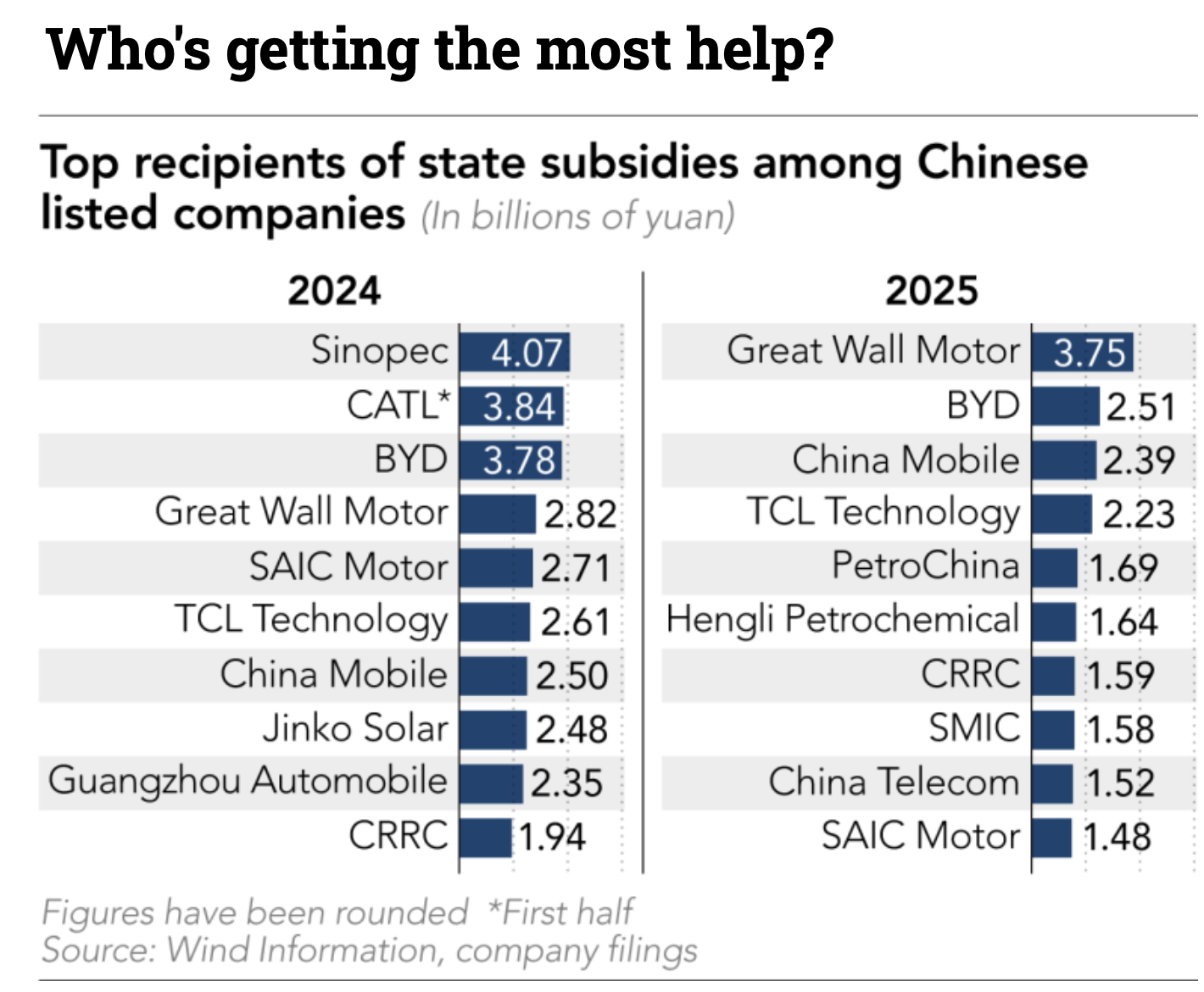

Then there were trade talks, and discussion of fentanyl precursors and oil and agricultural trade as well as semiconductors, the usual stuff. FWIW, which may not be much, I see this as the first major step to serious de-escalation between the two nations. But here’s an interesting tidbit, and a critical piece of the Trump rationale behind tariffs on Chinese manufactured goods. The below table from Nikkei News shows how much major Chinese companies (all listed on their stock exchanges) are getting in state subsidies. This is, of course, the very definition of “cheating” on trade.

Ask yourself why profitable public companies that focus on exports would need state support. This appears to be just another reason that Chinese manufactured goods are relatively cheap compared with elsewhere in the world.

Ok, enough about those stories as traders don’t seem to care about them. In fact, right now, traders don’t seem to care about much. But let’s look at the markets this morning.

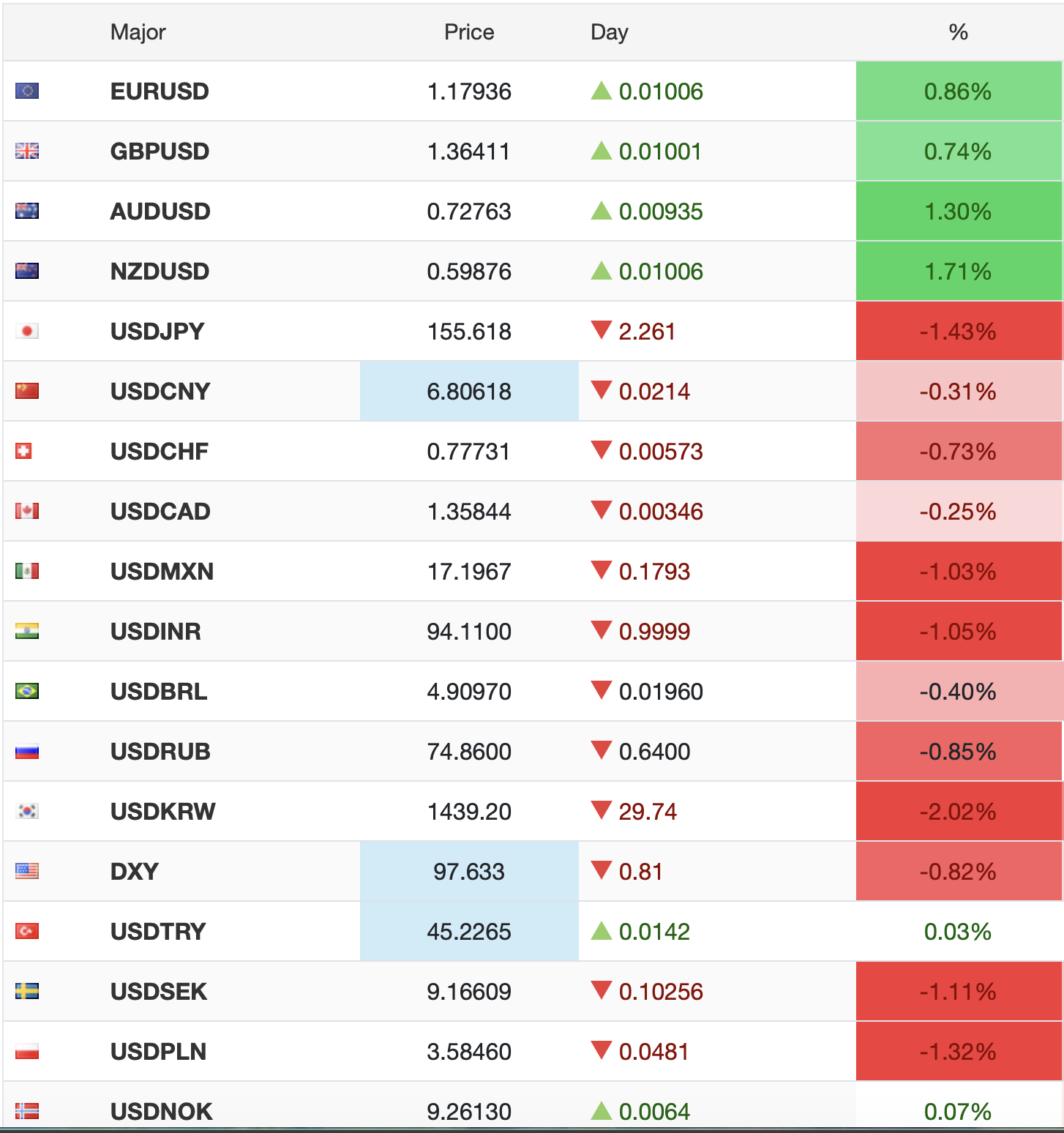

Since there is not that much ongoing across all markets right now, I’m going to start in the FX world as yesterday saw a noteworthy move in the Brazilian real (-2.4%) as you can see in the chart below.

Source: tradingeconomics.com

While thus far this morning it has rebounded ever so slightly, +0.25%, the story is that Flavio Bolsonaro, former president Jair’s son and a leading candidate in the upcoming presidential election, has been caught up in a local financing scandal which may impact his electoral prospects and leave Lula, and his socialist policies, in charge. Now, it must be remembered that this is a one-day movement but has done nothing to change the trend, as you can see below. BRL has gained more than 21% in the past 18 months as real interest rates remain quite high and are drawing in carry traders from around the world.

Source: tradingeconomics.com

But away from that story in Brazil, FX is sound asleep across both G10 and EMG blocs.

Mixed is the only way to describe Asian equity markets last night with Tokyo (-1.0%), China (-1.7%) and Indonesia (-2.0%) all under pressure while Korea (+1.75%), India (+1.1%) and Taiwan (+0.9%) all rallied nicely. As to the rest of the region, it was +/- a lot less movement. Data overnight showed Chinese financing shrinking slightly, a surprising outcome, but one in sync with the reality on the ground there that the combination of a still imploding property market and a significant reduction in local government financing on the back of that is weighing on the economy overall. They claim they will grow GDP at 4.5% to 5.0% this year, and I’m sure they will “meet” that target when the official data is produced, but all is not well there.

European bourses, though, are having a much better day with the DAX (+1.2%) leading the way higher although solid gains in France (+0.6%) and Spain (+0.8%) as well. Everything I read about this price action this morning points to excitement over AI, but given Europe is virtually absent from the AI universe, I am not sure what they are implying. It doesn’t seem likely there will be a European AI champion anytime soon, if ever. But that’s the story I see. Meanwhile, US futures continue to trade modestly higher at this hour (7:30).

In the bond market, while JGB yields continued higher overnight by 4bps, making yet further 19-year highs, European sovereign bonds have all seen yields slide between -4bp and -5bps this morning, allegedly on optimism that the Trump-Xi meeting will lead to pressure on Iran to reopen the Strait and reduce oil prices. But that seems misplaced in the short-term in my view. Nonetheless, that’s the story.

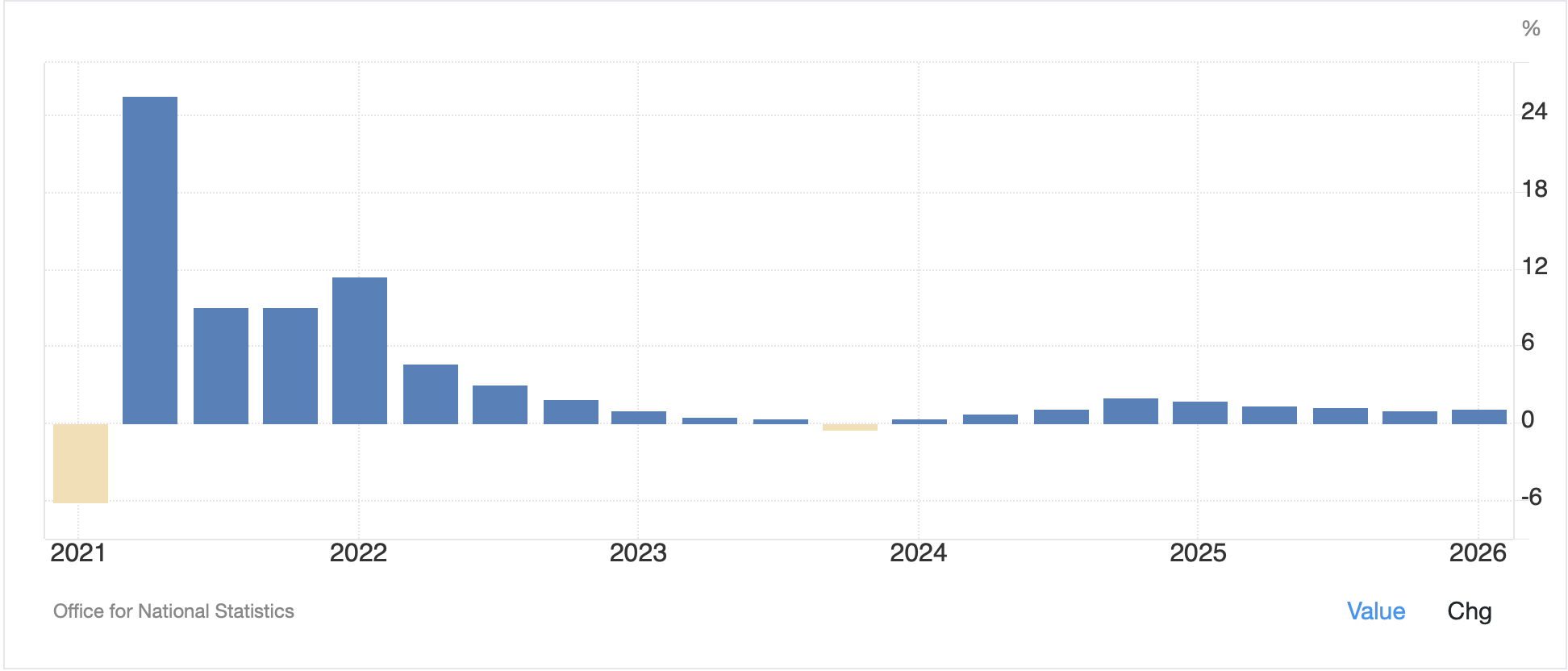

Earlier this week I discussed the political sh*t show in the UK and how PM Starmer appears to be on his last legs. One of the reasons for this is that his policies have not exactly helped the nation’s economy. For instance, this morning, preliminary GDP figures were released, and the Y/Y number was a better than expected 1.1%. Now, the fact that 1.1% annual growth is better than expected is a major part of the problem. A look at UK GDP growth for the past 5 years gives a sense of why the people there are so unhappy. Of course, hamstringing yourself with the worst energy policies on the planet are a big part of this outcome, and that defines the Starmer administration.

Source: tradingeconomics.com

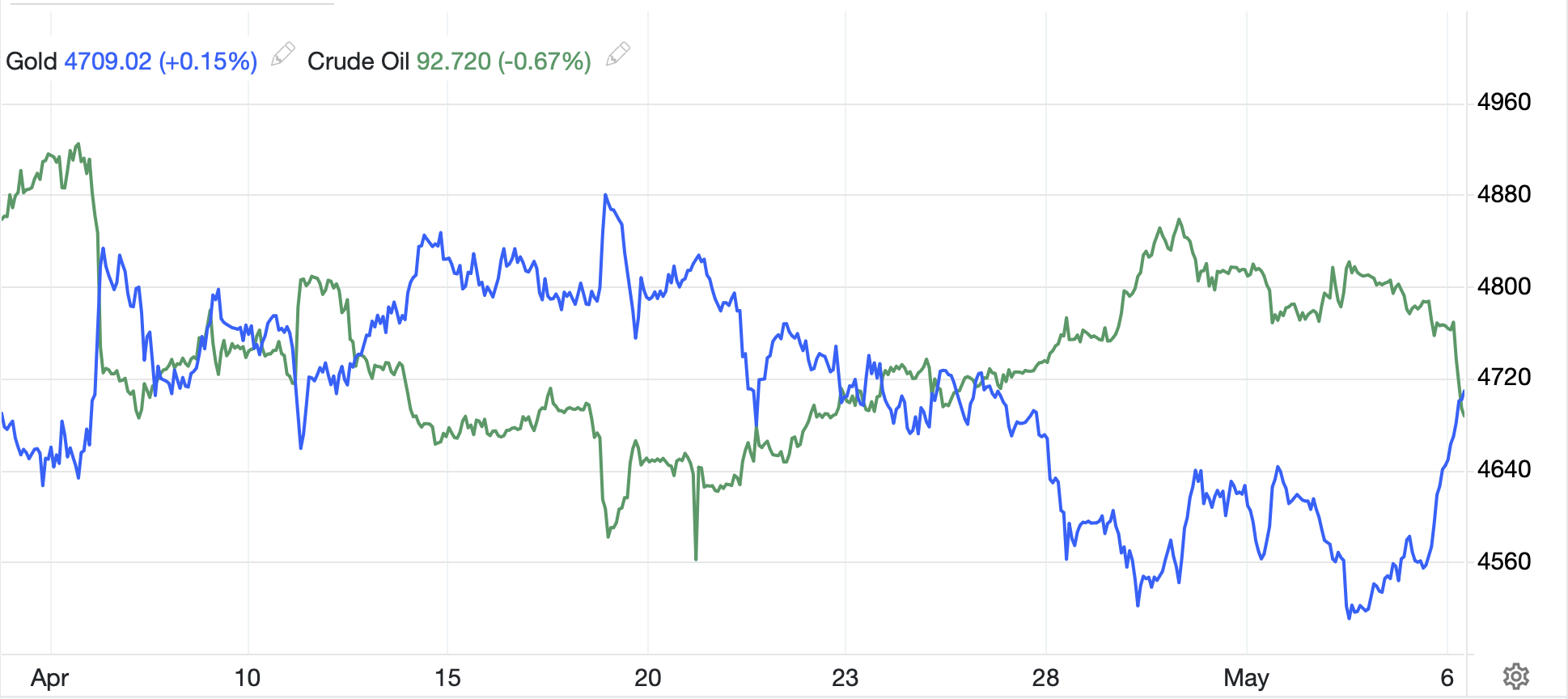

Finally, a turn to commodity markets shows…almost no movement. Both oil (-0.1%) and gold (+0.1%), the leaders in the category, are going nowhere right now. We have seen other commodities sink a bit (silver -0.8%, copper -0.7%), but given their volatility, those are also limited moves in reality. When it comes to the oil market, there is an enormous amount of discussion regarding the imminent collapse of the global economy as the shuttering of the Strait is going to lead to a virtual energy apocalypse. But to my eye (and I am not an oil trader) I cannot help but look at the below chart and see a market that has found a pretty good balance between supply and demand at around $100/bbl.

Source: tradingeconomics.com

It is also important to remember that the oil market remains in a steep backwardation which tells us that supply issues over time are not a great concern. In fact, I read this morning that with the overall curve at current levels, some oil drillers are considering expanding operations to take advantage of the higher prices, yet another reason to expect that the fears of $200/bbl oil are massively overblown. They ain’t coming, I think.

On the data front, this morning brings the weekly Initial (exp 205K) and Continuing (1790K) Claims data as well as Retail Sales (+0.5%, +0.6% ex-autos) and Business Inventories (+0.8%). We hear from a few more Fed speakers but, again, I don’t think they are of much importance right now. The market is not pricing in any Fed funds movement for the rest of the year, and then a 25bp hike is the new view after that. But the one thing we know about Fed funds futures is they are subject to major changes based on policy comments. I’m sure we are all anxiously awaiting Chair Warsh’s first meeting next month.

And that’s it for today. Quiet markets and no reason to think that will change right now. Remember, fiat currencies are still crap, but nothing has changed my view that the dollar is the best of the bunch.

Good luck

Adf