For one day, at least, there was hope

The war might be shrinking in scope

But as of this morning

The markets are warning

That there’s still a slippery slope

The Strait is still under duress

Though some ships have found an egress

The truce is still frail

And much can still fail

Beware, we’re not past all the stress

The most interesting story, to me, about the cease fire is that Pakistan gave each side different terms so they both agreed to something different. This might explain the confusion over whether the Israeli attacks in Lebanon were part of the deal, and the question about Iran’s collection of tolls for passing through the Strait of Hormuz. On the one hand, that very duplicity calls into question the help that Pakistan actually offered in this process. Of course, the other side is, if that subterfuge is what got the two sides talking directly, and apparently VP Vance is on his way to do that, then it was very worthwhile. It is still far too early to determine if the fighting is going to stop and if the Strait is going to fully reopen soon, but talks are better than no talks, at least in my view.

As to who ‘won’ the war, that question will take a long time to answer. After all, whatever the short-term impacts, if Iran is dramatically weakened and its sponsorship of terrorism is eliminated, the world will have won the war, certainly the Middle East as a whole, as it will make for a much safer place. However, if the radical wing of the regime there remains in charge and continues to press its global ambitions, then nobody will have won the war, not the rest of the Gulf nations and not the Iranian people themselves.

In the meantime, since I am not going to bring about world peace, let’s see how markets are behaving. After all, they really do offer some insight into global affairs as price information is some of the best information available.

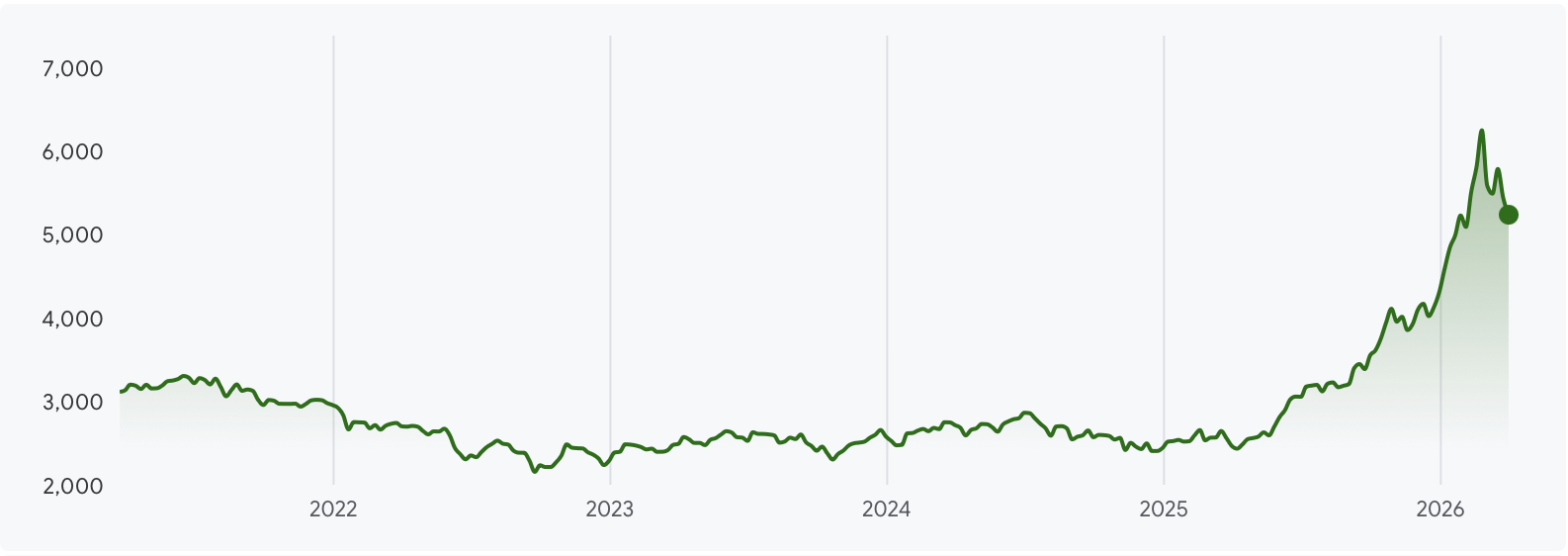

After yesterday’s sharp decline in oil prices, we have seen a bounce this morning (+5.0%) although as I type at 6:50, it remains just below $100/bbl. You can see from the chart below of the past month that we’re kind of in the middle of the range. Alyosha (read Market Vibes on Substack) explains the Point of Control as the place where a market trades most frequently during a given period of time. His records show that $94/bbl is that number in WTI, a level we touched and have since bounced from. Headlines continue to be the driver, and I suppose that the next key headlines will be comments regarding the peace talks.

Source: tradingeconomics.com

NatGas prices (+0.3% in US, +2.0% in Europe) are also rebounding, but not nearly as dramatically. In a way that is surprising as the Iranian attack on Ras Laffan, Qatar’s main LNG facility has inflicted significant damage, sufficient to cause multiple years of reduced production, yet gas has not been nearly as impacted despite its critical importance to the global economy.

As to metals markets, gold (+0.4%) continues to find support, but is still far below the highs seen in January, and silver (0.0%) is at a loss for its next move. On the one hand, silver, especially given its multiple industrial uses, seems likely to have significant long-term support, but right now, along with gold, it feels like owners are still liquidating as they need cash, and speculators aren’t interested yet. I still like both in the long run.

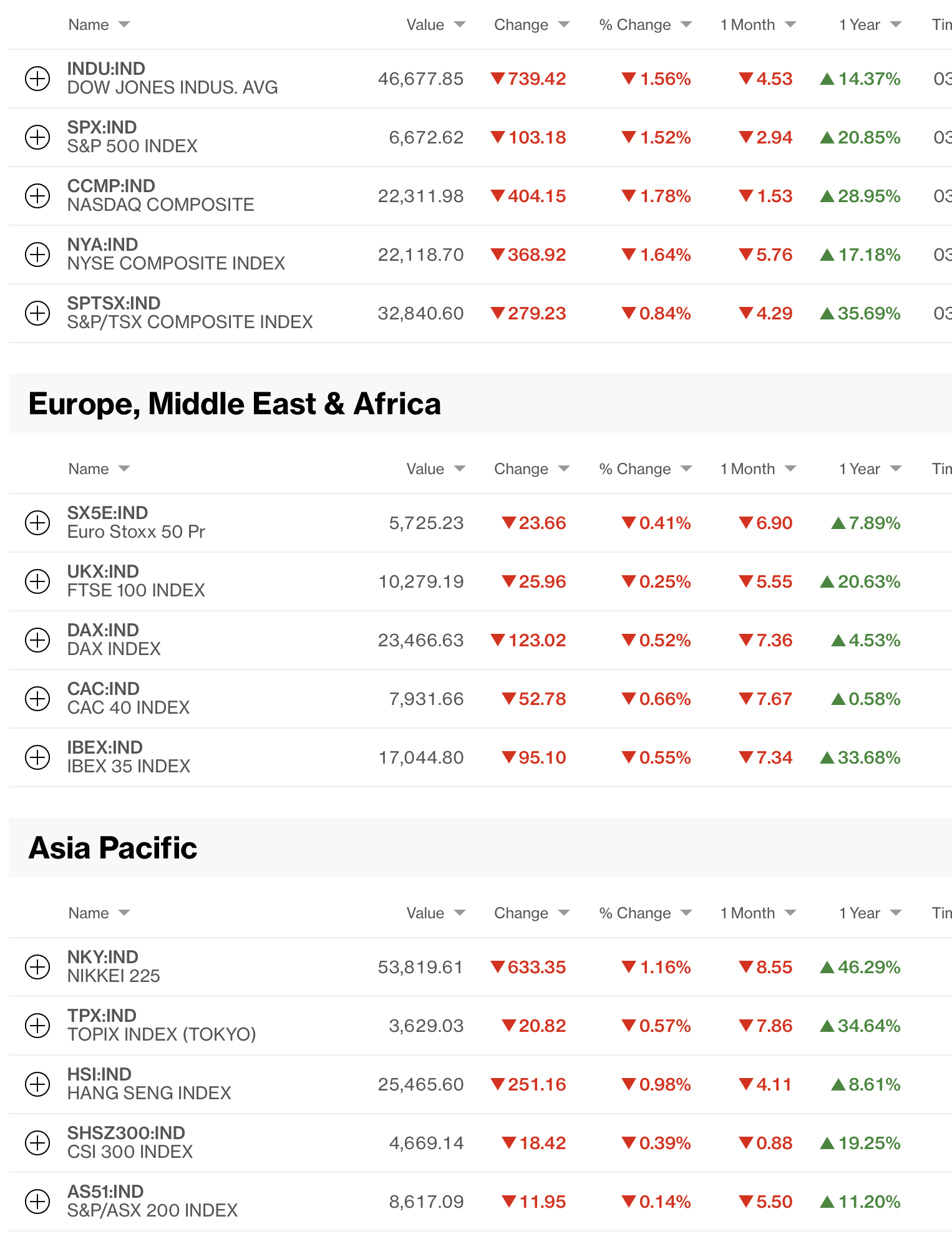

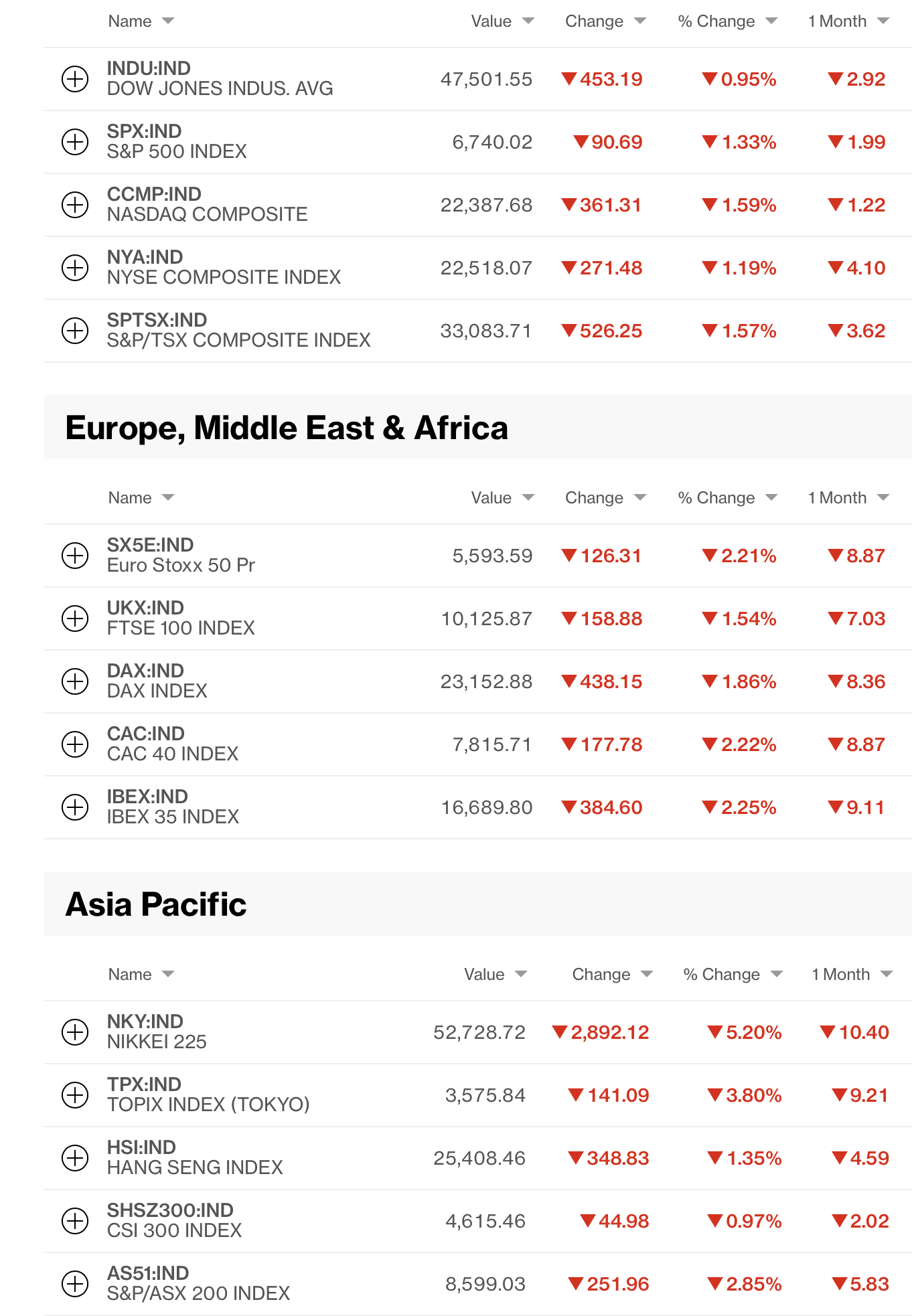

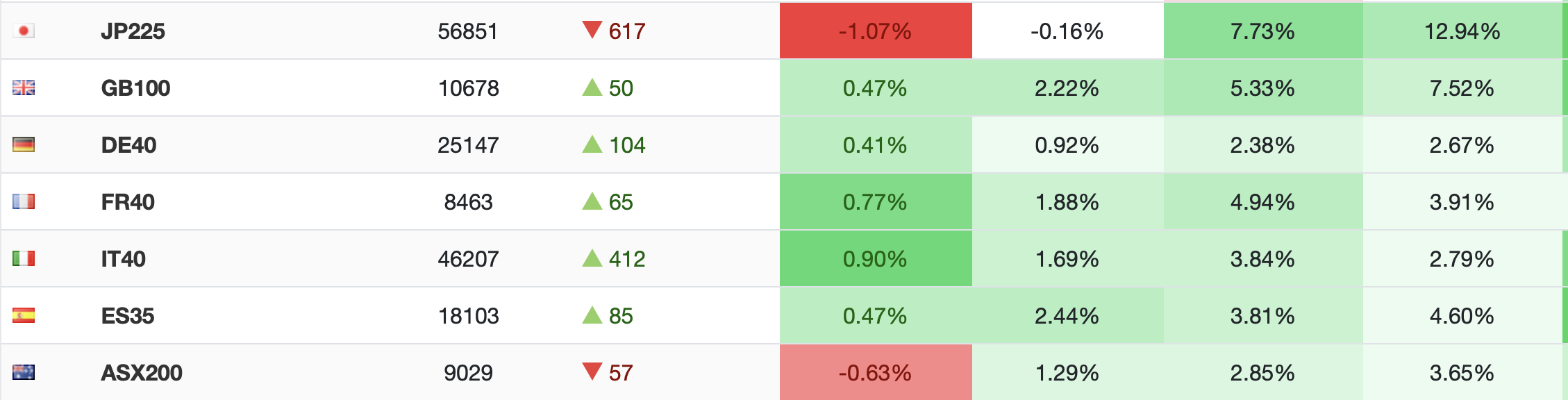

Turning to equities, yesterday’s huge rallies culminated with every major US market gaining 2.5% or more. But that seemed to be the peak, for now at least. Overnight, Tokyo (-0.7%), China (-0.6%) and HK (-0.5%) all slipped a bit and that was emblematic of most of Asia with Korea (-1.6%), India (-1.2%) and most other markets slipping. The few gainers (Australia, Taiwan, Indonesia) all managed gains on the order of just 0.2% or so, hardly inspiring.

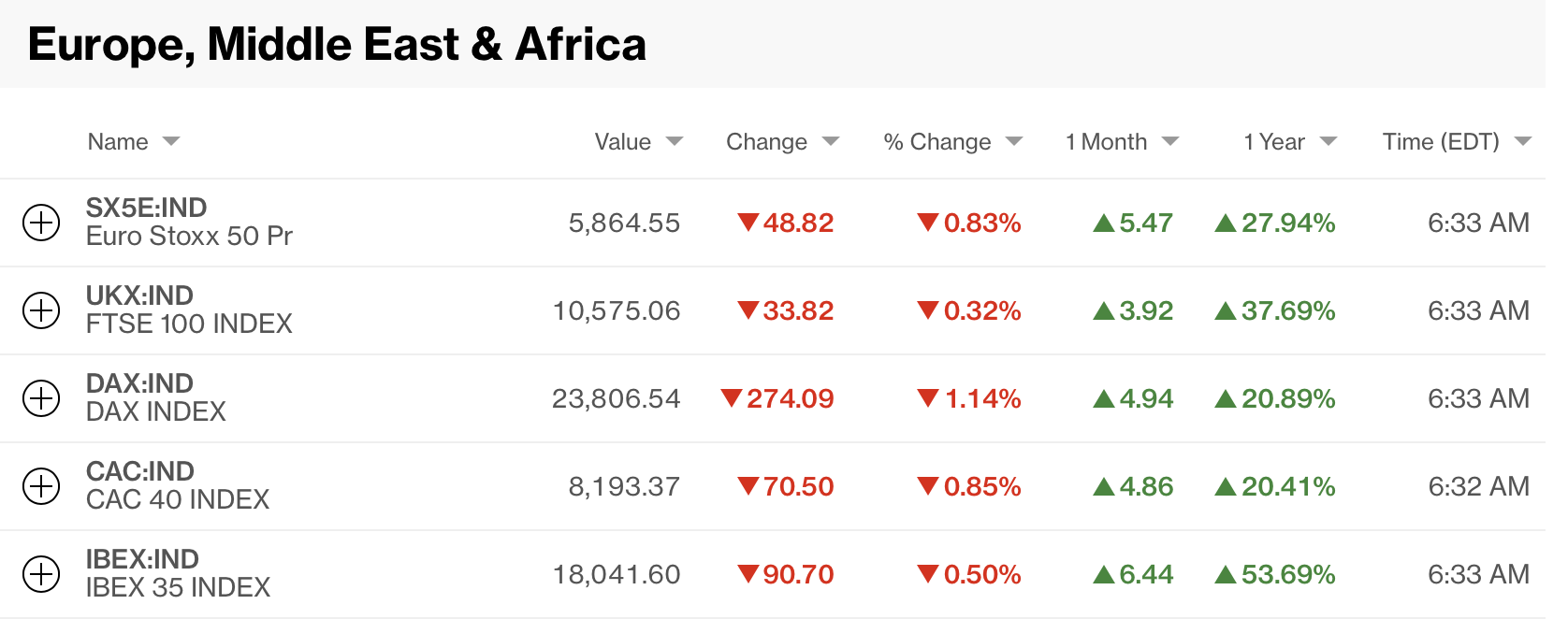

In Europe, the Bloomberg screenshot explains things well, as yesterday’s euphoria gives way to more circumspection this morning, at least for now. However, as you can see, equities remain far closer to their highs, than lows based on the gains over the past year.

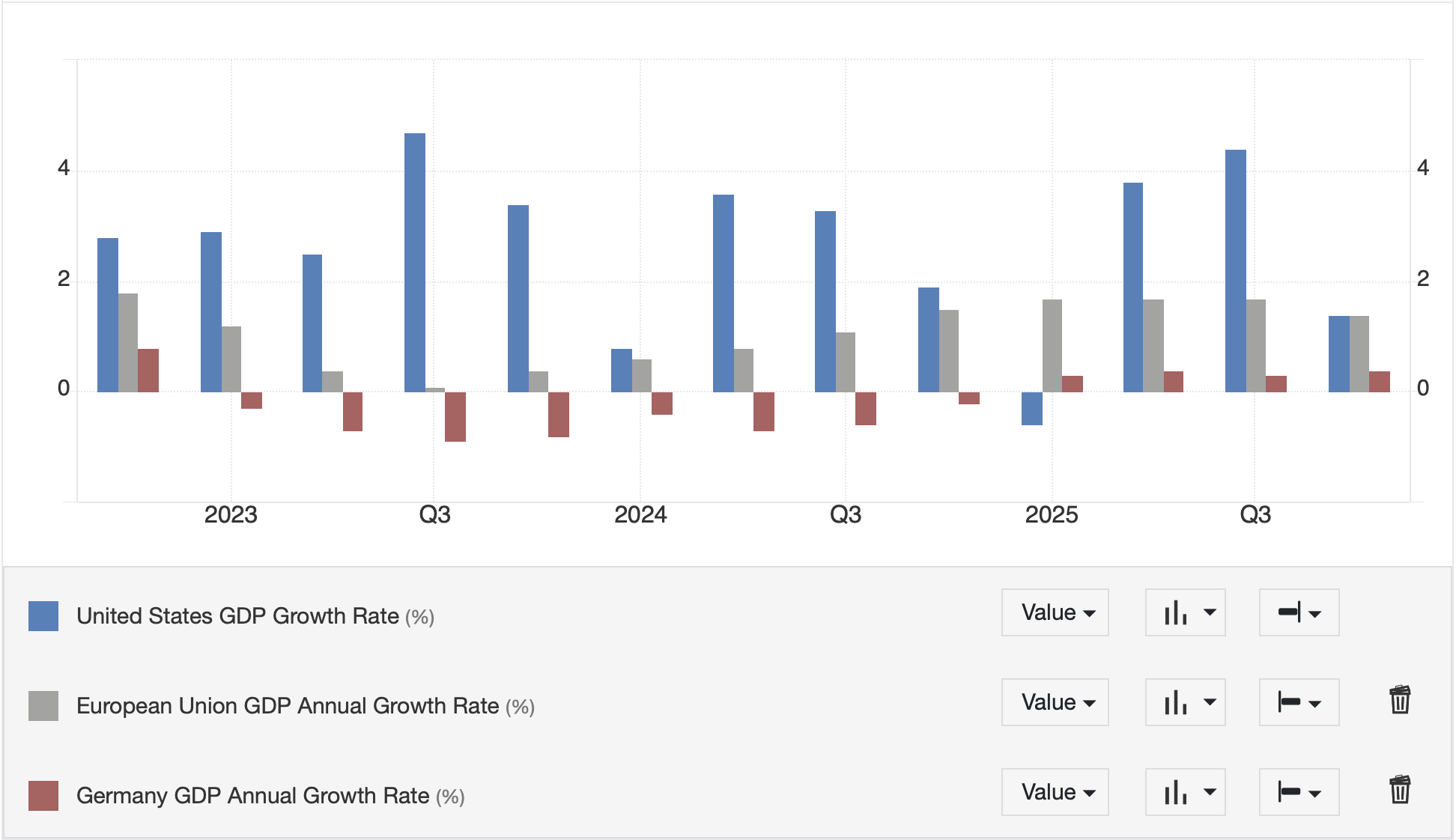

There was some data this morning showing German IP far weaker than expected at -0.3% after a revised 0.0% print in January. With this in mind, it is understandable that the DAX is lagging, and it seems ever more likely that Germany is going to have yet another quarter with no economic growth. Looking at US futures, at this hour (7:10) they are all sitting lower by -0.3% or so.

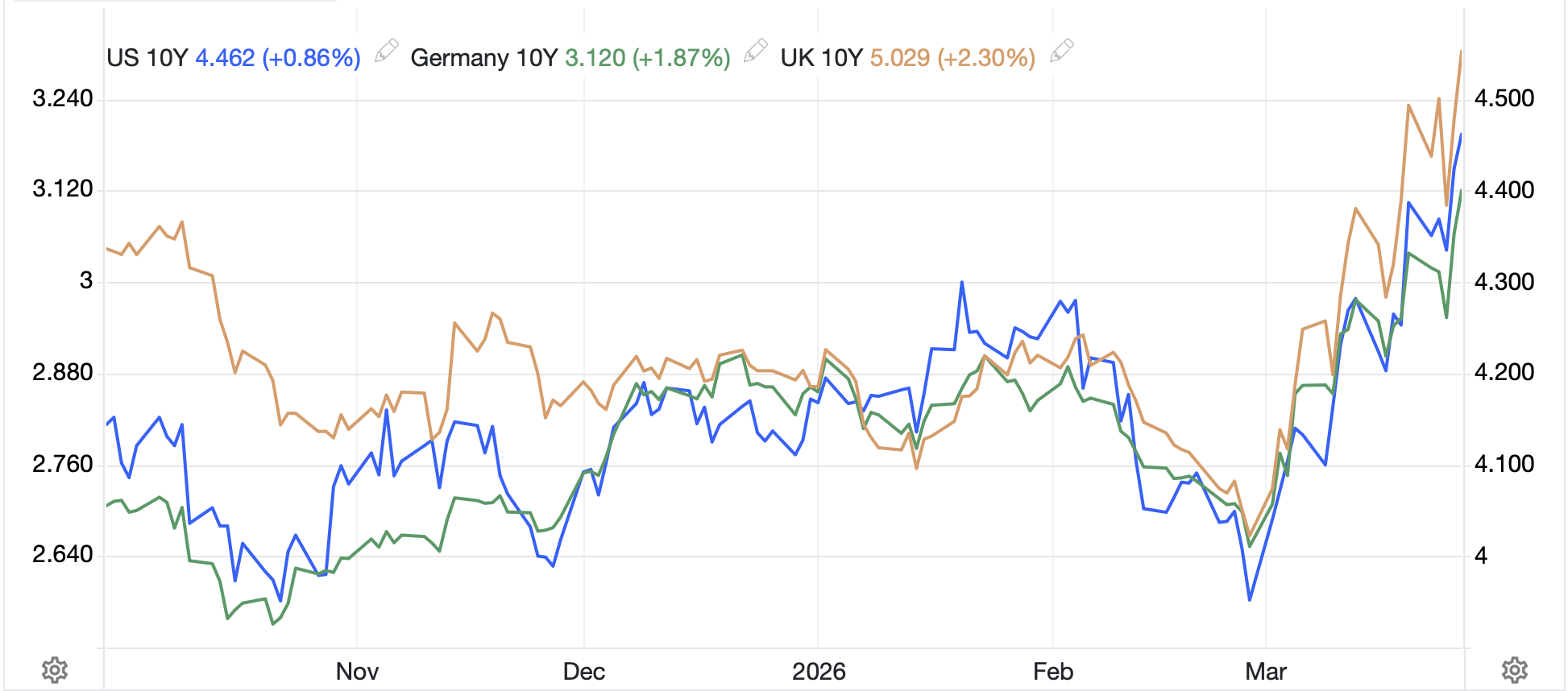

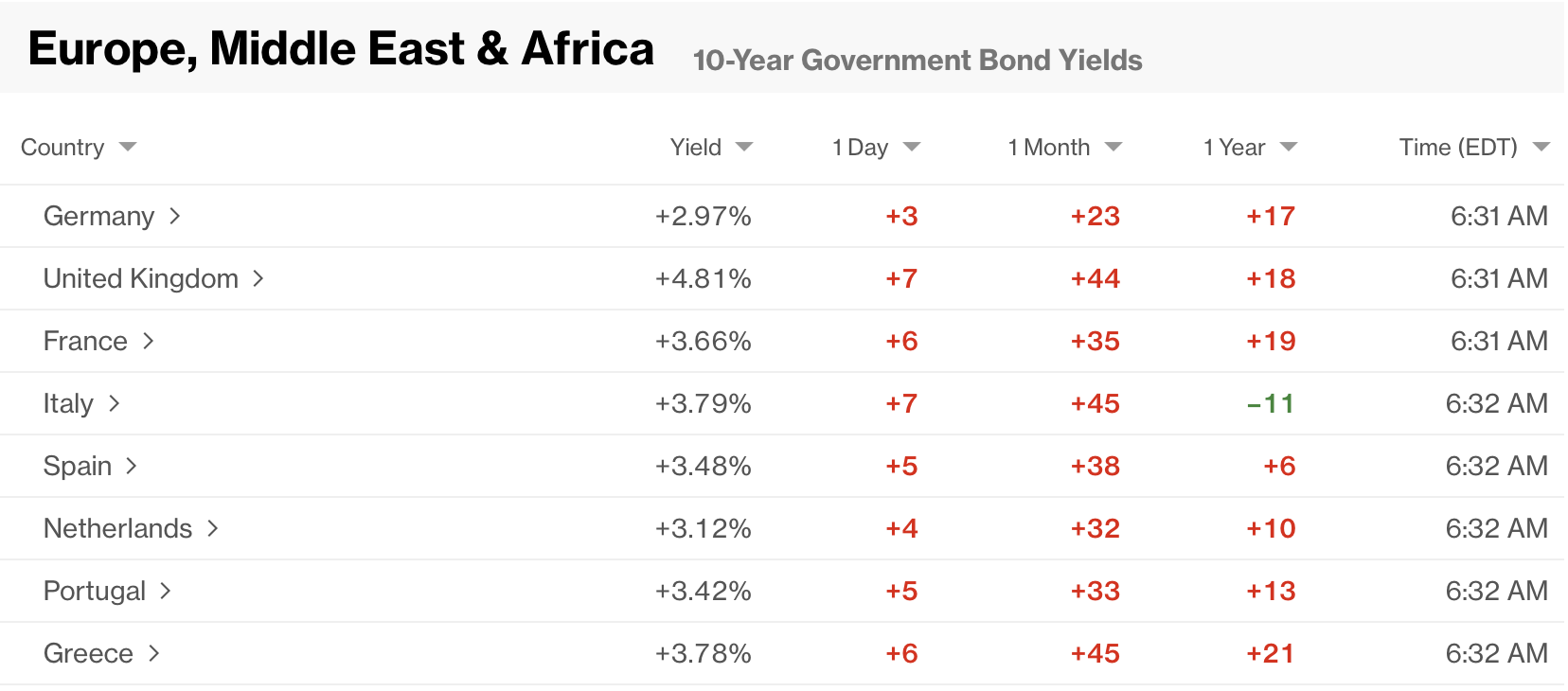

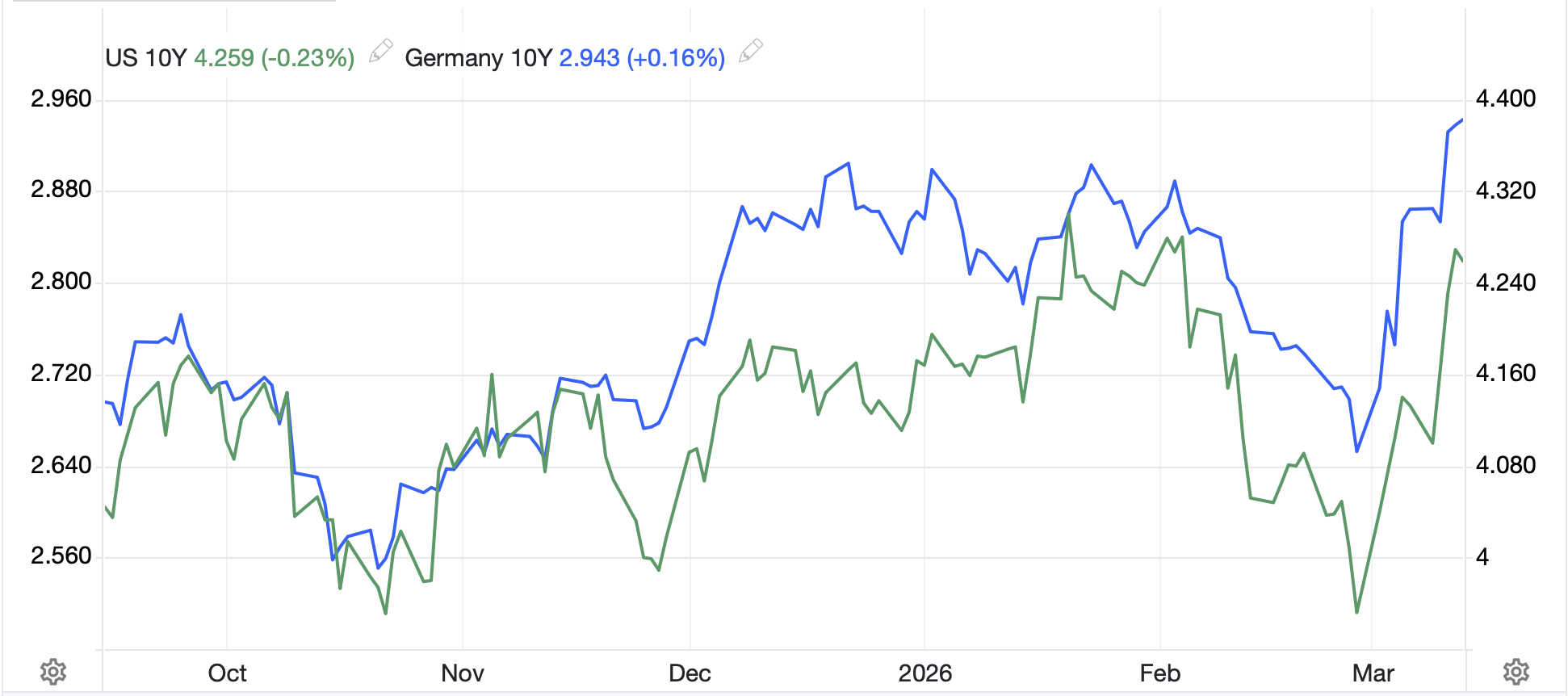

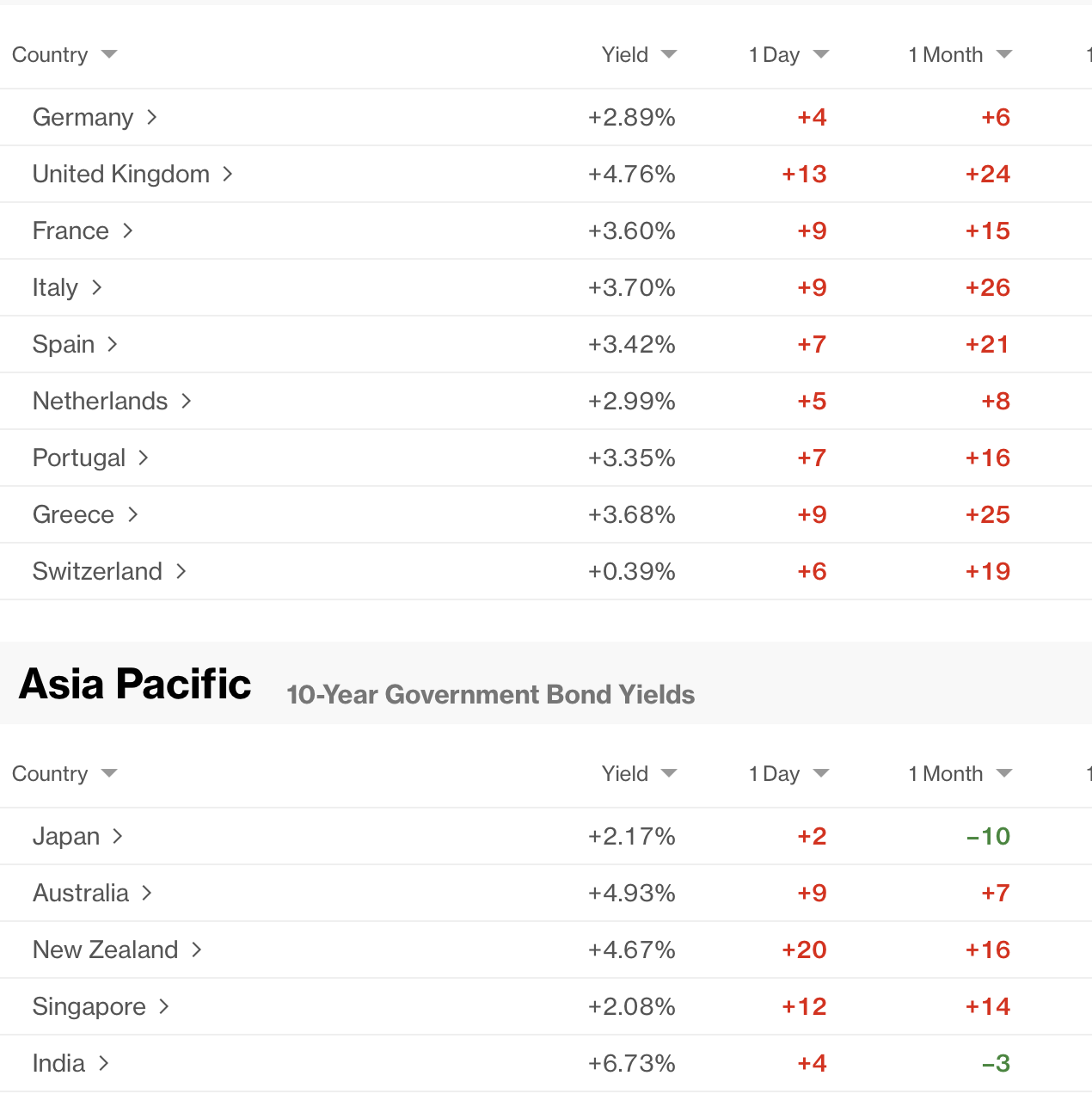

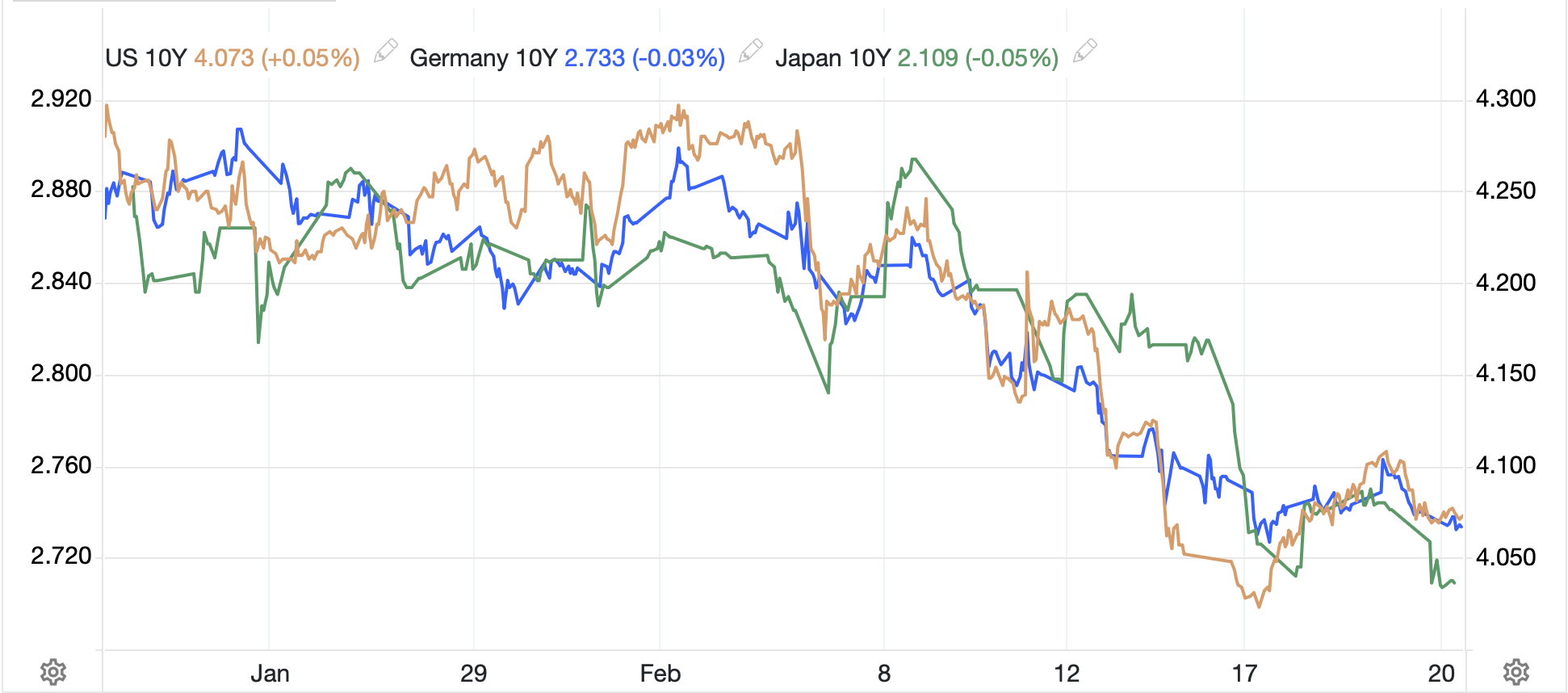

In the bond market, Treasuries (-1bp) are the outlier this morning as all European sovereign yield are higher between 4bps and 6bps. Yesterday’s euphoria over the potential end of the fighting and the decline in energy prices is being rethought as, undoubtedly, even if a peace treaty is agreed and signed over the next two weeks, there are going to be major impediments to the resumption of the pre-war status quo, if it ever returns. I also suspect that investors here are growing concerned that after the European response to this military action, fears the US is going to exit NATO (NATO General Secretary Mark Rutte spent 3 hours behind closed doors in the White House yesterday with no comments afterwards) means that Europe is going to have to borrow and spend even more on their own defense. This will, of course, strain the budgets as the turn from butter to guns may be a difficult one politically.

Finally, the dollar this morning is mixed. It should be no surprise that NOK (+0.6%) is leading the way as oil rebounds, although three other major oil producers, CAD, MXN and BRL are essentially unchanged in the session. The euro (+0.15%) has continued a touch higher from yesterday while the yen (-0.25%) is slipping a bit. As I said, it is a mixed session overall with no direction of which to speak.

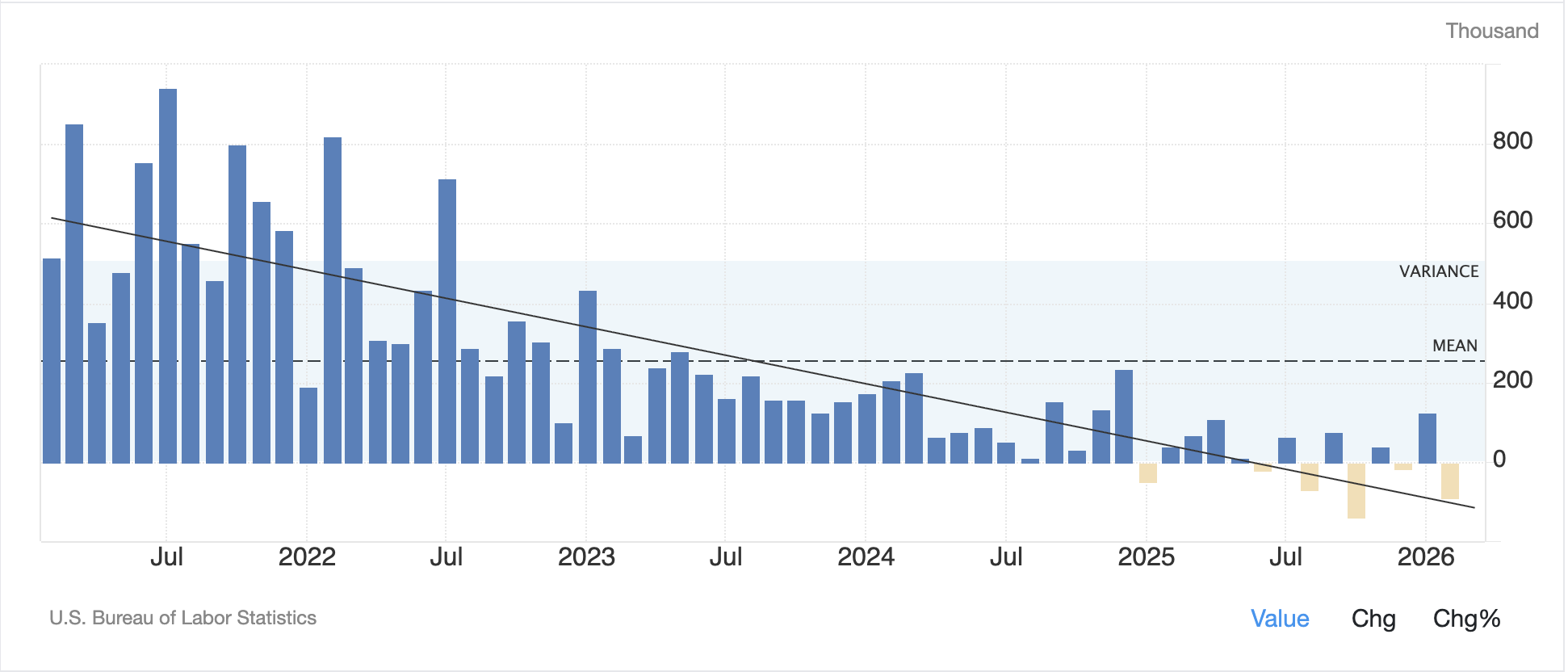

Turning to the data, this morning we get the regular Initial (exp 210K) and Continuing (1840K) Claims as well as the final look at Q4 GDP (0.7%). But in addition, we get the February PCE data suite, which typically comes at the end of the following month, but given the ongoing issues from the shutdown, seem to be behind. Expectations are for Personal Income (+0.3%), Personal Spending (+0.5%), PCE (0.4%, 2.8% Y/Y) and core PCE (0.4%, 3.0% Y/Y). And those numbers are from before the war. Arguably, of much more importance is tomorrow’s March CPI data, which we can discuss tomorrow.

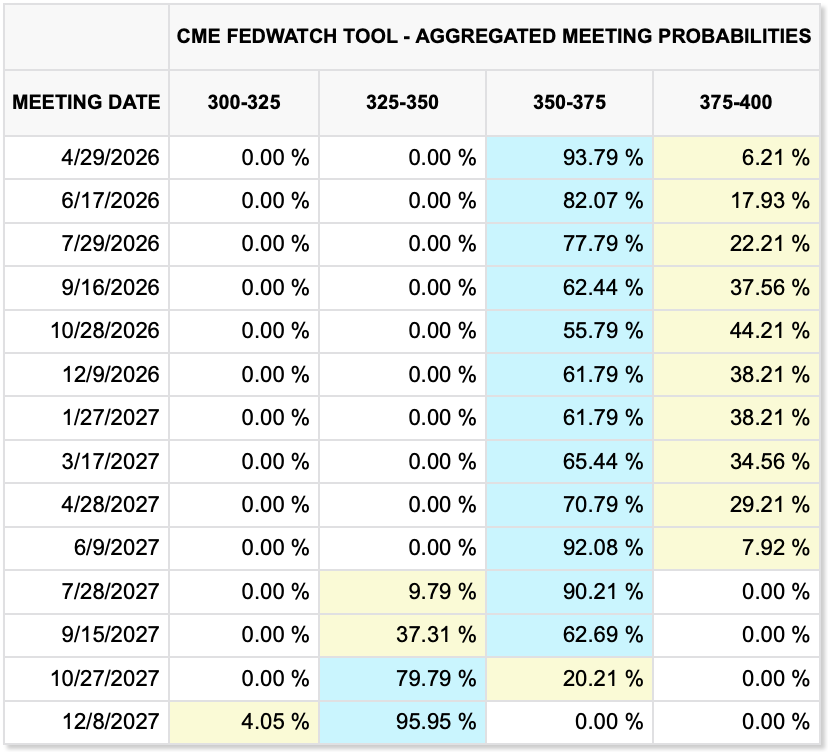

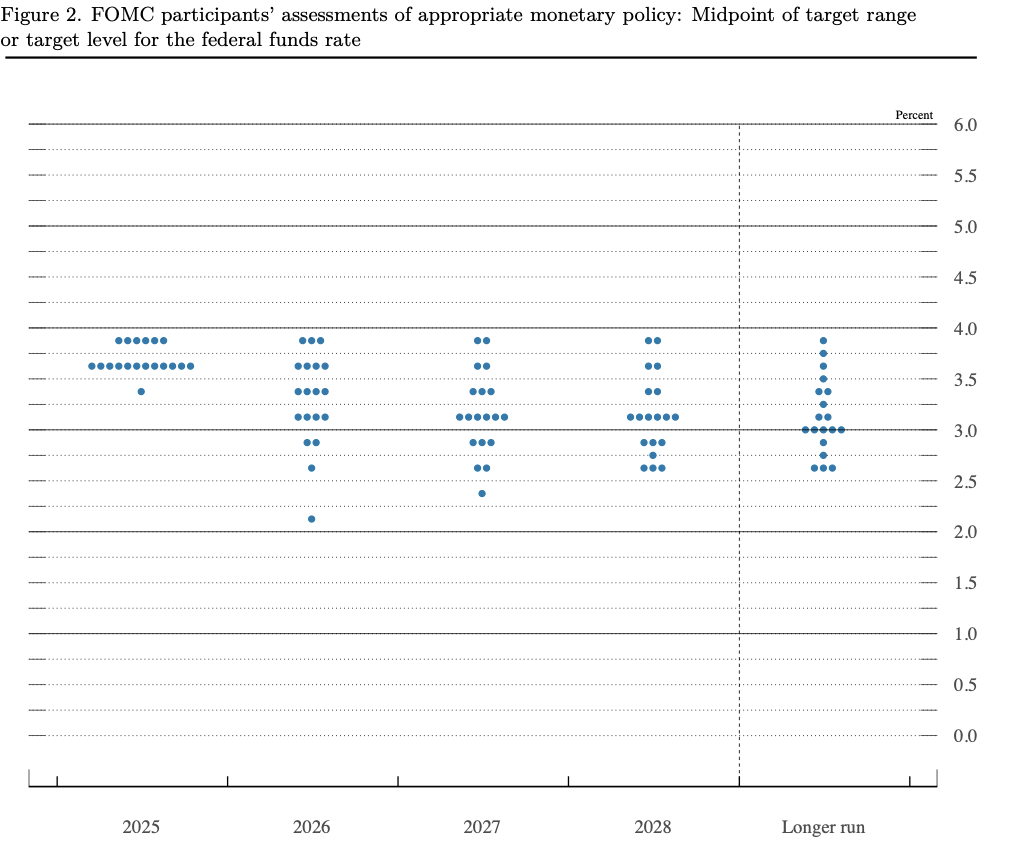

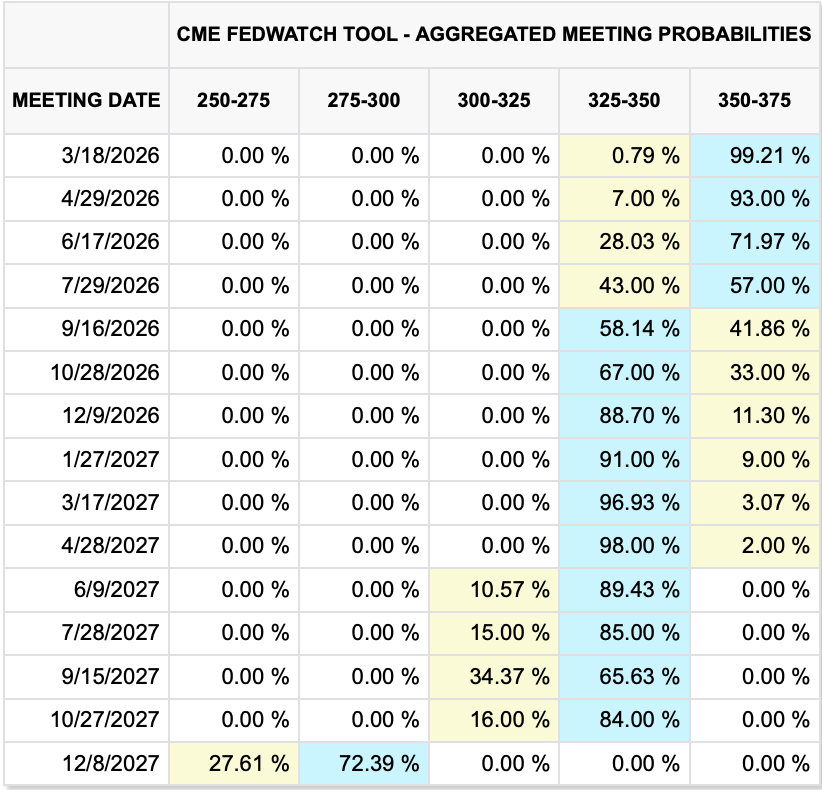

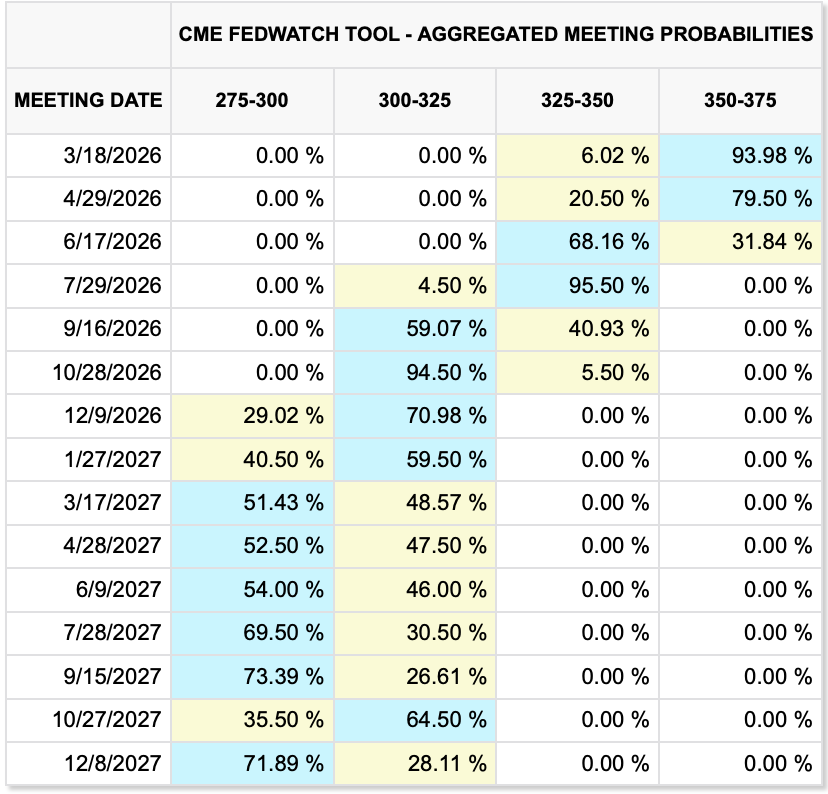

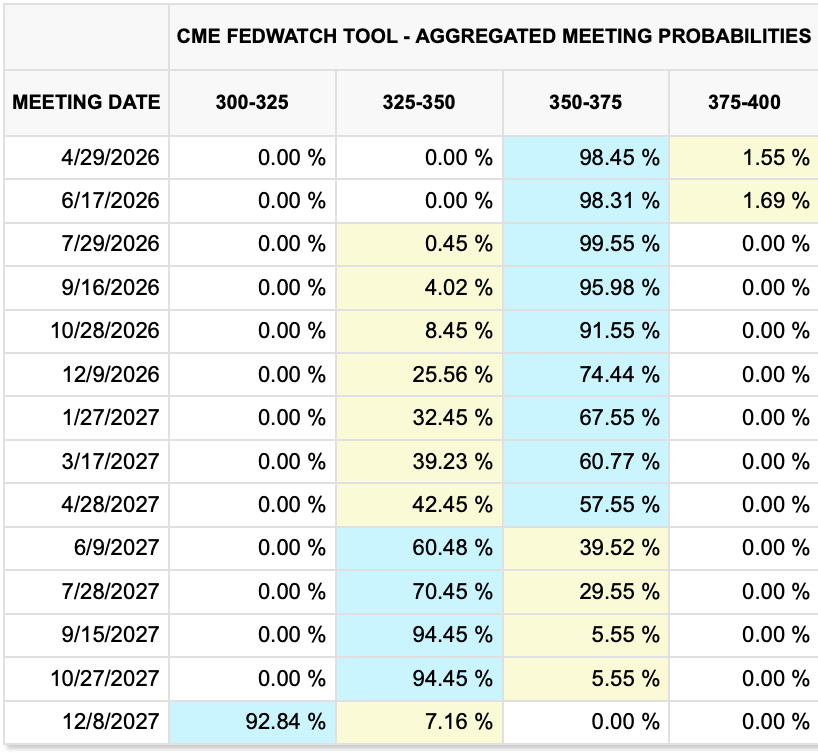

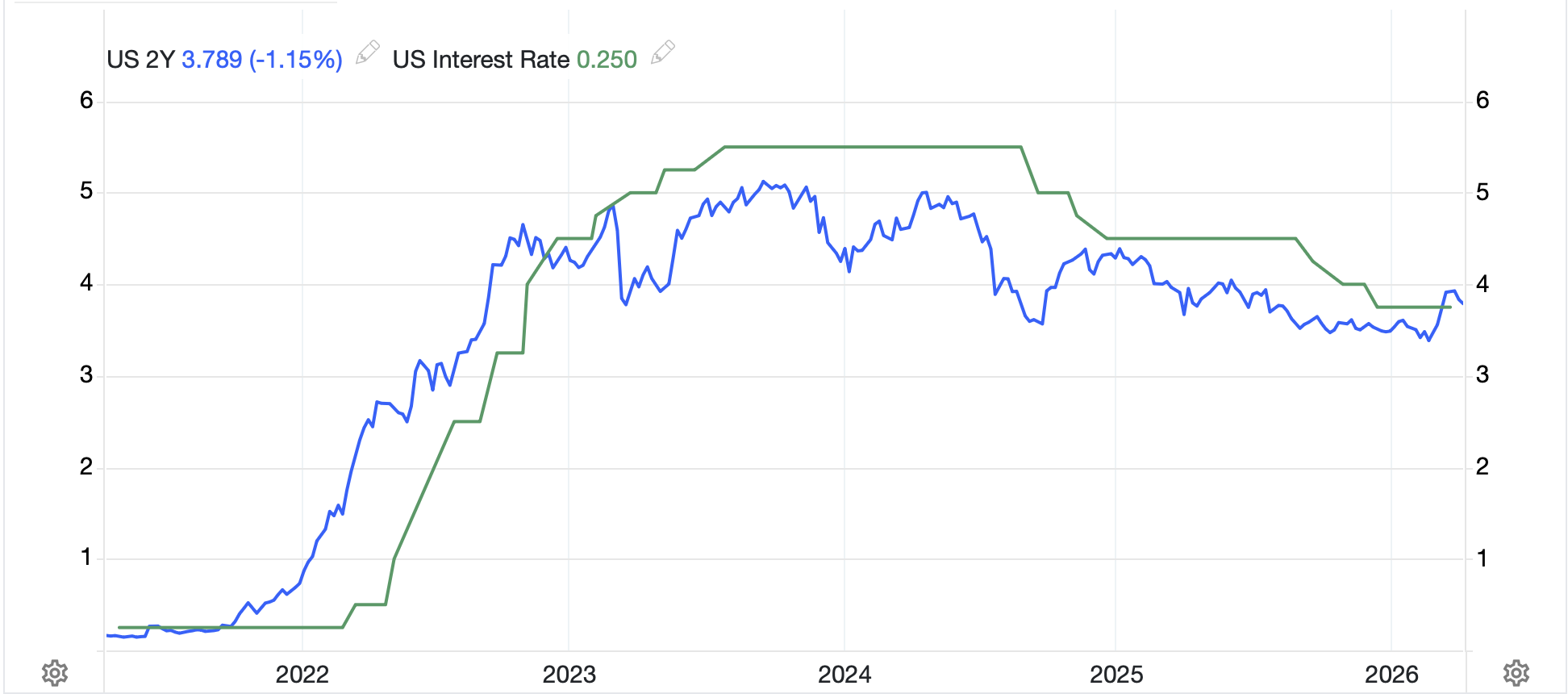

Yesterday saw yet another build in oil inventories in the US, something which will eventually lead to lower prices, and the FOMC Minutes explaining that they were concerned about both inflation and employment. In the meantime, a look at the Fed funds futures market shows that the market is pricing even less chance of a rate cut in 2026 with the first one now not assumed until June 2027.

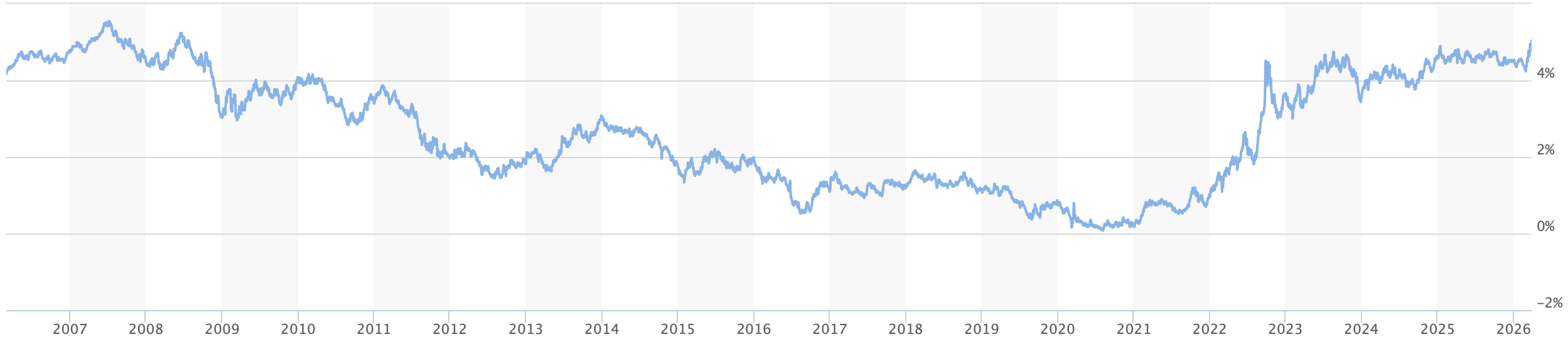

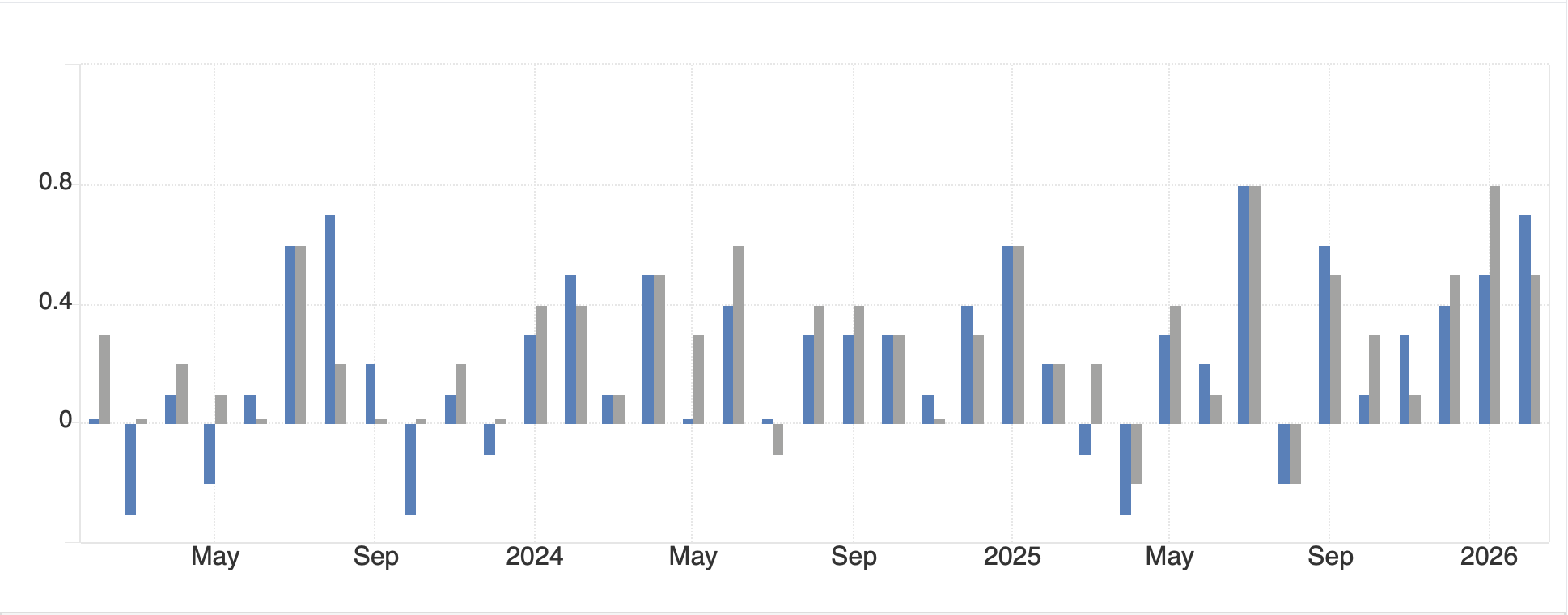

The thing about futures pricing, though, is that while it does give a good sense of sentiment, it is subject to change quickly on new news. There is much to be said about watching the 2yr Treasury note as the best predictor of Fed funds going forward and you can see how tight that relationship is in the chart below.

Source: tradingeconomics.com

My view on inflation is not that sanguine, and I fear it is going to remain far higher than the Fed’s 2.0% target for Core PCE for a long time to come. Ultimately, that plays into my views on owning things that hurt when they fall on your foot, or shares in companies that generate profits. (This is where I also mention USDi, for those of you inclined in the crypto space, as the only inflation-tracking currency around. Learn more at http://www.usdicoin.com)

As to today, this is the rebound and since nobody knows what will play out in the talks, I would look for a choppy, but inconclusive session in pretty much everything.

Good luck

Adf