Said Waller, I’m not in a rush

To cut, though some hopes that may crush

Inflation’s still sticky

And so, it’s quite tricky

For us to cut with prices flush

He also said that PCE

Tomorrow, may help him to see

If trends from Q4

Still hold anymore

Or whether its new home is three

Investors and traders have a problem, or perhaps several of them. The timing of key data and events coincides with the Easter holiday weekend as well as month- and quarter-ends (and for Japan, fiscal year end). Their problem is to discern how much movement is based on new information and the anticipation of tomorrow’s releases versus how much movement is a result of declining liquidity as trading desks throughout Europe see staff exit early for the holiday weekend. If movement is due to new information, perhaps a response is required. However, if it is due to illiquidity, sitting tight may well be the right thing to do.

The biggest news yesterday came from a speech by Fed Governor Chris Waller. He certainly didn’t bury the lead as this was his opening paragraph:

“We made a lot of headway toward our inflation goal in 2023, and the labor market moved substantially into better balance, all while holding the unemployment rate below 4 percent for nearly two years. But the data we have received so far this year has made me uncertain about the speed of continued progress. Back in February, I noted that data on fourth quarter gross domestic product (GDP) as well as January data on job growth and inflation came in hotter than expected. I concluded then that we needed time to verify that the progress on inflation we saw in the second half of 2023 would continue, which meant there was no rush to begin cutting interest rates to normalize the stance of monetary policy.”

He spent the rest of the speech going through particular details about the labor market and the broad economic measures and data we have seen with the conclusion being, higher for longer (H4L) is still the correct policy. While he did not explicitly say he moved his ‘dot’ to less than three cuts, I believe we can infer that he is now in the 2-cut camp based on the entirety of the speech.

Given the absence of other data released yesterday, as well as the dearth of other commentary, he was the main event. Interestingly, despite what appears to have been a more hawkish tone to his comments, equity markets were sanguine about the news and rallied anyway. To me, that indicates equity investors have made their peace with the current interest rate structure.

What does this mean for markets going forward? First, let’s assume that there are three potential ways the Fed funds discussion can evolve going forward; 1) raising rates from here, 2) status quo (H4L) and 3) starting to reduce rates. Based on recent market price action in both equities and bonds, there is very little fear attached to number 2. Investors have absorbed this information, are pricing a 61% probability of a June rate cut but are now pricing slightly less than 3 cuts in for the rest of the year. In other words, H4L is no longer frightening. The key near-term risk to markets is number 1; if the inflation data not merely drags on at current levels but starts to accelerate again. I believe that is what would be necessary for the FOMC to consider tightening policy further and my take is that risk assets will not respond well to that situation. Stocks would suffer on a valuation basis while bonds would likely sell off on the basis of still untamed inflation.

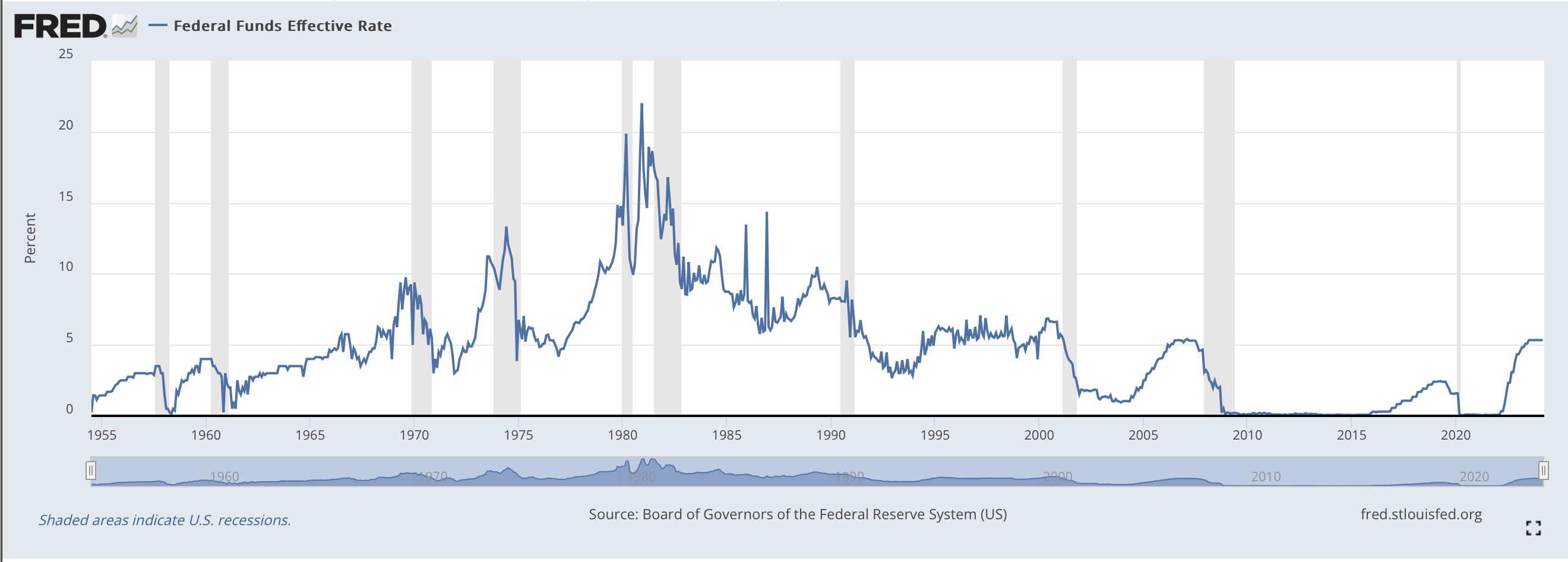

It is the third choice though, cutting rates, that is likely to generate the most fireworks. Certainly, the initial movement will be a risk asset rally as investors will make the case that a lower discount rate means higher current values as well as invoke the idea that money currently invested in money-market funds will quickly move to stocks as interest rates decline. At the same time, the front end of the yield curve will see yields decline amid what is likely to be a bull steepening of the curve. And that’s the problem. History has shown that when the curve re-steepens after a period of inversion, that is when trouble comes for markets. As can be seen in the chart below from the St Louis Fed’s FRED database, the correlation between a declining Fed funds rate and a recession is very high (grey shaded areas represent recessions).

This makes perfect sense as when the economy is heading into, or more likely already in, a recession, the Fed cuts rates to address the issue. As such, the fervent desire to see rate cuts seems misplaced. Strong economic activity comes alongside higher interest rates, not rate cuts. If the Fed is cutting, that means there are problems as remember, whatever they say, they are always reactive, not proactive. So, while the initial risk asset move may be positive, history has shown that during recessions, the average decline in the equity markets is on the order of 30%. Keep that in mind if you are hoping for the Fed to cut rates.

Ok, let’s tour the markets from overnight to see how things stand ahead of a bunch of data this morning. Japanese stocks suffered overnight, falling -1.5%, as the threat of intervention did little to strengthen the yen but certainly got some investors nervous. As well, it is Fiscal year end there tonight, so I imagine we are seeing some profit taking given the remarkable run Japanese stocks have had in the past twelve months, rising 44% in yen terms. The rest of Asia saw more gainers than losers with China, India and Australia all following the US markets higher although South Korea and Taiwan did lag. In Europe, most bourses are higher this morning, but the gains have been more modest, on the order of 0.3% or so. And as I write (7:30), US futures are unchanged on the day after yesterday’s gains.

In the bond market, yields are broadly higher with Treasuries (+3bps) reversing yesterday’s decline and similar price action in Europe with all sovereign yields higher by between 3bps and 5bps although Italy (+8bps) is an outlier as their finances are starting to look a bit dicier. I would be remiss if I didn’t mention that JGB yields have edged down another basis point and are now at 0.70%. There is no sign that yields are running away here.

Oil prices (+1.6%) continue to climb on the same story of reduced supply and ongoing demand. Yesterday’s EIA data showed a smaller inventory build than forecast and there is no indication that OPEC+ is going to open the taps anytime soon. Gold (+0.8%) is continuing its recent rally, following on yesterday’s move, as investors throughout Asia continue to hoard the barbarous relic. As to the base metals, they are essentially unchanged over the past several sessions, seemingly waiting for the next economic data.

Finally, the dollar is feeling its oats this morning, rallying against every one of its G10 counterparts with this group (AUD -0.6%, NZD -0.6%, SEK -0.6%, NOK -0.6%) leading the way lower. As well, the EMG bloc is also under pressure led by ZAR (-0.7%) and HUF (-0.6%) although the entire bloc is under pressure. Of note is CNY (-0.15%) which the PBOC continues to struggle with as they cannot seem to decide if matching yen weakness is more important that maintaining stability. It seems to me they are really hoping for BOJ intervention to reduce pressure on the renminbi.

On the data front, there is a bunch today starting with Initial (exp 215K) and Continuing (1808K) Claims, as well as the final look at Q4 GDP (3.2%). As well we get Chicago PMI (46.0) and Michigan Sentiment (76.5) to finish out the morning. There are no scheduled Fed speakers, but then, all eyes will be on Powell tomorrow.

It seems to me that Governor Waller made it clear that the tone in the Eccles Building is for more patience until they see inflation decline, or perhaps see the employment situation worse substantially. With that as the backdrop, it is hard to see a good reason to sell dollars. Keep that in mind for your hedging activities.

Good luck

Adf