The story is still ‘bout the Fed

And whether, when looking ahead

They see skies are blue

And so, they eschew

A rate cut the bears will all dread

But if they are growing concerned

The ‘conomy’s lately downturned

Then fifty will be

What we all will see

And bears, once again, will be spurned

As we move closer to the FOMC announcement and Powell press conference, the nature of the discussion has focused entirely on the size of the rate cut that will be announced tomorrow. Yet again this morning, the Fed whisperer, Nick Timiraos at the WSJ, published an article on the subject, once again making the case for 50 basis points. The money quote is below:

“Fed officials aren’t likely to regret a larger rate cut this week if the economy chugs along between now and their next meeting, in early November, because rates will still be at a relatively high level, he said. But if the Fed makes a smaller move and the labor market deteriorates more rapidly, officials will feel greater regret.”

As well, the futures market is growing more and more certain 50bps is coming as evidenced by the pricing this morning as per the below chart from the CME:

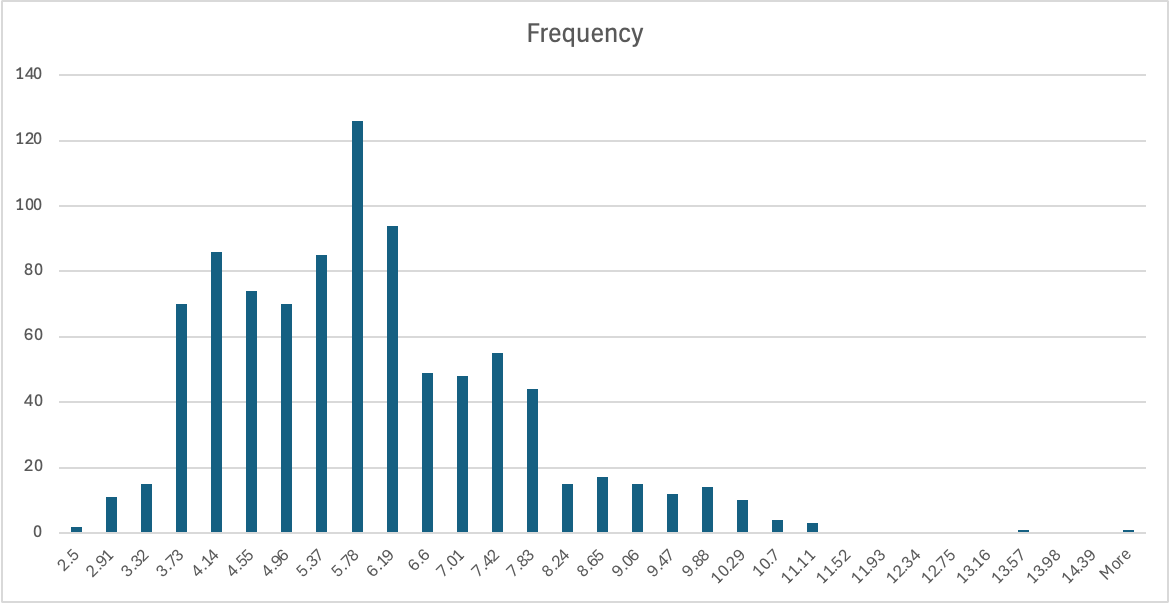

The interesting thing is that an unbiased (if such a thing exists) look at the data does not scream out to me that the economy is collapsing such that an aggressive start to an easing cycle is necessary. Unemployment remains in the lowest quintile of outcomes over the past 76 years. For reference, the median reading since January 1948 has been 5.5%, the average has been 5.7% and today it is at 4.2%. The chart below shows the distribution of outcomes over the entire data series from the FRED database.

Data source: FRED database; calculation: fx_poetry.com

It is difficult to look at this chart and think the economy is imploding. And let us consider another thing, the widely mentioned long and variable lags by which monetary policy impacts the economy. Whatever the Fed does tomorrow, the impact on almost the entire economy will not be felt for at least a year, if not much longer than that. After all, do companies really make a borrowing decision based on the marginal 25bps of interest cost per annum? I would argue that most corporate borrowing is based entirely on their current schedule of maturing debt and any forecast needs for capex or other funding. It strikes me that whether the Fed funds rate is 5.25% or 5.00% is not going to change much in the real economy.

Markets, of course, are a different kettle of fish in this discussion, but let’s face it, the bond market has already priced in 250 basis points of cuts in the next twelve months, so whether they start with 25 or 50 seems less relevant than the destination. Certainly, the equity market will try to goose things on a 50bp cut, and will almost certainly fall if the cut is only 25bps, at least initially, but again, will corporate profits change that much in the short-run because of this move?

In the end, I fear we make far too much of the outcome, at least in this case. Now, if Powell and the Fed were to decide that the recent call for a 75bp cut by three senators was an eloquent argument and did that, the market surprise would be substantial and the initial move in risky assets would be higher. But something like that would also engender fears that the Fed knows something bad about the economy that the rest of us have missed, and that would result in its own negative consequences. I guess the good news is we only have another 30 hours or so before we find out.

As to the market activity overnight, yesterday’s mixed US equity performance, with the DJIA making new all-time highs while the NASDAQ fell -0.5%, led to weakness in Tokyo (Nikkei -1.0%) as tech shares underperformed, but strength in HK (+1.4%) and much of the rest of Asia that was open. Both China and South Korea remained closed for holidays. In Europe, though, given the virtual lack of technology shares available, the DJIA was the template with all markets higher this morning led by Spain’s IBEX (+1.25%)), but with robust gains elsewhere on the order of +0.6% to +0.8%. As to US futures, at this hour (7:30), they are higher by about 0.25%.

In the bond market, yields continue to edge lower overall. While Treasuries are unchanged this morning, that follows another 2bp decline yesterday afternoon. In Europe this morning, sovereign yields are all lower by between -1bp and -3bps, catching up (down?) to the Treasury market as well as responding to pretty awful German ZEW numbers (Sentiment 3.6 vs. 17.0 expected and 19.2 last month; Current Conditions -84.5 vs. -80.0 expected and -77.3 last month). Germany remains the sick man of Europe and there is no doubt that they need to see the ECB start to cut rates more aggressively to help support their withering manufacturing sector. And one more thing, JGB yields fell -2bps last night and are now at 0.81% in the 10yr. While the focus will turn to the BOJ at the end of the week after the FOMC announcement tomorrow, the market does not appear to be particularly concerned over aggressive tightening there.

In the commodity markets, WTI (+0.15%) has crept back above $70/bbl for the first time in nearly two weeks as the big story in the market revolves around the net speculative Comex positioning which has turned negative for the first time ever. That means that hedge funds and speculators are net short oil futures. While they may have a negative outlook, the positioning does indicate there is an opportunity for a massive short-squeeze sometime going forward. As to the metals markets, they are little changed this morning, broadly holding their recent gains with both precious and industrial metals all showing healthy gains in the past week. A 50bp cut should support prices across the board here.

Finally, the dollar is softer again this morning, but by a modest amount, about -0.1% across the board. Those are the types of gains we have seen across the G10 and most of the EMG currencies with one outlier, MXN (-0.9%). However, the peso, which had strengthened nearly one full peso in the past four trading sessions looks more like it is responding to that movement than to any fundamental changes. The judicial review story is now old news although there may be some concerns that Banxico will cut more aggressively next week if the Fed does so tomorrow.

On the data front, this morning brings Retail Sales (exp -0.2%, ex autos +0.2%) as well as IP (0.2%) and Capacity Utilization (77.9%). We also hear from Dallas Fed president Logan this morning. It’s funny, a strong Retail Sales number could well weigh on the chances for a 50bp cut as further evidence that things continue to be moving along fine. Remember, even though inflation has been trending lower, it is not yet nearly at its target. Retail Sales strength would indicate that employment remains robust as people spend money more readily when they have a paycheck, so the need for more stimulus may just not be that critical.

In the end, my best take is the Fed is going to cut 50bps tomorrow and the market is going to increasingly price that in as the session unfolds. This will be especially true if Retail Sales is weaker than forecast, but even if it surprises on the upside, I remain convinced Powell wants to cut 50bps based on the number of articles discussing the idea in the mainstream press. Ultimately, I think the dollar will suffer a bit further on that move and commodities will be the big winners.

Good luck

Adf