The PPI data was shocking

Though previous months took a knocking

So, what now to think

Will CPI sink?

Or will, rate cuts, it still be blocking?

One of the features of the world these days is that the difference between a conspiracy theory and the truth has shortened to a matter of months. I raise this issue as yesterday’s PPI data was remarkably surprising in both the released April numbers, with both headline and core printing at MUCH higher than expected 0.5%, while the revisions to the March numbers were suspiciously uniform to -0.1% for both readings. The result was that despite the seeming hot print, the Y/Y numbers for both core and headline were exactly as forecast!

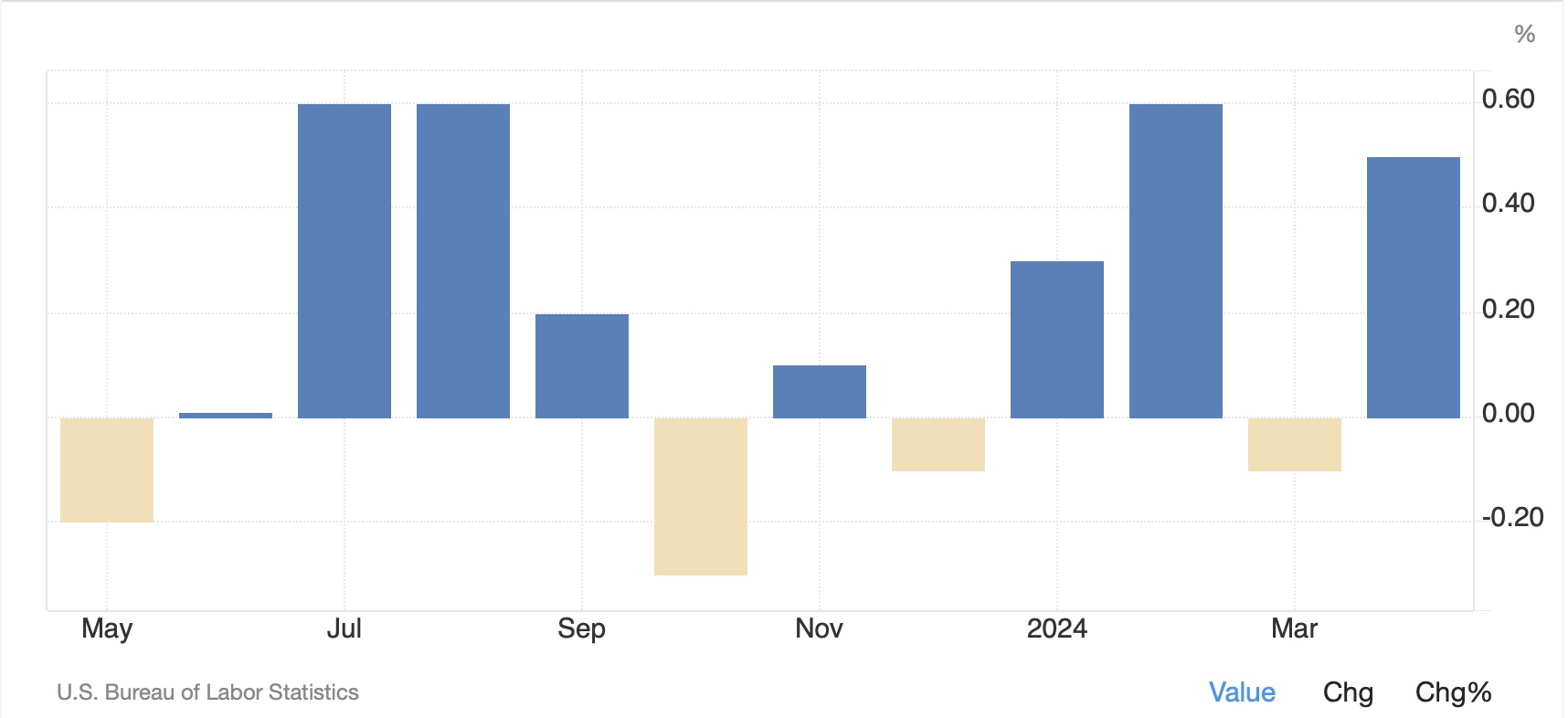

One of the things we know about data like PPI and CPI is that they are calculated from a sampling of data of the overall economy and there are fairly large error bars for any given reading. In that sense, it cannot be surprising that the data misses forecasts regularly. As well, given the sampling methodology, the fact that there are revisions is also no surprise. But…it would not be hard for someone to suggest that the Bureau of Labor Statistics, when it saw the results of the monthly readings, manipulated the data to achieve a more comforting (for the current administration, i.e., their bosses) result. I am not saying that is what happened, but you can see how a committed conspiracy theorist might get there. Now, in fairness, a look at the headline reading, on a monthly basis, for the past year, as per the below chart, shows that this is the 4th month in 12 that there was a negative reading.

Source: tradingeconomics.com

So, the fact that the revision fell to a negative number cannot be that surprising. But it certainly got tongues wagging! FWIW, I continue to believe that the process is where the flaws lie and that the BLS workers are trying to do their job in the best way they can. In the end, though, much more attention will be paid to this morning’s CPI than to yesterday’s PPI.

For Jay and his friends at the Fed

His confidence ‘flation is dead

Is missing in action

Henceforth the attraction

That higher for longer’s ahead

Which brings us to Chairman Powell and his comments at the Foreign Bankers’ Association in Amsterdam yesterday. In essence, he didn’t change a single thing regarding his views expressed at the last FOMC meeting, explaining he still lacked confidence that inflation would be reaching their 2.0% target soon. As such, there is no reason to believe that the Fed is going to cut rates anytime soon. As of this morning, the Fed funds futures market has a 9% probability of a rate cut priced for June, up from 3% yesterday, and a total of 45bps of cuts priced for the year. There is obviously still a strong belief that the Fed will be able to act, although I am not sure why that is the case. Interestingly, on the same panel, Dutch Central Bank president Klaas Knot essentially guaranteed an ECB cut in June. As well, yesterday morning we heard Huw Pill, the chief economist at the BOE also talk up the probability of a June cut. From a market response perspective, though, given these cuts are largely assumed, it will take new information to drive any substantive movement in the FX markets.

Here’s one thing to consider for everyone pining for that rate cut. Given the history of the Fed always being behind the curve when it comes to policy shifts, if they realize they need to cut it is probably an indication that things in the US economy have turned down rather rapidly. We may not want to see that either. Just sayin!

In China, a new idea’s floated

Though not yet officially quoted

In thinking, quite bold

All houses, unsold,

Will soon be, for homeless, devoted

Ok, let’s move on from yesterday to the overnight session and then this morning’s CPI and Retail Sales reports. The first thing to note was the story from Beijing that in an effort to deal with the ongoing property crisis in China, the government, via regional special funding vehicles that borrow more money, is considering buying all the unsold homes from developers, at a steep discount, and then converting them into low-cost affordable housing. In truth, I think this is an inspired idea on one level, as it would allocate a wasted resource to a better use. On the other hand, the idea that the government would issue yet more debt seems like a potential future problem will grow larger. As of now, this is not official policy, but the leak was clearly designed as a trial balloon to gauge the market’s response. Not surprisingly, the response was that the Shanghai property index rose sharply, but the rest of the Chinese share complex was in the red. At the same time, the PBOC left rates on hold last night, as expected, but the CNY (+0.3%) managed to rally nicely on the combination of events.

But away from that China story, very little of note happened as all eyes await the CPI later this morning. After yesterday’s somewhat surprising rally in the US, Asia beyond China had a mixed performance with some gainers (Australia, Taiwan, South Korea) and some laggards (Hong Kong, New Zealand, Singapore) as investors adjusted positions ahead of the big report. In Europe, too, the picture is mixed although there are far more gainers than laggards. In the end, none of the movement is that large overall, so also indicative of waiting for the data. Finally, it will be no surprise that US futures are basically flat at this hour (6:30).

In the bond market, traders decided that the hot April number was to be ignored and instead have accepted the idea that inflation is not really that hot after all. At least that is what we might glean from the price action yesterday and overnight where yields initially jumped a few basis points before grinding down over the session and closing lower by 4bps. This morning, that decline has continued with a further 2bp drop in Treasuries. In Europe this morning, sovereign yields are seeming to catch up to the Treasury price action with declines across the board of between 6bps and 8bps. Part of that is also a result of changing expectations for Eurozone growth and inflation with a growing belief that inflation is headed lower and the ECB is set to cut and continue to do so going forward.

In the commodity markets, the big story has been copper (+2.4%), which has rallied parabolically and is currently above $5.00/lb, a new all-time high. This takes the movement this week to more than 10% and more than 36% in the past year. The electrification story is gaining traction again, and I guess the fact that nobody is digging new mines may finally be dawning on traders. Precious metals are coming along for the ride with gold rebounding (+0.4%) on this story as well as the dollar’s recent weakness. As to the oil market, it is little changed this morning in the middle of its recent trading range. Perhaps today’s EIA inventory data will drive some movement.

Finally, the dollar is under modest pressure this morning after slipping a bit during yesterday’s session as well. The combination of the Powell comments being seen as dovish and the interpretation of the PPI data in the same manner (which seems harder for me to understand) weighed on the greenback against virtually all its counterparts. It should be no surprise that CLP (+0.9%) is the biggest winner given the move in copper. But JPY (+0.5%) has also performed well with no new obvious catalysts. In fact, the movement has been quite broad with the worst performers merely remaining unchanged vs. the dollar rather than gaining. However, this morning’s data is going to be critical to the near-term views, so we need to wait and see.

As to the data, here are the current forecasts: CPI (0.4% M/M, 3.4% Y/Y), core CPI (0.3% M/M, 3.6% Y/Y), Retail Sales (0.4%, 0.2% ex autos) and Empire State Manufacturing (-10.0). In addition, we hear from two Fed speakers, Minneapolis Fed president Kashkari and Governor Bowman. However, on the Fed speaker part, especially since Powell just reinforced his post-FOMC press conference message, it seems hard to believe that there will be any changes of note.

And that’s all she wrote (well he). A hot print will likely be met with an initial risk-off take with both equity and bond markets suffering, but I suspect that it will need to be really, really bad to change the current narrative. However, a cool print seems likely to result in a major rally in both stocks and bonds and a much sharper sell-off in the dollar.

Good luck

adf