With central bank meetings ahead

Tonight BOJ, then the Fed

The discourse today’s

On German malaise

And why vs. the PIGS its widespread

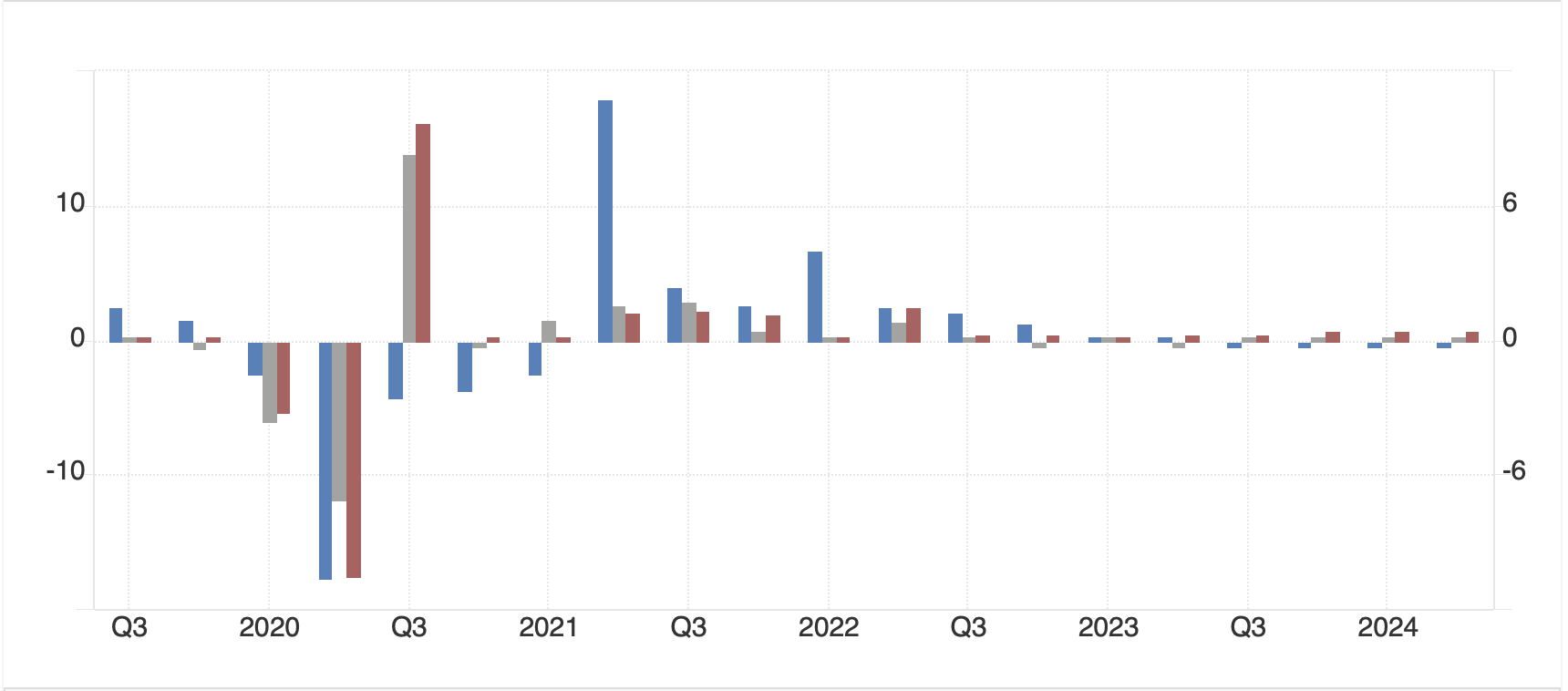

As investors await the news from Ueda-san tonight and Chairman Powell tomorrow, the market discussion has revolved around the potential problems that Madame Lagarde is going to have going forward given the split in economic outcomes within the Eurozone. As can be seen in the below graph, German GDP growth (grey bars) has been running at a negative rate for the past 4 quarters. But you can also see that the situation in both Spain (red bars) and Italy (blue bars) has been the opposite, with both of those nations maintaining a steady pace of growth.

Source: tradingeconomics.com

So, while Germany is the largest single economy within the Eurozone, its current trajectory is very different than much of the rest of the bloc, ironically specifically the PIGS. Should the ECB ignore German weakness and manage monetary policy toward the overall group? Or should they ease more aggressively in order to support the Germans while risking a rebound in still sticky inflation?

Perhaps the first thing to answer is why Germany has been suffering for so long. This is an easy question to answer. Germany’s energy policy, Energiewende, has been an unmitigated disaster. Their efforts to address climate change have led to the highest energy costs in Europe which, not surprisingly, has resulted in a massive reduction in manufacturing activity. Areas where Germany had been supreme, like chemicals and autos, are hugely energy intensive industries, so as their cost of production rose, the companies moved their activities elsewhere. Adding to the insanity was the policy to shutter their nuclear fleet, which had produced 10% of the nation’s electricity, during the post Ukraine invasion energy crisis. And ultimately, this is the problem. The cost of money is not Germany’s economic problem, it is their policies which have undermined their own growth ability. While the ECB cannot ignore Germany outright, there is nothing they can do that will help the nation rebound in any meaningful way. With that in mind, I would contend Lagarde needs to focus on the rest of the bloc to make sure policy suits them. But that is a political discussion.

What are the likely impacts of this situation? Eurozone growth, overall, surprised on the high side despite the lagging German data. As well, inflation readings released thus far this month have shown that prices remain sticky on the continent. With that in mind, the idea the ECB needs to cut aggressively seems to make little sense. This is not to say they will maintain tighter policy, just that it doesn’t seem justified to ease. But right now, the market zeitgeist is all about easing monetary policy (except in Japan) so I expect they will do just that going forward. With this in mind, it strikes that the euro (+0.15%) is going to struggle to rally from current levels absent a dramatic shift in Fed policy to aggressive rate cuts. As to European bourses, I suspect that they will reflect each nations’ own circumstances, so the DAX seems likely to lag going forward.

Will he, or won’t he?

Though inflation’s been falling

Hiking pressure’s real

A quick thought regarding tonight’s BOJ meeting and whether Ueda-san believes that further rate hikes are appropriate for the Japanese economy. As with many things Japanese, the proper move is not necessarily the obvious one. A dispassionate view of the recent data trends shows that inflation (2.8%) has been sliding slowly, GDP growth (-0.5%) has been falling more quickly and Unemployment (2.5%) remains at levels consistent with the economy’s situation given the shrinking population. On the surface, this does not seem like a situation where hiking is desperately needed except for one thing, the yen remains broadly weak. The chart below shows that since the advent of Abenomics in 2011, the yen has lost 50% of its value.

Source: tradingeconomics.com

Now, initially, that was a key plank of the Abenomics platform, weakening the yen to end deflation. Well, kudos to them, 13 years later they have achieved that result. But where do they go from here? There is a growing belief that the BOJ is going to hike by 15bps tonight and bring their base rate up to 0.25%. I disagree with this theory given the very clear recent direction of travel in the inflation data in Japan as despite the yen’s weakness, it dispels any notion that a rate hike is needed to push things along. One positive of the weak yen is that the balance of trade has returned to surplus in Japan.

Source: tradingeconomics.com

For decades, Japan ran a large positive trade balance but since the GFC, that situation has been far less consistent. However, the trade balance remains an important domestic signal as to the strength of the economy and its recent return to surplus is welcomed by the Kishida government. It is not clear how raising interest rates will help that situation. Net, with inflation sliding and the economy under pressure, hiking interest rates does not make any sense to me.

Ok, let’s take a look at how markets have behaved overnight. Yesterday’s lackluster US equity market performance was followed by very modest strength in Japan (+0.15%), although weakness throughout the rest of Asia with the Hang Seng (-1.4%) the laggard, although mainland Chinese (-0.6%) and Australian (-0.5%) shares also suffered. Meanwhile, in Europe this morning bourses on the continent are higher by about 0.4% across the board after the Eurozone GDP data seemed to encourage optimism. The UK (FTSE 100 -0.2%), however, is under a bit of pressure amid ongoing discussions in the new Labour government about the need for austerity. At this hour (7:20) US futures are edging higher by about 0.25%.

In the bond market, after yesterday’s sharp decline in yields around the world, it has been far less exciting with Treasury yields edging down another basis point and European sovereigns either unchanged or 1bp lower. Perhaps the most interesting things is that JGB yields fell 2bps overnight and the 10yr yield is now back below 1.00%. That doesn’t seem like a market preparing for a rate hike there.

In the commodity space, everybody still hates commodities with oil (-0.5%) continuing its recent slide. In fact, it is down nearly 10% in the past month (which is good for us as we refill our gas tanks). In the metals markets, copper continues to slide, down another -1.5% this morning as optimism over economic and manufacturing activity around the world remains absent, especially in China. For instance, the Politburo there met yesterday and pledged to help the domestic economy, although they did not lay out specific actions they would take. Recall last week’s Third Plenum was also a disappointment, so until the market perceives China is back and growing rapidly, or that the global growth impulse without them is picking up, it seems that industrial metals will remain under pressure. Gold (+0.4%) however, remains reasonably well bid as continued Asian central bank buying along with retail interest in Asia props up the price.

Finally, the dollar is generally under modest pressure although the outlier is the yen (-0.6%) which does not appear to be expecting a BOJ hike tonight. But elsewhere, the movements in both the G10 and EMG blocs have been pretty limited overall, on the order of 0.15% – 0.35%. It is hard to find an interesting story about any particular currency as a driver today.

On the data front, this morning brings the Case-Shiller Home Price Index (exp +6.7%), JOLTs Job Openings (8.0M) and the Consumer Confidence Index (99.7). I keep looking at that Case-Shiller index and wondering when the housing portion of the inflation readings is going to decline given its consistent strength. But really, I suspect that all eyes will be on Microsoft’s earnings this afternoon along with the other hundred plus names that are reporting today. With the Fed coming tomorrow, macro is not important right now. So, more lackluster trading seems the most likely outcome today, although with the opportunity for some fireworks starting around midnight when the BOJ statement comes out.

Good luck

Adf