So, once again, we were misled

By all those who told us, with dread,

The ratings reduction

Would cause much destruction

With both stocks and bonds, money, dead

Instead, what we saw yesterday

Was traders jumped into the fray

Despite all the gloom

It seems there’s still room

Where bullish investors hold sway

I know it is hard to believe, but it seems that all the angst that was fomented over the weekend following Moody’s ratings downgrade of US Treasury debt was for naught. In fact, the decline in both stocks and bonds didn’t even last one session, let alone weeks or months as both markets closed the session essentially unchanged on the day, recouping the early losses seen. A quick look at the chart below shows the price action in S&P 500 futures from the time of the announcement through yesterday’s close and then this morning. It seems the market is concerned about things other than the US credit rating.

Source: tradingeconomics.com

In fact, I am willing to say that we are unlikely to hear anything more about the downgrade until such time that equity prices fall on some other catalyst, and the punditry will add in the ratings story to help bolster whatever claim they are making at that time. Please remember, as well, that I am quite concerned that equity valuations remain rich and that a decline is quite possible, if not likely. It’s just that the ratings downgrade story is not going to be the driver of that move.

In Japan, it seems

No one’s buying JGBs

Has bug met windshield?

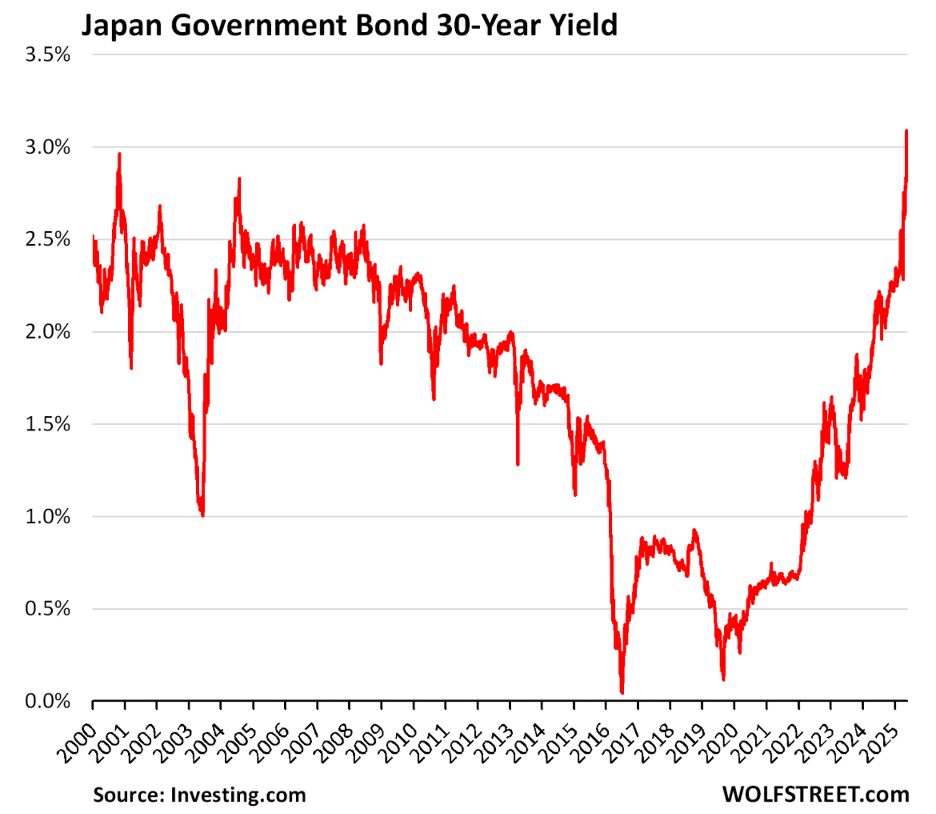

Last night, Japan auctioned 20-year JGBs with the yield coming at 2.52%, the highest since these bonds were first issued back in 1999. As well, yields in 30-year and 40-year JGBs also soared, rising 12bps in each case to the highest yield in more than 25 years as per the below chart of the 30-year bond.

While the selloff in JGBs has been accelerating, real yields there are still negative with CPI running at 3.6%. This presents quite a conundrum for Japanese investors as despite the negative real yield, the ability to borrow cheaply (remember short term rates in Japan are 0.50%) and invest in long-dated bonds and earn 3.0% is quite tempting. 250 basis points of carry with no currency risk is now going to compete with 450 basis points of carry (US 30-year yields of ~5.0% – 0.50% funding costs in Japan) with FX risk.

What makes this especially tricky for Japanese investors is that the dollar’s future path, which had been clearly higher for longer, appears to have adjusted. It seems evident the Trump administration is keen to see the dollar decline, or perhaps more accurately, see other currencies appreciate, especially if those nations run significant trade surpluses with the US. Japan certainly fits that bill. And the thing about currency risk is that FX can move swiftly enough to wipe out any carry benefits before institutional investors can even organize meetings to determine if they want to change their strategy.

One of the things that we have heard regularly for the past several years (decades?) is that the US fiscal situation has put the nation in a precarious position, relying on investment by foreigners to fund the massive budget deficits that the government has been running. The problem with these warnings is they have been ongoing for so long, nobody really pays them any attention. It is not to say the theory is incorrect, just that there have been other things that have offset that factor and attracted capital to the US anyway. It is also not apparent that Moody’s ratings cut has changed that dynamic.

But, if at the margin, Japanese investors start to focus more on the JGB market to reduce currency risk, rather than on the highest yield available in major nations, that would likely have a negative impact on the Treasury market. That is, of course, a big IF and there is no evidence yet that is the situation. It is something, though, we must watch closely.

Remember, too, global debt/GDP is more than 300% across all types of debt, public and private. That tells me it will never be repaid, only rolled over. The question is at what point will investors decide that holding debt is too great a risk at current yields? While I assure you governments around the world will work hard to prevent that outcome, including changing regulations to force purchases, it is not clear how much higher that ratio can go without more seriously negative consequences. We will need to watch this closely.

With that in mind, let’s turn to markets and see how things have behaved in the wake of the reversal in US markets yesterday. Asian equities were mixed with Japan essentially unchanged, China (+0.5%) and Hong Kong (+1.5%) showing the best performance in the region while India (-1.0%) was the laggard. Otherwise, there were both gainers and losers of limited note. In Europe, though, equity markets are rallying across the board led by Spain’s IBEX (+1.6%) despite another infrastructure disaster where half the nation lost telecoms for several hours as Telefonica (Spain’s major telecom company) messed up a systems upgrade. The rest of the continent has seen shares rise on the order of 0.4% to 0.5% as ECB comments seem to be encouraging the idea of another rate cut coming soon and European Current Account data showed a greater surplus than expected. US futures, though, are ever so slightly lower at this hour (7:15), down about -0.1% across the board.

In the bond market, in the 10-year space, yields are within 1bp of yesterday’s closing for Treasuries (+1bp), European sovereigns (-1bp) and JGBs (+1bp). It seems that despite all the talk of the end of times, investors haven’t given up yet, at least not in the 10yr space. However, the evidence is growing that fixed income investors are growing leery of tenors longer than that.

In the commodity markets, oil (-0.6%) is slightly softer but remains well within its recent trading range amid the slightest of downtrends. In truth, I find this chart to be an excellent description of my feelings of this market, a really slow decline over time.

Source: tradingeconomics.com

As to the metals markets, gold (+0.6%) is continuing its rebound from the worst levels seen last Thursday and is currently more than $100/oz higher than those recent lows. This has helped silver (+0.5%) as well although copper (-0.5%) is not playing along today.

Finally, the dollar, remarkably, did not collapse in the wake of the Moody’s downgrade. In fact, similar to the price action in both stocks and bonds yesterday, the dollar retraced much of its early losses. This morning, it remains on the soft side, but movement is much less pronounced across both the G10 and EMG blocs. However, the worst performer today is AUD (-0.7%) which some may attribute to the fact that the RBA cut their base rate by 25bps last night (although that was widely expected). But I would point to the law that was recently enacted by the Albanese government in Australia to begin taxing UNREALIZED capital gains. This idea has been floated by other governments but never actually enacted. I fear that the consequences for Australia will be dire as it becomes clear the policy is extraordinarily destructive. Capital will flee and that bodes ill for the currency. If they truly follow through with this, be very careful.

There is no data today, but we hear from six different Fed speakers as they are all participating in an Atlanta Fed symposium. However, I do not expect anything other than patience is the watchword as they observe the Trump administration policies unfold.

In the end, the predicted doom did not come to pass. However, for my money, I would pay closest attention to Australia. I fear the negative consequences of this policy will be extreme.

Good luck

Adf