The White House said seventy nations

Are seeking to have conversations

With President Trump

Avoiding the thump

That comes amid tariff’s predations

But China is not on the list

As Xi claims that he’ll raise his fist

To “fight to the end”

And try to defend

His nation from being dismissed

Last week, risk was anathema to one and all. President Trump’s tariffs were upending the world economy, recession was coming to the US, and possibly the world. I couldn’t help but be reminded of this classic on the potential outcomes.

Leading up to the tariff announcements, nations around the world were puffing out their metaphorical chests and claiming all the things they would do to respond. But the reality is that as I have repeatedly said, the US is the consumer of last resort, and most nations cannot afford to lose access without significantly damaging their own economies. As such, it is not that surprising that such a long list of nations has reached out immediately, indicating a willingness to change their own policies in order to prevent these tariffs. Arguably, China is the one outlier here, with President Xi claiming they will “fight to the end” in this trade war.

Already, a number of nations have promised to reduce their tariffs on US goods to 0.0% if that is what is required, although thus far, the President has not accepted those deals. It is a fair question to ask what he is seeking, since apparently, it is not simply free access. Granted, there are also numerous non-tariff barriers that are in play, and perhaps he is focused on those as well. Or perhaps he really is looking at tariffs as a key revenue source and doesn’t want to give up that revenue opportunity. Or perhaps he is simply waiting for enough nations to bend the knee before one large announcement when all these deals are accepted. The latter idea would be in keeping with the idea that he is trying to isolate China.

These are just three possibilities of the many, and nobody other than President Trump himself knows how this will end up. I find it encouraging that Treasury Secretary Bessent is leading the discussions with Japan, a key ally and trade partner, as I have great faith in his understanding and abilities. However, in the end, it is the President’s decision so…who knows?

Of course, the end of last week brought mayhem to risk markets with equities around the world falling sharply in price. While there had been numerous voices explaining that equity valuations in the US were far too high and unsustainable, many of those same voices were screaming the loudest at the repricing. But, as I said yesterday, markets have a great deal of trouble trading in that manner for too long as traders and investors simply get tired and stop trading at all.

But what was interesting was that US markets turned around after the incredibly weak opening in futures markets Sunday night, and closed mixed on the day, with the NASDAQ actually managing a tiny gain. I’m not sure exactly what to ascribe as the cause of that reversal, maybe bargain hunters, maybe short covering, or maybe much of the forced selling from margin calls had been completed. In the morning, there was a rumor that Trump would delay the imposition of tariffs by 90 days, but that was squelched very quickly. You can see that price action on the chart below.

Source: tradingeconomics.com

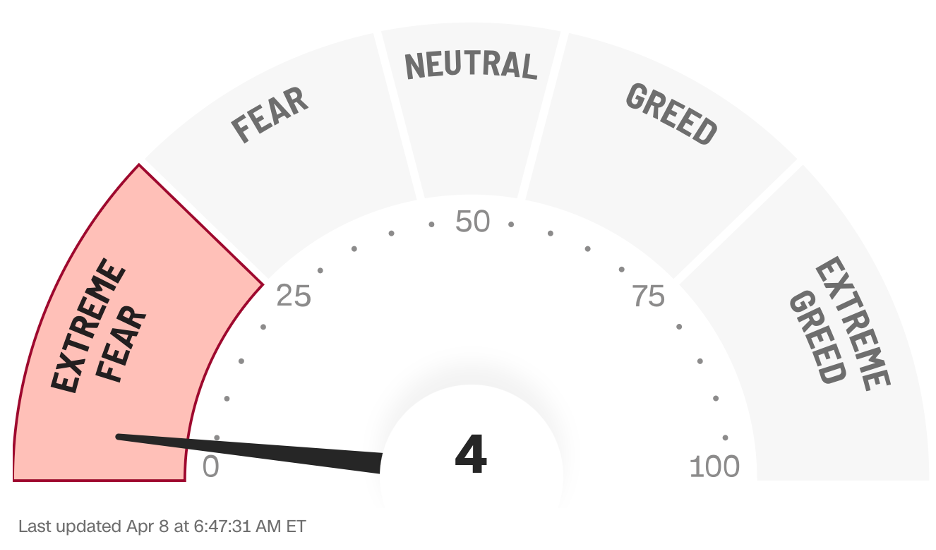

The bounce, though, is continuing and we saw substantial rebounds overnight throughout Asia as well as in Europe this morning and with US futures pointing higher as well. As much fear as was felt on Friday, it seems just the opposite today. Interestingly, the Fear & Greed Index is still sitting at its all-time lows of just 4 as of this morning. Perhaps that is the indicator driving the buying.

Source: cnn.com

To recap, many nations are offering to change their tariff policies with the US, although none of those offers have yet been accepted. Tariffs are due to be enacted starting tomorrow, and there is still a great deal of concern around, but equity markets worldwide are rebounding from their worst levels. For anyone who thought markets made sense, I dare you to put this puzzle together!

But let’s see how big the bounces were. Tokyo (+6.0%) exploded higher, recouping much of Friday’s losses, although still down net since this began. Surprisingly, China (+1.7%) and Hong Kong (+1.5%) showed much less bounce, although they didn’t fall as sharply either. However, I have to assume that President Xi cannot be very happy as the Chinese plunge protection team was active last night, buying more than $5.7 billion in ETF’s to support the market and there was verbal support as well from the government. Too, the yuan is sliding more aggressively but we will cover that below. As to the rest of Asia, the picture was mixed with Taiwan, Vietnam, Thailand and Singapore falling sharply while India, Australia and New Zealand all had nice bounces.

In Europe, there is a rebound as well, albeit not so dramatic with the FTSE 100 (+1.9%) leading the way and the DAX (+1.4%) and CAC (+1.3%) having solid sessions. One of the offers was from the EU, saying they will take the tariffs on manufactured goods to 0.0% if the US would reciprocate, although that offer was not accepted, at least not yet. US futures are all firmer this morning, up between 1.25% and 2.0% at this hour (7:15). I think the message here is that nobody really knows anything else yet, and short-term trading is the driver.

In the bond market, there was a massive reversal yesterday with Treasury yields spiking more than 30bps from bottom to top during the session and closing near the highs. (see below)

Source: tradingeconomics.com

We saw similar price action throughout European sovereigns as well, although the rise was not quite as dramatic, a bit more than 20bps in German bunds although 30bps in UK gilts. This morning, however, after all that price movement, yields are within 1bp of yesterday’s closing levels as traders and investors try to figure out what to do next. JGB yields did rally 16bps yesterday, which given their level, was commensurate with the Treasury movement. Arguably, looking at the chart above, what we have seen is a reset to pre-tariff levels.

In the commodity markets, oil (+0.25%) managed to close above $60/bbl, although the trend there remains lower in my eyes. I have had a bearish overall view on oil for more than a year as I explained back in January 2024 that there was plenty of oil around, and it was political decisions that was restricting its availability, not physical ones. As such, it is no surprise to me that the trend here is lower, especially with President Trump’s energy policy to drill, baby, drill, and OPEC increasing production as well. It is hard to get excited about major price rises here. Meanwhile, gold (+1.0%) and silver (+1.0%) are rebounding, with gold back above the $3000/oz level after its short profit taking foray below that key psychological level. Copper is still under pressure as the growth story remains uncertain, at best, for now.

Finally, the dollar is a bit softer this morning, but with some notable exceptions. While G7 currencies are all firmer, ranging from NZD (+1.1%) down to NOK (+0.1%) and everything in between, in the EMG bloc, CNY (-0.25%) is back to the weakest levels (dollar strength) since early January and prior to that since September 2023.

Source: tradingeconomics.com

Xi is now caught in a tough spot as given the US tariffs, which total to about 104% on Chinese imports, the natural response is to allow the yuan to depreciate. However, he has made a big deal about the yuan being a stable store of value, so if he lets it slide, that will undermine that argument. My money is on a weaker CNY going forward. Elsewhere in Asia, KRW (-0.6%) and INR (-0.4%) led the way lower.

On the data front, the NFIB Small Business Optimism Index was released at a softer than expected 97.4 this morning, but there is nothing else on the calendar other than an afternoon speech by SF Fed president Daly.

It cannot be a surprise that we had a rebound from last week’s dramatic declines. The question, of course, is have we now seen the bottom. My take is that is not the case, and while we may hold tight for a few sessions, further declines are still in the offing. At least absent a major change where Mr Trump announces that he has accepted the reduction in tariffs elsewhere around the world. Remember, even after the declines, US equities are still richly valued. As to the dollar, that is a much harder question, and I sense that there will be much more idiosyncratic movement rather than bloc dollar movement going forward.

Good luck

Adf