The world is no longer the same

So, now everyone must reframe

Their views on positions

And whether conditions

Allow them to still play the game

Most markets have priced fatter tails

With stock markets seeing net sales

But oil and gold

Seem likely to hold

Their gains across longer timescales

Here we are on Monday morning in a very different world than we left on Friday evening. While there was much talk about whether a peace would be reached then, obviously that never happened. Of course, at this point, there is no other story than the ongoing military action in Iran and the Middle East. As this is not a news commentary, but a financial markets one, that is all I will discuss here.

Not surprisingly, we have seen some large moves across markets, and largely in the direction one would have expected regarding risk. So, oil prices (+7.5%) have exploded higher as shipping through the Strait of Hormuz has ceased for now and there is no timeline for it to reopen. Given ~20% of the daily global consumption of oil flows through that waterway, there should be no surprise here. You can see from the chart below that as concerns grew regarding military action, oil’s price climbed and then, of course, gapped on the opening last night.

Source: tradingeconomics.com

Perhaps a bit more surprising to me is that Brent Crude (+7.5%) has moved virtually the exact same amount as WTI. I only say that because Brent is the price basis for global oil outside the US which is obviously going to be more impacted than the US markets. But the Brent chart is virtually identical to the WTI above. As to the future, clearly, no market is more dependent on the Middle East conflict than this one, but at this point, there is no indication it is going to end very soon, so I expect prices to remain at least at current levels for now, and if the conflict starts to target oil production facilities, we could go quite a bit higher.

While we are looking at commodities, it should also be no surprise that gold (+2.1%) is higher this morning as it performs its historical role as a safe haven. While not quite as extreme as the oil chart, the similarities between the two, as you can see below, are significant. Of course, it was a bit more than a month ago when we had that dramatic sell-off in the precious metals, so this has all been a recovery from there. But a grind higher punctuated with a gap last night is the gold story as well.

Source: tradingeconomics.com

Arguably, gold will have more staying power than oil as when the conflict ends, and my initial take is it will not be a forever war, oil will once again flow more freely. Gold, however, remains a haven in an uncertain world and nothing seems likely to reduce uncertainty anytime soon.

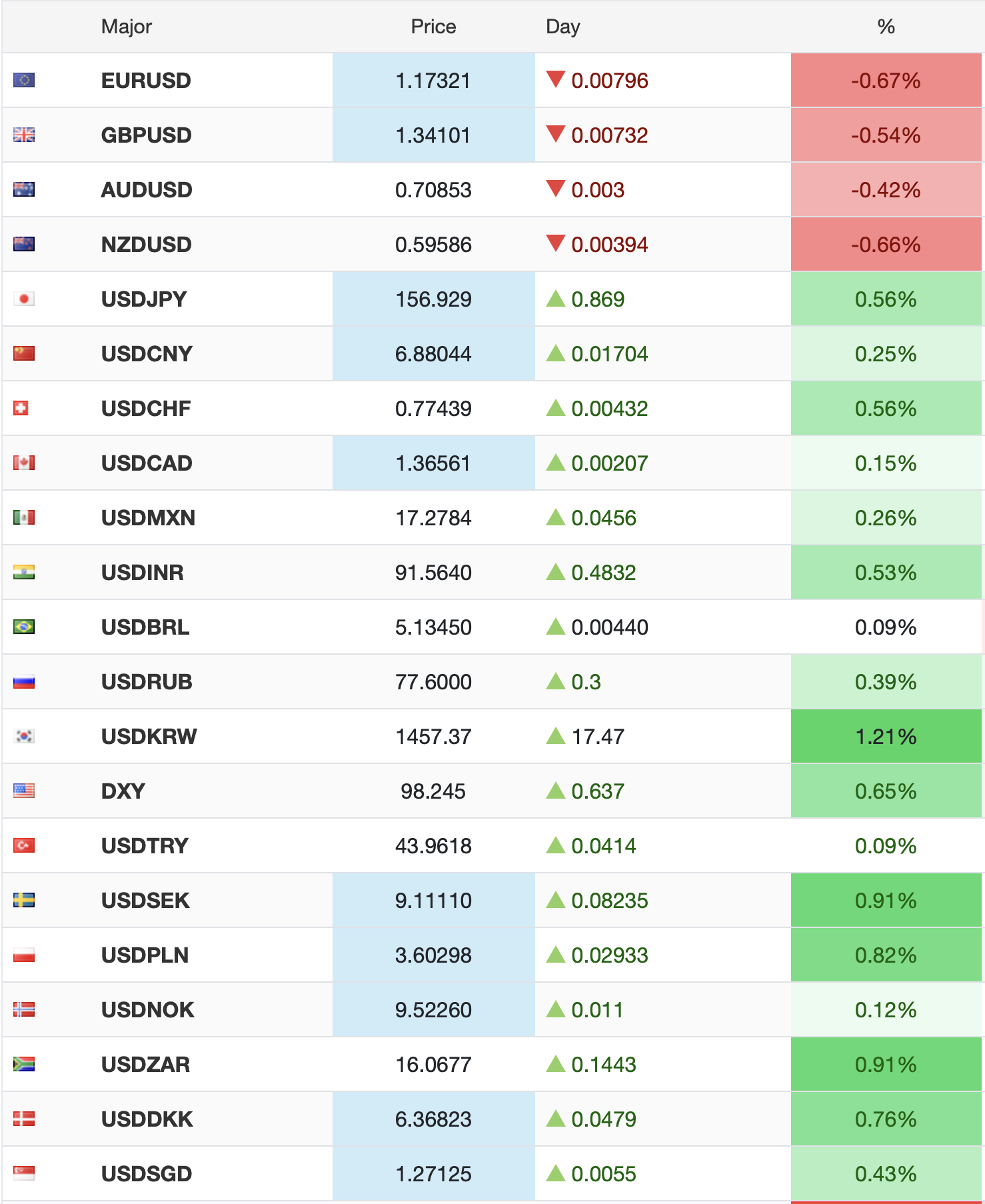

The other two traditional haven assets are the dollar and Treasury bonds so let’s look at them next. Starting with the dollar, it has done what it regularly does in an uncertain situation, it has rallied sharply. As you can see from the below table, shot at 6:39 this morning, the dollar is firmer against every single major currency this morning.

Source: tradingeconomics.com

Too, using the euro as our proxy for the dollar writ large, you can see that the chart below looks almost identical to that of both gold and oil above. (I have inverted the Y-axis to highlight the similarities.)

Source: tradingeconomics.com

It appears that markets began pricing in this event back in the middle of February, although the real move required the onset of the military action.

As to the last haven asset, US Treasuries, they are not really doing the job today. Yields there have edged higher by 2bps this morning and we are seeing similar price action across the entire European sovereign space. The two exceptions today are UK Gilts (+8bps), which seem to be trading on concerns the BOE is less likely to cut rates as higher oil prices will prevent inflation from continuing lower and JGBs (-4bps) which are serving their haven role well, arguably given the distance from the action and the fact that with yields above 2%, investors seeking safety feel they have some cushion.

Source: tradingeconomics.com

The treasury move was interesting as the initial trade, at last night’s opening, was for lower yields as per the chart above, but that has since reversed. It could be investors are concerned over additional defense spending blowing out the deficit further but there is no clear signal or commentary I have seen yet on the subject.

Finally, it should not be surprising that equity markets around the world are mostly lower this morning as investors pull in their wings and await more clarity on the outcome and how long this will continue. The exception to this was mainland China (+0.4%) which managed to edge higher, but otherwise, all of Asia and Europe are down on the day, some pretty substantially. Below you can see a screenshot of futures markets at 7:00 with the type of movements ongoing.

Source: tradingeconomics.com

The MOEX is Russia’s stock market, so it is not clear what value that adds to the conversation and the TSX, Toronto, does not have a futures market, so the price represents Friday’s close. But as you can see, all of Europe and all of Asia ex-China have fallen sharply.

And that’s where we sit this morning. Ironically, there is going to be a significant amount of data released this week, including the NFP report on Friday, but it is not clear market participants will be paying close attention. For good orders’ sake, I will list the data releases anyway.

| Today | ISM Manufacturing | 51.8 |

| ISM Manufacturing Prices | 59.5 | |

| Wednesday | ADP Employment | 45K |

| ISM Services | 54.0 | |

| Thursday | Initial Claims | 216K |

| Continuing Claims | 1840K | |

| Nonfarm Productivity Q4 | 4.8% | |

| Unit Labor Costs Q4 | 0.2% | |

| Friday | Nonfarm Payrolls | 60K |

| Private Payrolls | 65K | |

| Manufacturing Payrolls | 0K | |

| Unemployment Rate | 4.3% | |

| Average Hourly Earnings | 0.3% (3.6% Y/Y) | |

| Average Weekly Hours | 34.3 | |

| Participation Rate | 62.5% | |

| Retail Sales | -0.2% | |

| -ex autos | 0.1% | |

| Consumer Credit | $11.8B |

Source: tradingeconomics.com

To me, market dynamics now are entirely restricted to the ongoing Middle East conflagration. Ultimately, war is inflationary, and for many firms it is quite profitable. But right now, investors are mostly hiding under their desks, waiting for the smoke to clear. Institutional investors are typically unwilling to buck a key narrative trend, and I see no reason to believe this time will be different.

While much of this price movement will likely reverse when the bombing stops, until then, be prepared for more volatility, not less.

Good luck

Adf