Though I’ve been away near a week

From what I read things are still bleak

Two months have gone by

Since stocks touched the sky

And traders all want a new peak

Meanwhile, GDP fell ‘neath nought

And lots see the future as fraught

The popular claim

Is Trump is to blame

And rue all the things he has wrought

I worked hard not to pay close attention to markets while I was away last week in an effort to get some true relaxation. And now that I’m back at my desk, I can see that I didn’t miss anything at all. The narratives remain the same, the split between those who believe everything the president says/does is a disaster and those who believe everything he says/does is brilliant has not changed at all. In other words, life continues as do all the arguments.

A review of the data last week showed two key outcomes, the labor market remains far more resilient than the recessionistas will accept and jobs continue to be created. For some reason, that seems like good news to me, but then I am not a highly paid economist with a narrative to stoke. On the other hand, Q1 GDP printed at -0.3%, the first negative print in 3 years, but also one that is easily explained by the rush of imports that occurred prior to the imposition of tariffs in early April. Remember, imports subtract from Gross DomesticProduct. However, a look under the hood of this number shows that the positive news was government activity declined while private sector investment exploded higher. It strikes me that this is the best possible direction for the US economy going forward.

In China, it seems Xi’s decided

That data has been too one-sided

So, henceforth they’ll furnish

Just data to burnish

The views Xi and friends have provided

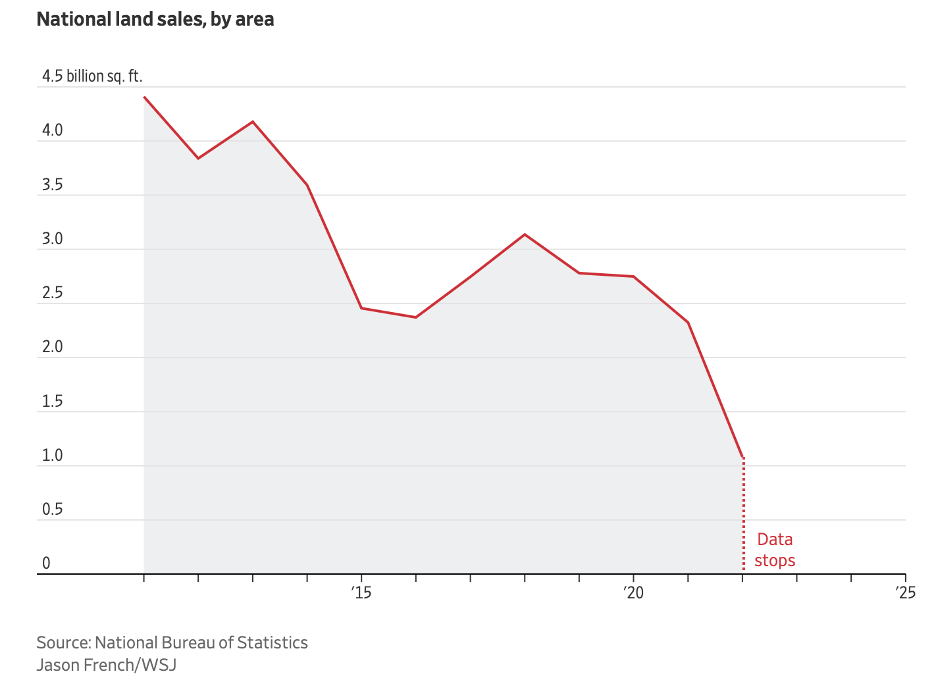

Turning to the more recent stories, though, the WSJ had a very interesting take on the fact that China’s statistical output is shrinking quite rapidly as data that has been trending lower suddenly stops being produced. The below chart from the article on National Land Sales is an excellent depiction of things, and likely an indication that land sales, which are critical to local government finances, have become even a bigger problem over the past three years than when the property market first started melting down in early 2021.

It is worth noting that in this trade war between the US and China, while much of the punditry continues to insist that China has the upper hand as the stuff they sell to the US is more critical and less replaceable than the stuff the US sells to them, I have maintained things are not necessarily that easy. The US is facing a supply shock, and will need time to work it through, but the US economy is the most dynamic in the world, and these issues will be resolved. China faces a demand shock, which in economic theory should be easier to address, but which in China’s reality has not proven to be the case. Consider that Xi and the CCP have been creating fiscal stimulus plans since Covid without any serious success. In fact, the Chinese have openly stated that they are seeking to shift the production/consumption mix of the nation closer to Western standards of 60%-70% consumption from their current 45%-50% level. It hasn’t worked yet, and I see no reason to believe that is going to change. We must never forget the US is the consumer of last resort, and if China doesn’t have access to this market, it is a major problem for them.

I have no inside knowledge of how things are evolving on this issue, but here’s my take; while Xi doesn’t need to worry about being elected, he still needs to ensure that China’s economy grows sufficiently to increase the well-being of his population. Whatever the official statistics have shown, it is clear that things in China are not what they would have the rest of the world believe and that is a problem for Xi. Meanwhile, Trump will not face another election and was elected with a pretty broad mandate. I believe given the timing of the mid-term elections, he has another 9-12 months to get things done and will play hardball with China to do so. In fact, I have a feeling that Trump may have the upper hand. This will be settled by the autumn is my view.

Ok, let’s turn to markets and what happened in the overnight session. Looking first at currencies for a change, I couldn’t help but notice the following chart.

Source: tradingeconomics.com

I also couldn’t help but notice the following comment from the Taiwanese central bank in response to a question about whether the FX rate is on the table in the trade negotiations. (As an aside, @PIQSuite is an excellent follow on X. Key market headlines on a real-time basis with other things available as well.)

The question of whether FX rates would be part of the trade talks seems to have been answered, and the answer is yes. Perhaps there will not need to be a Mar-a-Lago accord after all regarding revaluing gold and terming out bonds. Instead, the pressures will be relieved on a country-by-country basis with each trade deal.

While the TWD revaluation of 10% over the past 2 sessions is the most dramatic, the dollar is generally lower this morning against both G10 and EMG currencies. In the G10, AUD (+0.85%) leads the way but JPY (+0.7%), NOK (+0.6%) and CHF (+0.5%) are all pushing higher. This must be music to President Trump’s ears. As to the emerging markets, KRW (+2.5%), is the next biggest mover although they admitted that FX rates were part of the trade discussions. SGD (+0.8%) has also seen a relatively large move and INR (+0.4%) is moving in that direction. It seems clear that Asia is the focus of both the administration and the markets this morning. The rest of the EMG bloc has seen much smaller gains, between +0.25% and +0.5%, with CNY (+0.15%) really doing very little.

Turning to the equity markets, last week clearly finished on a strong note and, in fact, since I last wrote, the S&P 500 has rallied a bit more than 2% and is higher by more than 14% since April 8th. Apparently, the world has not yet ended, but there hasn’t been a new high in the stock market in more than 3 months, and people are edgy! As to the overnight session, the Nikkei (+1.0%) rallied along with the Hang Seng (+1.75%) although Mainland shares (CSI 300 -0.1%) showed little life. Elsewhere in the region, Taiwan (-1.25%) and Australia (-1.0%) felt the most pressure and the rest were mixed with much smaller movements. In Europe, indices are mixed as earnings data from each country are the drivers amid a lack of broad-based news. So, the UK (+1.2%) and Germany (+0.6%) are firmer while France (-0.6%) is lagging on the back of some weaker earnings numbers. As to the US, futures are pointing lower by about -0.7% across the board at this hour (7:15).

In the bond market, last week saw Treasury yields jump sharply after the better-than-expected payroll report, finishing the day 9bps higher, although still within the middle of the trading range since February and lower on the year. This morning, they are basically unchanged while European sovereign yields have slipped by about -2bps across the board. The picture there continues to focus on the uptick in fiscal spending that is expected and the borrowing that will be needed to pay for it. However, there is still a strong view that the ECB will be cutting rates going forward.

Lastly, in the commodity markets, oil (-1.15%) is sliding again as OPEC+ has promised to continue to increase production. There are two takes on this activity, both of which probably have some truth. First is the idea that President Trump has made a deal with MBS in Saudi Arabia to increase production and drive prices lower. Remember, lower energy prices are a boon to the US (and the world). But added to that is the idea that MBS agreed so he can help force fracking production to pull back and regain market share for OPEC+. However, regardless of the rationale, nothing has changed my view that oil prices are heading lower, and I still like the $50/bbl level as a target. As to the metals, gold (+2.3%) which has been under pressure for several weeks in a correction, seems to have found support below $3300/oz and could well be setting up for another leg higher. This has taken silver (+1.3%) and copper (+.8%) along for the ride. If the dollar is going to continue lower, metals prices should remain quite firm.

On the data front, today only brings ISM Services (exp 50.6), but really, all eyes will be on the FOMC meeting on Wednesday. I will highlight the rest of the week’s data tomorrow morning.

The past month has seen significant volatility in markets as participants did not correctly estimate the potential moves in trade policy. At this point, it seems those questions are being answered, with President Trump even hinting some deals could be finalized this week. I believe we are going to see trade announcements that include new FX goals, and they will be pushing the dollar lower across the board. While I don’t see a collapse coming, that is the trend for now.

Good luck

Adf