The story that has the most traction

Continues to be the reaction

To stories AI

Will force firms to try

To profit from worker subtraction

The tech nerds see naught but potential

For robots plus, workers, essential

But history’s shown

Employment has grown

And new tech’s threat’s not existential

Block, the payments processing company announced during its earnings call that it would be laying off 4000 employees, nearly half its workforce, by the end of Q1 this year. This was not a response to weak performance, but rather the founder, Jack Dorsey’s, belief that AI has reached the point where his company can be more effective with much fewer staff. Of course, this is the entire AI argument compressed into a single event.

Recall Monday’s note and market response to the Citrini Research article that explained one scenario from AI adoption would be massive layoffs, a recession and a major stock market decline by 2028 as companies eliminated people from their processes. This brought about a tremendous amount of back and forth with economists and historians explaining that every major technology creation (e.g. electricity, the automobile, the internet) was both disruptive but instrumental in expanding economic activity. This morning’s WSJ had a nice summation by Greg Ip of the entire discussion.

It strikes me that this discussion is only beginning and we are going to hear from proponents of both sides for many months to come, although I imagine it will not be the top story every day. As I consider the issue, I think back to John Maynard Keynes forecast in 1930 that the rapid advancement of technology would lead to a 15-hour workweek as all our needs could be met with much less effort. Obviously, that was not his best forecast. Rather, Jevon’s Paradox comes to mind, which states that as technology increases the efficiency with which a resource is used, the total consumption of that resource increases, it doesn’t decrease. In this discussion, that resource is human labor.

FWIW, my view is AI is a remarkable tool for certain things but is neither sentient nor capable of breakthroughs on its own. It is a wonderful research tool, and a wonderful computer programming tool, but as my experience taught me, people like to deal with people, not with machines, even when there are machines available to do the job. Economic dislocation in certain areas is likely going forward, but not collapse, at least not because of greater usage of AI tools.

I highlight this because, while Block’s stock price rallied sharply in the aftermarket, up more than 20%, US futures are lower this morning by -0.5% or so as there continue to be fears about the dystopian outcome. Remember, Nvidia had terrific earnings and the stock fell as well. Of course, this could also be a response to the fact that the price of many equities is extremely rich on a P/E basis or a P/S basis, and we are simply seeing a little reversion to the mean.

At any rate, as no war in Iran has begun and there have been no other changes on the geopolitical map, let’s tour markets to see how things look as we head into the weekend and month end.

Yesterday’s desultory equity performance in the US was followed by a mixed picture in Asia with the Nikkei (+0.2%) and Hang Seng (+1.0%) closing the month higher, but China (-0.3%), Korea (-1.0%) and India (-1.2%) all falling. Malaysia (-1.4%), too, stands out for a poor session but the rest of the region was mixed with much smaller moves. Given the tech heavy makeup of most of these nations’ bourses, I suspect that volatility will be the main feature going forward. As to Europe, it’s a sleeper with continental bourses all +/- 0.2% or less while the UK (+0.35%) managed a modest rally after a by-election resulted in PM Starmer’s Labour party coming in 3rd place in a seat they have held for 100 years. This appears to be adding pressure on Starmer to do something, or on Labour to remove him, but a key concern is they will move further left, something which I doubt will help the UK economy or stock market.

Turning to the bond market, yields are declining all around the world with Treasuries slipping -5bps yesterday and another -2bps this morning, now below the 4.00% level. In fact, a look at the chart below shows a pretty strong trend lower in yields.

Source: tradingeconomics.com

But we saw European sovereign yields slide yesterday and continue lower by another -1bp to -2bps this morning and last night, JGB yields fell -4bps and showing a very similar trend to Treasury yields as per the below. It seems that concerns over too much debt issuance driving yields higher have been put on the back burner for now.

Source: tradingeconomics.com

In the commodity space, it appears that Iran fears are making a comeback as oil (+2.1%) has rebounded sharply from the levels seen in the wake of the massive inventory build I described yesterday morning. It sure looks like somebody bought a lot of oil yesterday morning at around 9:45am, although I have no guess as to who it would have been.

Source: tradingeconomics.com

Interestingly, the news from Geneva is that the talks are going to continue next week, so while both sides are disputing the other’s version of things, the fact they are still speaking is a huge positive. I fear given the military buildup, some type of action will occur, but we can be hopeful.

Meanwhile, in the metals space, gold (+0.1%) is little changed for the past several sessions, consolidating just below the $5200/oz level. Whatever the narrative may be here, regarding central bank buying and the end of the dollar system, this tells me that the market is tired and needs some R&R before moving forward. I remain bullish, but not today.

Source: tradingeconmics.com

Silver (+1.7%) is showing very similar price action to gold, albeit with a bit more daily volatility. The story here about a short squeeze for COMEX delivery is fading from the FinTwit feeds, but the structure remains not enough of the stuff for industrial usage going forward.

Finally, the dollar, this morning is, net, doing very little. But there are two stories to note. The first is CNY (-0.2%) where the PBOC changed its risk reserve rules for foreign exchange holdings for Chinese banks, reducing the required reserve to 0% from 20%. In practice, this means that Chinese banks can run forward positions without a capital charge and allows them to be more competitive pricing forward sales of CNY for local hedging counterparts. Obviously, this is a huge adjustment and speaks to the fact that they must be getting a bit uncomfortable with the speed with which the renminbi has been rising over recent months. Ironically, there was a Bloomberg article highlighting how options traders were paying up for 6.50 CNY calls/USD puts anticipating further CNY strength. Perhaps the PBOC didn’t like that!

The other story is from Hong Kong, where the currency is usually not an issue as it is pegged in a very tight band to the USD, allowed to trade between 7.75 and 7.85. The HKMA (HK’s central bank) is committed to buying and selling HKD as necessary to maintain that band. This has been a key feature of Hong Kong’s financial attractiveness for the past decades. The way this operates is there is an exchange fund that is designed to be used only for FX intervention, and it has ~HKD 4 trillion in balances (~$510 billion) which, given their GDP is only $400 billion or so, seems like plenty. Well, as always seems to be the case, the government there is proposing taking some of that money to use for financing a government project, a technology hub being built, and since they don’t want to raise taxes, they thought raiding that fund would be the answer. The concern is the precedent it sets as if that goes through, what is the next project that will be determined to need the funding. If we know one thing about governments it is that if they find a pot of money they can tap to spend more without raising taxes, they are going to do it! The amount in question is a small fraction, just $19 billion, so would not likely impact the HKD peg. But this is something to watch as it will not be a positive if we see this a second time.

Otherwise, NOK (+0.5%) is gaining on oil’s gains while KRW (-0.5%) is slipping on the equity market decline and foreign sales. Beyond that, nothing.

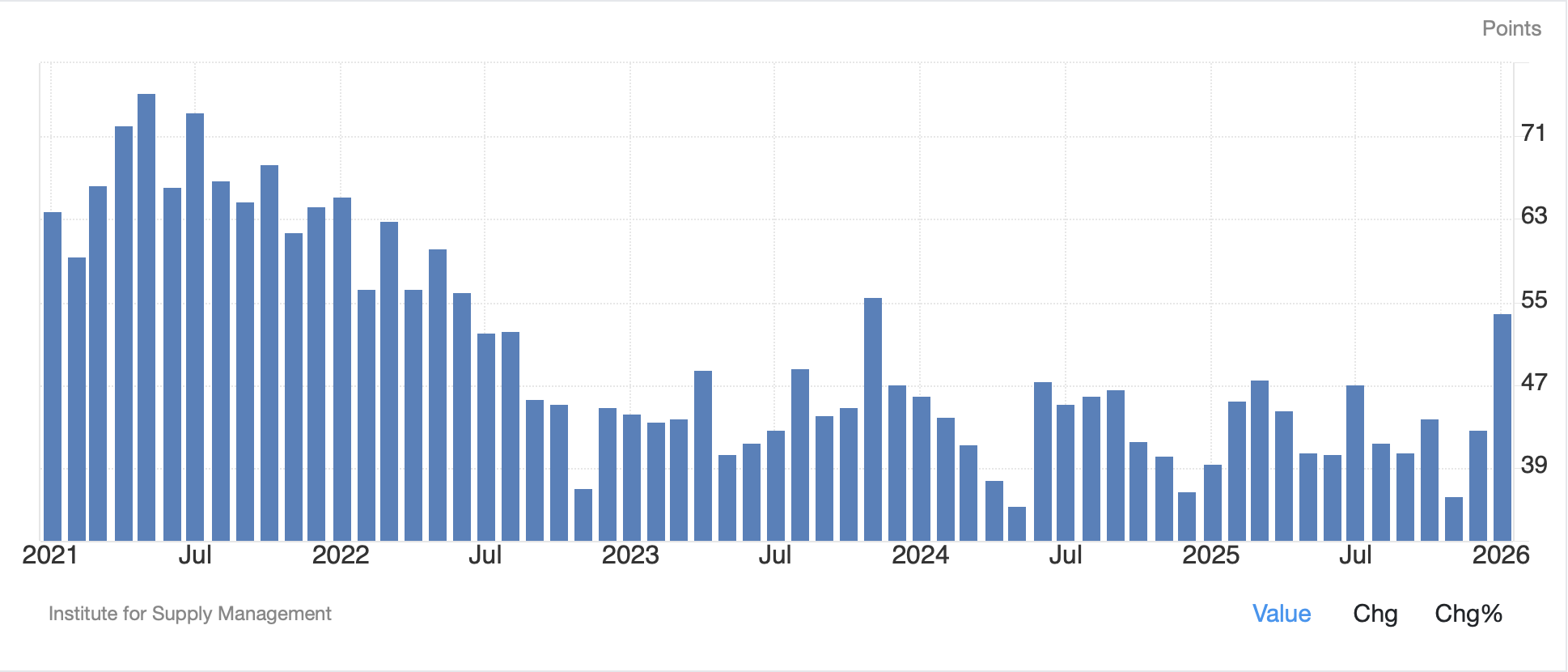

On the data front, this morning brings headline PPI (exp 0.3%,2.6% Y/Y) and core (0.3%, 3.0% Y/Y) as well as Chicago PMI (52.8). Regarding the last, a look at the chart below shows that last month’s reading was the highest since November 2023 and is arguably a good sign that we are seeing increased industrial activity in the middle of the country. Recall, the Chicago number is often seen as a precursor for the economy as a whole.

Source: tradingeconomics.com

And that’s it. Given equity market performance this month has been flat to slightly negative, it seems unlikely there will be large rebalancing flows. I continue to look for quiet markets although the trend in bonds does seem like it is building up some steam.

Good luck

Adf