The new Mr Yen

Is watching for excess moves

With eyes like a bat

While every day of this Trump presidency is filled with remarkable activity at the US government level, financial markets are starting to tune out the noise. Yes, each pronouncement may well be important to some part of the market structure, but the sheer volume of activity is overwhelming investment views. The result is that while markets are still trading, there seem to be fewer specific drivers of activity. Consider the fact that tariffs have been on everyone’s mind since Trump’s inauguration, but nobody, yet, has any idea how they will impact the global macro situation. Are they inflationary? Will sellers reduce margins? Will there be a strong backlash by the US consumer? None of this is known and so trading the commentary is virtually impossible.

With that in mind, it is worth turning our attention this morning to Japan, where the yen (-0.4%) has been steadily climbing in value, although not this morning, since the beginning of the year as you can see from the chart below.

Source: tradingeconomics.com

Amongst G10 currencies, the yen is the top performer thus far year-to-date, rising about 5%. Arguably, the key driver here has been the ongoing narrative that the BOJ is going to continue to tighten monetary policy while the Fed, as discussed yesterday, is still assumed to be cutting rates later in the year.

Let’s consider both sides of that equation. Starting with the Fed, just yesterday Atlanta Fed president Bostic explained to a housing conference, “we need to stay where we are. We need to be in a restrictive posture.” Now, I cannot believe the folks at the conference were thrilled with that message as the housing market has been desperate for lower rates amid slowing sales and building activity. But back to the FX perspective, what if the Fed is not going to cut this year? It strikes me that will have an impact on the narrative, and by extension, on market pricing.

Meanwhile, Atsushi Mimura, the vice finance minister for international affairs (a position known colloquially to the market as Mr Yen) explained, when asked about the current market narrative regarding the BOJ’s recent comments and their impact on the yen, said, “there is no gap with my view. Amid high uncertainty, we have to keep watching the impact of any speculative trading on, not only the exchange market, but also financial markets overall.”

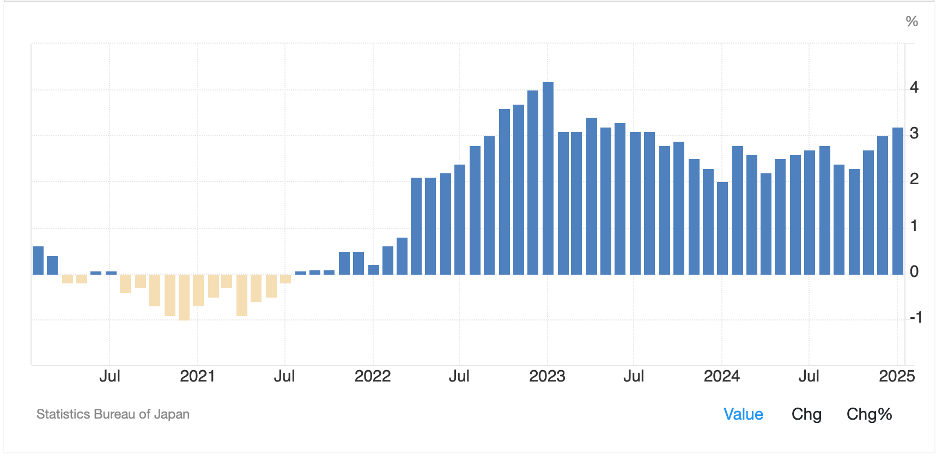

If I were to try to describe the current market narrative on the yen, it would be that further yen strength is likely based on the assumed future narrowing of interest rate differentials between the US and Japan. That has been reinforced by Ueda-san’s comments that they expect to continue to ‘normalize’ policy rates, i.e. raise them, if the economy continues to perform well and if inflation remains stably at or above their 2% target. With that in mind, a look at the below chart of Japanese core inflation shows that it has been above 2.0% since April 2022. That seems pretty stable to me, but then I am just a poet.

Source: tradingecomnomics.com

Adding it all up, I feel far better about the Japanese continuing to slowly tighten monetary policy as they have a solid macro backdrop with inflation clearly too high and looking like it may be trending a bit higher. However, the other side of the equation is far more suspect, as while the market is pricing in rate cuts this year, recent Fed commentary continues to maintain that the current level of rates is necessary to wring the last drops of inflation out of the economy.

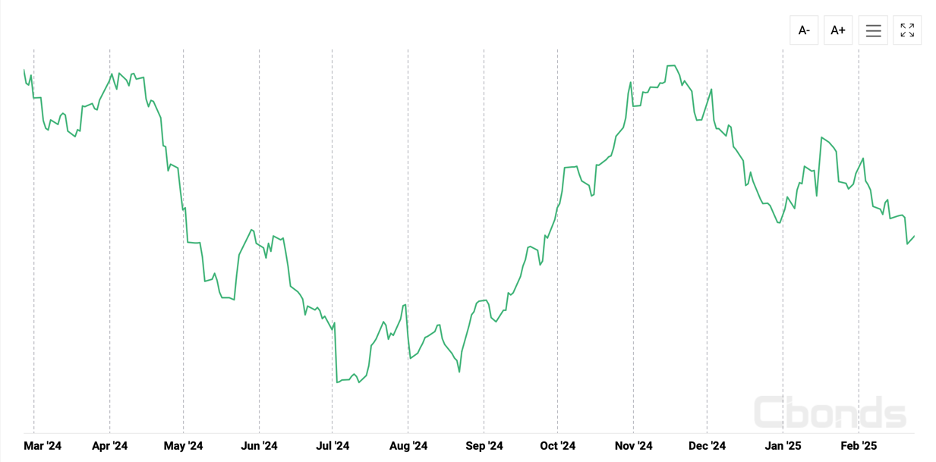

There is a caveat to this, though, and that is the gathering concern that the US economy is getting set to fall off a cliff. While that may be a bit hyperbolic, I do continue to read pundits who are making the case that the data is starting to slip and if the Fed is not going to be cutting rates, things could get worse. In fairness to that viewpoint, the Citi Surprise Index is pointing lower and has been declining since the beginning of December, meaning that the data releases in the US have underperformed expectations for the past two months. (see below)

Source: cbonds.com

However, a look at the Atlanta Fed’s GDPNow estimate shows that Q1 is still on track for growth of 2.3%, not gangbusters, but still quite solid and a long way from recession. I think we will need to see substantially weaker data than we have to date to get the Fed to change their wait-and-see mode, and remember, employment is a lagging indicator, so waiting for that to rise will take even longer. For now, I think marginal further yen strength is the most likely outcome as we will need a big change in the US to alter current Fed policy.

Ok, let’s see how markets have behaved overnight. Yesterday saw a reversal of recent US equity performance with the DJIA slipping while the NASDAQ rallied, although neither moved that far. In Asia, the Nikkei (+0.3%) edged higher as did the CSI 300 (+0.2%) although the Hang Seng (-0.3%) gave back a small portion of yesterday’s outsized gains. The rest of the region, though, was under more significant pressure with Korea, Taiwan, Indonesia and Thailand all seeing their main indices decline by more than -1.0%. In Europe, red is the most common color on the screen with one exception, the UK (+0.35%) where there is talk of resurrecting free trade talks between the US and UK. But otherwise, weakness is the theme amid mediocre secondary data and growing concern over US tariffs. Finally, US futures are nicely higher this morning after Nvidia’s earnings were quite solid.

In the bond market, Treasury yields (+4bps) have backed up off their recent lows but remain in their recent downtrend. Traders keep trying to ascertain the impacts of Trump’s policies and whether DOGE will be able to find substantial budget cuts or not with opinions on both sides of the debate widely espoused. European sovereign yields have edged higher this morning, up 2bps pretty much across the board, arguably responding to the growing recognition that Europe will be issuing far more debt going forward to fund their own defensive needs. And JGB yields (+4bps) rose after the commentary above.

In the commodity markets, oil (+1.1%) is bouncing after a multi-day decline although it remains below that $70/bbl level. The latest news is that Trump is reversing his stance on Venezuela as the nation refuses to take back its criminal aliens. Meanwhile, gold (-1.1%) is in the midst of its first serious correction in the past two months, down a bit more than 2% from its recent highs, and trading quite poorly. There continue to be questions regarding tariffs and whether gold imports will be subject to them, as well as the ongoing arbitrage story between NY and London markets. However, the underlying driver of the barbarous relic remains a growing concern over increased riskiness in markets and rising inflation amid the ongoing deglobalization we are observing.

Finally, the dollar is modestly firmer overall vs. its G10 counterparts, with the yen decline the biggest in the bloc. However, we are seeing EMG currency weakness with most of the major currencies in this bloc lower by -0.3% to -0.5% on the session. In this case, I think the growing understanding that the Fed is not cutting rates soon, as well as concerns over tariff implementation, is going to keep pressure on this entire group of currencies.

On the data front, we see the weekly Initial (exp 221K) and Continuing (1870K) Claims as well as Durable Goods (2.0%, 0.3% ex Transport) and finally the second look at Q4 GDP (2.3%) along with the Real Consumer Spending piece (4.2%). Four Fed speakers are on the calendar, Barr, Bostic, Hammack and Harker, but again, as we heard from Mr Bostic above, they seem pretty comfortable watching and waiting for now.

While I continue to believe the yen will grind slowly higher, the rest of the currency world seems likely to have a much tougher time unless we see something like a Mar-a Lago Accord designed to weaken the dollar overall. Absent that, it is hard to see organic weakness of any magnitude, although that doesn’t mean the dollar will rise. We could simply chop around on headlines until the next important shift in policy is evident.

Good luck

Adf