Poor Ishiba-san

Started with so much promise

Fell flat on his face

In what cannot be a major surprise in the current political zeitgeist, a fringe party that focused all its attention on inflation and immigration (where have we heard that before?) called Sanseito, captured 12 seats, enough to prevent Ishiba-san’s coalition of the LDP and Komeito from maintaining control of the Upper House of Parliament there. The electoral loss has increased pressure on PM Ishiba with many questioning his ability to maintain his status for any extended length of time. While he is adamant that he is going to continue in the role, and that he is fighting the good fight for Japan with respect to trade talks with the US, it appears that the population has been far more focused on the cost of living, which continues to rise, and the increase in foreign visitors in the nation. Sanseito describe themselves as a “Japan First” party.

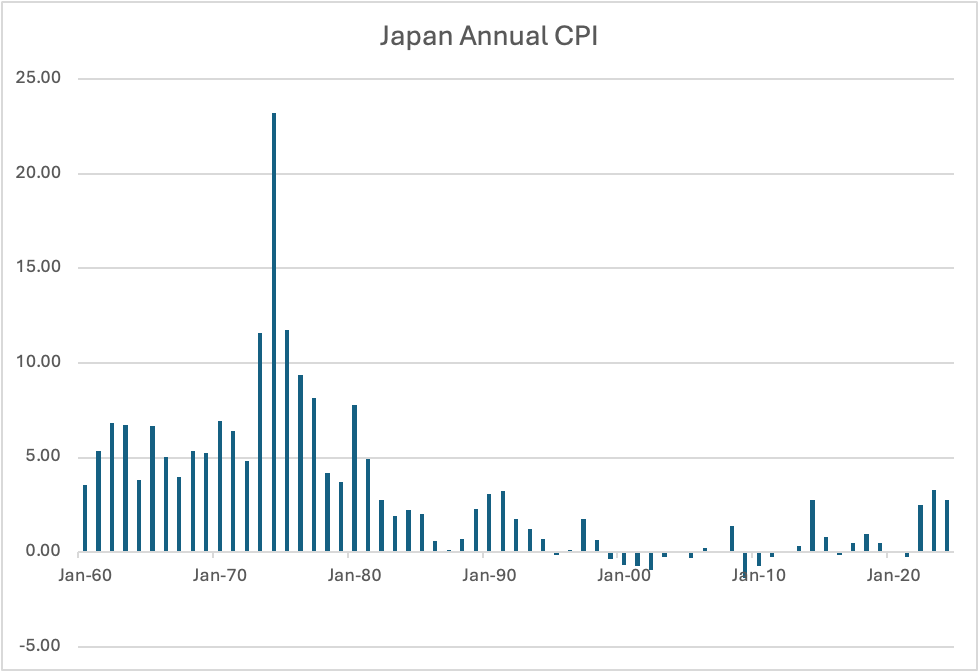

Consider, for a moment, the cost of living in Japan. For the 30 years up until 2022, as you can see from the chart below taken from FRED data, the average annual CPI was 0.44%.

In fact, the imperative for Japanese monetary policy was to end the decades of deflation as it was deemed a tremendous drag on the economy. This was the genesis of their Negative Interest rate policy as well as their massive QE program, which went far beyond JGBs into equities and ETFs. Now, while the economists and politicians hated deflation, it wasn’t such a bad thing for the folks who lived there. Think of your life if prices for stuff that you consume rose less than 1% a year for 20-30 years.

But now, under the guise of, be careful what you wish for, you just may get it, the Japanese government has been successful in raising the nation’s inflation rate to their 2.0% target and beyond and have shown no ability to halt the process. After all, the Japanese overnight rate remains at 0.50% leaving real rates significantly negative, which is no way to fight inflation. So, while Ishiba-san explained to the electorate that he was defending Japan’s pride and industry, the voters said, we want prices to stop rising.

The biggest problem for Japan is that they now have less than 2 weeks to conclude a trade deal with the US based on the latest timeline, and their government is weak with no mandate on trade. It is not impossible that Japan caves on most issues because if they fight, given the government’s current status, it could be a lot worse.

Now, Friday, when I discussed this possibility, I made that case that if the LDP lost the Upper House majority, it would be a distinct negative for both the yen and the JGB market. Well, as you can see in the chart below, the first call has thus far been wrong with the USDJPY falling a full yen right away, and after an initial bounce, it has resumed that downtrend. Like the dollar’s strength when the GFC exploded in 2008, despite the fact that the US was the epicenter of the problem, it appears that Japanese investors are bringing more money home as concern over the future increases. Over time, I expect that the yen is likely to weaken, but I guess not yet.

Source: tradingeconomics.com

As to JGBs, Japan was on holiday last night, celebrating Sea Day, so there was no market in Tokyo. While there is a JGB futures market, there was very little activity, and we will need to wait until this evening to learn their fate.

The deadline for trade talks is looming

And Europe, responses, are grooming

If talks fall apart

And cut to the heart

Of what people there are consuming

The other story that is getting discussed this morning is the fast-approaching trade talk deadline of August 1st. The EU has been actively negotiating to achieve a deal and there appears to be a decent chance that something will be concluded. However, this morning’s stories are all about how Europe is preparing a dramatic response (“if they want war, they’ll get war” according to German Chancellor Merz) if they cannot reach a deal and the US imposes much higher tariffs on EU exports. It is actually quite amusing to see the framing of Europe as the righteous entity being unfairly treated and forced to create a response to the American bullies. But, that is the message from the WSJ and Bloomberg, and I’m sure from the other news sources that I don’t follow.

Every time I consider the trade situation, and the speed with which President Trump is working to conclude deals, I am amazed at how quickly this is all coming about. Consider that the Doha Development Round of trade talks was launched in 2001 and IS STILL ONGOING with no resolution yet. The previous framework, the Uruguay Round took 8 years to complete. Thus, perhaps the question should be, why have trade talks taken so long in the past. Much has been made of how President Trump blinked when the original 90-day window closed and so extended the timeline for a few weeks. Apparently, the use of more sticks and fewer carrots is what has been needed to get these things moving along. Otherwise, trade negotiators had cushy jobs with no accountability and no responsibility, so no incentive to come to an agreement.

Many analysts have explained that the US will suffer from these deals as inflation will rise because of tariffs and growth will slow. Of course, these were the same analysts who explained that tariffs by the US would result in other nations’ currencies weakening to offset the tariff. Once again, I would highlight that old analyst models are not fit for purpose in the current world situation. I have no idea if there will be a successful conclusion of these deals, but I won’t bet against that outcome. In the end, as I have repeatedly explained, the US has been the consumer of last resort for nations around the world, and loss of access to the US market is a major problem for everybody else. That is a very large incentive to agree to deals.

Ok, enough, let’s see how things look this morning. Tokyo was closed last night but we saw gains in Hong Kong (+0.7%) and China (+0.7%) as the PBOC maintained its policy ease supporting the economy. In fact, Chinese money supply has been growing recently which should help the economy there, although it is still struggling a bit. The rest of the region was a mixed bag with some gainers (Korea, India, Indonesia) and some laggards (Taiwan, Australia, Malaysia). In Europe this morning, equities are under some pressure with the CAC (-0.5%) the laggard, although all bourses are lower. This appears to be trade related with some concerns things won’t work out. As to US futures, at this hour (7:05), they are pointing higher by about 0.25%.

In the bond market, yields are falling everywhere with Treasuries (-4bps) lagging the continent where European sovereigns have all seen 10-year yields decline by -6bps to -7bps. It seems that there is growing hope the ECB will cut rates this Thursday, although according to the ECB’s own Watch Tool, the probability is just 2.7% of that happening.

In the commodity space, oil is unchanged this morning as the variety of stories around leave no clear directional driver. However, remember, it has bounced off recent lows despite production increases, and if confidence in economic growth is returning, which it seems to be, then I suspect the demand story will improve. Meanwhile, metals markets (Au +0.65%, Ag +0.89%, Cu +1.1%, Pt +1.2%) are all having a good morning as a combination of dollar weakness and better economic sentiment are supporting the space.

As to the dollar, it is broadly lower against all its major counterparties apart from NOK (-0.2%) and INR (-0.2%) as NY walks in the door. While the yen has been the biggest mover, the rest of the world has seen gains on the order of 0.35% or so uniformly. The INR story apparently revolves around the trade talks with the US and concerns they may not be completed on time, but looking at the krone, after a strong rally last week following oil’s recovery, this morning looks like a bit of profit-taking there.

On the data front, there is very little coming out this week amid the summer holidays.

| Today | Leading Indicators | -0.2% |

| Wednesday | Existing Home Sales | 4.01M |

| Thursday | ECB Rate Decision | 2.00% (no change) |

| Initial Claims | 228K | |

| Continuing Claims | 1952K | |

| Flash PMI Manufacturing | 52.5 | |

| Flash PMI Services | 53.0 | |

| New Home Sales | 650K | |

| Friday | Durable Goods | -10.5% |

| -ex Transport | 0.1% |

Source: tradingeconomics.com

In addition to this limited calendar, it appears the FOMC is on vacation with only two speakers, Chairman Powell tomorrow morning and Governor Bowman tomorrow afternoon. It is hard to get too excited about much in the way of market movement today. As has been the case for the past six months, we are all awaiting the next White House Bingo call, as that is what is driving things for now.

Good luck

Adf