Some days markets have no desire

To move, lacking seller or buyer

But don’t be concerned

The one thing we’ve learned

Is narratives always point higher

While it is clearly not summer as I look out my window and see a snow-covered yard, the doldrums seem to be the best description of markets right now. A dearth of data, and in truth, a lack of commentary by all the usual players, at least new commentary, has both investors and traders looking elsewhere for signals.

Now, this is not to claim that there is nothing happening in the world, but right now, it all seems to be on hold. With the SOTU behind us, we have had nothing new from the White House regarding virtually anything, tariffs, taxes, Iran, you name it. Nvidia earnings last night beat expectations, but apparently not by enough to get people excited. And virtually every other story is a warmed-over version of things we already know.

I think the most interesting market related news that I saw this morning was that the most hawkish member of the BOJ, Hajime Takata, said the BOJ needed to raise rates to fight Japan’s “heated” inflation. This seemed a response to Takaichi-san appointing two doves to the board there. However, the market response was essentially nil, as it should be, with the yen (+0.2%) edging higher while JGB yields (+2bps) also edged higher.

Other than that, seriously, I cannot find a single thing that seems to matter to markets. And it’s not like we have that much to look forward to today in the US, with Initial Claims the only data, so there is no reason to go on too long.

Here is a recap of the overnight session. As I touched on JGB’s above, I will start with the rest of the government bond markets. What we see is that yields are literally unchanged this morning from yesterday’s closing levels. All of them! I am hard-pressed to describe a less exciting market than this.

Turning to equities, yesterday’s solid US performance was followed by mixed outcomes in Asia (Tokyo +0.3%, HK -1.4%, China -0.2%) in the major markets while most other regional bourses saw modest gains or losses with no driving stories. The exception to this was Korea (+3.7%) which has been on an amazing tear lately, as the two largest market cap stocks there, Samsung and SK Hynix, continue to explode higher on demand for memory chips. In fact, I think it is worthwhile to visualize this move as it is rare for equity markets to go parabolic like this.

Source: finance.yahoo.com

Of course, remember what happens to parabolic markets. We just saw that in silver one month ago as per the below, so traders beware!

Source: tradingeconomics.com

Turning to Europe, France (+0.9%) is rallying on some earnings data from key companies, but the rest of the continent, and the UK, are doing little (Germany +0.4%, Spain -0.2%, UK +0.1%). Fittingly, US futures are also unchanged at this hour (7:00).

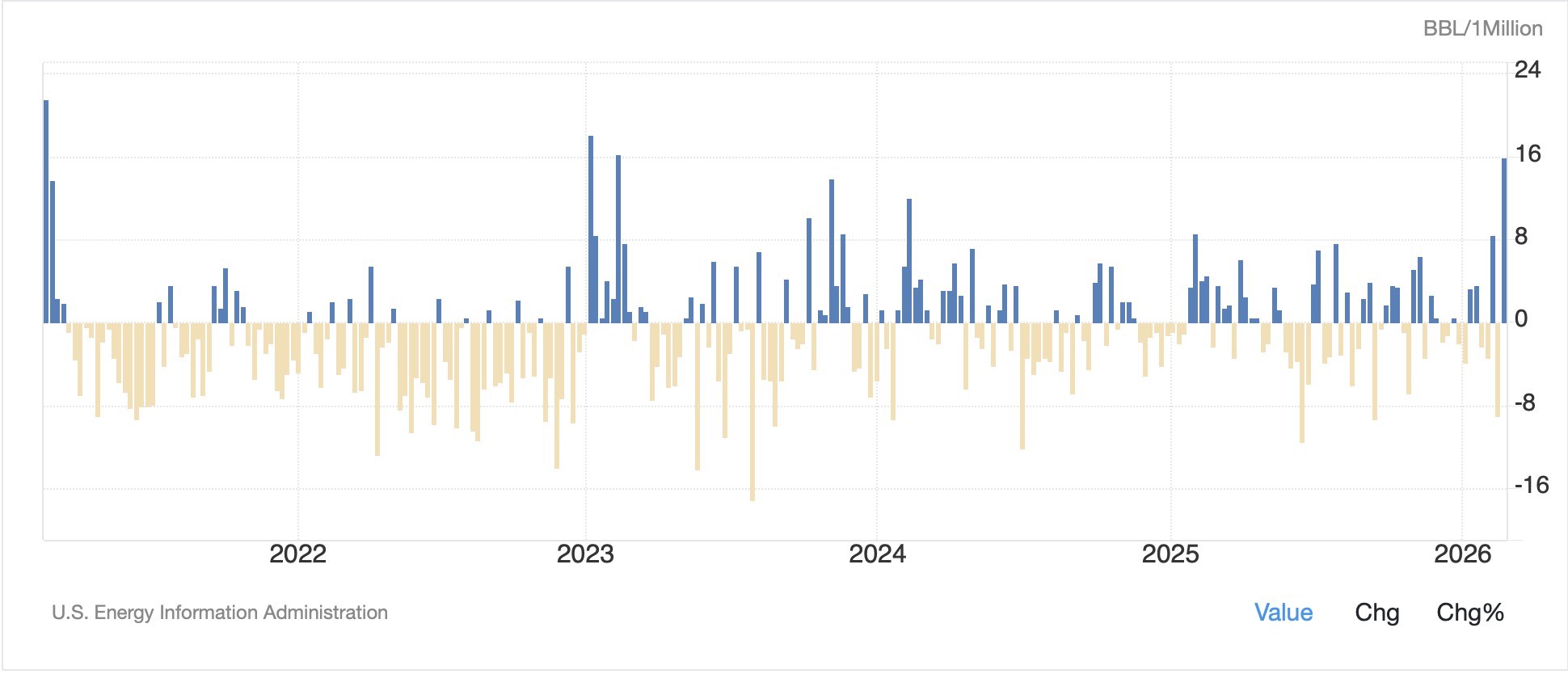

In the commodity space, oil (-1.7%) has softened substantially this morning as the absence of a war in Iran weighs on long positions, but more importantly, I believe, yesterday’s EIA data showed a massive build of inventories of 16mm barrels, far higher than expected and the largest build since February 2023. Back then, it appeared to be the residual response to the Russian invasion of Ukraine as there was a scramble for barrels. Perhaps this is a signal that in the event of a war, there is supply around. If you look at the inventory chart below, we have certainly seen a net build over the past three years. Again, it is hard for me to look at things like this and see significantly higher prices in the future.

Source: tradingeconomics.com

In the metals markets, gold is unchanged this morning, though trading well above the $5000/oz level and seems like it is consolidating before moving higher. Silver (-2.5%) is sliding as there continues to be a discussion regarding deliveries into COMEX contracts with the first notice day for the March contracts tomorrow. There are many pundits who claim there is insufficient silver available to handle the likely deliveries which, if true, would likely cause a significant short squeeze. However, I have no insight into how this will play out. My longer-term view remains that there is a structural shortage of the stuff for industrial applications and the price trend will continue higher, but we have learned how volatile it can be.

Finally, the dollar is modestly stronger this morning with the yen’s rise the exception in the G10 space (EUR -0.1%, GBP -0.2%, AUD -0.2%, CHF -0.3%, NOK -0.3%). In the EMG bloc, we are seeing similar modest weakness across the board (PLN -0.2%, ZAR -0.3%, MXN -0.2%) with the outlier here being CNY (+0.2%). Regarding the renminbi, the Chinese have been marching it slowly higher for the past year, as per the below chart. My take is President Xi is very focused on convincing others the CNY is a viable reserve currency candidate despite all the capital flow restrictions. I’m not sure how that would work, but that is the best I can come up with.

Source: tradingeconomics.com

And that’s all we have in markets this morning. On the data front, Initial (exp 215K) and Continuing (1860K) Claims are the only releases and we hear from Fed governor Bowman, although to the best of my knowledge, nobody is listening to Fedspeak right now. The market continues to price just one 25bp cut for 2026 at this point, although that seems likely to change once we get a better idea as to what Mr Warsh would like to do when he gets the Chair.

My guess is that if there is going to be an attack on Iran, it will happen this weekend, so until then, given the absence of data, I think we drift in all markets and wait for Monday. Today, and tomorrow, ought to be quiet.

Good luck

Adf