On Friday, the Payrolls release

Described a much greater increase

Than pundits had thought

Thus, stocks were all bought

As well there was new hope for peace

This morning the story of note

Is ‘bout a cease fire anecdote

As well, there’s a story

‘Bout analyst glory

And how he learned much in a boat

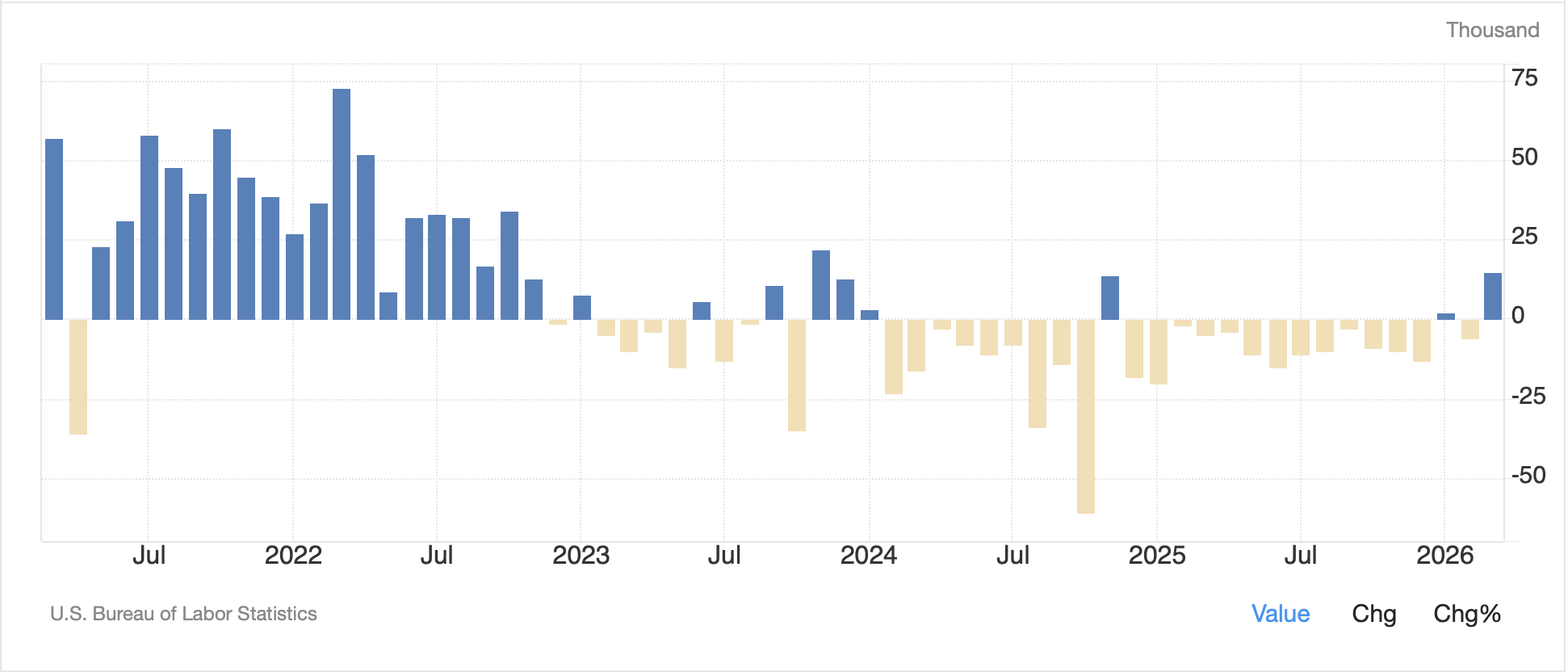

Quickly, let’s recap Friday’s NFP report which showed payrolls jumped 178K, far greater than the 60K expected, although, as has been the case for a while, there was a revision lower to last month’s data. Net, however, given the labor market dynamics discussed on Friday, where zero net job growth appears to equate to a stable, relatively low, unemployment rate, the data was indicative of solid economic activity. Manufacturing Payrolls rose 15K, showing, as per the below chart from tradingeconomics.com, their strongest growth since November 2023 and hopefully the beginning of a trend back toward the levels seen in the wake of the Covid restart. Perhaps President Trump’s reshoring efforts are beginning to pay off.

The Unemployment Rate also ticked lower, to 4.3%, although earnings data was on the soft side, 3.5% annual growth. (My favorite part was government employment fell again, taking the federal, non-military, workforce to its smallest level since the mid 1960’s, a healthy trend I believe.)

The upshot is that Friday saw equity markets rebound from weaker opening levels, Treasury yields rise and oil prices jump along with the dollar while gold prices slid. Of course, in today’s world, that news is completely out of date.

As I type Monday morning, with all of Europe closed for Easter Monday, and most of Asia having been closed as well, the two stories around are 1) talks about a 45-day cease-fire in the war, and 2) an analyst report from Citrini Research describing the traffic through the Strait of Hormuz being much greater than previously believed based on the tracking of ship transponders.

Regarding the first, it is always difficult to understand exactly what is happening with this administration during its conduct of the Iran war. I don’t say that pejoratively, rather I believe it is entirely part of the plan of strategic ambiguity based on President Trump’s overall style. Much of the weekend focused on the remarkable and successful rescue of the 2nd fighter pilot that was shot down late last week, and deservedly so. But there are stories about the US, Iran and regional mediators (Pakistan? Egypt?) trying to get to a 45-day cease-fire that could lead to the end of the war. Of course, we also had President Trump threaten to destroy all of Iran’s infrastructure if they don’t reopen the Strait of Hormuz. As of now, the war continues apace with the latest key news being the killing of the IRGC’s spy chief in an Israeli attack.

But it is the second story that has more punch, and that is that Citrini Research, recently noted for its late February report that described a fictional scenario in 2028 regarding major negative outcomes from the ongoing AI adoption and its impact on employment, the economy writ large, and markets, published a note where they had sent an analyst to the Strait of Hormuz who recorded what was happening there. The upshot is that the activity through the Strait is far greater than had been reported as a number of ships have turned off their transponders and are transiting near the Omani coast.

If one ever doubted the wisdom of the markets, this may be the best indication that markets really are an amazing source of information. Consider the fact that despite the Strait of Hormuz being ostensibly closed, the waterway where ~20% of the world’s oil and LNG transits, the price for both products has been remarkably calm. I am not denying oil (WTI -1.1% this morning) has risen significantly from pre-war levels, just that the fact it has not reached the levels of the Russian invasion spike, let alone the pre-GFC spike, even on a nominal basis, is incredible.

Source: finance.yahoo.com

Russia did not interrupt 20% of the global oil flow. At the margin, if 20% of global oil was not flowing, and given the inelasticity of demand for oil in the short run (estimated at just -0.05 to -0.3 according to Grok), prices above $150/bbl would seem to be more likely. But here we are this morning at $110/bbl. That tells me that the Strait is not shut, although the flow has slowed significantly. But, if 20% of the regular traffic gets through, which seems to be what the Citrini report implies, and both the Saudis and Emiratis have the ability to pipe oil as well, to the tune of an extra 5mm-6mm/bpd, that means the shortage is half the initial fears. (20% of 20mm/bpd + 5mm to 6mm piped). It turns out the world, as a whole, is more resilient than many thought. Certainly, there are nations that are going to suffer because they cannot compete with energy prices this high, but overall, my sense is that the global impact is going to be less than initially feared.

I am not trying to downplay the seriousness of the situation, but from a markets perspective, we need to recognize that perhaps the world is not about to end. This is not to say that things cannot get worse, just that the starting point is probably better than we thought.

Ok, let’s tour the few markets that were open overnight before we’re done. In equity markets, Tokyo (+0.6%) had a pretty good session all things considered as did Korea (+1.4%) and India (+1.1%), which were the major markets open. The picture amongst the other regional exchanges was mixed, although probably a little more red than green. Of course, Asia is the area most negatively impacted by the oil situation. With Europe closed, a quick look at US futures shows that at this hour (8:10) they are modestly firmer.

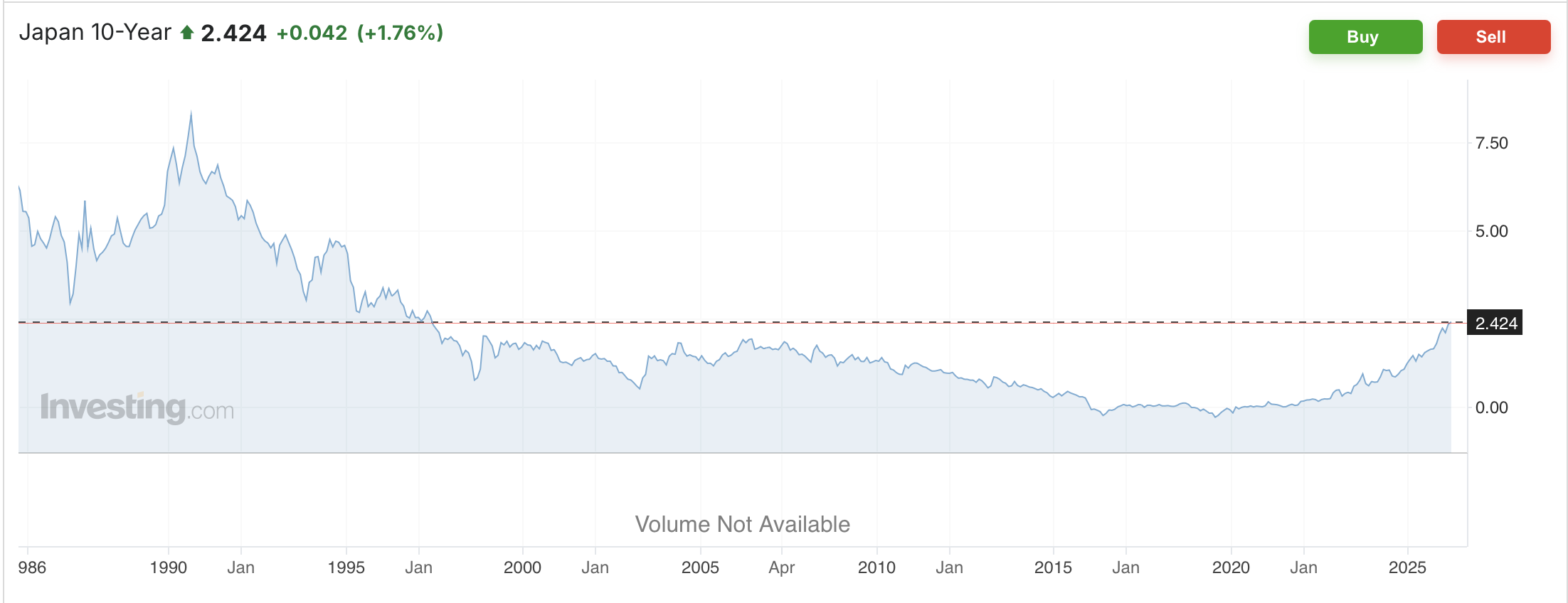

In the bond market, Treasury yields have backed up another 2bps after climbing 4bps on Friday. The only other market open was Japan, with JGB yields rising 3bps and trading at a new high for this move, thus the highest since January 1997 as per the below from Investing.com

We’ve already discussed oil prices with the real interest, to me, the fact that WTI is higher than Brent Crude, an indication that there is increased demand given its availability to any place in the world. As to the metals markets, gold (-0.1%) and silver (+0.2%) are not really telling us much today. There certainly doesn’t seem to be any new information to drive these markets right now.

Finally, the dollar is softer this morning in thin trading, which given the moves in oil and stocks, is not that surprising. But the DXY remains basically right at 100.00 and the yen has been hovering just below the 160 “line in the sand” for the past three weeks as per the below chart from tradingeconomics.com

But with most European centers closed, as well as Canada, I expect that there will be little movement from current levels with very narrow liquidity. Don’t try to do something large today.

Which takes us to the data this week, as follows:

| Today | ISM Service | 550 |

| Tuesday | Durable Goods | -0.5% |

| -ex Transport | 0.5% | |

| Wednesday | FOMC Minutes | |

| Thursday | Initial Claims | 209K |

| Continuing Claims | 1832K | |

| Q4 GDP (final) | 0.7% | |

| Personal Income (Feb) | 0.3% | |

| Personal Spending (Feb) | 0.5% | |

| PCE (Feb) | 0.4% (2.8% Y/Y) | |

| Core PCE (Feb) | 0.4% (3.0% Y/Y) | |

| Real Consumer Spending (Q4) | 2.9% | |

| Friday | CPI | 0.9% (3.3% Y/Y) |

| Ex food & energy | 0.3% (2.7% Y/Y) | |

| Michigan Sentiment | 52.0 | |

| Factory Orders | 0.0% |

Source: tradingeconomics.com

Mercifully, there are only two Fed speakers this week, but again, who is listening to anything they say these days? Certainly, other than Chair Powell, I don’t think they matter at all. PCE and CPI are the big numbers this week, at least from the perspective of how markets are going to anticipate future outcomes, whether monetary policy or fiscal policy. But still, the war is the thing that matters. A cease fire ought to be quite bullish in the short term, for stocks, bonds and gold, while oil and the dollar fall. But it’s anybody’s guess if something like that is going to happen. I wish I had something better to say than play it close to the vest. We are still in a hugely volatile environment with many potential exogenous factors.

Good luck

Adf