The back story of every war

Is nobody knows what’s in store

Especially now

As Trump’s sacred cow

Is changing his message once more

So, yesterday morning, his Tweet

Led many to think a retreat

Was on the horizon

But Trump is surprisin’

With him, one must banish conceit

This morning the story is talks

Twixt both sides are unorthodox

As leaders o’er there

Are fighting since there’s

Nobody in charge, doves nor hawks

Obviously, the Iran situation remains the key driver of all market activity at this point and the stories about negotiations are the lead. From what I can gather, and there is no definitive source I trust completely, a number of nations including Russia, Egypt, Turkey and Saudi Arabia have been trying to get conversations going. Of course, the biggest problem is determining who speaks for Iran as the bulk of their previous leadership has been decapitated. My take is there are different factions, some really hard line apocalyptics who would rather the entire world burn down, especially the US and Israel, than end the hostilities, and there are others who are more pragmatic and want the fighting to end, while perhaps being willing to give up some previous goals, like nuclear weapons ownership.

Everything that I have read about the Iranian leadership structure is that there are many military group leaders who have preset plans if there is no central leadership, and I assume that is why headlines from this morning about ongoing Iranian missile attacks continue. While I am no military strategist, just a poet, from what I have read, if the USMC does, in fact, take over Kharg Island, it is defensible militarily and would essentially end Iranian funding completely. Trump’s comments about the US and Iran running the facility together would imply the US can determine how much oil is shipped while Iran earns the proceeds. In that scenario, it would be possible for the US to starve Iran of the money they need to continue their reign of terror and support for proxy groups. That could well be a very satisfactory outcome for everybody but the mullahs who continue to seek the destruction of Israel and the US. It would also reopen the Strait of Hormuz and we would see dramatic reversals in the price of oil and inflation fears. In fact, I bet rate cuts by central banks would be back on the table immediately!

Ok, enough prognostication from someone in the peanut gallery. Let’s see how markets have responded some 24 hours after Trump’s tweet yesterday morning. volatility remains the primary feature of every financial market led by oil futures. As you can see in the chart below of the last week of WTI price action, there has been a nearly $18 trading range, about 20% of movement in that timeline.

Source: tradingeconomics.com

With the black sticky stuff higher by 2.2% this morning, I would argue that there will be no sense of calm in the markets until oil heads back toward its pre-war levels of $60/bbl or so. If you recall, we discussed the support at $55/bbl in December and questioned what was driving the rise from there. The daily chart for the past six months below offers a better sense of what I believe the market will find reassuring.

Source: tradingeconomics.com

One other thing to remember is that the futures market remains in steep backwardation. A look at the table below shows that prices for future delivery remain upwards of $20/bbl less than prompt prices. All the evidence indicates that this war will be over soon.

Source: barchart.com

Sticking with commodities, precious metals have found some support with gold (+0.5%) and silver (+1.1%) both hanging on this morning.

Turning to equity markets, yesterday’s solid rallies in the US, with all three major indices rising more than 1% was followed by broad strength in Asia (Tokyo +1.4%, HK +2.8%, China +1.3%) with more gainers (Korea, India Australia, Indonesia) than laggards (Taiwan, Malaysia, New Zealand) elsewhere in the region. Two newsworthy items here were that Australia and the EU have signed a free trade agreement reducing tariffs between the two substantially, while RBNZ governor Breman talked about hiking interest rates if inflation picks up because of oil’s rise. (As an aside, that would be a catastrophic error for the nation if she did it.)

Meanwhile, in Europe, it is a far less exciting session as they were able to respond to the Trump tweet during yesterday’s trading. So, this morning, the DAX (-0.35%) is the laggard while the rest of the continent is +/-0.2% or less on the day. This morning’s Flash PMI releases were broadly negative in tone as while Manufacturing readings were a touch better than expected Services in Germany, France, the UK and the EU overall, all showed substantial weakness. I guess the prospect of another energy crisis in Europe is taking its toll. As to US futures, at this hour (7:00) they are basically unchanged.

In the bond market, after a reversal yesterday, where Treasury yields slipped nearly -5bps, this morning they have backed up 3bps. Bond investors remain caught between the idea that inflation is going to be a problem because of higher energy prices and the idea that the economy is going to slip into a recession because of higher energy prices. Remember, too, there is an underlying dynamic where many analysts believe the US is going to hit a financing wall and yields are going to explode much higher. But that story has been with us for quite a while, so I don’t put great stock in it for now.

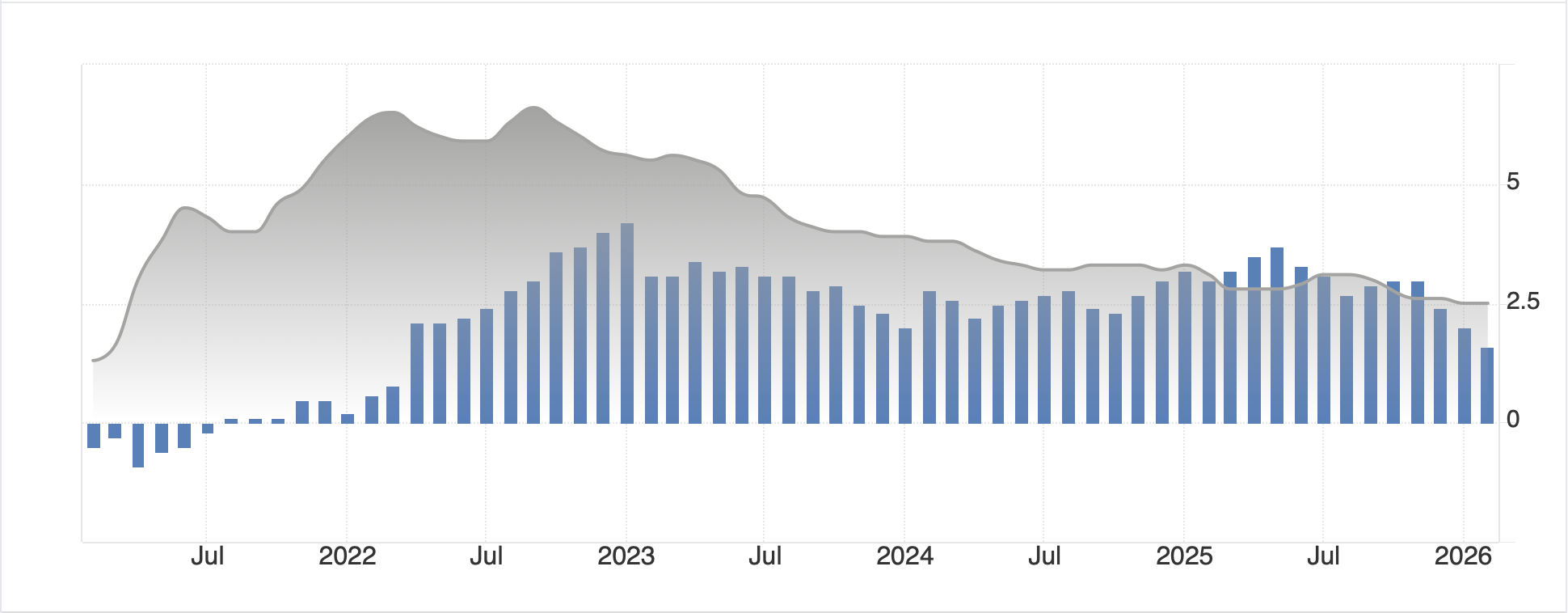

European sovereign yields also slipped yesterday and this morning they are little changed to slightly higher, with both France and Italy (+2bps) the worst performers and all other continental bonds, along with Gilts, essentially unchanged. As to JGBs, last night yields slipped -5bps on both the prospects of the war ending and lower oil prices as well as a better-than-expected inflation reading where headline fell to 1.3% and core to 1.6%, down from 2% in January and a tick below expectations.

A funny thing about Japanese inflation is that if I look at a chart over the past 5 years, it is not hard to make the case that the BOJ has things moving in the right direction, and of course a reading of 1.6% is below their target. In fact, if you look at the chart below comparing Japanese (blue bars) and US (gray space) core inflation, I expect Chairman Powell would give anything to have the Japanese chart!

Source: tradingeconomics.com

Finally, the dollar, while firmer this morning (DXY +0.3%) has traded right back into its long-term trading range of 96/100. Again, I cannot look at the chart below and conclude that the dollar is going anywhere anytime soon. If skyrocketing oil prices and a war in Iran cannot get a real breakout, I think we will have to go back to interest rate differentials as the driver!

Source: tradingeconomics.com

As to specific currencies, ZAR (-1.35%) is the day’s laggard as the recent sharp decline in both gold and platinum weigh on the nation’s accounts, as well as their status as a major energy importer. We’ve also seen weakness in PLN (-0.5%), HUF (-0.6%), INR (-0.5%) and, interestingly, AUD (-0.5%) despite the latter’s deal with the EU. I think ongoing high energy prices remain the issue here. For the majors, -0.2% is the order of the day for the euro, pound, yen and Swiss franc.

On the data front, there’s not a ton of data this week.

| Today | Nonfarm Productivity Q4 | 2.0% |

| Unit Labor Costs Q4 | 3.5% | |

| Flash Manufacturing PMI | 51.3 | |

| Flash Services PMI | 51.5 | |

| Thursday | Initial Claims | 210K |

| Continuing Claims | 1860K | |

| Friday | Michigan Sentiment | 53.8 |

| Michigan Inflation Expected | 3.2% |

Source: tradingeconomics.com

In addition to the modest data releases, we hear from 5 Fed speakers over 7 venues this week, but it is very hard for me to believe that anything they say will matter while the war hogs the headlines.

Prognostication is silly here as headlines drive everything. My sense is playing it close to the vest remains the best strategy. But remember this, despite all the pearl clutching and teeth gnashing, the S&P 500 is just 6% from its high print back in January. This has not even achieved what is typically considered a correction. The lesson here is that history shows we can decline much further, but also that there is a lot of resilience in the market right now, hence, close to the vest.

Good luck

Adf