Apparently, nerves are on edge

Though pundits, no worries, allege

But missiles are flying

So, traders are buying

Safe havens as they start to hedge

So, it cannot be that surprising

The dollar and gold keep on rising

While sales are quite brisk

For assets with risk

Like stocks with investors downsizing

While some of you may be concerned over the news that Russia has launched an intercontinental ballistic missile in an its latest attack on Ukraine (as an aside, since both Russia and Ukraine are in Europe, was it really intercontinental?), by focusing on mundane aspects of life and death, you may have missed the truly important news release from yesterday afternoon, Nvidia’s guidance was disappointing and its stock price declined! It is for situations like this that I write this morning missive, to make sure you focus on the important stuff.

All kidding aside, the knock-on effects of the escalation of the fight in Ukraine are likely to be more impactful over time, especially for Europe. Consider the fact that most of Europe has recently been blanketed by a major winter storm with much colder than normal temperatures, and another one is forecast for the coming days. As well, part of this weather pattern is weaker than normal wind speeds, so much of the continent is suffering a dunkelflaute again. The energy implications are significant as both wind and solar power are virtually non-existent which means they are hugely reliant on NatGas to both keep the lights on and keep warm.

However, Europeans continue their energy suicide and have recently closed one of the only domestic sources of NatGas to satisfy their Green tendencies. This means they will be buying more LNG and competing more aggressively with Asia for cargoes. While NatGas prices in the US have risen sharply in the past month, ~46%, they remain far below prices in Europe, less than one-quarter as expensive. It is exactly this reason that an increasing number of companies in Europe are looking to relocate to areas with less expensive energy, like the US, and why investment in the US continues to outpace investment elsewhere. Look no further than this to understand a key ingredient of the dollar’s ongoing strength.

Of course, there is another story that is dominating the press, the ongoing Trump cabinet picks and all the prognostications as to what they all mean for the future of US policies. You literally cannot read a story without someone elsewhere in the world quoted as explaining they are awaiting the inauguration to see how things evolve and so they are postponing any new actions. This is true for both governments and private companies (although obviously, the Biden administration is taking the opposite tack of trying to do as much as possible before the inauguration, like starting WWIII it seems).

And that is the world this morning, anxiety over the escalation in Ukraine, disappointment that Nvidia didn’t beat the most optimistic forecast expectations and uncertainty over what President-elect Trump is going to do once he is in office. It is with this in mind that we look at markets and see that the best performances are coming from havens and necessities. On days like this, risk does not seem as appetizing.

Let’s start in the commodity markets this morning, where oil (+2.0%) is responding to both the Russia/Ukraine escalation and the US veto of a UN ceasefire resolution in Gaza with both of these prompting increased concerns of a short-term supply disruption. While yesterday’s US inventory data showed some builds, for now, fear is the greater factor. Meanwhile, NatGas (+6.3%) is skyrocketing amid forecasts for colder weather as a polar blast hits both Europe and the West Coast. While the longer-term implications of a Trump presidency are for energy prices to stabilize or decline on the back of increased supply, that is not yet the case. Meanwhile, gold (+0.5%) continues its rebound from its recent correction as havens are clearly in demand. Remember, too, that almost every central bank remains in easing mode as they all convince themselves they have beaten inflation.

However, a look at equity markets shows a less resilient picture, at least from Asia where we saw the Nikkei (-0.85%) slip after that Nvidia result and the Hang Seng (-0.5%) also feel that pain. Remember, these indices are very tech focused and Nvidia remains the tech bellwether. While mainland Chinese shares were little changed, there was weakness in India, Taiwan, Malaysia and Indonesia, as a taste of how things behaved overnight. Europe, though, is managing to shake off some of its concerns and most markets have edged higher, between 0.2% and 0.4% although the CAC (-0.15%) is lagging. The latter is somewhat ironic given that French Business Confidence rose more than expected to 97, although that is merely back toward the long-term average of that series. Arguably, the European move is on the back of US futures, which had been lower all evening but at this hour (7:30) are now all in the green by at least 0.2%.

However, under the heading havens are in demand, bond yields are backing off a bit with Treasury yields lower by -2bps and most European sovereigns lower by between -1bp and -3bps. The tension in this market remains between recent declines in some inflation readings and growing concerns over the potential inflationary policies that President Trump will enact when he gets into office. Nothing has changed my view that inflation is not dead and that a grind higher in yields seems the most likely outcome.

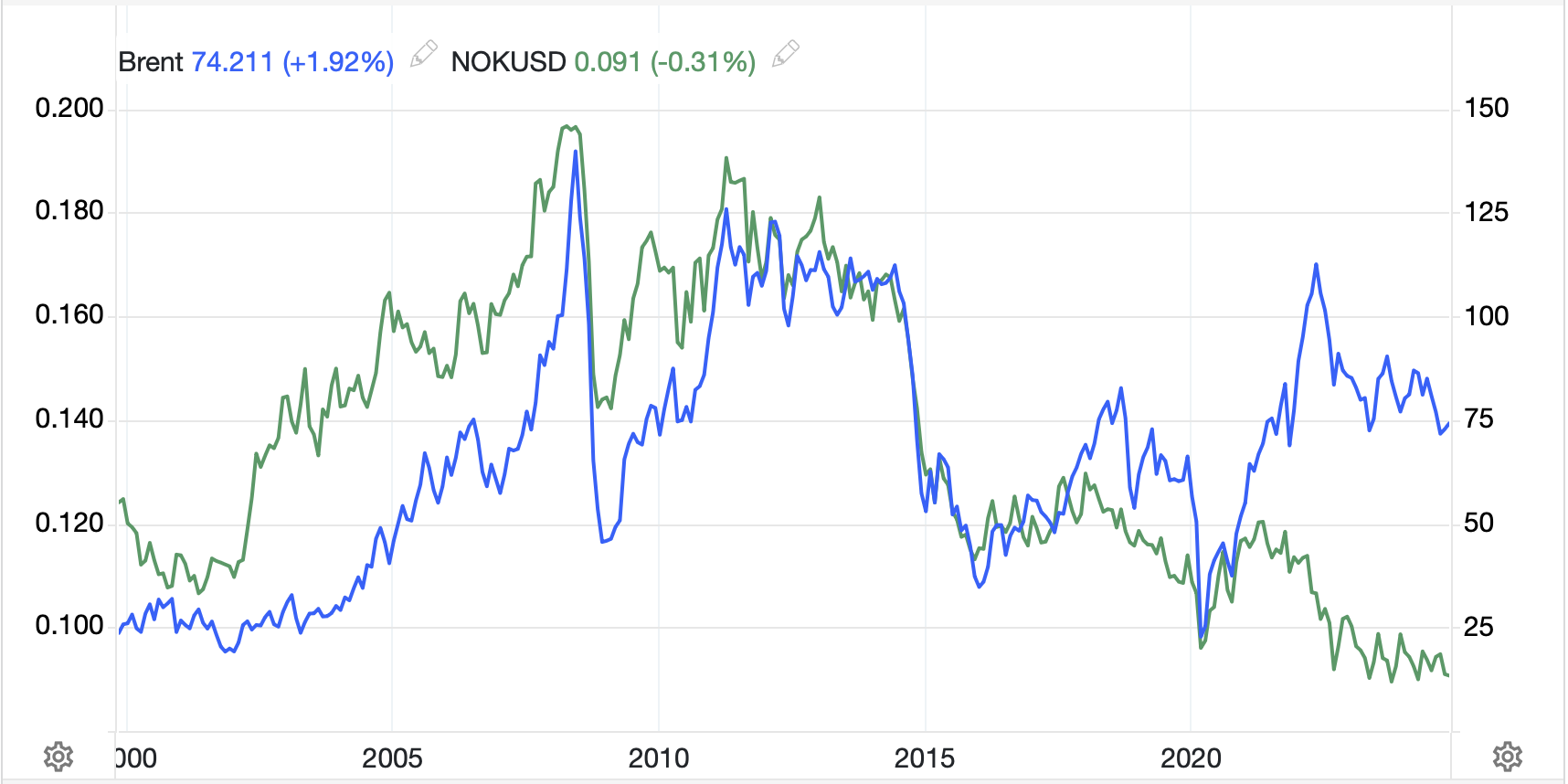

Finally, the dollar continues to find support versus almost all its counterparts, although this morning the yen (+0.5%) is demonstrating its own haven characteristics. But broadly, the DXY is higher by 0.1% with the euro creeping ever closer to 1.0500 and the pound to 1.2600. As well, NOK (+0.3%) is benefitting from the oil’s rise. This latter relationship, which makes perfect economic sense given the importance of oil to Norway’s economy, has been quite strong for a long time as can be seen in the chart below. While daily wiggles may be different, the only true disruption was the start of the Ukraine war where oil jumped massively, and NOK did not follow along given its proximity to the war. But otherwise, it’s pretty clear.

Source: tradingeconomics.com (NOKUSD is the inverse of what you typically see)

As to the emerging markets, we are seeing weakness in LATAM (BRL -0.8%, MXN -0.5%) as well as EEMEA (PLN -0.3%, CZK -0.5%, HUF -0.5%) although ZAR (+0.2%) seems to be benefitting from the ongoing rise in gold. Asian currencies were much less impacted overnight and have not moved much at all.

On the data front, this morning brings the weekly Initial (exp 220K) and Continuing (1870K) Claims data as well as Philly Fed (8.0) and then at 10:00 Existing Home Sales (3.93M) and Leading Indicators (-0.3%). Chicago Fed president Goolsbee speaks this afternoon, but again, it would be quite a surprise if he veers away from Powell’s comments last week. This morning, the Fed funds futures are pricing a 55.7% probability of that December rate cut, and today’s data seems unlikely to change that. Next week’s PCE data will be far more important.

It is interesting to see the equity market rebound but there is a huge amount of belief that Mr Trump is going to fix everything. While I hope his policies improve the situation, and there is much to improve, it will take time before we see any truly positive impacts I believe. I understand that markets are forward looking, but clarity remains elusive at this time. The one thing that remains clear to me, though, is the demand for dollars is likely to continue for a while yet.

Good luck

Adf