The financial impacts of war

Are many, and so here are four

Inflation will rise

And what this implies

Investors, most bonds, will abhor

The dollar is like to remain

Demanded and that will cause pain

For stocks everywhere

But one thing will fare

Just fine, look for gold, more, to gain

Obviously, the war in Iran remains the top story and is likely to remain so for a few more weeks at least. Arguably, the only way this will change is either a regime change takes place and talks for peace begin, or Iran is able to retaliate in a heretofore unknown fashion sufficient to force the US and Israel to withdraw. President Trump has indicated he believes this campaign will last 4-5 weeks with that regime change the result. But remember, the Russia/Ukraine war slipped from the headlines after 6-8 weeks, and it is still ongoing. In fact, I challenge you to find a story about that war anywhere these days.

My point is, despite the ongoing hostilities, the rest of the world continues on its way, albeit with some new bumps in the road. Clearly, the biggest bump remains the price of oil and, for much of Europe and Asia, its continued availability. While the price of oil (+0.1% today) has risen about 18% in the past month, a look at the long-term chart below offers a bit more perspective as to just how limited this movement has been so far.

Source: tradingeconomics.com

I have highlighted the week of the Russian invasion from February 2022, which saw oil rise more than 20% at the time and remain elevated for about 5 months before it retraced to prewar levels. The reaction this time has not been nearly as dramatic even though the effective closure of the Strait of Hormuz has removed about 20% of global oil supply from the market right now, as well as a similar proportion of LNG. This is why we have seen the massive spike in European and Asian LNG prices as that was the destination of those cargoes. Ironically, one of the most negatively impacted nations is China, which was Iran’s biggest oil customer, but now has seen a dramatic decline in the availability of oil. Of course, they have built a significant stockpile, their own SPR, which holds between 1.2 -1.5 billion barrels, enough to supply the nation for upwards of 4 months. While not an immediate concern, it will start to hurt after a while if this continues.

It appears to me that unless Iran starts targeting and destroying oil production facilities throughout the Middle East, which is certainly possible, the upside for prices from here is limited under current circumstances. My guess, and it is just that, is another 10%. Of course, the risk for Iran there is that it draws the Saudis, Emiratis and the rest of the Gulf into the war against Iran, probably not a desired outcome either.

As an aside, I wonder if prices rise far enough in a worst-case scenario, if the UK removes its drilling restrictions, although thus far, PM Starmer has not indicated anything of the sort. It depends on just how painful things become I suppose.

Moving on to the equity markets, while US markets have declined somewhat since the war began, the S&P 500 remains just 2.5% below its all-time high set February 28, and as you can see from the chart below, does not appear to be altering the recent trajectory in any meaningful fashion.

Source: tradingeconomics.com

However, the same cannot be said for several other markets, notably those in Asia. The Kospi (-12.1%) is the worst offender as seen below. But weakness in the region was widespread with the Nikkei (-3.6%), Hang Seng (-2.0%), Taiex (-4.3%) and Thailand’s SET 50 (-5.4%) leading the way lower with most other bourses falling on the order of -1.0% to -2.0%. This makes sense as virtually all these nations rely on energy from the Middle East, and with both higher prices and reduced supply, trouble is afoot.

Source: finance.yahoo.com

Of course, as you can also see in the KOSPI chart above, with similar price action elsewhere in the region, these stock markets have been on a tear given their tech focus (Korea’s two largest companies are Samsung and SK Hynix, both semiconductor manufacturers) so there was some room for a reversal. In fact, remarkably, despite the KOSPI having fallen almost 20% this week, it remains above its trend line. My take is this is a major correction and something we will see until things in the Middle East settle down.

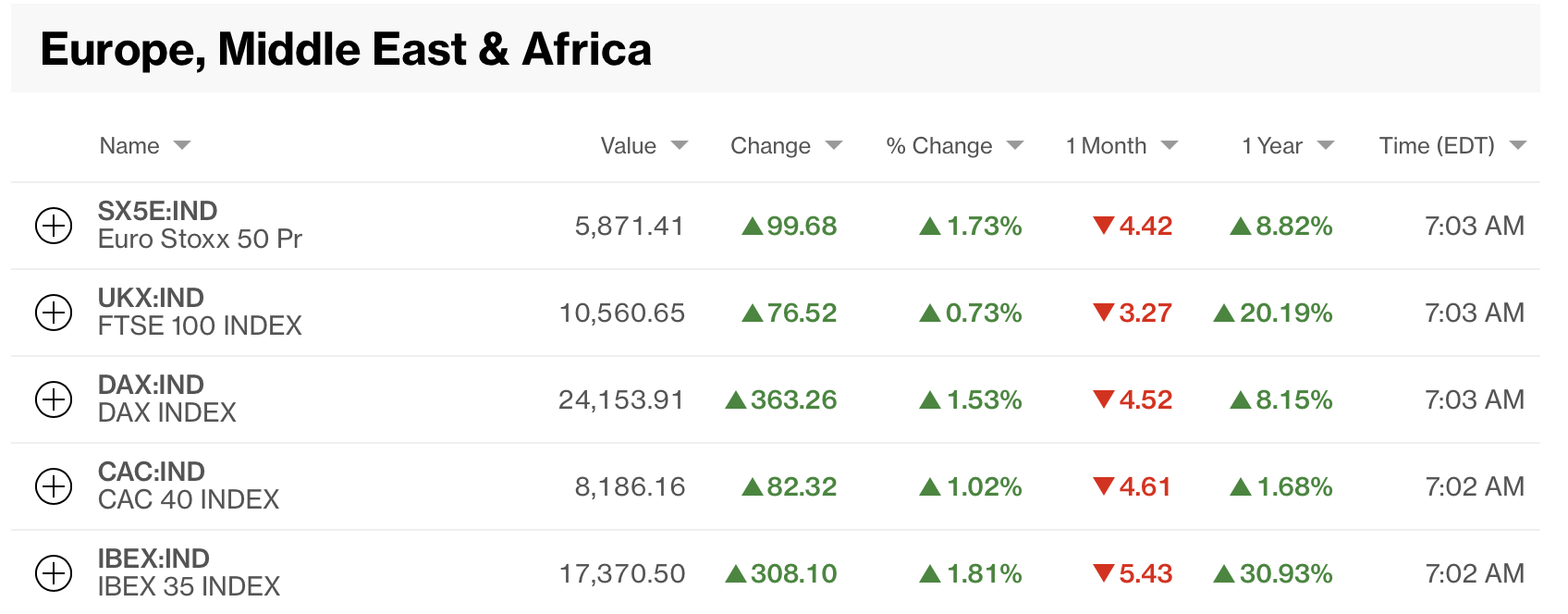

Working in favor of my correction explanation is the fact that European bourses, which all fell sharply yesterday, are all higher this morning as per the below Bloomberg table.

As to US futures, at this hour (7:30) they are little changed.

Turning to the bond market, after some initial fears over the inflation implications of the war, as well as the selling that accompanies margin calls, yields have settled down a bit. This morning Treasury yields (+2bps) are a touch higher but, at 4.08%, hardly running away. As to European sovereign yields, they are essentially unchanged this morning, and even JGB yields (-2bps) slipped a bit last night. As I discussed above, markets have digested much of the news and seem to have found a new equilibrium

I didn’t mention metals markets above, but this morning, in sync with other markets that are rebounding, we see the entire space higher; Au +1.7%, Ag +4.3%, Cu +1.1%, Pt +3.8%. This story of insufficient supply to meet ongoing industrial demand has not changed, nor has the demand by both central banks and individuals, especially in Asia, to hold gold as a store of value.

Finally, the dollar is backing off slightly this morning, which given the price action elsewhere, makes perfect sense. In the G10 space, the movement has been on the order of 0.1% to 0.2% for the majors (EUR +0.2%, GBP +0.1%, AUD +0.1%, CHF +0.2%) with only JPY (+0.35%) and SEK (+0.8%) showing real gains. However, it is important to remember that SEK was one of the worst performers recently, so had more ground to regain. As to the EMG bloc, movement there has been more substantial, but again, this is after much larger declines. For instance, BRL (+0.6%) and KRW (+0.9%) have both seen sharp declines in the past week before reversing overnight as per the below chart.

Source: tradingeconomics.com

However, if we look at the DXY as our proxy, it remains in the middle of its trading range of the past 9+ months.

Source: tradingeconomics.com

In sum, we are three trading days into an entirely new geopolitical situation, and markets have digested the news and are seemingly trying to return to some sense of normalcy. Now, there is still significant headline risk as nobody knows how things will evolve here. What I will say is that if the Iranian regime falls or capitulates, I would look for risk to be quickly scooped up while oil prices slide. Conversely, if things drag on much longer than another month, I think we could well see investor concern over how this will impact the global economy, especially if oil prices remain in the $75 – $80/bbl range, which likely means equity markets will suffer.

To the extent that anyone is still looking at data, this morning brings the ISM Services (exp 53.5) and then we see Crude Oil inventories later this morning. The Services PMI data throughout Europe and Asia was in line with expectations showing slow growth remains the story. Chinese data was marginally softer for large companies and marginally stronger for small companies. As well, the Fed’s Beige Book is released at 2:00 this afternoon.

However, I don’t see data as a driver yet, so headline risk remains the biggest one out there, but the indications are markets are starting to absorb the war and move on.

Good luck

Adf