Inflation just won’t go away

As evidenced by the UK

This year started out

Removing all doubt

The Old Lady’s work’s gone astray

And elsewhere, the problem is still

Inflation is quite hard to kill

Though central banks want

More rate cuts to flaunt

Those goals are quite hard to fulfill

While most eyes remain on President Trump with his ongoing efforts to reduce the size of the US government, as well as his tariff discussions and efforts to negotiate a lasting peace in Ukraine, we cannot ignore the other things that go on around the world. One of the big issues, which has almost universally been acclaimed a problem, is that inflation is higher than most of the world had become accustomed to pre-Covid. As well, the virtual universal central bank goal remains the local inflation rate, however calculated, to be at 2.0%. Alas for the central bankers in their seats today, that remains quite a difficult reach. A quick look at the most recent headline CPI readings across the G20 shows that only 5 nations (counting the Eurozone as a bloc since they have only one monetary policy) are at or below that magic level as per the below table.

Source: tradingeconomics.com

Of those nations who are below, two, China and Switzerland, are actually quite concerned about the lack of price pressure and seeking to raise the inflation rate, and the other three (Canada, Singapore and Saudi Arabia) are right on the number, with core inflation readings tending higher than the headline reported here.

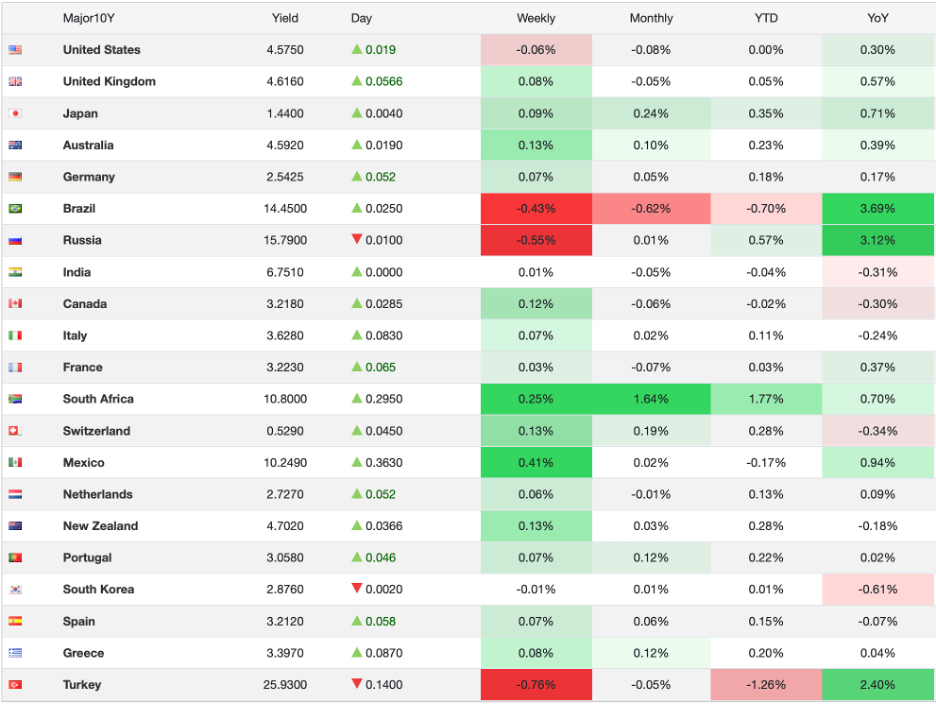

Perhaps a better way to highlight the problem is to look at the 10-year bonds of most countries and see how they have been behaving of late as an indication of whether investors are comfortable with the inflation fighting efforts by each nation. While it is not universal, you can look at the column on the far right of the below table and see that 10-year yields have been rising for the past year.

Source: tradingeconomics.com

I only bring this up because, despite the fact that I have been downplaying central bank, especially the Fed’s, impact on markets, ultimately, every nation tasks their central bank to manage inflation. That seems reasonable since inflation, as Milton Friedman explained to us in 1963, is “always and everywhere a monetary phenomenon.” But perhaps you don’t believe that and are schooled in the idea that faster growth leads to higher wages and therefore higher inflation. Certainly, Paul Samuelson’s iconic textbook (as an aside, Dr Samuelson was my Economics 101 professor in college) made clear that was the pathway. Alas, as my good friend, @inflation_guy Mike Ashton, wrote yesterday, there is no evidence that is the case. Read the article, it is well worth it and can help you start looking elsewhere for causes of inflation, like perhaps the growth in the money supply!

Of course, the reason that we continue to come back to inflation in our discussions is because it is critical to the outcomes in financial markets. And that is our true focus. It is the reason there is so much discussion regarding President Trump’s mooted tariffs and how inflationary they will be. It is the reason that parties out of power continue to highlight any prices that have risen substantially in an effort to disparage the parties in power. And it is the reason that central banks remain central to the plot of all financial markets, at least based on the current configuration of the global economy. If there was only one financial lesson from the pandemic response, it is that Magical Money Tree Modern Monetary Theory is a failed concept of how to run policy. This poet’s fervent hope is that Treasury Secretary Bessent is smart enough to understand that and will address fiscal issues in other manners. I believe that to be the case.

Back to the UK, where CPI printed at 3.0%, 2 ticks higher than the median forecast, while core CPI printed at 3.7%. This cannot be comforting for the BOE as most of the MPC remain committed to helping PM Starmer’s government find growth somehow and are keen to cut rates in support. The problem they have is that inflation will not fade despite extremely lackluster GDP growth. Recall, last week, even though the Q/Q GDP print of 0.1% beat forecasts, it was still just 0.1%. Not falling into recession hardly seems a resounding victory for policy in the UK, especially since stagnation, or is it now stagflation, is the end result. It should be no surprise that market participants have sold off the pound (-0.3%), Gilts (+5bps) and UK equities (-0.4%) and it is hard to find a positive way to spin any of this. Again, while I have adjusted my views on Japan, the UK falls squarely in the camp of in trouble and likely to see a weaker currency.

Ok, let’s look elsewhere to see how things behaved overnight. After a very modest rise in US equity indices yesterday, the Asian markets were mixed with the Nikkei (-0.3%) and Hang Seng (-0.15%) slacking off a bit although the CSI 300 (+0.7%) managed to find buyers after President Xi met with business leaders and the expectation is for further government stimulus, as well as a reduction in regulations, to help support the economy. Australia (-0.7%) is still under pressure despite yesterday’s RBA rate cut as the post-meeting statement was quite hawkish, indicating caution is their approach for now given still sticky inflation. (Where have we heard that before?)

In Europe, the only color on the screen is red with declines of between -0.4% and -0.9% as investors seem to be taking some profits after a solid run in most of these markets. I guess the fact that European governments have been shown to be powerless in the world has not helped investor sentiment either as it appears these nations may be subject to more outside forces than they will be able to address adequately. Lastly, US futures are unchanged at this hour (7:40).

In the bond market, as per the table above, yields are higher across the board with Treasuries (+2bps) the best performer as virtually all European sovereign issues have seen yields rise between 5bps and 7bps. It simply appears that confidence in the Eurozone is slipping and demand for Eurozone assets is falling alongside that.

In the commodity markets, it should be no surprise that gold (+0.1%) continues to edge higher. The barbarous relic continues to find price support despite the fact that interest in gold, at least in Western economies, remains lackluster at best. There is much discussion now about an audit of the US’s gold reserves at Fort Knox and in the NY Fed, something that has not been performed since 1953. Not surprisingly, there are rumors that there is much less gold in storage than officially claimed (a little over 8 tons) and rumors that there is much more which has not been reported but was obtained via seizures throughout history. This story has legs as despite the lack of institutional interest in the US, it is picking up a retail following and we are seeing the punditry increasingly raise their price forecasts for the coming years. As to oil (+0.8%) it is higher again this morning but remains in a tight trading range with market technicians looking at the $70/bbl level as a key support to hold. A break there could well see a quick $5/bbl decline.

Finally, the dollar is modestly firmer this morning against most of its counterparts with most G10 currencies showing declines similar to the pound’s -0.2%, although the yen (+0.15%) is bucking that trend. However, versus its EMG counterparts, the dollar is having a much better day, rising vs. PLN (-0.9%), ZAR (-0.7%) and BRL (-0.5%) on various idiosyncratic stories. The zloty seems to be suffering from its proximity to Ukraine and the uncertainty with the future regarding a potential peace effort. The rand is falling after the FinMin delayed the budget speech as internal squabbling in the governing coalition seems to be preventing a coherent message while the real is under pressure as inflation remains above target and the central bank’s tighter policy has been negatively impacting growth in the economy.

On the data front, this morning brings Housing Starts (exp 1.4M) and Building Permits (1.46M) and then this afternoon we see the FOMC Minutes from the January meeting. That will be intensely parsed for a better understanding of what the committee is thinking. We do hear from Governor Jefferson after the market closes, but generally, the cautious stance remains the most popular commentary.

Has anything really changed? The market remains uncertain over Trump’s moves, the Fed remains on hold and cautious, and data shows that the economy continues to tick along nicely with price pressures unwilling to dissipate. I see no reason to abandon the dollar at this point.

Good luck

Adf