Each day it gets tougher and tougher

To figure out things that can buffer

Portfolios from

The beating war drum

And so, we are all set to suffer

Remember, too, I’m just a poet

And I do my best not to show it

But my Spidey sense

Says come some days hence

The end will be nigh and we’ll know it

Basically, as Herbert Stein explained back in 1986, “If it can’t go on forever, it will stop.” The pressures on the global economy are increasing dramatically as not only markets in oil and natural gas, but also fertilizer and helium (critical for semiconductor manufacturing) markets are being significantly impacted. And frankly, the world as we know it now cannot exist without a healthy supply, and supply chain, in all those things. It is this pressure, which is building up on both sides of this war, that will ultimately push both sides to some resolution. Iran cannot live without the oil and its revenues, but it can certainly destroy a lot of other nations in its death throes. That is not the outcome we want to see.

And frankly, it appears to me that markets are pricing an off-ramp, because otherwise, I would expect the inelasticity of demand for oil would have driven oil prices much higher than we have seen. But, while that may be the medium term (next several weeks) view, on a day-to-day basis, one never knows what’s going to happen. Yesterday, there was a sense that things were going to deescalate. But overnight, that sentiment changed and now risk is under pressure as oil heads higher once again.

Here’s the problem, if you read all the headlines about the situation in the Persian Gulf, you are no more well-informed than if you ignore them all. We continue to be bathed in opinions and propaganda from both sides, and it is certainly not within my ability to determine what is truth, assuming any of it is. Which takes us back to markets as our best indicator, because as it has been said, opinions are like a$$holes, everybody has one and they all stink.

So, let’s go to the tape. Yesterday saw a positive outcome, but as you look at the chart of the S&P 500 below, you can count that from the beginning of March, when this all began, there have been 19 trading sessions including today. Nine of those sessions saw green candles (higher) and 10 saw red candles (lower). This does not strike me as a market where investors have capitulated in any serious manner. As I mentioned earlier in the week, despite all the angst, right now the S&P 500 is lower by just 6.5% from its all-time high from late January. That’s not even a correction by most definitions, let alone a war footing.

Source: tradingeconomics.com

As it happens, today is a down day, with US futures sitting lower by about -0.5% across the board as of 7:00. And that is consistent with what we observed overnight with both major Asian (Tokyo -0.3%, HK -1.9%, China -1.3%) and minor Asian (Korea -3.2%, Taiwan -0.3%, Indonesia -1.9%, Australia -0.2%) markets all lower in the session. Clearly, rising oil prices continue to weigh heavily on every nation in Asia as they are the primary recipient of Middle East oil and, as oil prices rise once again, it hurts all those nations. I assure you that as much as we dislike rising gasoline prices, it is nothing compared to what those nations are feeling.

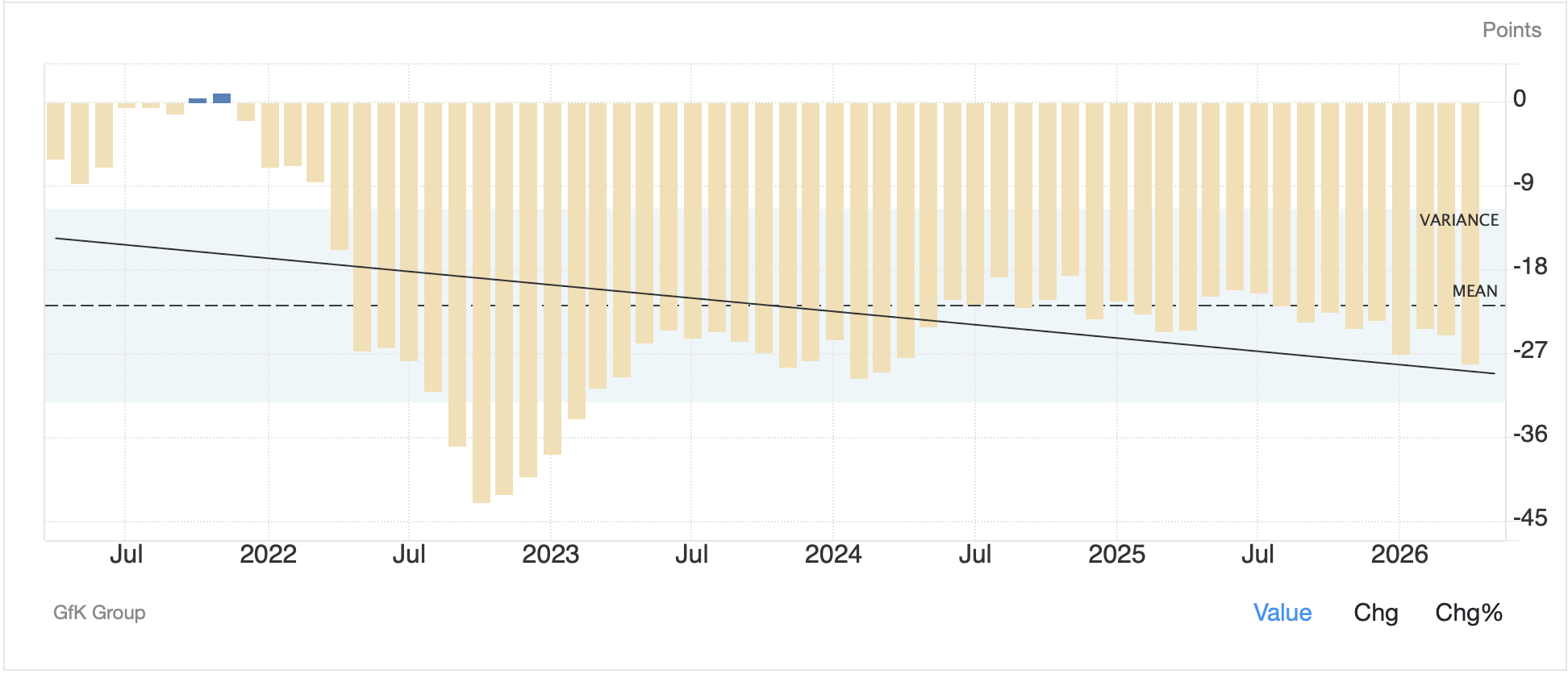

Europe, too, is lower across the board this morning led by Germany (-1.4%) which is not only suffering from general risk-off sentiment but has the added disincentive of declining consumer confidence as measured by the GfK indicator falling to -28.0, its lowest level in two years. a quick peak at the chart of this indicator shows that while things have rebounded since the darkest days of the 2022 inflation problems, the downward trend is strengthening again.

Source: tradingeconomics.com

But the rest of European bourses are also under pressure with the UK (-1.1%), France (-0.9%), Spain (-0.9%) and Italy (-1.1%) all falling sharply.

As has been the case on days like this, bond prices are under pressure as well, with yields correspondingly rising. So, after a 6bps decline in the 10-year Treasury yield yesterday this morning it has backed up by 4bps. As to European sovereign yields, the picture is quite ugly as you can see in the below Bloomberg screenshot.

‘Nuff said.

Which takes us to the driving force in all markets these days, oil (+2.6%) which is rebounding with WTI back above $90/bbl and Brent above $100/bbl. The one consistent thing I have seen on X this morning is that the propagandists on both sides seem to be preparing for a final outcome soon. Whether it is the idea that the US is going to run away with its tail between its legs, or the Iranians are going to collapse, the timeline definitely seems to be shortening. Hence my view that this will not be ongoing very much longer.

Turning to precious metals, as has been the case for the entire war, with oil rising, both gold (-2.0%) and silver (-4.2%) are under pressure. I must admit the consistency with which this price action holds; oil up, gold down, is somewhat baffling to me. My initial thesis was that we were seeing central banks liquidate gold to help pay bills, but why would they only do that on days when oil rose? Something else is going on here and I have not yet been able to figure it out. I do not believe that gold, after 5000 years as the safest of moneys, has suddenly lost that mojo. I also know that the premium for physical metal in Shanghai remains substantial. With this in mind, it is not hard to conclude that the futures market, where the price action is most visible, has seen a great deal of manipulation by someone trying to keep prices low, although to what end I cannot tell. We need to watch closely.

Finally, the dollar, as has been its wont, is higher this morning alongside oil, albeit not dramatically so. There are still numerous analysts who are calling for the dollar to decline sharply going forward, once the war premium is gone, but then they have been expecting that for a year and have not been able to explain its stability since early last year.

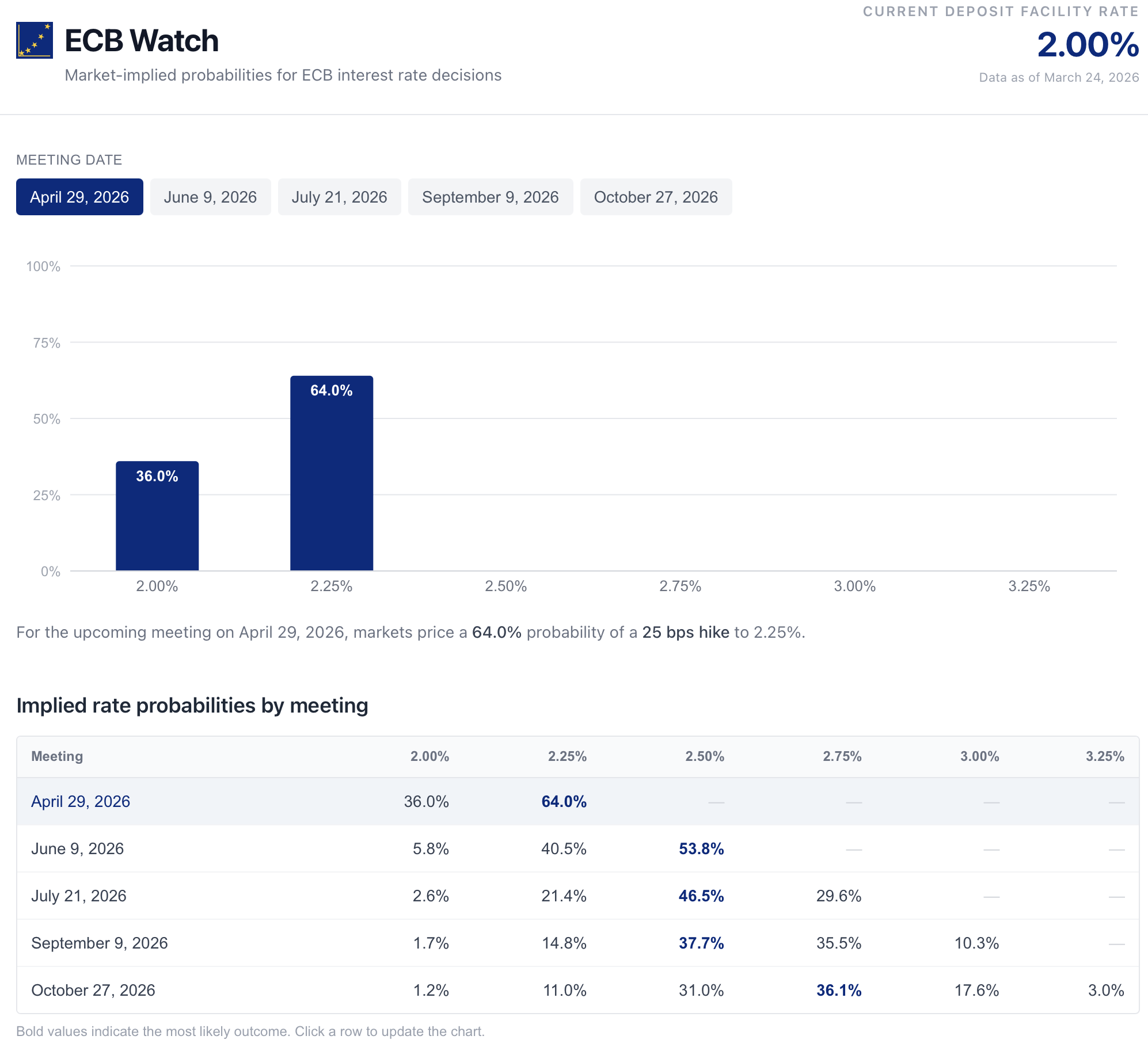

Like the CME’s futures page, the ECB publishes its own market-implied probabilities for the deposit rate there as per the below from ecb-watch.eu

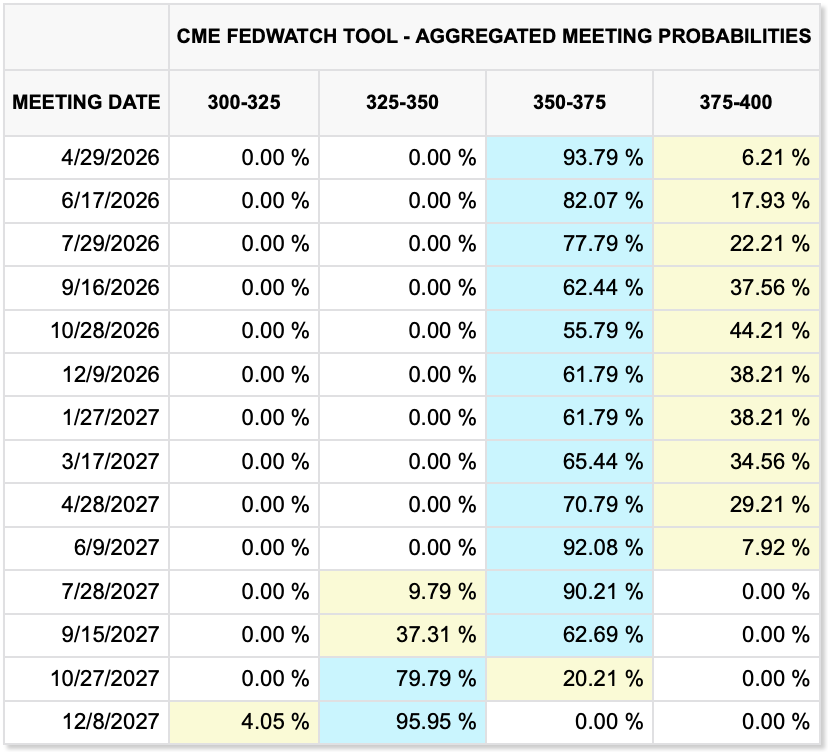

Now, I grant that if I look at the table at the bottom of the screenshot and compare it to the CME futures probabilities below, the market is pricing in more rate hikes in Europe than the US.

But I can never get over the actual interest rate involved as an important part of the interest rate parity decision process and mechanics. Sure, if the ECB hikes 50bps over the next three months and the Fed only hikes 25bps, that is a marginal advantage to the euro but owning euros after that is still a negative carry trade. Ultimately, the question is exactly how aggressively will central banks around the world address the initial bout of higher inflation that is coming alongside the higher oil prices. In truth, I think the US has far more leeway to raise rates as the underlying economy is in far better shape than that of the Eurozone, but as we heard yesterday, Madame Lagarde will not be “paralyzed” by events, i.e. she will hike rates if someone whispers in her ear to do so. I sincerely hope none of the central banks go down that road.

Elsewhere in the FX world, it is worth noting that USDJPY is pushing back toward the 160 level, although is unchanged this morning. As to today’s trading, NOK (+0.5%) is the big winner on oil’s strength, with BRL (+0.2%) the only other currency showing strength vs. the greenback. Otherwise, modest weakness (GBP -0.1%, AUD -0.2%, CNY -0.25, MXN -0.2%, ZAR -0.4%) is the order of the day.

On the data front, yesterday had some surprising outcomes with the Current Account ($-190.7B) falling to its lowest deficit in five years. meanwhile, oil inventories showed a much large build of crude and even distillates, while only gasoline saw an inventory draw. Perhaps that helped yesterday’s oil price decline. This morning, Initial (exp 210K) and Continuing (1850K) Claims are on the docket and that’s really it. There was an interesting article in the WSJ this morning describing how many cities are actually shrinking because of the change in immigration patterns we have seen since the border was closed. The importance of this is that old expectations of how much job growth defines economic strength need to adjust to the new population realities and frankly, nobody knows the adjustments yet. But the old idea that we need to see 200K new jobs each month seems to way overstate how to stabilize the Unemployment Rate.

And that’s really it. Today is a risk-off session and likely to remain so unless we get a new headline about a potential end to the conflict. But based on the recent pattern, tomorrow seems just as likely to be a risk-on session, although with the weekend coming, and the propensity for military action to start on the weekend, perhaps not. As to the dollar, it ain’t dead yet!

Good luck

Adf