The current conclusion to draw

Which could be a huge, fatal flaw

Is war’s not deciding

For traders in guiding

Positions, as few hem and haw

But right now, a deadline draws near

Which ought, by all rights, instill fear

The war’s escalation

Will lead to stagflation

With outcomes in stocks quite severe

As I type some 14 hours from the latest Trumpian deadline for Iran to reopen the Strait of Hormuz or have their electricity and transportation infrastructure destroyed, investors appear to be quite sanguine about the entire process. It seems very clear to me that market participants are quite certain the President will back away from this threat and extend the deadline or announce some other outcome. That is the only conclusion I can draw from the fact that equity markets around the world are consistently higher this morning. Investors clearly perceive this as an empty threat, which tells me that the pain trade is a sharp decline in equity markets if the US and Israel do destroy Iranian infrastructure. I guess we shall all learn more sometime this evening in NY.

But that is the backdrop for markets this morning. As I freely admit I do not know what the outcome will be, there is little point in hashing out the issue here. However, I cannot help but laugh at this clip as a description of the President’s negotiating style.

Moving on, in brighter news, the 4 astronauts have circled the far side of the moon, setting the record for the furthest any humans have been from Earth, and are now starting their return trip after having sent some remarkable imagery of the moon.

In truth, though, there’s little else to discuss so let’s look at markets. Yesterday’s session in the US continued the rebound in share prices from the recent nadir on March 30th. Since then, it has been four consecutive up days although futures this morning are little changed to very slightly lower. But the US move has been mirrored around the world with essentially all of Asia and Europe back at it today.

In Asia, while both Japan and China were essentially flat, Korea (+0.8%), India (+0.7%), Taiwan (+2.0%, catching up because it had been closed longer) and Australia (+1.7%) all had strong sessions. Hong Kong (-0.7%) did slip, as did several of the other smaller regional exchanges, but the mood was pretty bright.

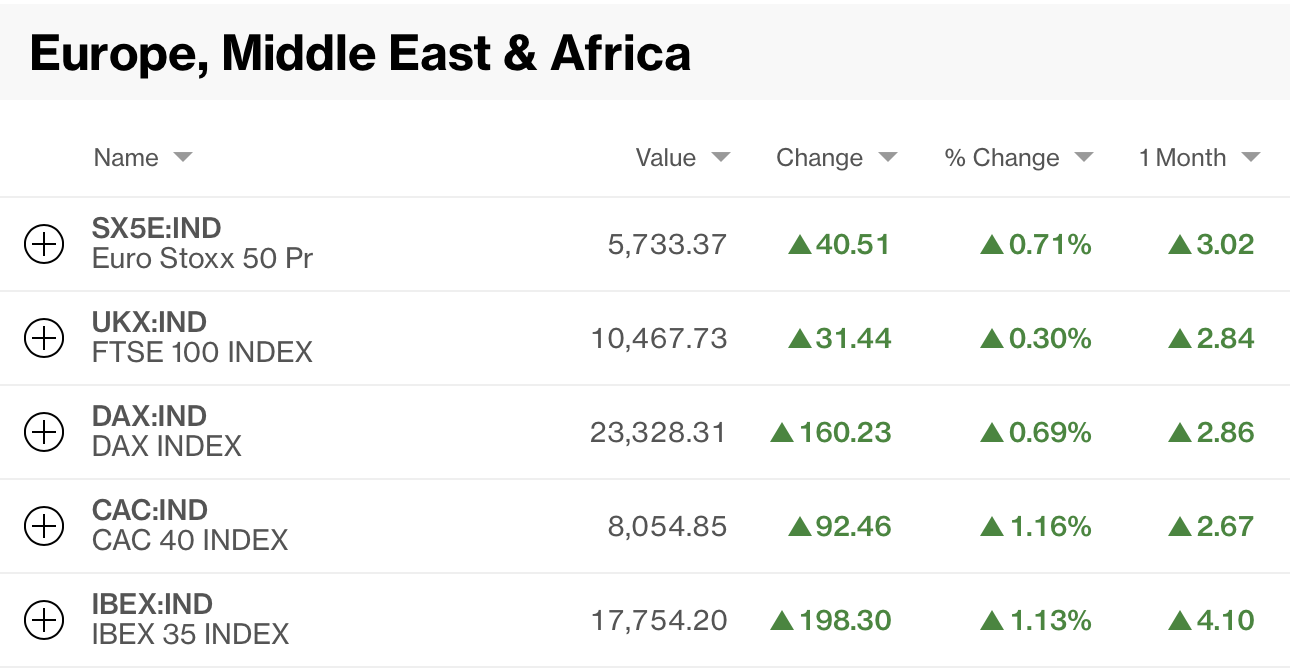

In Europe, I’ll let the following Bloomberg screenshot do the talking, but you can clearly see that fear is not on the menu right now.

In the bond market, Treasury yields are higher by 1bp this morning after a flat session yesterday while European sovereign yields have all risen about 3bps as they catch up from their long weekend with no trading. JGB yields are unchanged this morning as their long, slow climb takes a day of rest.

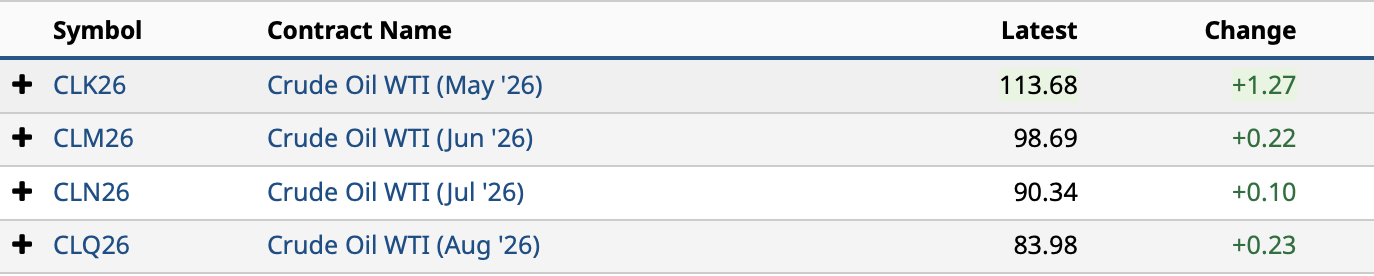

In the commodity space, I first must correct an error I have made regarding the relative prices of WTI and Brent. My go to source for oil pricing has been tradingeconomics.com. Their methodology shows the front month of the futures contract, but they don’t list the month in question. Due to the nature of the two different markets, currently, WTI’s front month is May while Brent’s front month is June. Given the steep backwardation in the oil markets, that difference is enough to explain the anomaly that I had seen. Below I have screen shots from barchart.com of the front contracts of both WTI and Brent and you can see the difference yourself.

If you look at the corresponding month in both contracts, you can see that Brent is consistently higher than WTI. (h/t Victor Adair, thank you Victor).

With that in mind, you can see that oil prices are a touch higher this morning, although they remain below the spike high seen at the beginning of the war. The chart below of WTI is certainly ominous with respect to the strength of the trend higher, and I must believe that if the US does take out Iranian infrastructure, we will breech the spike high on the chart and go higher still.

Source: tradingeconomics.com

Turning to the metals markets, this is perhaps the least surprising headline one can imagine from Bloomberg:

China Ramps Up Gold Buying as Middle East War Dents Prices

With gold prices having fallen nearly 18% from their peak back in late January, and China continuing to diversify reserves out of USD directly, they saw this as a great buying opportunity. This morning, the barbarous relic is little changed, although continues to trade lightly well above its spike lows. Silver (-0.9%) is also doing little and it appears that commodity traders are a bit more uncertain how to move forward with the Trump ultimatum hanging over the Iranian’s heads.

Finally, as we might expect given the willingness for investors and traders to add to equity positions, the dollar is slipping a bit this morning, although as I type at 7:00, it has recouped most of its overnight declines. Thus, the DXY is trading right at 100.00, the euro and pound have edged higher by just 0.1% and USDJPY continues to hover just below the 160 level, having touched it once on March 30, but not since. The biggest mover today has been SEK (-0.8

%) which has fallen on the back of softer than expected inflation data which has encouraged traders to believe the Riksbank will be able to cut rates ahead of other central banks in the event economic activity slows sharply. There is also a lot of discussion regarding INR (-0.3%) as the RBI has instituted policies restricting the size of short rupee positions local banks are allowed to maintain and forcing a lot of rupee buying to close those positions. Thus, the rupee remains caught between the forced position closures and concerns about oil prices depending on how things evolve in Iran.

Source: tradingeconomics.com

The one other currency move of note has been KRW (+0.6%) which continues to rebound from its worst levels seen on March 30th, as it is trading far more in line with the equity markets than the oil markets. If things escalate in Iran, I suspect the won is going to suffer greatly.

On the data front, this morning brings only Durable Goods orders (exp -0.5%, +0.5% -ex Transport) and speeches from two Fed members, Governor Jefferson and Chicago Fed president Goolsbee. Services PMI data was released throughout Europe this morning and it was broadly weaker than forecast (Italy, Germany, UK) although both France and Spain managed slightly better outcomes.

While I remain cautious and hedged personally, apparently my views are out of vogue. However, it strikes me that today will see little in the way of large movement ahead of the deadline, unless, of course, the president changes something before then.

Good luck

Adf