The first thing we saw yesterday

Was ADP led to dismay

But Treasury news

Adjusted some views

And stocks started trading okay

However, t’were two things we learned

First NYCB stock was spurned

Now, you may recall

That their greatest haul

Was Signature Bank, which was burned

And lastly Chair Powell, at two

Explained what he’s likely to do

They’re not cutting rates

As both their mandates

Remain far ahead in their view

Just when you thought it was safe to go back in the water…

I am old enough to remember when there was a growing certainty that not only was the Fed virtually guaranteed to cut rates by the May meeting, but the March meeting was very much on the table. After all, inflation was below their 2.0% target (if you look at the recent 6-month run rate anyway) and therefore they just had to cut rates or stock prices might fall! Or something like that. But somehow, Jay and the FOMC missed that memo. Instead, what they told us was [my emphasis];

“The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee judges that the risks to achieving its employment and inflation goals are moving into better balance. The economic outlook is uncertain, and the Committee remains highly attentive to inflation risks.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent. In considering any adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.”

In other words, while it is highly unlikely that they will need to hike rates further, unlike the markets or the punditry, Powell has little confidence that they have won the inflation battle and rate cuts remain merely a distant prospect. Certainly, there was no obvious concern that interest rates are “too” high at this time. In other words, this was a much more hawkish statement, and Powell’s answers in the press conference were in exactly the same vein. Memories of the dovish December meeting have faded from view. And this was the denouement to quite a day, one which gave us so much new information.

Things started with a weaker than expected ADP Employment result, just 107K, although that data point’s correlation to NFP has been diminishing of late. Regardless, it was the type of softness that got people primed for a dovish Fed. Then, the QRA indicated that the Treasury will be issuing what appears to be about $45-$50 billion in new coupons this quarter to fund a $400 billion or $500 billion budget deficit. The balance of that will be via T-bills which means that while the ratio is not as aggressively leaning toward T-bills as last quarter, it is still miles above the historical rate of 20% ish. Those two stories got bond bulls hyped, although equity markets struggled on some weak earnings numbers.

And then we heard from New York Community Bank (NYCB), which you may recall, was the lucky recipient of the Signature Bank assets last March. Well, it turns out they made a hash of things, losing a bunch of money with some pretty bad loan impairments added on to increased capital requirements because they grew to a new, larger risk-weighting tier after the acquisition. At this time, there is no indication they are about to go bust, but the question has been asked a lot as the stock cratered and investors ran into Treasury debt just to be safe. As it happens, the stock, which had basically doubled over the past year after buying Signature, has reverted to its pre-acquisition price and that added jitters to everyone’s views. PS, those loan impairments were CRE based which naturally leads to the question of what is going on with other regional banks.

Finally, during the press conference, Chairman Powell was clear that a March rate cut was highly unlikely and that was the final nail in the equity market’s coffin. So, the NASDAQ led the way lower, falling -2.2% while the S&P 500 tumbled -1.6%. At the same time, 10-year yields dropped like a stone, down 12bps to 3.91%.

Looking ahead, I wonder how all those folks who were certain the Fed HAD to cut because policy was just TOO TIGHT for their liking will reframe their narrative. To my eye, yesterday’s equity declines are a blip and will not even register at the Eccles Building. There is a bit of irony in that the doves need now eat so much crow.

Ok, on to this morning, where the overnight price action saw another mixed picture in Asia, but this time with Japan (Nikkei -0.75%) sliding while Chinese shares (Hang Seng +0.5%, CSI +0.1%) edging higher. There was yet another announcement of a bit of further fiscal support from the Chinese government, but Xi remains reluctant to bring out the bazookas. European shares are also mixed with gains in the UK and Spain and losses in France and Germany. PMI data showed that the Flash numbers were pretty much spot on and all of Europe remains well below 50.0 except Norway (50.7) which benefits from its oil industry. It remains very difficult to get excited about the Eurozone’s economic prospects these days which should ultimately weigh on the ECB to cut rates sooner and the euro to suffer in that case. As to US futures, after a wipeout yesterday, this morning they are firmer by about 0.5% at this hour (6:45).

In the bond market, after yesterday’s Treasury yield collapse, 10-year yields are higher by 3bps this morning and European sovereigns have risen about 4bps on average. This movement is more a response to the large move yesterday rather than a result of new information. Overnight, JGB yields slipped 4bps, clearly following in the footsteps of Treasury yields.

As to commodities, oil (+1.0%) has bounced after a weak session yesterday that was driven by demand worries. But tensions in the Middle East seem to be reasserting themselves with several stories in the press this morning regarding the danger to the world from a potential collapse in shipping capabilities. The ongoing Houthi attacks in the Red Sea are starting to really take their toll on supply chain situations. This is not only bad for inflation readings but could well impair the ultimate delivery of critical things like oil, thus driving its price even higher. As to the metals markets, they are all under pressure this morning with gold holding on best given its haven status but all the industrial metals lower by 1% or more.

Finally, the dollar is coming up roses this morning. While in the early going yesterday, before the FOMC meeting, the dollar broadly sold off on the softer ADP and dovish QRA, Powell changed everything, and the dollar reversed course in the middle of the day and rallied back nicely. This is true against virtually all its G10 and EMG counterparts. The weakest members are AUD (-0.7%) after weak housing data Down Under added to thoughts of a rate cut coming soon. As well, we see GBP (-0.4%) just ahead of the BOE meeting where expectations are for a more dovish statement although no policy change. But we are seeing weakness in CLP (-1.3%) on the back of that weak copper price and weakness in ZAR (-0.4%) on the weak metals complex as well. Given the hawkish tilt from Powell yesterday, unless there is a concerted effort by the Fed speakers that will be flooding the tape over the coming weeks to reverse that course, I suspect the dollar will benefit in the near-term.

On the data front, this morning brings Initial (exp 212K) and Continuing (1840K) Claims, Nonfarm Productivity (2.5%), Unit Labor Costs (1.6%) and ISM Manufacturing (47.0). With NFP tomorrow, I expect that the productivity and ULC data should be of the most interest as they will play most deeply into the Fed’s thinking. Improved productivity implies that there is less reason to cut interest rates as the “neutral rate” should be higher than previously thought. In fact, that dynamic would be very positive for the dollar, and interestingly, for the equity market as well as it would be a clear boost to earnings potential. We shall see how it turns out.

Good luck

Adf

Tag Archives: #riskoff

As Good As It Gets

Said Waller, I have no regrets

For things are “as good as it gets”

We’ve been quite outstanding

And reached that soft landing

Though rate cut forecasts won’t be met

Wow is all I can say. While Treasury Secretary Yellen was brasher last week by explicitly saying they have achieved the mythical soft landing, Governor Waller’s speech yesterday went into great detail about his work in 2022 on Beveridge curve analysis that almost perfectly forecast the current situation. I certainly hope he didn’t sprain his arm patting himself on the back. The certitude that has been coming from Fed speakers and their acolytes, like ex Fed economist @claudia_sahm, is remarkable to me. After literally a century of having no great insight into the workings of inflation, the Fed has now declared they have it under control because the past 6 months have seen price increases rise at a slowing pace.

Key Waller comments were as follows, “By late November, the latest economic data left me encouraged that there were signs of moderating economic activity in the fourth quarter, but inflation was still too high. As of today, the data has come in even better. Real gross domestic product (GDP) is expected to have grown between 1 and 2 percent in the fourth quarter, unemployment is still below 4 percent, and core personal consumption expenditure (PCE) inflation has been running close to 2 percent for the last 6 months. For a macroeconomist, this is almost as good as it gets.”

He finished with this comment, although interestingly, the market did not applaud, “As long as inflation doesn’t rebound and stay elevated, I believe the FOMC will be able to lower the target range for the federal funds rate this year. This view is consistent with the FOMC’s economic projections in December, in which the median projection was three 25-basis-point cuts in 2024.”

Maybe the Fed really has stuck the landing and inflation is going to smoothly slide back to 2% and stay there while the economy ticks over at 2%-3% GDP growth. Certainly, if the fiscal impulse continues to run at deficit levels of 8% of GDP, I would hope we could get 3% growth. But to my understanding of the way the economy responds to policy actions, that 8% deficit is going to find itself into rising prices across the economy. But then again, I’m just an FX guy.

In the end, the market heard Waller and decided that maybe higher for longer was still a thing. The Fed funds futures market reduced its probability of a March rate cut to 60% from 70% before the speech and the bond market sold off pretty hard with yields closing at 4.07%, their highest level since the day before that December FOMC meeting when everybody was certain that the Fed had pivoted. It seems the question now is, have they actually pivoted?

One of the problems they have is that the inflation data last month indicated the pace of price increases could be stabilizing around the 3.0%-3.5% level, rather than their target 2.0% level. We have very consistently heard from all the acolytes that if you annualize the past 3 or 6 months’ worth of data, the Y/Y rate is pushing to 2.0%. This, they claim, means the Fed has achieved their goal. The problem with this argument is that the Fed’s goal is not simply touching a 2.0% inflation rate, it is to maintain it at that level over time. That is a much more difficult landing to stick, and there is no evidence things will work out that way especially given we haven’t even reached a Y/Y rate of 2.0%!

Here’s another problem for that crew, inflation elsewhere in the world is not continuing its recent decline. Yesterday, Canadian CPI data showed that the trend numbers, Trimmed-Mean (3.7%) and Median (3.6%) were both higher than forecast and higher than last month. This morning, from the UK we learned that CPI rose 0.4% M/M, far more than expected with the Y/Y data rising to 4.0% headline and 5.1% core. In both these nations, the recent trend had been lower but has now reversed. While we have seen a significant rebalancing of markets and measured inflation has clearly fallen from its levels of the past two years, I would argue the evidence is scant that this trend is necessarily going to continue. Wage growth continues to hold up as employees try to catch up to the huge price increases since 2019. With the Unemployment Rate remaining near multi-decade lows, absent a major recession it appears it will be very difficult to continue to squeeze prices lower. And this doesn’t even consider the fact that increased tensions in the Middle East and the rerouting of ships around the Cape of Good Hope in South Africa, is adding weeks and costs to any movement of goods or oil, and could last for a considerable length of time.

We have consistently heard from ECB members that rate cuts are not coming soon. We have had a lot of pushback lately from FOMC members about the timing of any rate cuts with both sets of speakers explicitly saying the market is overexuberant in their current pricing. As I wrote yesterday, I think we are looking at a bimodal outcome, either virtually no rate cuts, or many more because we are in a recession. In either case, I think equity markets will need to reprice lower. However, the impact of these two situations will be different on the dollar, the bond market and commodities. We will discuss those outcomes tomorrow.

In the meantime, overnight was a sea of red (as opposed to the Red Sea) in equity markets with the Hang Seng (-3.7%) leading the way lower but weakness on the mainland as well (CSI -2.2%) and throughout the region. Japanese stocks (Nikkei -0.4%) were actually the leaders in the space. The China story was informed by their monthly data dump which showed GDP grew at a slightly weaker than forecast 5.2%, while IP (6.8%), Retail Sales (7.4%) and Fixed Asset Investment (3.0%) were all around expectations, but still soft overall and compared to last month. The Unemployment Rate there ticked higher to 5.1%, and they put out a new version of the youth unemployment rate at 14.9%, which they insist is a better measure than the old one which was screaming higher and was discontinued when it breached 21%.

European equity markets are also under pressure, mostly down about -1.0% on the continent and lower by -1.75% in the UK after the data releases. As to the US, after a lackluster session that was saved by a late day rally yesterday, futures this morning are lower by about -0.25% at 7:30.

In the bond market, after the large move yesterday, Treasury yields are unchanged on the day and European yields have edged up by about 1bp across the board with UK Gilts the exception, having jumped 10bps after the inflation readings. JGBs continue their lackluster activity and while they rose 2bps overnight, they remain below 0.60% overall. Again, slowing inflation there indicates little reason to believe they are going to change their monetary policy anytime soon.

On the commodity front, oil (-1.8%) is showing a lot more concern over demand destruction after the modestly weaker Chinese data than concern over supply issues from Middle East tensions. Plus, with US rates higher, commodity prices tend to suffer anyway. Gold, which got crushed yesterday amid the repricing of interest rates is unchanged this morning, licking its wounds while copper and aluminum trade either side of unchanged as the economic situation remains so uncertain right now.

Finally, the dollar remains king of all it sees this morning, rallying further after yesterday’s rally and now has retraced virtually all the weakness that came from Powell’s December “pivot”. This has been true in both the G10 and EMG blocs as the dollar is almost universally higher this morning. The one exception is the pound, which has managed a 0.35% rally on the back of the move in UK interest rates after the higher inflation data print this morning. The key to remember here is that despite a great deal of chatter about the dollar’s demise, the reality is that it has moved very little, net, over the past year and is far higher than where it was 5 years ago. If the Fed really is going to maintain higher for longer, which if inflation continues its rebound seems likely to me, then the dollar has to benefit.

Turning to the data, this morning we see Retail Sales (exp 0.4%, 0.2% ex autos), IP (0.0%) and Capacity Utilization (78.7%). In addition, we have three Fed speakers this morning and then this afternoon we get the Fed’s Beige Book and NY Fed president Williams speaks. Given what appears to be a change in tone from Waller, it will be interesting to see if the others follow his lead or push back. I have to believe that we are going to see more higher for longer talk and how it is premature to talk about rate cuts in March. If that is the case, the dollar should retain its recent strength and I expect risk assets to come under further pressure.

Good luck

Adf

Democracy’s Died

There once was a fellow named Trump

Whose plan was, Joe Biden, to dump

He started last night

By winning the fight

And heads to New Hampshire to stump

Political pundits worldwide

Now claim that democracy’s died

But markets don’t seem

In touch with that theme

Instead, interest rates are their guide

The Iowa caucus results can be no surprise to anyone as the polls were quite clearly in Donald Trump’s favor. In the end, he won with slightly more than 50% of the vote while Governor DeSantis came second, Ambassador Haley was in third and Vivek Ramaswamy was a weak fourth. Ramaswamy has now dropped out of the race and thrown his support behind Trump. Next week, is the New Hampshire primary and then two weeks later is the South Carolina primary. After that, comes Super Tuesday in early March, and quite frankly, it would be shocking, at this point, if Trump did not wrap up the nomination by then.

I only mention this because of all the elections this year, arguably the US presidential one is the most impactful on the world at large as well as financial markets. I will remind you of the equity market behavior in 2016 when Trump was elected the first time and as the evening progressed, the initial response was to see equity futures fall sharply as it became clearer that Trump was going to win, but by the time the markets opened in NY, they had completely reversed and rallied quite sharply, several percent. Ultimately, I would not be surprised to see more market impacts this year as well. It is one of the reasons that I believe the major theme this year is going to be more volatility across all markets than we have seen in the past several years combined.

However, right now, we are too early in the cycle and there has been no change of views or broad polling results, so investors are going to focus elsewhere, namely central bank actions. This brings us to the question of will the Fed actually be cutting interest rates six times in 2024, or more accurately, will they be reducing the Fed funds rate by 150bps? Funnily enough, I think that may be the least likely outcome of the array of possibilities that exist. Instead, I expect that the futures market is pricing in an almost binary outcome. On the one hand, the Fed remains true to their comments that inflation remains too high and while some cuts will come, it is very premature, so perhaps only one or two cuts this year.* On the other hand, the recessionistas are correct, a hard landing is coming and the Fed is going to have to cut by 300bps or 350bps to support the market. Play with these probabilities and it is pretty easy to come up with a scenario that shows 150bps of cuts this year.

But for now, whatever my views on how the Fed and other central banks are going to behave, the only important thing is what the market is anticipating. This takes us back to the market’s assumption about the Fed’s reaction function regarding all the data that is coming our way. Hence, the fact that the market largely ignored what appeared to be a hotter than expected CPI print last week, but jumped all over a softer than expected PPI print is telling in and of itself. The market is desperate for the Fed to cut rates which will open the doors for all the other central banks to cut rates.

And in truth, I think this is exactly what we should expect for the time being. The market is all-in on the idea that not only has the peak in inflation been seen, but that it is quickly falling back to the 2% target that is almost universal. And they are all-in on the idea that central banks will be able to lower rates back to much more comfortable levels for those in debt while supporting risk asset prices. My take is we will need to see a long series of data that indicates anything other than this scenario before market views change. So, any data that indicates inflation remains sticky will be ignored, while data that indicates it is falling sharply will be regurgitated constantly. The same will be true in the employment and production data. All I’m saying is we need to be prepared to see certain data that doesn’t fit the narrative get completely ignored for now. Manage your risk accordingly.

As to the overnight session, things have been less optimistic overall with most stock markets in Asia under pressure, even Japan (Nikkei -0.8%) and Hong Kong (-2.2%) really feeling pressure although mainland Chinese shares held in there after word that the Chinese government would be issuing an emergency CNY 1 trillion (~$139 billion) of debt to fund spending domestically. As to Europe, all red there, albeit only on the order of -0.4% across the board and US futures are also lower this morning, something around -0.25% at this hour (7:45).

In the bond market, after the US holiday prevented any changes of note yesterday, we see Treasury yields backing up 7bps this morning, a similar move to what we saw in Europe yesterday. Arguably, this seems like a catch-up move. In fact European sovereign yields are essentially unchanged on the day as German GDP data confirming the recession of 2023 did nothing to change views, nor surprisingly, did slightly better than expected UK employment data where wage growth was seen rising less rapidly than anticipated. JGB yields remain moribund and the idea that the BOJ is going to change anything seems a more and more distant prospect for now.

Oil prices (+0.6%) are a touch higher amid further threats from the Houthis as well as some missile attacks by Iran on areas in Iraq and Syria. I cannot keep up with all the different allegations here, but we cannot ignore the fact that things seem to be escalating. This cannot be a good outcome for oil prices, or perhaps more accurately, seems likely to push them higher. The higher interest rates are weighing on precious metals with gold and silver both lower, but surprisingly, copper and aluminum are both rallying this morning.

Finally, the dollar is flexing its muscles this morning, higher against all its counterparts in both the G10 and EMG spaces. AUD, NOK and SEK have all declined by -0.8% or so, leading the way in the G10 space, although -0.6% covers the bulk of the rest of the bloc. In the EMG space, KRW (-1.25%), PLN (-1.0%) and MXN (-1.0%) are the laggards across an entire bloc that is under pressure. This is all about the dollar this morning with no idiosyncratic stories to drive things.

On the data front, we only have the Empire State Manufacturing Index (exp -5.0) and we hear from Fed Governor Waller as well at 11:00. It seems to me that the market has really gone a bit too far in its bullish beliefs and today is a bit of a correction. Unless we start to see a lot more push back regarding policy ease though, I expect this movement will be short-lived. Although ultimately, I believe that we will see a weaker economy, higher inflation and weaker asset prices, I do not think that is the near-term view. Rather, I expect we will see more dip buying for risk assets by tomorrow at the latest.

Good luck

Adf

*I am well aware that the recent dot plot indicated a median expectation of 75bps of rate cuts this year, but do not forget that the dispersion of that grouping was quite wide, with one assuming no cuts and several assuming just one or two. I feel it is very weak thinking to say the Fed has indicated three rate cuts this year, they have done no such thing!

Some Shocks

While many still seek goldilocks

The problem is we’ve seen some shocks

Inflation won’t fall

And oil’s in thrall

To US and UK war hawks

But if we adhere to the data

It’s really not looking that great-a

For those who think Jay

Will soon lead the way

By cutting the Fed’s funding rate-a

We are back to being inundated with new information from both economic data and global events, both of which are driving markets for now. Interestingly, depending on the asset class, it seems that some are studiously ignoring what this new information means, at least what it has historically meant.

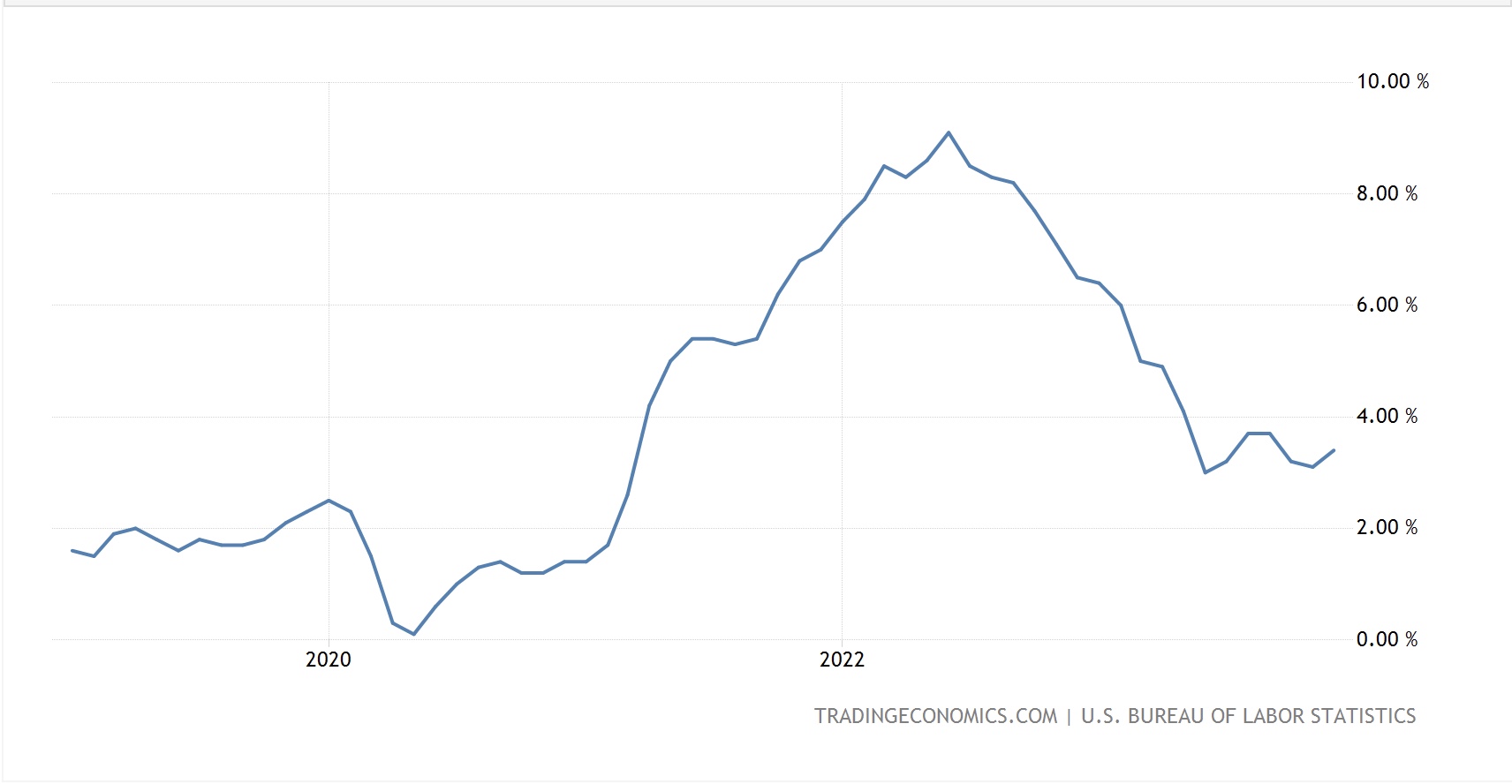

Let’s start with yesterday’s CPI data, which printed higher than forecast on both the headline (3.4%) and core (3.9%) measures. One needn’t be a market technician to look at the chart below of annualized CPI over the past five years and consider the possibility that the downtrend has ended, and we are reversing higher.

Source: tradingeconomics.com

To the extent that financial data has trends, and I think that is a very realistic estimate of how things work, the Fed may have a much tougher time squeezing the last 1.0% – 1.5% out of the inflationary process than many seem to believe. At least many in the bond market seem to believe that as despite the hotter than expected CPI data, bond yields actually declined yesterday. As well, there is no indication from the Fed funds futures market that they have changed their view on the number of rate cuts coming in 2024 with an even higher probability of a March cut, > 70% this morning, and still 6 cuts priced in for the entire year.

Regarding this seeming dichotomy, it is almost as if the market is trying to force the Fed’s hand. Historically, the Fed has tried not to ‘surprise’ markets when it comes to decisions, keeping a close eye on market pricing on the day of each meeting. As such, if the market is pricing in a cut or a hike, the Fed has been highly likely to follow through in the past. When there have been disagreements, the Fed will typically roll out lots of speakers to get their view across before the meeting in order to prevent that surprise on meeting day. As well, it is very clear that there is virtually no expectation of a rate adjustment at the FOMC meeting on January 31st, so perhaps the Fed doesn’t feel it is warranted to be that concerned yet. And of course, the data may turn in the direction of much softer inflation and even modestly worse employment so a cut will become the de facto norm. But my point is, the March 20th meeting is just 67 days away. For an economy whose trends move very slowly, it seems like the market may be a bit ahead of itself in this case.

We did hear from three Fed speakers yesterday, Mester, Barkin and Goolsbee, all of whom indicated that while the broad direction of things seemed pretty good, a rate cut in March is very premature. In fact, that has been the consistent theme from every Fed speaker and the market just doesn’t seem to care. We will see two PCE reports, two more CPI reports and two more NFP reports before the March FOMC meeting. And they will all be part of Q1 data, not Q4 data, so will at least have more relevance to the current situation. Maybe the market is correct, and inflation is going to turn back lower, and the first signs of economic weakness will convince Powell and friends it’s time to preemptively cut rates. However, even if that turns out to be the case, it is hard for me to see that as a > 70% probable outcome. Of course, I am just an FX poet, so maybe I just don’t get it.

The other topic that is making an impact is the Middle East. You may recall that oil prices had been on the soft side as the market saw weakening demand due to an impending recession with massive supply gains coming from better and better producer efficiency. In fact, I wrote about the latter this past Sunday in Oil’s Price is not Rising. However, all that efficiency is unimportant when compared to the escalation that we saw last evening in the Middle East, where US and UK forces attacked Houthi positions in Yemen in retaliation for the Houthi attacks on shipping in the Red Sea. This morning, oil is higher by 3.5% and since Monday, the rise has been 6.6%.

This poses several problems overall. First, of course, is the widening of the Middle East conflict being a problem in and of itself. The US military is already straining with its mission given the number of different places US troops are in harm’s way throughout the Middle East and Asia. The one thing we have learned throughout history is that war is inflationary. So, escalations in fighting will ultimately lead to escalations in prices of many things. Oil is merely the first casualty.

If you are Jay Powell whose current mission is to reduce inflationary pressures, a widening military conflict is not going to help the situation. In fact, it is likely that he will be called upon to support the military by ensuring the Treasury can issue as much debt as necessary at reasonable prices. This means the end of QT and a restarting of QE. If that were to be the case, and that is a big if, inflation would start another strong leg higher, and markets will be greatly impacted. Commodity prices will rise, the dollar will likely weaken, a bear steepening for bond yields would be in the cards and equity markets would rally, at least initially. But it would throw out any ideas of low inflation. I am not saying this is the current expectation, just that it is something that needs to be considered as events unfold going forward.

A quick look at the impact on markets today shows that equity markets are non-plussed by the escalation as yesterday’s benign US performance was followed by another rally in Japan although Chinese shares continue to lag after a big data dump showed economic activity there remains export oriented into a slowing global growth situation. Inflation remains moribund there, the Trade Surplus grew, and domestic funding continues to grow at a slower and slower pace. In Europe, though, there does not seem to be much concern as equity indices are all higher by about 0.5% although US futures are suffering a bit, -0.35%, at this hour (7:45).

In the bond market, Treasury yields are 3bps higher this morning than yesterday’s close, although they remain right at 4.00%, so are not really moving very much right now. Meanwhile, European sovereign yields, which closed before the US yields declined late, are all down about 3bps this morning, helped by confirmation that final inflation readings in Europe remained at recent lows. In the UK, the net data dump showed slightly weaker than forecast IP and GDP data which has helped drive the bid in Gilts. A quick JGB look, where yields fell 2bps, revolves around a story that the BOJ is going to reduce its end of year inflation forecast thus reducing the probability of any policy change anytime soon. This is one of the things helping the Nikkei and also a key driver of USDJPY higher.

Aside from oil prices rising, we are seeing gold (+1.0%) on the move today on the back of the Middle East escalation although the base metals are mixed. One other commodity note is uranium, a market which has been getting a lot more love lately given the recent acceptance by a portion of the eco community that its ability to generate electricity without producing CO2 is a net benefit. 40 nations have promised to increase their nuclear power use and demand for uranium has been rising amid a market where there is very limited supply and annual production does not meet current annual demand, let alone projected future demand. I simply wanted to highlight that there are price movements all over the place and while uranium may not be a major contribution to inflation, the fact that its price is rising so rapidly (100% in the past year) is not going to push inflation lower.

Finally, the dollar is firming up this morning as risk assets come under pressure. This is a typical war footing, where investors flee to the dollar in times of stress, just like they flee to gold. While the movement thus far has not been substantial, just 0.3% on average, it definitely has room to move further if things deteriorate in the Red Sea.

On the data front, we see PPI this morning, expected 0.9% headline, 2.0% ex food & energy, although given CPI was released yesterday, I doubt it will matter very much. As well, we hear from Minneapolis Fed president Kashkari, so it will be interesting to see if he has a different take than March is too soon, but things seem to be going well.

As we head into the weekend, the Middle East is the wild card. If things heat up, look for oil prices to continue to rise and risk to be discarded. That will probably help the bond market for now, and the dollar, but stocks will suffer.

Good luck and good weekend

Adf

Singin’ the Blues

Before Powell stepped to the mike The buyers of bonds went on strike Then Jay warned again Inflation is when Both prices and yields tend to spike Investors absorbed this new news, (The bond market fail and Jay’s cues) And offloaded risk In manner quite brisk So, that’s why we’re singin’ the blues

Remember when I explained that some weeks are just really slow? Just kidding! The remarkable thing about financial markets is one most always be alert to a shift in sentiment, even if it doesn’t make that much sense. However, yesterday’s shift made sense.

Last week when the QRA was published, the market took the news that a much larger percentage of issuance in the coming two quarters would be T-bills and not notes or bonds as a huge positive. We saw a significant rally in the bond market with 10-year Treasury yields falling nearly 50bps and we saw a corresponding rally in the equity markets as the major indices rose nearly 5%. Everybody was happy and the narrative was the worst was over for the risk asset correction. Oops!

This week has been the Treasury auction week, when they issue the newest tranches of 3yr, 10yr and 30yr notes and bonds. On Tuesday, the 3yr went fine. On Wednesday, the 10yr was acceptable, if a little weak, but given the broader narrative of positivity, it had limited impact. Alas, yesterday, the 30yr was an unmitigated disaster.

The two key statistics that are followed in this relatively arcane part of the markets are the tail (the difference between the final yield and the lowest bid accepted) and the bid-to-cover (BTC) ratio which describes the total amount of bids compared to the issue on offer. Typical tails are in the 0.5bp – 1.5bp range. Yesterday saw a 5.3bp tail, the largest ever, with the implication that they had to go through many bids to fill in the auction. The BTC yesterday was 2.24, far below the 2.38 average of the past ten auctions, and another indication that investors are not that interested in owning long duration Treasury paper. In fact, dealers (mostly banks) had to absorb almost 40% of the issue, double the usual amount. This is another indication that there aren’t many natural buyers of this paper right now.

In the wake of this auction, we saw bond yields rise sharply, up 11bps from the open, through the auction and then afterwards until the time that Chairman Powell spoke. Now, while Powell didn’t actually throw more gasoline on this fire, he certainly stoked it. Speaking at an IMF conference, he opened his comments with the following (emphasis added), “The Federal Open Market Committee (FOMC) is committed to achieving a stance of monetary policy that is sufficiently restrictive to bring inflation down to 2 percent over time; we are not confident that we have achieved such a stance.” A bit later he made sure to remind us, “If it becomes appropriate to tighten policy further, we will not hesitate to do so. We will keep at it until the job is done.”

Needless to say, risk assets did not perform well yesterday or overnight (US indices fell between -0.65% and -0.95%, Asian indices fell as much as -1.75% and European bourses are all lower by about -1.0% this morning) as investors dreams of rainbows and unicorns came crashing into the reality of the idea that interest rates are not going to be declining anytime soon. Not only is it unlikely that the Fed is going to reverse course, but yesterday was the first concrete indication that the cost of funding the US budget deficit may be starting to become a problem. (In fairness, it has been a problem all year and pointed out as such by numerous pundits, but yesterday the market, as a whole, seemed to get the message.) This is a major crimp in the narrative that just got developed last week.

Recall, the view that had come out of the Fed’s allegedly dovish stance and the weaker than expected NFP report was the Fed was done, inflation was going to fall, and yields would be heading lower across the curve. The unspoken part of that narrative was that there would be plenty of demand for Treasury paper because both investors and traders would be jumping in to get ahead of the decline in yields. Apparently, this feature of the narrative will need to be restructured, and with it, potentially, the entire narrative. This process is going to be the major market driver over the coming months and quarters. If the Fed maintains its higher for longer stance, and more importantly, continues along the QT path, shrinking its balance sheet, they will achieve the reduction in demand they currently seek to bring things into balance. Unfortunately, given the Fed’s inability to fine-tune this process, things have the chance to get very messy on the downside.

Summing up, the bullish narrative took a major hit yesterday and we will need to see a perfect combination of gently slowing economic data alongside quickly slowing inflation data to resurrect it. Personally, I would take the under on that bet. In fact, I fear that we could well see a much more rapid decline in economic data, with a recession on tap for early 2024 along with still sticky inflation keeping the Fed firmly wedged between that rock and that hard place. In this scenario, risk assets are very likely to underperform substantially. A key to watch will be the shape of the US yield curve. If (when) the bear steepening reasserts itself and long-term yields rise above the front end of the curve, you can be sure that a recession will be right around the corner. Sic semper erat, et sic semper erit. (Look it up)

Ok, well after that distressing discussion, a quick look at how other markets have behaved shows the following. Treasuries have edged lower by 2bps this morning, but that was after yesterday’s 14bp rally. European sovereigns, though, were closed when all the fun happened and so are catching up with yields higher by 6bps-7bps across the board. Not surprisingly, JGBs are little changed, but then there is no indication that the BOJ is going to stop QE anytime soon.

On the commodity front, oil (+1.5%) seems like it is finding a floor after its recent sharp decline, although given its inherent volatility (both literal and financial) I’m not confident the bottom is in. There has been much talk of significant speculative selling as a key driver of this move, but regardless of why, I would be wary of much signal from its price movement right now. Meanwhile, gold (-0.6%) which rallied sharply yesterday is in the process of giving it all back and base metals remain under general pressure.

Finally, the dollar is mixed this morning with both gainers and losers across the G10 and EMG blocs. In truth, the G10 movement has been quite limited, +/- 0.2% or less with one exception, NOK (+0.8%) which is benefitting from higher-than-expected CPI data and the belief that Norgesbank is going to be tighter going forward. In the EMG bloc, the movements have been a bit larger, 0.3% – 0.5%, but we are also seeing a mix of directions with, for example, MXN weaker while PLN is stronger. Net, I would say there is not much new here (the dollar did rally yesterday in the wake of the higher US yields) and I expect that traders will be happy to go home square this weekend.

On the data front, this morning brings the Michigan Consumer Sentiment (exp 63.7) and, remarkably, even more Fed speakers with Logan and Bostic on the calendar. At this point in time, I suspect that both traders and investors are going to be re-evaluating their medium- and long-term views on the progression of both economic activity and inflation. The bullishness of last week’s narrative has clearly been called into question. Arguably, we are going to need to see a lot more data to help convince market participants of the next trend. Next Tuesday starts with CPI data where a hot print will likely be seen quite negatively as it will push any Fed ease further into the future. But today does not seem like a session where much more will happen. In the end, as long as the Fed remains the most hawkish, and after yesterday I think that was reinforced, the dollar should find support.

Good luck and good weekend

Adf

Many More Pains

Reporting of real GDP Is what most investors will see But nominal data Is what could create a New narrative reality Combining both growth and inflation This number could be the foundation For further yield gains And many more pains Inflicted on stock adoration

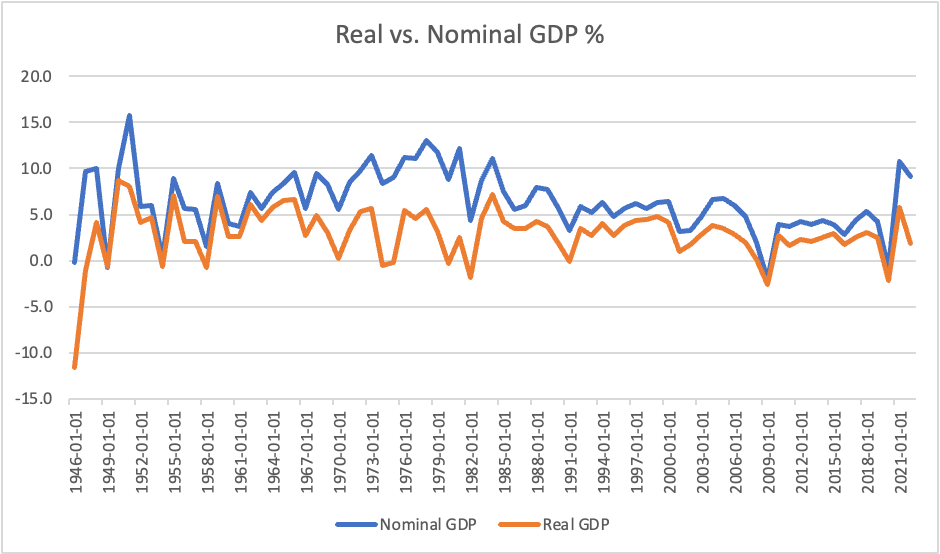

After another lousy day in the equity markets, today the first Q3 GDP data will be released. The current consensus forecast is for a 4.3% gain while the Atlanta Fed’s GDPNow number is up to 5.4%. And that’s the real GDP (rGDP) number, which removes inflation from the discussion. However, given all that is ongoing, it may be worthwhile to take a look at nominal GDP (nGDP), which is simply the change in total activity including price changes and economic output. As you can see from the below graph (data source, FRED database), in the post-WWII era, we’ve had 10 periods where rGDP fell below zero, better known as recessions, but only 3 periods where nGDP was negative, with the GFC in 2009 being the worst at -2.0%. The gap between the two lines is inflation, and you can also see how that has ebbed and flowed over time.

But turning to the current period, it is noteworthy that in the wake of the GFC, which was rightly called the worst financial crisis since the Great Depression and up through the Covid recession in 2020, nGDP had been pretty modest overall. In fact, a quick look at the data shows that the average nGDP during that decade was just 3.4%. This compares quite unfavorably with the long-term historical average of 6.4% since 1946. Looking at rGDP data, the average between the GFC and Covid was just 1.8%, again comparing quite unfavorably to the long-term growth of 2.9%.

The thing is, we have all gotten quite used to that economic environment of slow growth and low inflation and there are many professional investors, let alone non-investment professionals, who believe that is the way the world works. Well, let me tell you, that was the exception, not the rule. Instead, if you look at the very right side of the chart, you can see that both nGDP and rGDP have risen sharply in the wake of the Covid recession as the deluge of fiscal spending combined with, first supply chain constraints and now reshoring/deglobalization efforts, has changed the framework. In fact, I would contend that it is in the government’s best interest to continue down this path of high nominal growth and high inflation in order to try to outgrow the increase in debt. After all, if nGDP can grow faster than the fiscal deficit, the real value of US debt will ultimately decline. Of course, while it would be fantastic if the bulk of that high growth was a function of gains in productivity and high real growth, the FAR more likely outcome will be persistent high inflation.

What does this mean for markets? As we have seen over the past several sessions, equities can quickly come under pressure in this scenario, and I believe they have further to decline. While top-line revenues can continue to grow, the problem will come from a market that is going to derate the market multiple, especially in the tech sector, from its current nosebleed levels. High inflation will also continue to press on bond prices and the value of the long-term 60/40 portfolio is likely to continue to be eroded. In my view, the best place to hide will be in commodities as during inflationary periods, they tend to hold their value.

An anecdote from my early days in trading is that bond traders used to believe that the “natural” yield for 10-year Treasuries was right around nGDP. If yields rose above that level, bonds were probably a buy, and below that level, they would have a short bias. Nominal GDP for the past two years has been 10.7% in 2021 and 9.1% in 2022. On this basis, there is considerably further for bond prices to fall and yields to rise. Something to keep in mind as the talking heads work to convince you to catch the falling knife that is the bond market.

Ok, so how have things behaved ahead of today’s data, and ahead of the ECB’s rate decision this morning? Equity markets around the world have been under pressure with the Nikkei (-2.1%) leading the way as most regional markets fell sharply, notably in South Korea and Taiwan, although Chinese shares held their own on the back of still more stimulus promised by the government there. It is clear that President Xi is growing increasingly worried about the financial situation at home. In Europe, we are also seeing weakness, with red across the screen on the order of -1.0% or more and US futures are also pointing lower at this hour (7:30) down by -0.75% or so across the board.

Bond markets are little changed this morning with most seeing yields creep very slightly higher, maybe 1bp or so, but that is after another bond sell-off yesterday which saw Treasury yields continue their rebound from Monday’s sharp drop. As I type, we are back at 4.97% on the 10-year and the curve inversion is down to -15bps. As an FYI, the 2yr-30yr curve is back to flat now and I expect it is only a matter of days before the 2yr-10yr is there as well. Yesterday’s 5yr auction was particularly poorly received with a very wide tail and concern is growing that will be the case for all coupon auctions going forward. Yields are heading higher folks.

Oil prices are falling this morning, down -1.8%, which has basically reversed yesterday’s rally. EIA data showed inventory builds and it seems the longer Israel holds off on its ground invasion of Gaza, the more people are willing to believe that there will be no escalation. However, gold prices continue to rally, up another 0.4% this morning and getting ever closer to the $2000/oz level. Meanwhile, this morning, ahead of the GDP data, both copper and aluminum are in good spirits and rising.

Finally, the dollar is clearly back in the ascendancy with USDJPY finally breaking through that 150.00 level with no sign of intervention yet, while the euro is pressing back toward 1.05 and the pound is below 1.21. We are seeing strength across the board for the greenback, against both G10 and EMG currencies as the yield story continues to be the driver. As to the ECB today, expectations are for no change in policy, and the real question will be whether Madame Lagarde can maintain a hawkish bias, or if the obvious weakening in the data will reveal her inherent dovishness. If it is the latter, look for the euro to break below 1.05 before tomorrow’s close.

In addition to the rGDP data (exp 4.3%), we see Initial (208K) and Continuing (1740K) Claims as well as Durable Goods (1.7%, 0.2% ex transports). The ECB Press conference starts at 8:45 and will be carefully watched. Yesterday’s New Home Sales data was much stronger than expected and the BOC left rates on hold with a hawkish commentary, although the CAD was unable to gain much in the wake. The world continues to point to higher yields to fight structural inflationary pressures. At the same time, the dollar will retain its status and remains in demand. While it may not rally that sharply, I see very little case for any substantive weakness in the near and medium term.

Good luck

Adf

Wrecked

There once was a Treasury note Whose yield every trader could quote Of late, its price dive To yields above five Has tongues wagging while bond bears gloat Now, looking ahead I expect This rise in yields could architect More problems worldwide As risk assets slide And equity markets get wrecked

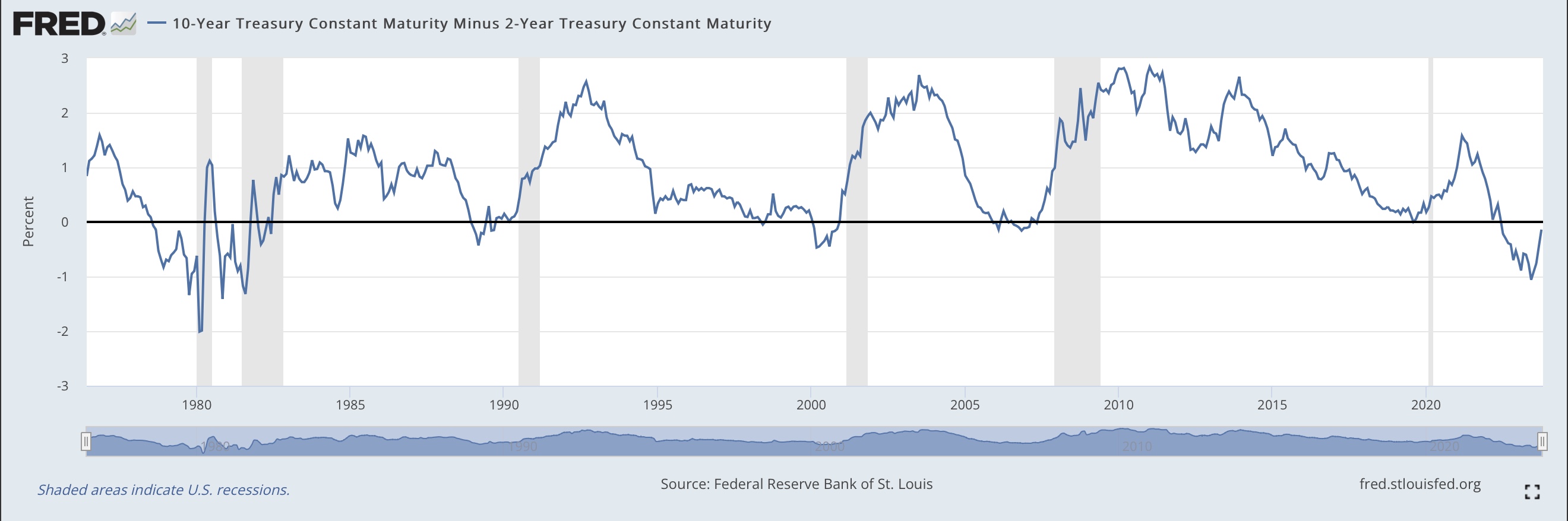

There is only one story in financial markets today, and that is the fact that the 10-year US Treasury note is now yielding above 5.0%. We briefly touched that level last Thursday, and then saw a pullback in yields on Friday, but today there is no question about a breach of that key psychological level. As a corollary to that price action, the 2yr-10yr spread is down to -12bps and looks quite clearly as though it is going to complete the normalization process this week. The real question is, how much further will it steepen? A quick look at the chart below from the St Louis Fed’s FRED database shows that the average steepness of this spread is somewhere around +100bps. The implication is that if the Fed continues to hold Fed funds at their current level, and higher for longer is the way forward, then 10-year Treasury yields could easily head to 6.00% and simply be back to their long-term relationship with the 2-year Treasury.

The other thing to note is why there is so much focus on the shape of the yield curve. As you can see from the shaded gray areas on this chart, every recession was preceded by a curve inversion (negative 2yr-10yr spread) but then when the recession was in process, the curve was steepening dramatically. It is this history that has economists and analysts concerned given the speed with which the curve is steepening of late.

And yet…two headlines in the WSJ this morning show a completely opposite expectation. “A Recession is no Longer the Consensus” is one of them, explaining a survey of economists now shows that fewer than half anticipate a recession will arrive at all, let alone soon. In addition, we have “The Economy was Supposed to Slow by Now. Instead it’s Revving Up” which describes the fact that recent data has been firmer than expected (see Retail Sales and NFP earlier this month) and now the proverbial soft landing is the new consensus call.

Now, maybe this time really will be different, but that is always a hard pill to swallow. There are many things that continue to haunt the economy with respect to things like bank lending standards tightening and consumer debt and delinquencies rising, neither a sign of economic strength. In fact, there was a terrific note published this weekend on Substack by GrahamsBenjamins going into more detail. The point is that there is a significant amount of economic stress in the economy and that combined with the rapid steepening of the yield curve has always been a sign of a looming recession. And folks, if (when?) that recession arrives, you can be confident that risk assets are going to decline sharply in value. Just sayin!

Ok, with that cheery opening, let’s see how markets have behaved overnight. Following last week’s lousy price action in the US, Asian shares were lower across the board, somewhere between -0.75% and -1.0% while European bourses are also lower, perhaps a little less dramatically, with an average decline on the order of -0.5%. US futures, too, are in the red, -0.6% or so at this hour (7:15), and not feeling very good.

Meanwhile, we already know the Treasury story, but it is important to understand that European sovereign yields are also rising rapidly, with most of them higher between 4bps and 6bps this morning. That critical Bund-BTP spread continues to trade just north of 200bps and holds the potential to be quite destabilizing if it widens much further. As well, we saw JGB yields creep up 2bps and are now at 0.85%. Inflation in Japan has been above 3.0% for the past 14 months, and more and more analysts are concluding the BOJ is going to have to tweak their policy yet again. There is far more to the bond market than just Treasuries, although Treasuries are clearly still story number one.

On the commodity front, oil (-0.6%) is a bit softer this morning although this seems a consolidation of last week’s strength. The biggest question in this market is the tension between the possible recession and a corresponding reduction in demand, and the structural supply shortages that are currently being exacerbated by the Saudi and Russian production cuts. My money is still on higher prices over time. Meanwhile, gold is little changed this morning, holding up quite well in the face of rising yields and seeming to be showcasing its haven status of late. As to the base metals, both copper and aluminum continue to grind lower with copper having fallen to its lowest level in a year and seemingly an indication of economic weakness to come.

Finally, the dollar is mixed to slightly softer this morning although slightly is the operative word. Looking across the G10 currencies, the Skandies are under a bit of pressure, but the majors are essentially unchanged. The real news is that the correlation between the dollar and Treasury yields seems to be disintegrating. If that is changing, then there are certainly many reasons to believe the dollar can decline given the US fiscal situation and the continuous growth in the US debt portfolio. As is often said, nothing matters until it matters. Throughout my entire career, spanning > 40 years, there has been a constant drumbeat of how the dollar should decline because of the massive budget and trade deficits that the US has run consistently. And that drumbeat has been studiously ignored for all that time. But perhaps, it will soon matter. While that is not my base forecast, one has to assign that outcome some real probability.

On the data front this week, this is what we see:

| Today | Chicago Fed National Activity | -0.16 |

| Tuesday | Flash PMI Manufacturing | 49.5 |

| Flash PMI Services | 49.9 | |

| Wednesday | New Home Sales | 680K |

| Thursday | Initial Claims | 209K |

| Continuing Claims | 1720K | |

| Durable Goods | 1.5% | |

| -ex Transport | 0.2% | |

| GDP Q3 | 4.2% | |

| Friday | Personal income | 0.4% |

| Personal Spending | 0.5% | |

| Core PCE | 0.3% (3.7% Y/Y) | |

| Michigan Sentiment | 63.0 |

Source: Tradingeconomics.com

Weirdly, while the Fed is supposed to be in its quiet period, I see three speeches scheduled, with Chairman Powell ostensibly speaking Wednesday afternoon. I will need to confirm that as it would be highly unusual at this time.

It seems to me the big question is whether the dollar – rates correlation is breaking down. If that is the case, then I will need to rethink, and likely adjust, my views of a stronger dollar over time, at least vs. the majors. But tick by tick price action is not necessary for the relationship to generally hold. I still like the dollar over time but am certainly going to review the situation more closely to see if something truly has changed.

Good luck

Adf

Dim-Witted

Said Jay, though we’re strongly committed To make sure no ‘flation’s permitted Quite frankly we’re lost And ‘fraid of the cost If we screw up cause we’re dim-witted So, we’ll watch the data releases And act if inflation increases But if it should fall Then it will forestall More hiking lest we step in feces

As expected, the Powell comments were yesterday’s highlights as he once again explained that the goal of 2% inflation remains their primary effort. Not surprisingly, given what we have heard from the onslaught of Fed speakers over the past two weeks, he made clear that there will be no rate hike at the November meeting, but December is still in play. When asked about the rise in long-term yields, he did indicate it could be doing some of the Fed’s work for them, just like we heard earlier this week from Lorrie Logan and others. Somewhat surprisingly, he mentioned the rising budget deficits, describing them as on an “unsustainable” path. Now, we all know this is true, but Powell has been extremely careful not to discuss government funding throughout his tenure as Chair. I suspect his next testimony to Congress could be a little spicier!

Of course, the other six speakers added exactly nothing to the conversation as they merely reiterated in their own words the same message. Perhaps of more interest was that despite effective confirmation that there was no hike upcoming and that the bar for a December rate hike was quite high, bonds continued to sell off with the 10yr yield closing at 5.0% while stocks took it on the chin again. Methinks there is more than a little concern starting to grow amongst asset managers that the concept of the Fed put may finally be gone.

The other really interesting outcome yesterday was the fact that gold rallied another 1.3% despite the ongoing rise in interest rates. As there was no new news out of the Middle East of any real note, one possible explanation is that investors are simply getting quite scared overall.

One thing is quite certain and that is if the situation changes such that Powell and company become concerned that the economy is reversing course and they have, in fact, overtightened monetary policy, any reversal of the current message is likely to lead to some very big moves. In that case I would expect a much weaker dollar, a huge rally in gold and other commodities, an initial rally in equities and, remarkably, not much movement in bonds. I remain of the strong belief that the supply issue is the key bond market driver, so that will only increase in the event of an economic slowdown and that cannot help the bond market, even if the Fed starts to buy them again. But that is all hypothetical.

Turning to the overnight session, while risk continues to be shed in Asia and Europe, we did see Japanese inflation data where the headline rate declined to 3.0% and the core to 2.8% although their super core reading is still at 4.2%. Certainly, Ueda-san must be pleased that the numbers are beginning to edge a bit lower although they remain far above the 2% target. Of course, the very fact that they are edging lower implies that any end to QQE is even further in the future. Recall, Ueda-san has been clear that he does not believe 2% inflation is yet sustainable in the economy and is concerned it is going to slip back below that level in the medium term. With that attitude, he has exactly zero incentive to end YCC or QQE and seems far more likely to continue with them.

The implication of this outcome is that the yen seems likely to weaken further. Currently, USDJPY is trading at 149.95 and although it hasn’t touched the 150 level since that first brush on October 3rd, it has been grinding ever so slowly back there again. This price action has all the earmarks of stealth intervention, something that may be carried out by the three Japanese mega banks at the BOJ’s behest. However, given the ongoing trajectory in US interest rates, it seems only a matter of time before we once again breech 150. It will be quite interesting to see the MOF/BOJ reaction at that time, although I suspect they will, at the very least, “check rates.” For hedgers, be careful here.

And really, that’s all we’ve got to talk about today. As mentioned above, equity markets fell in Asia overnight, with losses on the order of -0.5% or so and European bourses are all down about -1.0% this morning heading into the US open. As to US futures, at this hour (7:00) they are off about -0.4% as we head into an option expiration session. Thus far, earnings season has not been sufficient to excite investors and fear seems to be the driver of note.

Turning to the bond market, while we have backed off from yesterday’s closing highs of 5.0% by 5bps, we remain at multi-year highs and there is no reason to believe that we have seen the top in yields. In fact, this move appears to be driven by rising real yields, not inflation concerns. While real yields have already risen substantially over the past 6 months, rising from ~1.0% to the current 2.45%, history has shown that real yields can easily rise to 4% or more in the right circumstances, and these may just be those circumstance. Again, there is no evidence that Treasury yields have topped. As to European sovereigns this morning, they are edging lower by about -1bp after a large rally yesterday as well. US Treasury price action continues to be the global driver for now.

Oil prices (+1.5%) continue to trade higher as concerns over a widening of the Israeli-Palestinian conflict keep traders on edge. Combine this with the weaker production numbers from the US and the drawdown in inventories and you have the ingredients for a further price rally. News that a US Missile Cruiser in the Red Sea shot down several drones and missiles launched from Yemen cannot have helped sentiment. Meanwhile, gold (+0.4%, +2.6% this week) continues to play the role of safe haven. Either that or there is a lot of short-covering ongoing. The price is approaching $2000/oz, one of those big round numbers on which markets tend to focus so I would look for a test there if nothing else. However, base metals are softer this morning as the price action today is not economically related.

Finally, the dollar continues to tread water this morning with most of the major currencies within +/- 0.2% of yesterday’s closing levels while EMG currencies seem to be edging a bit lower, down on the order of -0.3%. The renminbi is little changed this morning despite (because of?) the PBOC injecting CNY733 billions of fresh liquidity into the market/economy there overnight. Again, just like the yen, the diametrically opposed monetary policy of China and the US should lead to further currency weakness here over time. Now, the PBOC doesn’t like to see sharp movement and will continue to prevent a blowout move, but the spot rate is currently trading right at its 2% band vs. the CFETS fixing, so something has got to give soon. In the end, the dollar trend remains intact, but I must admit I am surprised it is not a bit stronger given the underlying fear in the market.

On the data front, there are no statistics released and we hear from two more Fed speakers, Harker and Mester, to finish things off before the quiet period begins. It seems hard to believe that anything they say will be seen as more important than Powell’s comments yesterday. As such, looking at today’s market activity, while there will be tape-watching regarding the Middle East and any escalation in hostilities, I suspect the equity market will have the most influence on things. At this point, further weakness seems the most likely outcome, especially as traders will be reluctant to be overly long risk heading into the weekend.

Good luck and good weekend

Adf

Much More Afraid

Watanabe-san, A previous Mr Yen, “No intervention”

As USD/JPY approaches the psychological level of 150.00, there is a growing belief in the market that the BOJ is soon going to intervene. Recall, last week we heard about the urgency with which the MOF is watching the exchange rate. Historically, the next step would be for the BOJ to ‘check rates’. This is when they call around to the big Tokyo bank FX trading desks and ask for levels. The implication is they are ready to sell dollars and defend the yen.

However, unlike the previous decline in the yen almost exactly a year ago, the recent movement has been somewhat more gradual as can be seen in the chart below (source tradingeconomics.com)

This was highlighted last night by Hiroshi Watanabe, the deputy FinMin in charge of currency policy from 2004 through 2007. He explained that after seeing the dollar remain in a 145-150 range for much of the past year, “I don’t think authorities are worried about the outlook as much as they were last year. There’s no sense of imminence because the dollar/yen level hasn’t changed much from a year ago, and it doesn’t seem like the yen will start to plunge even if it breaches the 150 mark.”

As is often the case when it comes to concerns about a currency’s value, the pace of its decline is far more important than the actual level. Most countries, or at least most finance ministries, feel they can handle slow and steady. It is the abrupt collapses that scare them. This move has been quite steady, and as long as both the Fed and BOJ maintain their current monetary policies, a continuation seems likely. Hedgers, keep that in mind.

Now, turning to yesterday’s trade A message was clearly conveyed As interest rates rise Risk appetite dies And people are much more afraid

The most pressing story in markets continues to be the US Treasury market where sellers outnumber buyers on a daily basis. Yields on the 10-year rose 10bps yesterday, touching 4.70% and are continuing higher by another 2bps so far this morning. The bear steepener continues to be the story with the 2yr-10yr spread falling to -40bps and looking for all the world like it is going to go positive before the end of the year, if not the end of the month. And it makes sense. There is still substantial demand for short-term paper yielding more than 5% (yesterday’s 3mo T-Bill auction cleared at 5.35%). Meanwhile, we are seeing money flee those assets with long duration over fears that inflation has not yet been quelled and that the structural issues (ongoing massive supply meeting limited demand) has investors pulling back quickly. Not only are Treasury bonds being sold aggressively driving yields higher, but yesterday saw utility stocks, often seen as a duration proxy given the high amount of debt on their balance sheets, fall nearly 5%.

This activity is having the knock-on effects that one would expect as well. Yields around the world continue to get dragged higher by Treasuries, the dollar continues to benefit, and commodity prices are suffering. In fact, yesterday saw a sharp decline in the price of oil and it has now retraced more than 6% from the peak last week. I had written about the simultaneous rise in yields, the dollar and oil as being a HUGE problem for global markets. Well, it seems that oil is starting to feel the pain of higher yields and a stronger dollar. As well, tomorrow OPEC meets in Vienna and there is some talk that the Saudis may increase their production, unwinding those unilateral cuts made back in June and continued since then.

But make no mistake, ongoing rises in Treasury yields will continue to underpin the dollar and that will be enough of a problem for economies elsewhere even if oil prices slide some more. And right now, there is no indication things are going to change. Yesterday we heard from two Fed speakers, Governor Bowman and Cleveland Fed President Mester with both maintaining the hawkish views. In fact, Bowman expressed the need for several more rate hikes in order to get inflation under control and both were clear that higher for longer was crucial. As long as that remains the Fed attitude, until we see a substantial change in the data stream, yields are going to continue to rise.

Now, this week brings the all-important NFP report on Friday, which has been a key driver of Fed policy. With inflation readings continuing far above the Fed’s target, as long as NFP remains positive and the Unemployment Rate remains either side of 4%, the Fed will have no reason to reconsider the current policy mix. In their minds, they have not yet broken anything, at least not so badly that it couldn’t be fixed. I’m sure they are straining their arms as they pat themselves on the back for the effectiveness of the Bank Term Funding Program (BTFP) which was created after the bank failures in March. In fairness, it seems to be working for now. However, I will warn that cans can only be kicked down the road for so long, and I fear the end of that road is nearing.

As to the rest of the session today, risk is decidedly on the back foot. Those equity markets in Asia that were open all fell pretty sharply with the Nikkei (-1.6%) and Hang Seng (-2.7%) leading the way lower. The story is similar in Europe with the major indices all lower by about -0.75% or so as they respond to the ongoing increase in interest rates around the world. Finally, US futures are lower by -0.45% at this hour (7:30) with concerns growing that yields will not stop rising.

Looking at European sovereign bonds, yields there are rising alongside Treasury yields with most of them higher by 3bps-4bps and Italy higher by 9bps. That Bund-BTP spread, currently at 193bps, is something we need to watch as 200bps is likely to be the first place the ECB really shows concern and if it heads higher than that, expect more direct actions. As to JGB yields, they remain static at 0.76%.

We already discussed oil prices and we are seeing serious weakness across the entire metals complex lately, although today’s declines are relatively muted, on the order of -0.2%, as the moves have already been pretty large. The lesson from the recent price activity is that yields continue to drive the market.

Finally, the dollar remains king with the euro below 1.05, USDJPY just below 150 and the pound making a run at 1.20. Last night, the RBA met and left rates on hold, as widely expected, but the tone of new governor Michele Bullock’s first meeting was seen as somewhat dovish leading to a nearly 1% decline in the Aussie. At the same time, the EMG bloc of currencies is also coming under pressure with declines today on the order of -0.5% across all three regions. There is a term, the dollar wrecking ball, which is quite apt. As it continues to rise it puts intense pressure on countries around the world as they scramble to get dollars to service the trillions upon trillions of dollars of debt outstanding. Nothing has changed my view that this has further to run.

On the data front today, the only release is JOLTS Job Openings (exp 8.8M) a number that remains significantly larger than the number of unemployed. We also hear from Atlanta Fed president Bostic this morning so it will be interesting if he is willing to push back against the ongoing hawkishness.

I see no catalysts to change the current trend in the dollar, so for all you receivables hedgers out there, keep that in mind.

Good luck

Adf

Into the Abyss

In Washington, something's amiss As hardliners say with a hiss Let government close As we don’t oppose A tumble into the abyss The reason that markets might care Is data will then become rare Thus, how will the Fed Keep looking ahead If rear-facing data’s not there?

As this is not a political commentary, I generally try not to focus on these issues. However, periodically, they impact the economics and the markets so I must. As we approach the fiscal year-end for the US this Saturday, there are still a number of appropriation bills that have not passed Congress and been signed into law. Some of the hardliners in the Republican majority in the House seem to be willing to die on this particular hill, although as we are talking politics, and there are still two days left before it becomes a fait accompli, things are subject to change.

But the issue for markets has far less to do with the actuality of the government shutting down and entirely to do with the fact that the Bureau of Labor Statistics and Commerce Department, the source of most government data, will be shut down and so not be able to publish the monthly numbers. Given that the Fed has repeatedly told us that they are data dependent, on what will they base their decisions if there is no fresh data to help guide them?

The inherent problem with data dependence is that all the data published by the government is backward looking, reporting what happened in the past week/month/quarter, and the Fed uses its numerous econometric models to extrapolate how that will play out in the future. History shows us, though, that the Fed’s models, especially lately, have not been terribly accurate. Does anyone remember transitory inflation? (Every time I go to the grocery store and see the price of staple items it crosses my mind. How about you?) Thus, if I were to analogize their process, it is like driving a car forward while looking only in the rearview mirror and the steering mechanism doesn’t work properly.

At any rate, this story is going to dominate for a while. Chairman Powell speaks this afternoon at a townhall with educators and he will be taking questions from the audience. You can be sure that reporters will be there and there will be a question about how the Fed will handle the lack of data in the event of a shutdown. This is unlikely to dominate the market narrative quite yet, but if the shutdown does happen, Monday could see some impact. We shall see.

In the meantime, risk remains under pressure around the world as there are three current market features that are dissuading investors from jumping in, and in many cases pushing them to the sidelines.

First is the price of oil, which rose 4% yesterday and is basically unchanged this morning, retaining all of this gains. We are now back to levels not seen since July 2022 when oil was falling from the post Ukraine invasion spike while the Biden administration was flooding the market with SPR reserves. Given the SPR is back to levels last seen in 1983, shortly after it was initiated, it seems there is less room for the Administration to repeat this performance. At the same time, there has been no indication that OPEC+, and the Saudis specifically, are getting set to open the taps again. Rising oil prices impact everything as they are an excellent proxy for the price of energy writ large. And everything requires energy to keep going. If it costs more to keep the lights on or ship products, it is going to work its way into the price of retail items.

Second is US yields, which we proxy with the 10-year Treasury bond. This morning it is trading at 4.65%, continuing its recent move and, in truth, looking like it is accelerating it. Since the beginning of September, the 10-year yield is higher by 55bps, a very large move, and that is dragging yields higher around the world. For instance, German bunds, French OATs, and UK gilts are all trading at decade-plus high yields, and even worse for the ECB, Italian BTPs, are seeing their spread to bunds widen back toward 200bps. You may recall that in July 2022 the ECB created a program called the Transmission Protection Instrument (TPI) which was designed to essentially roll maturing bund positions from the ECB’s balance sheet into Italian BTPs to support that market and prevent the euro from exploding. Once that got going it was quite effective at moderating that spread, and things seemed fine. But recently, the Italian fiscal situation has become increasingly weakened and the market is pushing on this issue again. The point is the market is focusing on more risks and thus risk appetite is waning.

Finally, the dollar continues to rise. Using the Dollar Index (DXY) as a proxy, it is currently trading well above 106 and taken out much technical resistance. While it is a bit softer this morning, with the euro (+0.4%) and pound (+0.5%) both bouncing a bit along with the yen (+0.2%), this trend remains very clear. (see graph courtesy tradingeconomics.com)

In fact, last night USDJPY touched 149.70, a new high for the move and that triggered some further comments from Japanese FinMin Suzuki that indicated he was close to the next stage of intervention known as “checking rates”. This is the process by which the BOJ calls out to the big banks in Tokyo asking for a price in USDJPY but does not deal. However, the simple fact of asking for the price gets these banks to sell dollars for their own accounts and they then spread the word that the BOJ is “checking rates” which all in the market know is a sell signal. So, last night, when the dollar hit that high level, Suzuki was on the tape saying that might be the next step and the dollar fell back a bit.

Remember, though, intervention will only matter if it is concerted, with all the central banks, especially the Fed involved, and really only if monetary policies change. And it is the latter that seems the least likely right now. So, if when the dollar trades above 150 expect some fireworks, but unless there are other changes, it will be temporary. Hedgers, be prepared.

And that is the situation as we head into today’s session. There is a bunch of data coming this morning starting with Initial (exp 215K) and Continuing (1675K) Claims, as well as our third look at Q2 GDP (2.1%). In addition to Chair Powell this afternoon, we hear from Chicago Fed president Goolsbee this morning and Governor Cook early this afternoon. The most recent comments from both of them indicate that more rate hikes may well be necessary, and neither is in a hurry to cut rates.

Yesterday saw a pretty flat day in the equity markets in the US and futures this morning are also little changed. however, there is growing concern, as I outlined above, that risk is becoming riskier and that the safety of short-dated US paper, which currently yields 5.5% or more, is a very good place to be invested for the time being. To my eye, the trends outlined above, higher oil, yields and a stronger dollar, remain intact. As long as that is the case, equity markets are going to struggle. As to the dollar, we will need substantial policy changes to turn that ship around, and right now, there is no sign that is on the horizon.

Good luck

Adf