The only thing that really matters

Is whether NVIDIA shatters

It’s forecasted earnings

And market bulls’ yearnings

Else watch for the NASDAQ in tatters

Of lesser importance we see

The thoughts from the FOMC

Since last they all met

Stock bulls have beset

The rate hawks with obvious glee

While I know this is a macro focused discussion, and that is what this poet understands best, unquestionably, the biggest market news for the day, for all markets, is the NVIDIA earnings release after the close this afternoon. There has been more press about this particular number, and more commentary on Fintwit (FinX?) than any other single stock earnings number I can remember. And let me be clear, I have no idea what is forecast, let alone what the whisper number is, nor do I really care. But I am definitely in the minority. My take is that there are many analysts who will consider adjusting their big picture view of the economy and markets based on one company’s earnings. This might be a sign that things are somewhat unhinged in markets.

Before then, absent any hard statistical data, we will see the FOMC Minutes from the January 31st meeting. You may remember that as the one where Chairman Powell flopped back to hawkish after he flipped to a dovish pivot in December. Since then, there has been a pretty steady drumbeat from all the FOMC members that they are still not confident they have beaten inflation and so want to wait further before they cut rates. And it’s a good thing they have had that view as last week we all saw that inflation was not cooling quite like the doves had expected. In fact, they look pretty smart right now because of their reluctance to join the rate cutting mania.

A review of the Fed funds futures this morning shows that the probability for a March cut has fallen to just 6.5% while May is down to a 37.3% probability. As a demonstration of just how much things have changed in the past month, in the middle of January, March was priced for a 46% probability and May for an 85% probability of the first cut in the cycle. As well, we have seen the number of cuts priced for the full year fall from 6 down to just under 4, not far from the dot plot guidance we received back in December. So far, the Fed has been successful in getting its message across despite a great deal of wailing and gnashing of teeth that if they didn’t cut soon, the world would end.

This begs the question, why is everybody so keen to see the Fed cut rates at all? Consider the issue from the perspective of the saver and retiree. Things are much better when one’s money market account yields 5% than 0% so I expect that most retirees are pretty happy at the current state of affairs. From the equity market’s perspective, the very fact that we have set 11 new S&P 500 all-time highs so far in 2024 indicates that the current level of interest rates is not that big a problem broadly speaking. Yes, there are segments of the market that have underperformed but that is always the case.

On the flipside, of course, Janet Yellen would like to see rates decline as it would cut her interest rate bill, and certainly all those commercial property holders with mortgages coming due this year, a number that has grown to ~$960 billion I understand, are desperate for lower rates, but that is a pretty small subset of the country. All I’m saying is that if the current rate structure is benefitting savers and also putting downward pressure on the rate of inflation, it’s just not clear why so many are desperate for a change. And what if, just for argument’s sake, PCE is hot as is the February CPI print which comes ahead of the next FOMC meeting? Rate hikes are going to start to get discussed a lot more frequently.

One other thing to keep in mind is that the US economy is currently the only major one that is showing any real life. Europe, the UK and Japan are all in recession and China’s growth is effectively stagnating. Other nations are desperate to cut interest rates to help support their economies but are unwilling to do so for fear that their currencies will fall further and invite even more inflation (China excluded) onto their shores. So, they really want the Fed to cut so they can follow along without the concomitant problem of a falling currency. But is the Fed responsible for the problems in Europe or Japan? I think not.

At any rate, we will not solve this dilemma today, and all we can do is observe how things play out over the coming weeks and months. FWIW, which is probably not a huge amount, I have seen precious little evidence that inflation is going to collapse, and rather expect it to stay here or edge higher. In that case, I think the Fed may maintain their current rates for far longer than even June. Absent a banking crisis, perhaps started by more trouble in the commercial real estate sector, my view remains, at most, one token cut this year. Of course, if we do see that banking crisis, then 300bps will be the minimum.

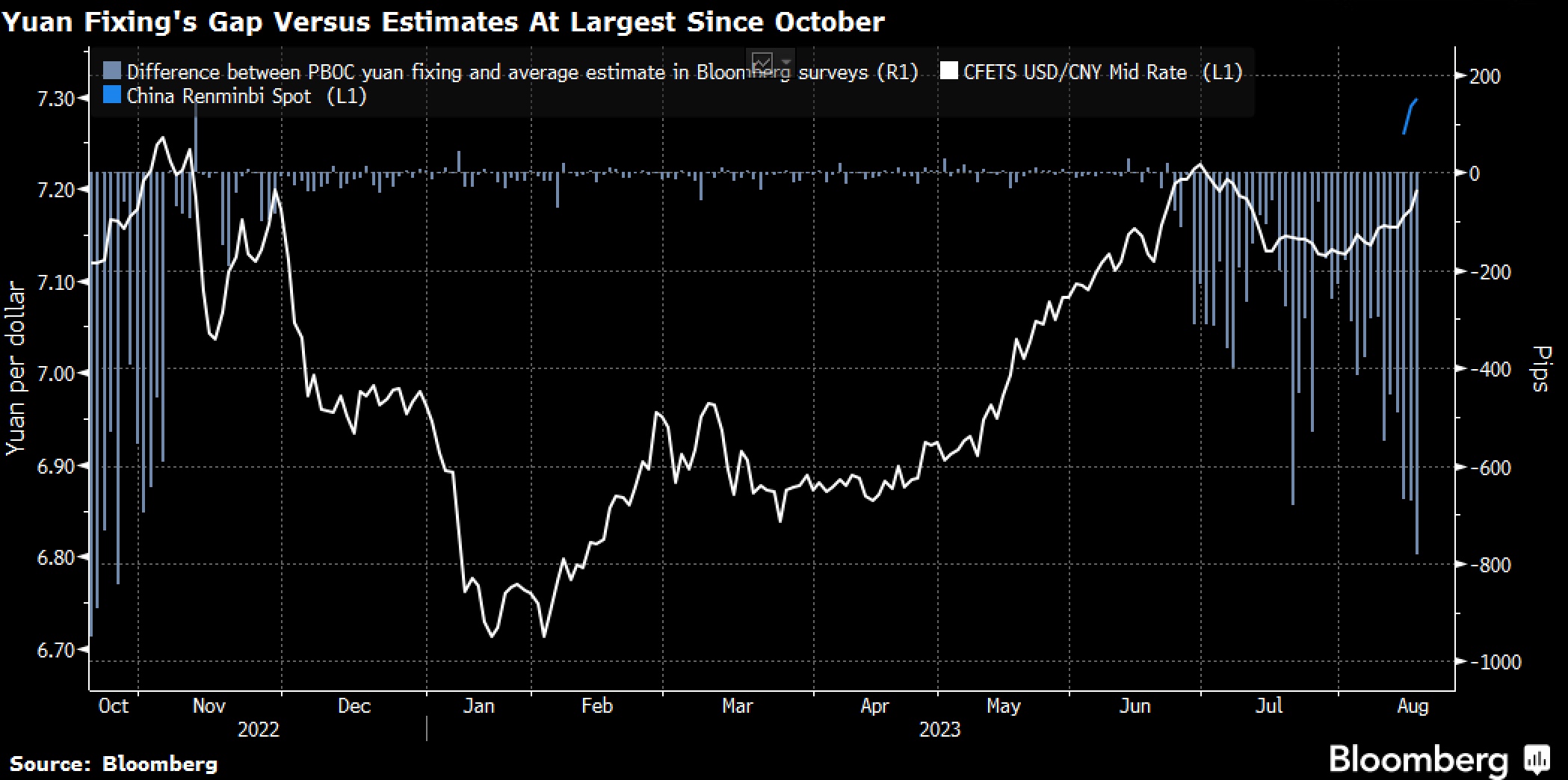

Ok, overnight, most markets remain in thrall to the NVIDIA earnings story with one exception, China, where the regulators there tightened things even further instituting a new rule that there can be no net selling by institutional accounts in the first 30 minutes of trading or the last 30 minutes of trading. This was in response to an algorithmic hedge fund selling a huge chunk of shares Tuesday ($350mm) in just a one-minute window and pressuring the whole market lower. Apparently, they have been fined and prevented from trading for the rest of the week. The idea behind the rule seems to be that if there can be no net selling in the last 30 minutes, the Chinese plunge protection team can work its magic unimpeded and push things higher on command. I continue to wonder why the Chinese Communist Party is so keen to support the very essence of capitalism, but there you have it.

With this in mind, you will not be surprised to know that the CSI 300 rallied 1.4% and the Hang Seng 1.6% overnight. But the rest of Asia was less positive with most markets following the US lead lower. Europe, though, except for the UK’s -0.85% performance, is higher on the day despite an absence of any major data or news. The scuttlebutt is that there is a positive vibe for NVIDIA earnings. Seriously! As to the US futures, at this hour (7:45), they are continuing yesterday’s decline with the NASDAQ leading the way lower by -0.65%.

In the bond market, Treasury yields are softer by 1bp this morning while most European yields are higher by 1bp, so in other words, not much movement overall. Asia saw a similar lack of movement as traders are awaiting the Minutes, NVIDIA and the uptick in Fedspeak tomorrow.

Oil prices (-0.4%) are a bit lower this morning but are just giving up yesterday’s small gains. In fact, they are essentially unchanged so far in February as concerns over weakening global growth have been offset by concerns over an uptick in the middle east anxiety. Speaking of energy, what I haven’t mentioned is NatGas, which while higher today by 10%, given it has fallen to $1.75/MMBtu, the move is not that impressive. Warmer than expected weather has really undermined the price action lately. In the metals markets, gold (+0.3%) continues to creep higher and today copper (+0.3%) is following suit. As to aluminum, it is much higher, +2.4%, as concerns over fresh US sanctions on Russian aluminum have raised the risk of overall market disruption.

Finally, the dollar is little changed against most of its counterparts, G10 and EMG. The biggest mover I see is ZAR (+0.4%) after core CPI ticked higher than expected and raised thoughts of tighter monetary policy there. In the G10, NZD (+0.25%) is also responding to a higher-than-expected PPI print bringing a rate hike more sharply into focus there. Otherwise, nada.

Aside from the Minutes, there is nothing else of note on the data calendar. We do hear from Atlanta’s Raphael Bostic and Governor Michelle Bowman today, but I don’t expect either to waver from the current lack of confidence story. It feels like it is going to be a quiet session overall, with the real fireworks reserved for 4:15 or so when NVIDIA reports.

Good luck

Adf