With payrolls on everyone’s mind The overnight range was confined The bulls live in fear That job growth’s still clear While bears worry payrolls declined But, looking beyond NFP There’s something the bulls fail to see Liquidity’s growth Is worse than just sloth It’s shrinking to quite a degree

Before I start this morning, please know I will be on vacation next week so there will be no poetry again until the 16th.

Now, to start this morning, all eyes are on the payroll report where the market is definitely in the ‘bad is good’ frame of mind. Median analyst expectations are as follows:

| Nonfarm Payrolls | 170K |

| Private Payrolls | 160K |

| Manufacturing Payrolls | 5K |

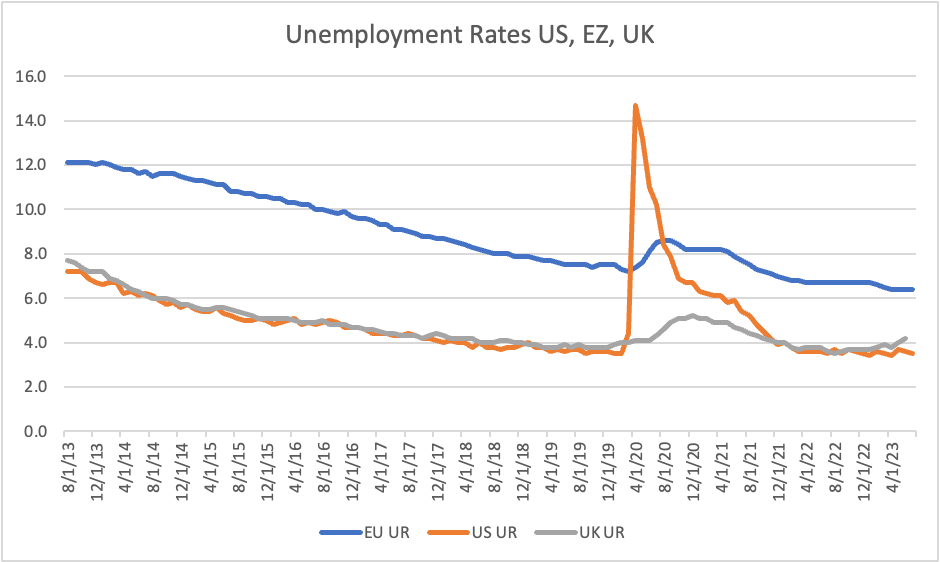

| Unemployment Rate | 3.7% |

| Average Hourly Earnings | 0.3% (4.3% Y/Y) |

| Average Weekly Hours | 34.4 |

| Participation Rate | 62.9% |

Source: tradingeconomics.com

We know that Wednesday’s ADP number was quite weak, and we know that Tuesday’s JOLTS number was quite strong. Yesterday’s Initial Claims data was also a harbinger of strength with the weekly number falling to 207K. If we look at the ISM employment sub-indices, both showed relative strength with the Manufacturing number rising above 50 for the first time in 5 months while the Services employment index remains at a healthy 53.4 level. Much of what I have read over the past several weeks has focused on the idea that companies are still reluctant to lose employees as they remember how difficult it was to hire post the Covid fiasco. I have a funny feeling we are going to see a better than expected number this morning, as between the JOLTS and Claims data it feels like we’re due for a pop. However, I believe we need to see a print above 200K to have a meaningful impact on the markets.

To be clear, if I am correct, I would look for bond yields to retest their recent highs, equities to fall and the dollar to rebound from its recent consolidation/correction.

But let’s discuss the dollar for a moment and a data point that gets short shrift these days, the Trade Balance. A brief history lesson shows that once upon a time, the Trade Balance was the most important monthly release for the FX market. This was during the Reagan years when US policy was highly focused on the trade deficit with Japan and concerns over whether Japan was going to replace the US as the preeminent global economy. (We know how that worked out!). But the point is trade data used to matter. One of the things that gets little attention these days but is directly impacted by the trade data is the amount of global USD liquidity that exists. Despite all the hyperventilation over the concept of dedollarization, the reality is that the dollar has never been a more integral part of the global financial system than now. The reason for this is the fact that there is somewhere north of $275 trillion of USD debt outstanding around the world, according to the IMF, and the US portion is only on the order of $95 trillion. This means the rest of the world needs to service $180 trillion of debt, paying USD interest.

How, you may ask, does everybody get those dollars to pay the interest on that debt? Well, one of the keys had been the US running a massive trade deficit, buying stuff and sending dollars all over the world. Those dollars were used to service the debt. But lately, the US trade deficit has been declining pretty steadily, with yesterday’s better than expected reading of -$58.3 billion a continuation of the last two years’ trend from the worst print of -$105B in March 2022. The thing is, if the US trade deficit is shrinking, we are not sending as many dollars out into the world for everyone else to use. There has also been a great deal of discussion lately about how M2 money supply has been shrinking at an unprecedentedly fast rate, yet another sign that liquidity is drying up. One consequence of these two factors, shrinking M2 and a shrinking trade deficit, is that foreigners need to bid more aggressively for the dollars they need to service and repay their USD notional debt. This has been a key driver in the dollar’s recent strength and there is no sign this is going to change in the near future.

But shrinking liquidity also weighs on other things, notably risk assets. Again, think about the post GFC era when QE’s 1 through infinity were ongoing and all the calls for inflation to ramp up never materialized. Well, as I wrote during that time and is becoming clearer today, there was plenty of inflation, it was just concentrated in asset prices like stocks, bonds and real estate, as opposed to everyday items like groceries, clothing and dining out. At this point, we realize that the Covid fiscal stimulus around the world is what unleashed the recent bout of inflation, and that central banks are working feverishly to halt this trend. Combine the Fed leading the way, having raised rates the furthest of the major central banks, and the fact that there are less dollars around due to shrinking money supply and trade deficits, and you come up with a good understanding of why the dollar remains well bid. Regardless of the short-term impact of numbers like today’s NFP, the underlying structural effects continue to point to dollar strength.

With that structural backdrop in mind, a look at today’s price activity shows modest net activity ahead of the data. Asian equity markets that were open had a mixed session with the Nikkei sliding while the Hang Seng managed some solid gains (+1.6%) and mainland Chinese markets remained closed, set to reopen on Monday. European bourses, though, are having an ok day, with gains on the order of 0.5% or so after better than expected Factory Orders data from Germany. As to US futures, they are currently (7:30) higher by 0.1% and trading in a tight range.

Bond yields are backing up again with Treasuries and most of Europe higher by 3bps or so. One move that has been growing lately is the Bund-BTP spread, which is now 202bps, right at the level where the ECB has historically started to get a bit nervous. If this spread continues to widen look for more ECB talk about, first, how the market is wrong, and then second, how the TPI, their program to buy BTPs and sell Bunds, is likely to be appropriate. At 250bps, their hair will be on fire, but that still feels pretty far off.

Oil prices, which are unchanged today, appear to be consolidating after a hellacious week where they fell >$10/bbl. The thing is demand data continues to point to growth and supply data continues to point to limits. The recent price action has all the earmarks of Russian disinformation a trading response to the massive run higher through the summer where a lot of trend followers got into the market too late. Longer term, the direction here remains higher in my view. As to the metals markets, they also are consolidating after a rough period with gold unchanged though silver, copper and aluminum are all higher between 0.3% and 0.9% this morning. Again, we have seen a pretty sharp decline here, so this feels like a trading reaction, not a fundamental thing.

Finally, the dollar is a bit firmer this morning as we await the data. USDJPY continues to hold the 149 level and it looks to be merely a matter of time before we test 150 again. According to the flow data from the BOJ, there was no indication that they intervened earlier this week which implies there was some rate checking. However, it is very clear they remain quite concerned over the movement. One currency that has really seen some movement lately is MXN, which after a long period of strength on the back of a very stout monetary policy by Banxico, has given back 10% in the past 5 weeks. Interestingly, the US is running a growing trade deficit with Mexico, which should help alleviate some pressure on the peso, but right now, the difference in tone between the Fed’s higher for longer and Banxico’s we are done is the driver.

Aside from payrolls this morning we see consumer Credit (exp $11.7B) and hear from Governor Waller at noon. Yesterday’s Fed speak was much of a muchness with no changes in tone overall. At this point, all we can do is wait.

Good luck, good weekend and until Monday October 16th

Adf