No respite was found yesterday

With risk assets given away

Now traders all wonder

If Trumpian thunder

Will ever, a rally, convey

But from the cheap seats what seems clear

Is Trump, for right now, will adhere

To efforts to trim

The grift and the skim

A prospect his enemies fear

The only discussion in markets today is about yesterday’s sharp declines in equity markets. Questions about how long this can continue or how long President Trump can withstand the pain that accompanies these declines are rampant. However, thus far the indications are that he and his administration are aware of the risks but also committed to achieving his goals of more domestic manufacturing activity and a perceived fairness or leveling of the international commerce playing field.

We have heard from Trump, Bessent and Commerce Secretary Lutnick, that there is going to be some pain, but they believe it will be short-lived in nature. And ask yourself this, given how overextended both market valuations and debt metrics had become, was there any way to address these issues (assuming you believed they were issues) without some pain? Of course not. I have long maintained that what needs to happen in the US economy is for markets to be allowed to clear, all markets, whether housing or financial, and that we have not seen that happen for more than 50 years.

While perhaps the case can be made that the housing market came close to clearing in the wake of the GFC, consider what has happened since then with the implementation of waves of QE and ZIRP. The chart below from the St Louis Fed’s FRED database shows their housing index over time. Ask yourself if you think the housing market really cleared? And more importantly, look at the acceleration since then. President Trump has made clear his focus is on Main Street, not Wall Street, and it is easy to argue that a key driver of this massive rise in house prices has been the Fed and their efforts to prop up Wall Street. Reversing that is going to be painful. Hell, simply stopping that move will be painful.

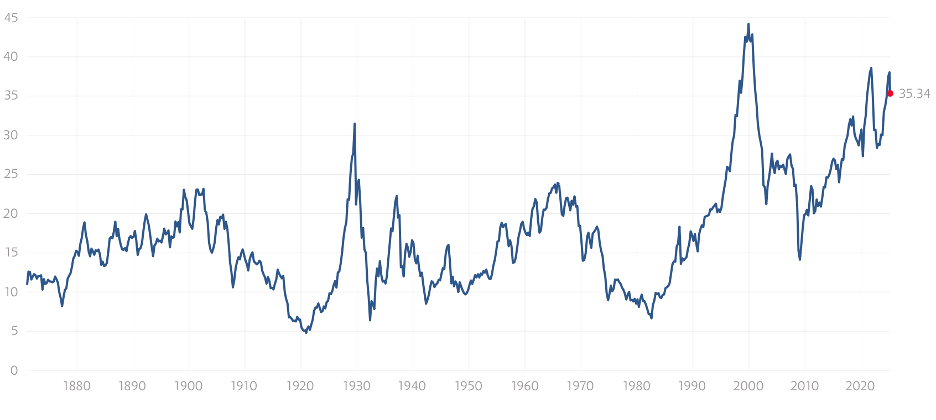

As to equity markets, the only clearing event that we have seen was the crash of the NASDAQ after the tech bubble burst in 2000. But again, the Fed was there cutting rates and easing policy to support things. The best evidence that equity markets are at unsustainable levels comes from the valuation metrics, with things like the Shiller CAPE ratio pushed to levels only ever seen in that tech bubble, and clearly significantly above long-term mean (17.21) and median (16.03) levels with today’s current reading of 35.34.

Source: multpl.com

All of this is my way of saying that I do not believe we are anywhere near the end of this process. While many of you don’t remember President Reagan, at the beginning of his first term, he stood by Fed Chairman Volcker in his efforts to squelch inflation, when Volcker raised Fed funds to 22.0% (see below) and the economy suffered two quick recessions in 1980 and 1982.

However, that was the medicine that was needed to break inflation’s back and begin a 40-year run of stability and growth in the US amid low inflation. It is not hard to believe that we are going to need to see another cleansing bout of austerity to once again reset the economy. And remember, Trump is not running again, so is not worried about reelection. If we do have a recession soon, it will likely be over and the recovery under way as we head into the next elections, a perfect political outcome for his party.

Ok, let’s see how other markets responded to yesterday’s US declines. In Asian equity markets, Tokyo (-0.6%) slid, but nowhere near the declines seen in the US. China (+0.3%) and Hong Kong (0.0%) basically ignored the situation, but the rest of Asia saw a lot more red on the screen with large losses seen in Korea, Taiwan, Australia, Malaysia, Singapore and the Philippines. In Europe, though, the price action is mixed with some gainers (DAX +0.4%, CAC +0.2%) and laggards (IBEX -0.2%, FTSE 100 -0.15%) as it appears funds continue to flow from the US markets to Europe on the back of the mooted defense buildup. US futures at this hour (7:10), are very modestly higher, 0.15% across the board, but my take is there is further pain to come.

In the bond market, yesterday saw a flight to safety with Treasury yields sliding 10bps and although we did not see similar moves in European sovereigns. This morning, Treasury yields are unchanged from the close while European bonds are showing modestly higher yields, between 1bp and 3bps. JGB’s though, saw yields follow Treasuries lower, dropping -6bps last night as not only did US yields fall, but Japanese Q4 GDP data was released at a weaker than preliminarily reported 2.2%. Although that was higher than Q3, and represents solid growth, it is not quite what was in the market.

In the commodity market, oil (+0.9%) while higher this morning continues to hold its downtrend as per the below chart. With further Russia/Ukraine peace talks starting up in Saudi Arabia, the prospects of Russian oil coming back to the market seem to be growing.

Source: tradingeconomics.com

As to the metals markets, gold (+1.0%) is the laggard this morning with both silver (+1.6%) and copper (+1.9%) leading the space higher. If US equities are responding to a growing probability of a US recession, then I would have expected the industrial metals to soften. However, after several down days, this could well be just a reflexive trading bounce. We will need to see further movement to get a better sense of things.

Finally, the dollar remains under pressure generally with the euro (+0.5%) once again gaining ground and touching the 1.09 level for the first time since the US presidential election. Not surprisingly, that has dragged the CE4 currencies higher as well, but the dollar’s weakness is seen vs. CNY (+0.4%), KRW (+0.5%), SEK (+0.45%), NOK (+0.8%) and even CAD (+0.25%). Again, the big picture here is that the current policy aims for the US have begun to alter the concept of US exceptionalism with regards to the stock market. As funds flow elsewhere, the dollar is quite likely to continue to decline. This will be reinforced if we continue to see 10-year Treasury yields decline.

On the data front, while today is not very exciting, we do see CPI and PPI this week.

| Today | JOLTS Job Openings | 7.75M |

| Wednesday | CPI | 0.3% (2.9% Y/Y) |

| Ex food & energy | 0.3% (3.2% Y/Y) | |

| Thursday | Initial Claims | 225K |

| Continuing Claims | 1910K | |

| PPI | 0.3% (3.3% Y/Y) | |

| Ex food & energy | 0.3% (3.6% Y/Y) | |

| Friday | Michigan Sentiment | 66.3 |

Source: tradingeconomics.com

We are now in the Fed’s quiet period so there are no Fed speakers until their meeting next Wednesday, but as I have been saying, nobody is really paying much attention to them anyway. I think we have seen some major changes evolve and that means that equities are likely to remain under pressure along with the dollar, while bonds should hold their own.

Good luck

Adf