As tiresome as it may be To talk about China and Xi The doldrums of summer Are simply a bummer With nothing else worthy to see However, come Friday we’ll turn To Jackson Hole where we should learn If Jay and the Fed, When looking ahead, Decide rate hikes soon can adjourn

The biggest news overnight was that the PBOC cut interest rates again, but this time somewhat less than expected. You may recall that last week, they cut the 1-yr Lending Facility rate by 15bps in a surprising move. In fact, this is what started the entire chain of events last week that resulted in China dominating the macroeconomic news. Well, last night they cut the 1yr Loan Prime rate by a less than expected 10bps with the market looking for a 15bp cut. And they left the 5yr Loan Prime rate, the rate at which most mortgages in China are priced, unchanged at 4.20% rather than implementing the 15bp cut that the market had anticipated. The result is that so far, Chinese support for their economy remains tepid at best.

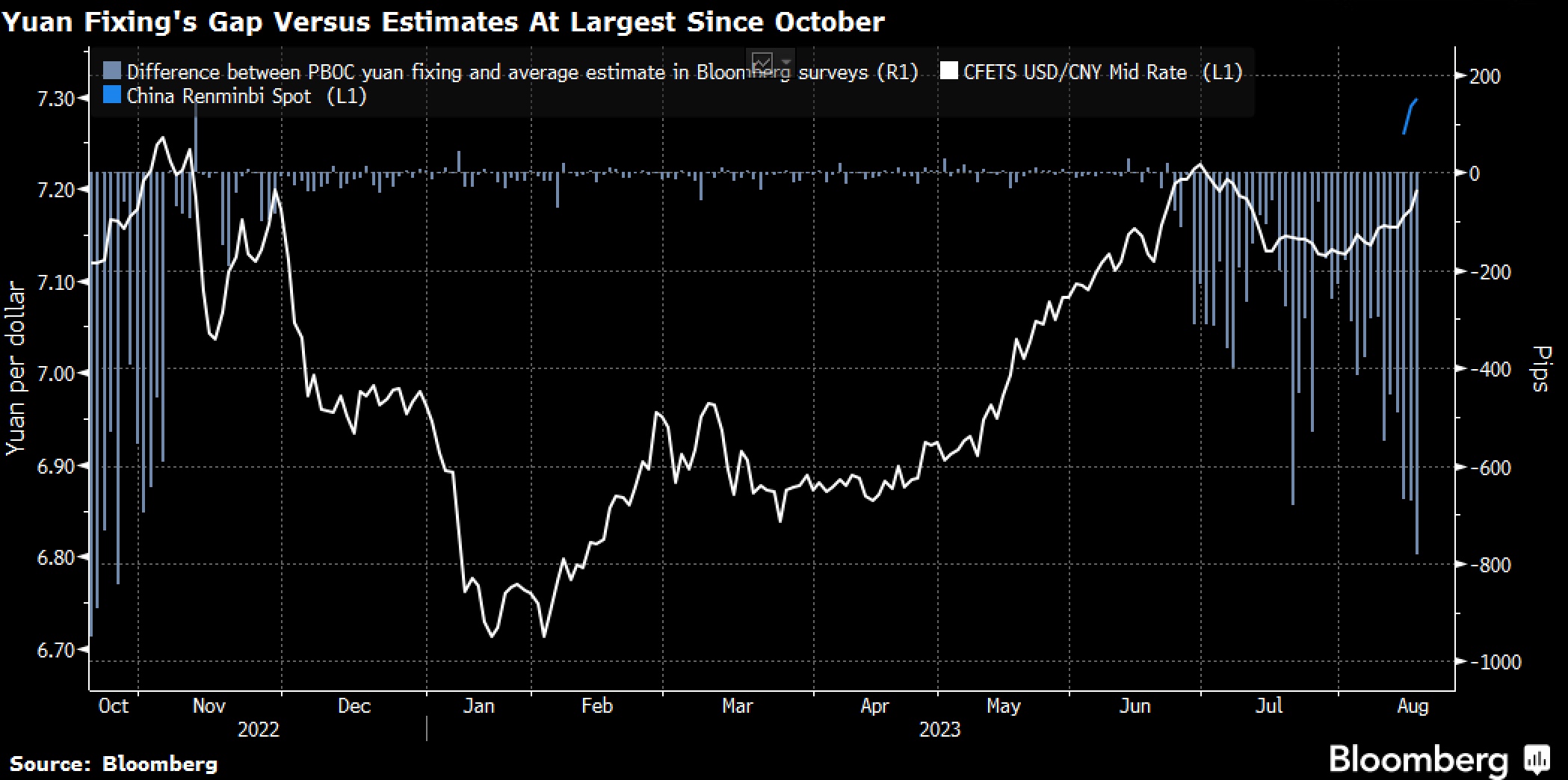

At the same time, there continues to be a grave concern in Beijing regarding the exchange rate as, once again, the daily fixing was far below the market rate, and once again, the renminbi fell anyway. It has become abundantly clear that the PBOC is quite concerned over a ‘too weak’ renminbi, hence the maintenance of the 5yr interest rate. As well, it was widely reported that Chinese state-owned banks were actively selling USDCNY in the market to prevent further weakness in their currency.

Perhaps this is a good time to briefly discuss the concept of the end of the dollar again, a topic that continues to make headlines. One of the key pillars of this thesis is that the PBOC has reduced the number of dollars on its balance sheet substantially over the past several years which is seen as an indication that they are preparing to support some new reserve asset. However, as last night’s price action indicated, it is quite possible, if not likely, that the only change has been one of location, rather than amount. As the PBOC reduced the dollars on its balance sheet, the big state-owned banks all increased the amount on their balance sheets. So now, the PBOC can direct those banks to intervene on their behalf whenever they want to do something. At the same time, the PBOC has the appearance of decoupling, something they are clearly trying to demonstrate.

This week is the big BRICS meeting where the stories are that they are going to unveil a new BRICS currency, allegedly to be gold-backed, as these nations try to undermine US power as well as offer an alternative to non-aligned nations. The thing to remember about this group of widely disparate nations is that it has never been a cohesive bloc, it was simply an acronym created by a Goldman Sachs analyst in 2001 to describe a group of fast-growing emerging markets. However, other than China and Russia, which have become closer since Russia’s invasion of Ukraine, they really have very little in common. They are geographically widely diverse, have very different governing structures as well as very different financial and monetary policies. In other words, there is nothing to suggest they can act as a cohesive group for any major decision. While I am certain there will be some announcement of some sort at the end of the conference, an alternative to the dollar will not be coming anytime soon.

As to Jackson Hole, since Powell’s speech isn’t until Friday morning, we have plenty of time to touch on that topic later in the week. In the meantime, risk is arguably in modest demand this morning. While Chinese shares suffered significantly overnight on the disappointing rate news, European bourses are all nicely higher, generally between 0.75% and 1.00%. Too, US futures are firmer this morning by about 0.5% after a late day rally Friday brought the major indices back near unchanged on the day from earlier lows in the session.

At the same time, bond yields continue to rally with 10-year Treasury yields back at 4.30%, up 4bps this morning, while European sovereign yields are all higher by between 4bps and 5bps. It seems the bond market is not completely on board with the soft-landing narrative even though an increasing number of analysts are coming around to that view. I think what we have learned thus far is that the US economy is not nearly as interest rate sensitive as it used to be. The post-Covid period of QE and ZIRP saw a massive refinancing of debt, both mortgage and corporate, into longer-dated, low fixed rates. With yields higher, there is much less need for refinancing, at least not yet, and so many of the problems that have been widely expected just have not happened yet. At some point, when debt needs to be refinanced, if rates are still at current levels, it is likely to prove problematic for the companies and the economy writ large. But that could still be some time from now. In the meantime, I continue believe the yield curve inversion, which is now down to -67bps, could disappear completely by 10yr yields continuing to rise. That is clearly not the consensus view.

Turning to commodities, they are generally looking good today led by oil (+1.2%) which has rebounded over the past several sessions and is back above $82/bbl. The metals, too, are looking good with gold up at the margin, although hovering just below $1900/oz, while copper also has a bit of support today, up 0.3%. For the industrial metals, China remains a key question mark. If the Chinese economy continues to slow, then demand for these commodities is likely to be disappointing and prices seem likely to come under short-term pressure. But remember, the long-term story remains one where many of these are essential for the mooted energy transition, and there simply is not enough of the stuff to satisfy the demand. Longer term, prices still have room to rise.

Finally, the dollar is starting to slide as I type. An earlier mixed picture has seen buyers of NOK (+0.75%) as oil continues to rebound, but also in essentially all of the G10 with only the yen (-0.3%) lagging. In fairness, this is classic risk-on price action. Turning to emerging market currencies, Asian currencies were mostly under pressure last night after the China rate news, but this morning EEMEA currencies are looking much better as they follow the euro (+0.3%) higher. It appears that fear is taking a day off today.

On the data front, there is not much of real interest this week:

| Tuesday | Existing Home Sales | 4.15M |

| Wednesday | Flash Manufacturing PMI | 49.0 |

| Flash Services PMI | 52.0 | |

| New Home Sales | 704K | |

| Thursday | Initial Claims | 240K |

| Continuing Claims | 1700K | |

| Chicago Fed Nat’l Index | -0.20 | |

| Durable Goods | -4.0% | |

| -ex transports | 0.2% | |

| Friday | Michigan Sentiment | 71.2 |

| Powell Speech |

Source: Bloomberg

Given the number of market participants on summer holiday, I suspect that there will be very little activity this week until we hear from Chairman Powell. I would look for a little bit of choppiness, but no real directional moves until we know the Fed’s latest views. And there is a real chance that he doesn’t tell us anything new, which means that we would then be waiting for NFP a week from Friday. Net, until the Fed’s hawkishness breaks, I still like the dollar best.

Good luck

Adf