In Europe, the data today Showed growth’s in a negative way Recession is here Though not too severe While pundits are filled with dismay Meanwhile in the States there’s a haze Of smoke for the last several days That Canada’s burning Is somewhat concerning As forests there still are ablaze

Arguably, the story that is getting the most press is the ongoing wildfires in Canada which has led to significant smoke issues throughout the Midwest and East Coast of the US. In fact, at one point yesterday, the FAA closed LaGuardia Airport in New York because the smoke was so thick. The latest that I have seen indicates these fires are likely to continue to burn for a number of days yet as they are nowhere near under control in Canada. I guess we will need to get used to an orange sun rather than a yellow one for the time being. While there is no evidence yet of any true behavioral changes, be alert for government edicts to prevent people from traveling or going outside and a short-term reduction in economic activity, at least in June while this is ongoing. I fear that the willingness of government officials to declare states of emergency and take on dictatorial powers has grown since Covid, so it will be interesting to see how this plays out. A headline across the tape just now (7:00) shows that LaGuardia is shut down for inbound flights again due to reduced visibility. In the end, be careful as inhaling too much smoke will not be good for you.

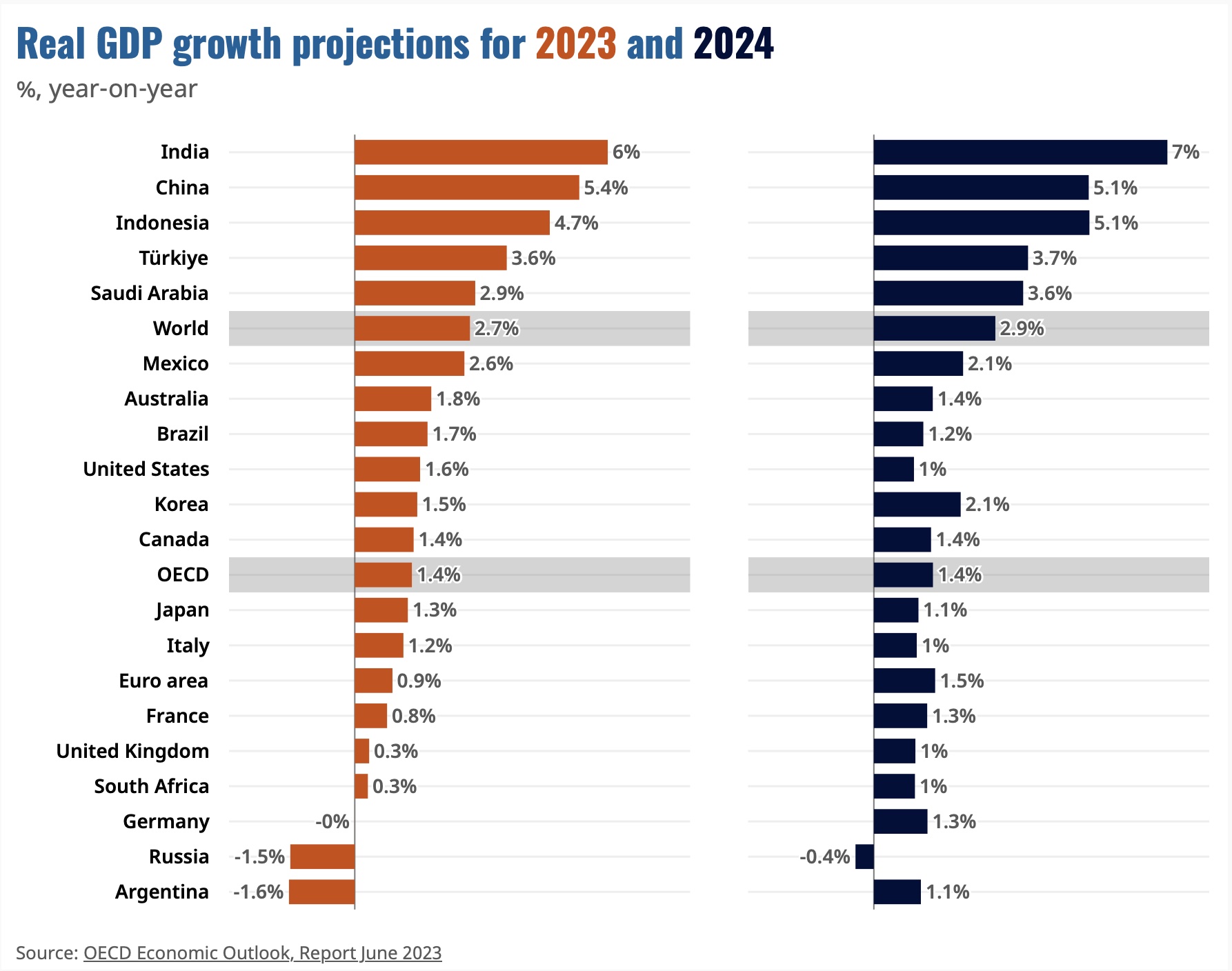

But after that, which is truly wagging every tongue in NY, the other story of note is that the Eurozone has fallen into a technical recession, with the final revision of Q1 GDP falling to -0.1%, and Q4’s numbers being revised lower as well, to -0.1%, after much weaker than previously assumed data from both Germany and Ireland was incorporated into the statistics. You may recall the argument in the beginning of 2022 when the US suffered through two consecutive quarters of negative real GDP growth, but there was a great effort to claim that was not a recession. And officially it was not as in the US a recession is not official until the NBER declares it so in hindsight. But Europe does not have an NBER and there is no argument at this point that the Eurozone went through quite a weak patch recently.

Arguably, though, of more importance is whether this weakness will continue or whether we have just witnessed the much-anticipated recession. This matters a great deal because next week, the ECB meets and is widely expected to raise its interest rate scheme by a further 25bps with the market pricing in an additional hike there by summer. If the Eurozone is in recession, especially if it starts to deepen a bit more aggressively than the recent -0.1% quarterly data, will the ECB have the resolve to continue to fight inflation and keep raising rates? Granted, their mandate is purely inflation focused, unlike the Fed’s dual mandate of inflation and employment, so they would be well within their rights to do so. But…continuing to raise interest rates into a clear recession is a very difficult decision as it can easily be seen as a policy error. At this point, my take is they will indeed hike next week, but I am far more skeptical about future hikes especially as the Fed is pausing skipping this meeting and may well be done. The idea that the ECB will continue to tighten policy aggressively while the Fed is not seems pretty far-fetched based on its history.

Speaking of rate hikes, Canada is in the news there as well after the BOC surprised the market and unpaused (?) by hiking 25bps yesterday. Essentially, they have concluded that economic activity is too strong to allow inflation to return to their 2% goal, the same reasoning we heard from the RBA last week when they surprised markets and raised their base rate. While the FX market response was not quite as aggressive as in Australia (CAD rose 0.5% on the news and has basically tread water since then), the move has certainly forced rethinking the assumption that the Fed is actually going to skip this meeting. Arguably, much will depend on next Tuesday’s CPI data with current estimates there for 4.2% headline and 5.2% core. Any number that prints hot will get tongues wagging about the Fed continuing to raise rates with corresponding market impacts. For now though, we can merely guess.

And that is the background for today’s session. Yesterday saw a bit of a pullback in risk assets in the US with most of Asia following lower, although Chinese stocks held up. Eurozone bourses are all marginally higher this morning, as it seems the growth data was less concerning and hopes that the ECB would be forced to stop hikes sooner have been a driving force. As to US futures, they are all essentially unchanged this morning as everybody continues to wait for the Fed next week.

Bond markets, though, were a bit shaken by the BOC move with yields climbing in the US yesterday and a further 1bp rise this morning back to 3.80%. In addition, 2yr yields are back up to 4.55%, and with the Treasury now having no debt ceiling at all, I expect we will see significant issuance driving yields higher still. In Europe, the picture is more mixed with yields either side of unchanged as there is confusion on how to play this market. And one final thing is in Japan, where JGB yields have edged higher by 2bps overnight and are now at 0.434%, slowing approaching the YCC cap. That is a potential issue for the not-too-distant future so we will keep on top of it.

Oil prices continue their slow rebound, up 0.9% this morning and actually up 4.3% in the past week. Perhaps the Saudi production cuts are finally being priced, or perhaps the idea that Canada has indicated stronger growth is seen as a harbinger of a better economic situation and less demand destruction. As to metals prices, gold, which fell sharply yesterday, is rebounding slightly and the base metals are mixed. As long as we get conflicting economic signals (weakness in Europe, strength in North America) I think these metals will have a difficult time choosing a direction.

Finally, the dollar is generally softer this morning, which given the higher yields in the US is a bit surprising. But NOK (+0.7%) leads the way on oil strength, and we continue to see strength throughout the commodity bloc. Even the euro has rallied this morning, although that feels far more like position adjustments than fundamentally driven movement. As to the EMG bloc, ZAR (+0.7%) is once again at the head of the list, entirely on commodity movement but most of EMEA is stronger while Asian currencies were generally under a bit of pressure overnight. At this point, I continue to believe most markets are awaiting the FOMC meeting as the next potential catalyst and so expect limited directional trading until then.

On the data front, Initial (exp 235K) and Continuing (1802K) Claims are on tap this morning, neither of which seem likely to move the needle. Yesterday’s Trade data was modestly better than expected while Consumer Credit grew a bit more than expected. In the end, though, it is still all about the Fed. As such, I expect more back and forth but no secular movement until we hear from the FOMC.

Good luck

Adf