Seems President Xi isn’t done

And last night he added a ton

Of new stimuli

In order to try

To hit a financial home run

The market response has been clear

Forget anything that’s austere

It’s buy with both hands

Ere Powell rebrands

QE as just more Christmas Cheer

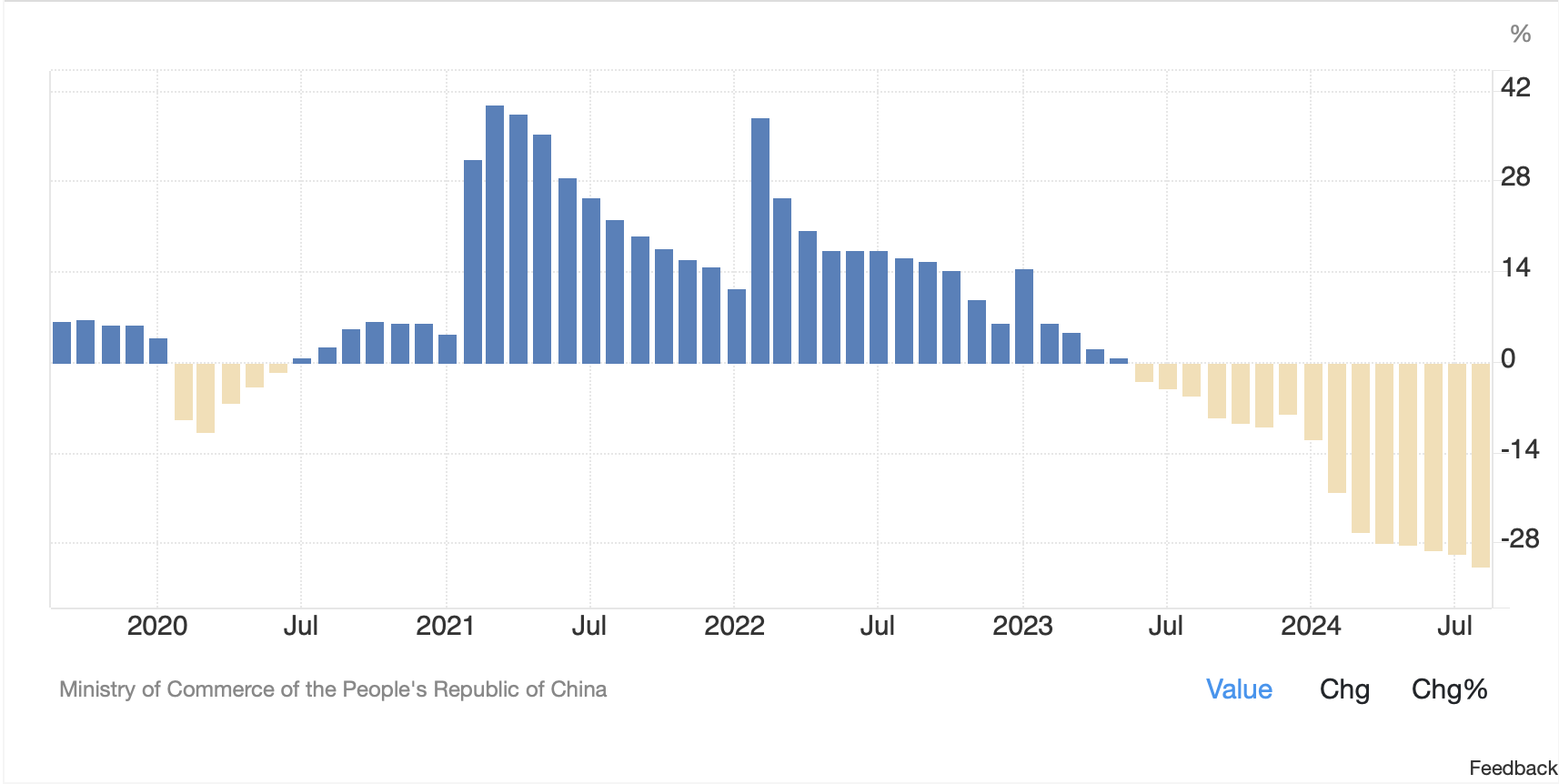

Things are obviously worse in China than President Xi had been willing to let on for the past several months/years, as after two straight days of monetary policy stimulus announcements, they pulled out the big guns and got the fiscal side of the process involved. Last night the Politburo pledged further support after a surprise meeting to discuss economic policies. Their economic discussions have historically only occurred in April, July and December, so this was the latest indication that Xi is really concerned.

Some of the actions include an (unspecified) effort to make the real estate market “stop declining”, limiting construction of new home projects, issuing CNY 2 trillion of special sovereign bonds to disburse funds to help fund financial assistance for low-income workers, shore up bank capital to encourage more lending and support further investment in productive capacity as well as to potentially buy up unfinished homes.

Obviously, Xi was quite concerned that the country would not achieve his 5% GDP growth target for 2024 as an increasing number of analysts around the world were penciling in slower growth, and he decided he could not wait until December for the next policy adjustments. Remember, too, that next week is a week-long Chinese holiday, so part of the impetus was to give cash to people to encourage more spending/activity. While it is far too early to determine how effective these new policies will be at supporting real, organic economic activity, they did wonders for equity markets and risk assets around the world.

And really, that continues to be the main story. With the Fed now having confirmed that lower rates are appropriate, I would look for almost every nation to boost stimulus, both monetary and fiscal, especially in the wake of recent election results which have seen incumbent after incumbent tossed from office. After all, what good is being in power if you cannot buy your way to re-election?

So, how has all this impacted financial markets this morning? You will not be surprised to see that risky assets are in huge demand with equity markets rallying everywhere along with metals, while haven assets see much more modest demand, with bond yields having slipped just a bit lower.

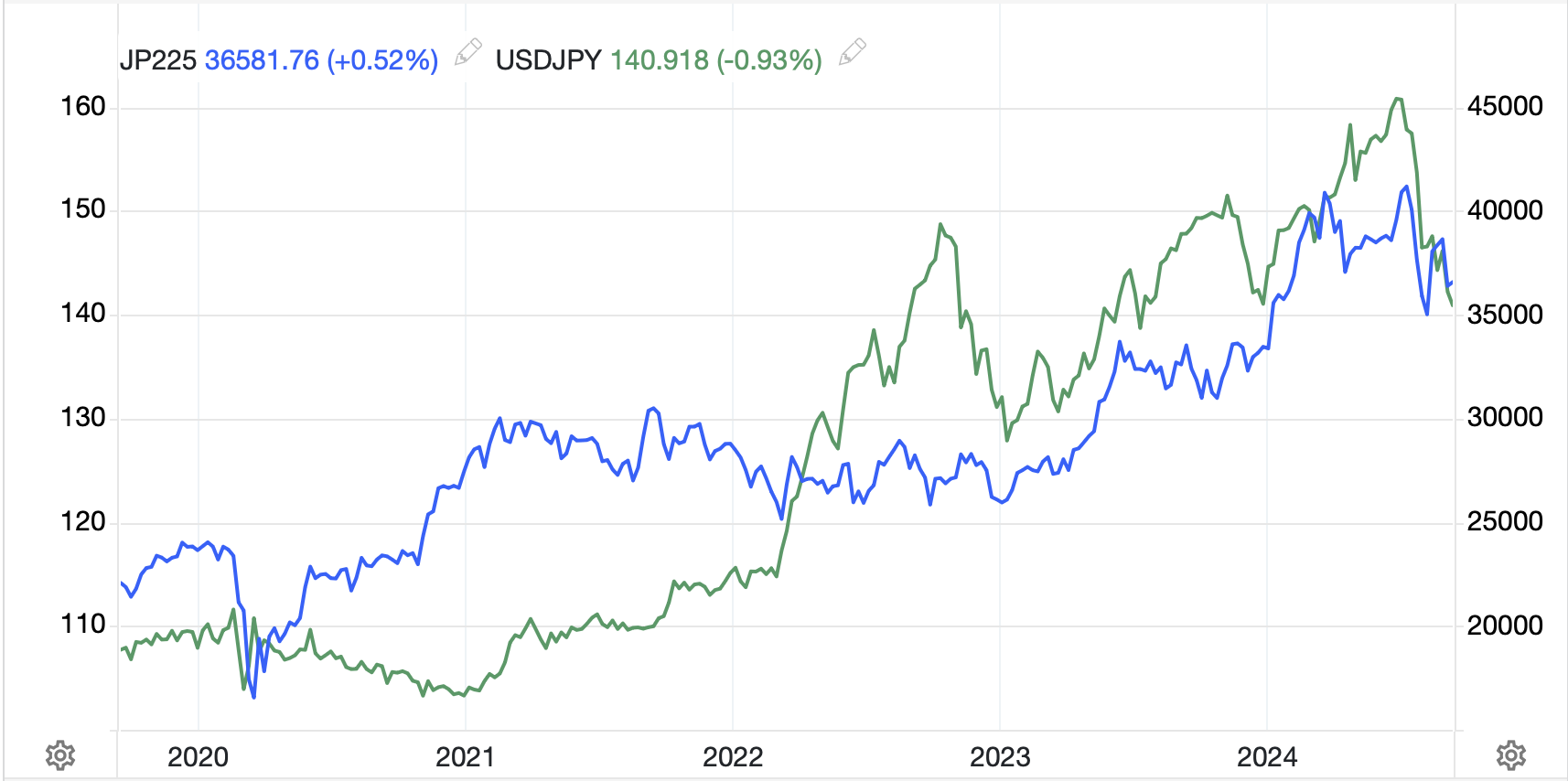

Yesterday’s mixed US market performance is but a distant memory this morning with Asian shares roaring higher (Nikkei +2.8%, Hang Seng +4.2%, CSI 300 +4.2%) and gains virtually across the region, albeit not quite as robust as those. But after the Fed cut, this fiscal stimulus from China is seen as helping everybody. Europe, too, is rocking this morning with gains well above 1.0% everywhere (DAX +1.2%, CAC +1.6%, IBEX +1.1%) except the UK (FTSE 100 +0.2%) which continues to struggle as the Labour government is shown to be further and further out of its depth with respect to actually running things rather than carping about how the Tories did it. And not to worry, US futures are all racing higher as well this morning, higher by between 0.3% (DJIA) and 1.5% (NASDAQ) at this hour (7:15).

In the bond market, Treasury yields have edged lower by 2bps and remain far below the Fed funds rate. It is not clear if this is the market anticipating a more significant economic slowdown or simply a continued manifestation of the fact that the Fed still owns a significant portion of the debt outstanding and so has restricted supply at the margin. In Europe, yields are also lower, with the riskiest nations seeing the biggest declines as risk assets are in vogue this morning. Thus, Italy (-7bps) and Greece (-6bps) have moved the farthest, but otherwise we are seeing movement on the order of -3bps elsewhere. In another quirk, and a telling comment on the state of France’s finances, Spanish 10yr bonos now yield less than French 10yr OATs for the first time in more than 15 years.

Turning to commodities, oil (-2.8%) didn’t get the China rebound memo and has tumbled nearly $2/bbl falling well below the $70/bbl level. It seems that Saudi Arabia is dropping its price target and preparing to increase production, something the market has been fearing. As well, in Libya, which had not been producing lately due to political issues, it appears a tentative agreement is in place that will allow for more supply on the market.

But you know what really benefits from a lot of deficit spending and the effective abandonment of inflation targets? That’s right, precious metals as gold (+0.8%) continues its steady move higher to new all-time highs and quickly approaches $2700/oz. This has taken both silver (+2.2%) and copper (+2.2%) along for the ride and there is currently no end in sight.

Finally, the dollar is under pressure this morning in a classic risk-on reaction. AUD (+0.9%) is the leading G10 gainer on the back of its strong metals exposure while NZD (+0.8%) is right behind. But the dollar’s weakness is manifest in Europe (EUR +0.2%, GBP +0.5%, SEK +0.5%) as well as against most EMG currencies. In fact, CNY (+0.55% and below 7.00) is one of the biggest movers today although we are seeing strength in KRW (+0.7%), MXN (+0.5%) and ZAR (+0.4%), an indication that this move is widespread. As long as the perception remains that the Fed is going to lead the way to lower interest rates, I can see the dollar underperforming. However, as soon as we see other nations become more aggressive, this move will abate.

On the data front, there is much on the calendar this morning starting with the weekly Initial (exp 225K) and Continuing (1832K) Claims data as well as the 3rd look at Q2 GDP (3.0%). We also see Durable Goods (-2.6%, +0.1% ex-Transports) and then the ancillary data that comes with the GDP report including Real Consumer Spending (2.9%), Final Sales (2.2%) and the GDP PCE indicator (2.5% headline, 2.8% core). But perhaps of far more importance, we hear from a host of Fed speakers this morning. Governor Kugler and Boston Fed president Collins speak about financial inclusion, Governor Bowman discusses the economy and monetary policy, Governor Cook discusses AI and workforce development, Vice-chair Barr discusses regulation and Chairman Powell gives the opening remarks at the US Treasury Market Conference in NY.

Yesterday, Governor Kugler added to the ‘mission accomplished’ view on inflation at the Fed and lauded the move to focus on Unemployment. I would contend this is the key issue right now, the fact that central banks around the world, but particularly the Fed, have determined that the inflation fight is over. While we may very well touch 2.0% core PCE in the next months, it strikes me as highly unlikely that level will be maintained. Rather, 2.0% is now the floor and if the Unemployment Rate behaves in its historic manner, accelerating higher now that it has started to move in that direction, look for much sharper interest rate cuts, much higher inflation and a much weaker dollar. To me, that is the biggest risk. However, if Unemployment follows the Fed’s projected path, and stays quiescent, then the current slow decline in rates and a very gradual decline in the dollar seems more likely.

Good luck

Adf