‘Ought Twenty-Six barely got started And Trump has already departed From previous norms Of post-Cold War forms Now socialists are broken-hearted

Their man in Caracas is gone With outrage from Beijing to Bonn But folks on the street Believe it’s a treat Please welcome this year’s first black swan

I certainly didn’t have the exfiltration of Venezuelan strongman Nicholas Maduro from his palace in the middle of the night on my bingo card, did you? But that is what we all woke up to Saturday morning. In a way, we cannot be surprised as President Trump indicated several weeks ago that he spoke with Maduro, told him if he left, he could have safe passage, and be left alone, but ostensibly Maduro turned him down. I’m guessing old Nick is questioning that decision right now.

As this all took place Saturday morning, no financial markets, other than cryptocurrencies, are open and based on Bitcoin’s movement of 0.1% as I type, it appears the issue is not seen as a major concern. There is much discussion regarding what will happen to the price of oil, as unquestionably, Venezuelan oil was part of the decision equation. But the Venezuelans have been producing less than 1 million bpd, far below their pre-socialist levels, and given they sit on the largest known oil reserves on the planet, far below what their ultimate capabilities can be. If you’re Chevron’s CEO, you must be thrilled this morning, as they are already operating in country there.

Too, remember that Venezuelan crude is heavy and sour, which is what most Gulf Coast refineries are tuned to utilise to distill diesel, gasoline and other products. It is too early to know what will happen to oil prices in the short run, but I would suggest that the longer-term view has to be lower prices going forward. Consider that the US already is the largest producer of oil and oil equivalents (about 20mm bpd) in the world. I would expect that Venezuela will be exiting OPEC under a new administration there, and with US oil expertise, will be seeking to expand that sector as rapidly as possible. In fact, achieving 10mm bpd within a few years does not seem unrealistic.

Now consider that by the end of the decade, the Western hemisphere could well be producing half the world’s oil supply, as already, despite degradation of capabilities in both Venezuela and Mexico, it produces more than one-third of the oil pumped. That would certainly put a crimp in Russia’s war machine as the price seems far more likely to head toward $50/bbl than $80/bbl or higher, and by all accounts, that would be hard on Russia’s budget.

Too, consider the geopolitical ramifications if China were suddenly paying full price rather than whatever discounts they currently get for sanctioned oil purchases. As well, what does a lower price do to the Iranian regime’s finances? Probably not very helpful.

It is way too early to know how things will evolve, but between growth in production in Guyana and Argentina, and the prospects for significant growth in Venezuela going forward, it should become cheaper to fill up your tank going forward.

We will see how markets open Sunday night, and I would not be surprised to see oil rally at the start, but I would contend the politics points to lower prices not higher ones.

Source: visualcapitalist.com

Note that neither Venezuela nor Argentina make this list individually. I would wager that by 2027, both will be prominent producers, along with Guyana.

Welcome to 2026! It is going to be an interesting year.

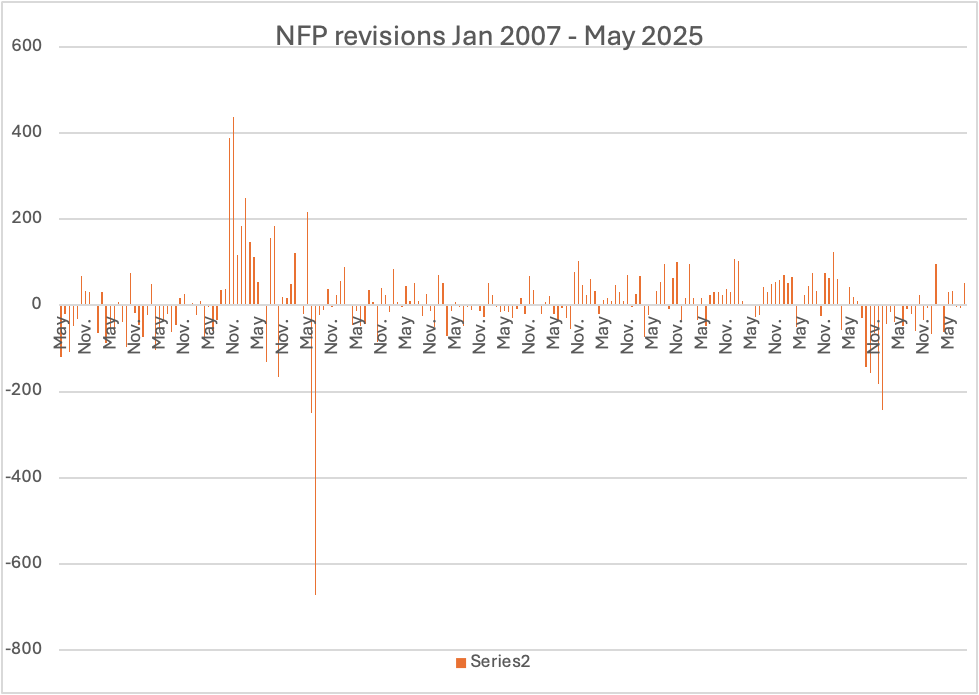

However, it is a fair question to ask if she was incompetent or politically motivated in her daily activities. After all, it is abundantly clear there are many government workers who are ostensibly non-partisan who are, in fact, highly partisan. As such, I took a look at the seasonally adjusted NFP data (the non-seasonally adjusted data is wildly volatile) to see if we could discern a pattern. I created the chart below from BLS data on revisions with May 2025, the latest month with the normal two revisions, on the left and January 2007, prior to the GFC, all the way on the right.

If you look on the left side of the chart, you can see a great many negative revisions. In fact, 21 of the last 29 months were revised lower from the original print. If we assume that the BLS models are unbiased, then one would expect a roughly equal distribution of both positive and negative revisions over time. It turns out, under the unbiased assumption, the probability of 21 out of 29 negative revisions is a very tiny 0.80%.

What conclusions can we draw from this? My first thought is that the BLS models are not very effective at modeling reality. I have raised this point many times in the past, the idea that the models that worked in the past, certainly pre-Covid, have been having trouble. This begs the question as to why an economist of Ms McEntarfer’s long experience didn’t seek to develop a more accurate model. As it is, there is no evidence that she did so. I imagine as a government employee, the idea that one should change something that exists within the government framework is quite alien. Thus, her competence could certainly be called into question, I think.

If we consider the alternative, that her actions were politically motivated, that will be more difficult to discern. However, given the predominance of Democrat voting members of the federal government and given the fact she was appointed to this position by President Biden, it is fair to assume she is not in favor of the current administration, at the very least. Now, during Mr Biden’s term, the initial NFP data was consistently better than expected, thus giving the impression that the economy was stronger than it may have otherwise been. After all, stories about revised data are usually on page 12 of the paper, not headline news. It is, therefore, possible that she was putting her proverbial thumb on the scale to flatter Biden’s economic performance. As to her likely distaste of Mr Trump, I expect that to the extent she had the ability to do so, weaker headlines and large negative revisions would be exactly her contribution.

However, the political issue is largely speculation on my part, although I would argue it is plausible. On the other hand, there is nothing in her background to suggest she is an especially thoughtful or creative economist and there is no indication that she examined the models she oversaw for flaws. In the end, I come down on incompetence driving a political motive. But I doubt we will ever know.

Now, it is not a very good look for a leader to proverbially kill the messenger, which is essentially what Trump did. Not surprisingly, much hair is on fire in the press and punditry, not because they though McEntarfer was particularly good at her job (I’m sure nobody had ever heard of her before) but because, as we have observed time and again, President Trump doesn’t follow their rules, and they don’t know what to do about it.

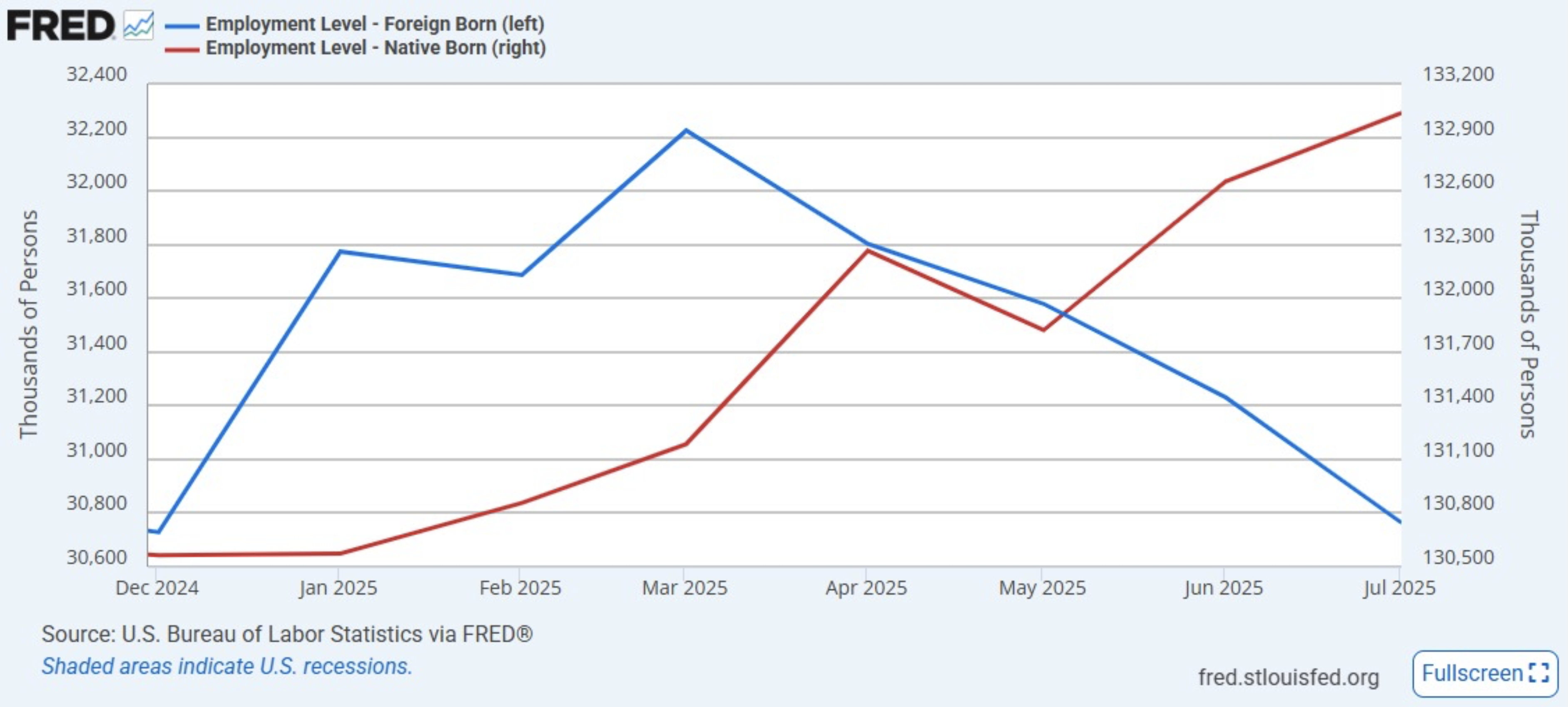

Will this matter in the end? This is merely the latest tempest in a teapot in my opinion and will do nothing to change the economy. However, there is one interesting feature of the employment situation that can be directly attributed to the immigration situation. As you can see in the FRED chart below, since March, the number of foreign-born workers has declined by 1.46 million while the number of US born workers has increased by more than 1.8 million. I would say that as long as American citizens are finding jobs, President Trump is likely to remain quite popular across the nation despite all the negative press.

The weak NFP report altered the narrative on Friday, with bond yields, equity markets and the dollar all tumbling and the probability of a September rate cut jumping to 80%. Perhaps President Trump is correct, and it is time to cut rates.

The year is now halfway completed While narrative writers repeated The story, same old, The dollar’s been sold ‘Cause global investors retreated

As well, they continue to scream Trump’s policies are too extreme His tariffs will drive Inflation to thrive While growth will soon start to lose steam

I don’t know about you, but this poet is tired of reading the same stories over and over from different pundits when it comes to the current macroeconomic situation. And so, I thought I might take a look at what the current narrative seems to be and, perhaps, analyze some of the reasons it will be wrong. I have full confidence it will be wrong because…it always is. Add to that the fact that the narratives continue to try to build on expectations of what President Trump wants to do and let’s face it, there is no more unpredictable political leader on the planet right now.

In fact, we can look at one of the key narratives that had been making the rounds right up until Thursday night when the House and Senate agreed the terms of the BBB which has since been signed into law. Serious pundits were convinced that the president could never get this done and yet there it is.

But let’s discuss another popular narrative, the end of American exceptionalism. First, I’d like to define the term American exceptionalism because I believe that the equity analysts borrowed the term from the Ronald Reagan. For the longest time, I would contend the term referred to the American experiment, writ large, with the dynamic market economy that was created by the legal framework in the US. After all, no other nation, certainly not these days, has anything like this framework. The combination of the 1st and 2nd Amendments to the Constitution have been critical in not only creating this framework but keeping it from getting too far out of hand.

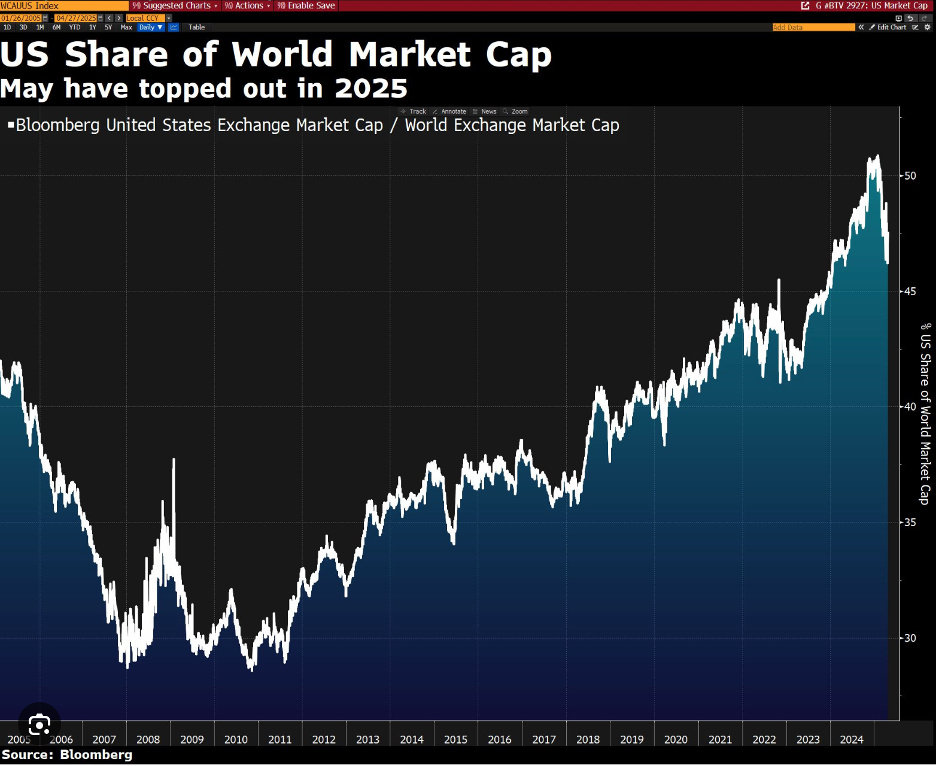

However, in the market context, American exceptionalism refers to the fact that the relative strength of the US economy drew investors from around the world into US equity markets, driving the value of US equities relative to both total global equities and the US proportion of global GDP to extreme heights. While the chart below shows a peak just above 50% of global market cap and that number is declining right now, I have seen estimates that the number could be as high as 70% of global market cap. I suppose it depends on how you define global market cap, but MSCI’s readings tend to be well respected.

In addition to the significant portion of equity market capitalization compared to the rest of the world is the fact that US GDP is a significantly smaller percentage, somewhere in the 23% – 26% range depending on how one calculates things with FX rates.

The upshot is that heading into 2025, US equity valuation was at least twice the size of the US economy compared to the entire world. Certainly, that is exceptional, and the term American exceptionalism seemed warranted. But as you can see from the first chart, other markets have been outperforming the US thus far this year with the result that the US no longer represents quite as large a percentage of the world’s equity market capitalization. So, is this the end of that form of American exceptionalism? The pundits are nearly unanimous this is the case.

A knock-on effect of this is that the dollar has been under pressure all year, having declined more than 10% vs. the DXY and 13% vs. the euro. In fact, a key factor in the weaker dollar thesis is that international investors are either selling their US stocks or hedging the FX exposure with either of those weighing on the dollar.

Source: tradingeconomics.com

Now, so far, that seems a logical conclusion and I cannot argue with it. However, as we look forward, is it reasonable to expect that to continue? In this instance, I think we need to head back to the BBB, which is undoubtedly going to provide significant economic stimulus to many parts of the economy (sorry green tech), and seems likely to help energy, tech and industrial companies continue to perform well. Much has been made of the idea that American exceptionalism has peaked but I wouldn’t be so sure. Net, I am not convinced the US ride is over, at least not for the economy, although segments of the equity market could well be in for a fall.

The other narrative that I continue to hear is that Trump’s policy mix, of tariffs and deportations is going to drive inflation much higher. In fact, Dr Torsten Sløk, who does excellent work, explained this weekend that tariffs would raise US CPI a very precise 0.3% this year. Of course, the problem with this story is that, thus far, inflation readings have been quite tame, falling since Liberation Day. It is certainly early in the game, but it is not at all clear to me that tariffs are going to be a major driver of inflation. First, many companies have decided to eat the cost themselves, notably Japanese car manufacturers. Second, M2 in the US has basically flatlined since April 2022 (see chart below), and if money supply is not growing, inflation will be hard-pressed to rise too quickly.

Now, it is certainly possible that the Fed increases the supply of money, although given the antagonism between Powell and Trump, I sense that the Fed will remain tighter for longer as they will make no effort to help the president if the economy starts to visibly slow down.

But, if I were to try to estimate what Trump’s end game is, I think the following chart is the most important.

This chart is the reason Donald Trump is our president, and it is one that the punditry does not understand. It is also the reason that US equities have performed so well. Corporate profit margins in the US have grown unabated since Covid.

Now, let’s put these two thoughts together. Corporate profit margins have exploded higher, currently at an all-time high of 10.23%. Meanwhile, the share of GDP that has gone toward labor has fallen dramatically since China entered the WTO. The result has been workers in the US have seen their incomes decline relative to corporate income. While it is true that, technically, the punditry is part of the work force, they are asset owners as opposed to Main Street who have far less invested in the equity markets. Ask yourself, how did corporates improve their margins so significantly? The combination of immigrant labor and moving production offshore weighed heavily on US wage growth. If you want to understand why President Trump is speaking to Main Street and using tariffs with reckless abandon it is because he is trying to adjust this process.

If he is successful, I expect that equity markets will lag other investments as those profit margins are likely to decline. If they just go back to pre-Covid levels of 6%, that represents a huge amount of money in the pockets of consumers. Do not be surprised if the result is solid economic growth with lagging profits and lagging equity prices. Too, a weaker dollar plays right into this game as it helps the competitiveness of US manufacturers both for domestic consumption and exports.

This is not the narrative, however. The narrative continues to be that Trump’s tariffs are going to generate significant inflation and drive the economy into a recession. In fact, just this morning I read that Professor Steven Hanke (a very smart fellow) now has a recession estimated at 80% to 90% probability. All the uncertainty is preventing activity as corporate managers hold back on making decisions, allegedly. Of course, now that the BBB is law, the tax situation is settled, and I will not be surprised to see investment return with clarity on that issue.

The narratives have been uniformly negative for a while. Part of that is because many of the narrative writers objectively despise President Trump and cannot abide anything he does. But part of that is because I believe the president is not focusing on the issues that market pundits have done for many years and instead is focusing on helping Main Street, not Wall Street. Perhaps that is why Wall Street political donations were heavily biased toward VP Harris and every other Democrat.

I hope this made some sense to you all, as I try to keep things in context. In addition, as it is Sunday evening, I expect tomorrow morning’s note to be quite brief. Love him or hate him, President Trump clearly hears the sounds of a different drummer than the rest of the political class and has proven that he can get what he wants. Do not ignore that fact.

With President Trump on the road The market has heard a boatload Of ideas and plans Including Iran’s Return to a more normal mode

There’s talk of a nuclear deal Audacious, if it’s truly real Instead of enriching While everyone’s bitching A partnership deal they would seal

One is never disappointed with the tone of the overnight news when President Trump is traveling. Between his flair for the dramatic and his desire to conclude deals, it seems like there is always something surprising when we awake each morning. This morning is no different.

While the mainstream media has been harping on the audacity of Qatar gifting a “flying palace” to the US for President Trump to use as Boeing’s delivery of the newest Air Force One is something like 10 years behind schedule, Mr Trump has indicated he is quite keen to make a deal with Iran that would bring them back into the fold of good neighbor nations. Ostensibly, Iran has suggested that they work with the Saudis, Emiratis and the US to enrich uranium together in order to develop nuclear power in the Middle East. As the Saudis and Emiratis have already expressed interest in building more nuclear power plants, it is not a stretch for them. But bringing Iran into the fold, so that enrichment activities are done jointly, and therefore can be closely overseen by the US and Saudi Arabia, would be a remarkable outcome.

The JCPOA deal signed by President Obama was a nullifying deal, one that was designed to prevent an activity, the enrichment of uranium to the required concentrations sufficient to build a bomb. But this is an encompassing deal, one that would join erstwhile enemies into a partnership to jointly produce uranium sufficiently enriched for nuclear power, without pushing toward weapons grade material. Now, this would be a remarkable change in attitude in Tehran as the theocracy there has basically made the end of the US and Israel their motto ever since 1979 and the revolution that brought them to power. But things are tough in Iran right now and the funny thing about power is that those who hold it are really reluctant to let go. It would not be unprecedented for a nation’s leadership to reverse course completely in order to maintain their grip, and it is also not hard to believe that a softer tone would be welcome in Iran by the populace.

Regardless, this is a bold and audacious idea, but one that could just work. Now, we should all care not simply because anything that could lead to less terrorism and destruction is an unalloyed good, but because the impact on the global economy would be significant, namely, the price of oil is likely to decline further. A deal like this is likely to include the end of restrictions on Iranian oil sales, or at least a dramatic reduction in those restrictions. While Iran has been producing and selling oil all along this would change the tone of the oil market with another major player now actively looking to expand production and sales. (After all, the Iranian economy is desperate and the ability to generate more revenue without restrictions would be an extraordinary carrot for the mullahs.)

With this in mind, it should be no surprise that the price of oil (-3.65%) has fallen sharply today, and the real question is just how low it can go. A look at the chart shows that the trend has been lower for the past year although it seems to have found a temporary bottom just above $56/bbl.

Source: tradingeconomics.com

I have maintained for the past year and a half that the ‘peak cheap oil’ thesis has been faulty and that there is plenty of the stuff around with political, not geological restrictions the driving force toward higher prices. This is Exhibit A on the political restriction case. President Trump is quite keen to see oil prices lower as it suits both the inflation story in the US as well as offers a significant advantage to US manufacturing facilities with access to cheap energy. I would guess this was not on anyone’s bingo card before today but must now be taken seriously as a potential outcome. While I’m not an oil trader, I suspect we will test, and break, through those lows just above $56 in the coming weeks and find a new home closer to $50/bbl.

This is such an extraordinary story, I could not ignore it. But as an aside, President Trump also mentioned that India has allegedly offered to cut their tariff rates on US goods to 0.0%! I don’t know if that would be reciprocal, and that has not yet been verified by India, but again, it demonstrates that many of the things we believed to be true regarding international relations are not carved in stone.

Ok, let’s look at how markets are absorbing these latest surprises. Yesterday’s price action could best be described as dull, with US equity markets doing little all day, although the NASDAQ managed to edge higher into the close. In Asia overnight, the major markets (Japan -0.9%, China -0.9% and Hong Kong -0.8%) all came under pressure although there doesn’t appear to have been a particular story. There were no new trade related comments, so I sense that the recent uptick just saw some profit-taking. Elsewhere in Asia, the biggest winner was India (+1.5%) and then it was a mixed bag. In Europe, equity markets have done very little overall after Eurozone data showed GDP activity was more disappointing than first reported with Q1’s second estimate down to 0.3%. As to US futures, at this hour (7:10), they are pointing lower by about -0.4% or so across the board.

In the bond market, Treasury yields, which have been climbing relentlessly all month as per the below chart, have backed off -2bps this morning, but 10-year yields are still above 4.50%, a level Mr Bessent is clearly unhappy with. But today’s price action has also seen European sovereign yields slide a similar amount, with the softer Eurozone growth one of the reasons here as well.

Source: tradingeconomics.com

Turning to the metals markets, the shine is off gold (-0.2%) which has fallen more than 4% in the past week, although remains well above $3100/oz. It seems that much of the fear that drove the price higher is being removed from the markets by the constant updates of trade and peace deals that we hear regularly. It remains to be seen if this lasts, and how the Fed will ultimately behave, but for now, fear is fading.

Finally, the dollar is a touch softer overall, but not universally so. In the G10, the euro (+0.2%) and pound (+0.2%) are both edging higher with UK data looking a tad better compared to that modest weakness in Eurozone data. But the yen (+0.6%) and CHF (+0.5%) are both nicely higher as there continues to be a strong belief that President Trump is seeking the dollar to decline in value. In the EMG bloc KRW (+0.7%) and ZAR (+0.8%) are the leaders with most of the rest of the bloc making very modest gains on the order of 0.2% or less. It appears that the dollar has decoupled from the US rate picture for the time being. I wonder if it is presaging lower US rates, or if this relationship is going to change for a longer time going forward. We will need to watch this closely.

On the data front, there is a bunch this morning as well as comments from Chairman Powell at 8:40.

Initial Claims

229K

Continuing Claims

1890K

Retail Sales

0.0%

-ex autos

0.3%

PPI

0.2% (2.5% Y/Y)

-ex food & energy

0.3% (3.1% Y/Y)

Empire State Manufacturing

-10

Philly Fed Manufacturing

-11

IP

0.2%

Capacity Utilization

77.8%

Source: tradingeconomics.com

I don’t see PPI as having much impact, but Retail Sales will get some discussion as will the manufacturing indices as weakness there will help the negative narrative that some are trying to portray. Net, though, the story seems likely to continue to be the announcements of deals as they come in. It is not clear to me that they will all be net positives, and I believe that much positivity has already been absorbed so we will need to see data that backs up the narrative and that could take a few quarters. In the meantime, my lower dollar thesis seems to fit better today. That’s my story and I’m sticking to it!

Confusion continues to reign O’er markets though pundits will feign That they understand The movements at hand Despite a quite rocky terrain

The speed with which Trump changes views Can even, the algos, confuse The pluses, I think Are traders must shrink Positions, elsewise pay high dues

For the longest time I believed that the algos were going to usurp all trading activity as their ability to respond to news was so much faster than any human. Certainly, this has been the key to success for major trading firms like Citadel and Virtu Financial. And they have been very successful. I think part of their success has been that we have been in an environment where both implied and actual volatility has declined in a secular manner, so not only could they respond quickly, but they could lever up their positions with impunity as the probability of a large reversal was relatively less.

However, I believe that the algos and their owners may have met their match in Donald Trump. Never before has someone been so powerful and yet so chaotic in his approach to very important things. Many pundits complain that even he doesn’t have a plan when he announces a new policy. But I think that’s his secret, keep everyone else off balance and then he has free reign. Chaos is the goal.

The market impact of this is that basically, for the past three months since shortly after his election, the major asset classes of stocks, bonds and the dollar, have chopped around a lot, but not moved anywhere at all. How can they as nobody seems willing to believe that the end game he has explained; reduced deficits, reduced trade balance, lower inflation and a strong military presence throughout the Western Hemisphere, is going to result from his actions. And in fairness, some of the actions do have a random quality to them. But if we have learned nothing from President Trump’s time in office, including his first term, it is that he is very willing to tell us what he is going to do. It just seems that most folks don’t believe he can do it so don’t take it seriously.

So, let’s look at how markets have behaved in the past three months. The noteworthy result is that the net movement over that period has been virtually nil. Look at the charts below from tradingeconomics.com:

S&P 500

10-Year Treasury

EUR/USD

While all these markets have moved higher and lower in the intervening period, they have not gone anywhere at all. The biggest mover over this time is the euro, which has rallied 0.54% with the other major markets showing far less movement than that.

One interesting phenomenon of this price action is that despite significant uncertainty over policy actions by the President and the implications they may have on markets, and even though recent price action can best be described as choppy rather than trend like, the VIX Index remains in the lowest quartile of its long-term range. Certainly, it has risen slightly over the past few weeks, but to my eye, it looks like it is underpricing the chaos yet to come.

Source Bloomberg.com

While I have no clearer idea how things will unfold than anyone else, other than I have a certain amount of faith that the President will achieve many of his goals in one way or another, I am definitely of the belief that volatility is going to be the coin of the realm for quite a while going forward. We have spent the past many years with numerous strategies created to enhance returns via selling volatility, either shorting options or levering up, and that is the trend that seems likely to change going forward. The implication for hedgers is that maintaining hedge ratios while having a plan in place is going to be more important than any time in the past decade or more.

Ok, let’s take a look at how markets did move overnight. Yesterday’s net negative session in the US was followed by similar price action in Asia. Tokyo (-1.4%), Hong Kong (-1.35) and China (-1.1%) all suffered on stories about tariffs and extra efforts by the Trump administration to tighten up export controls on semiconductors. It should be no surprise that virtually every index in Asia followed suit with losses between -0.3% (Singapore) and -2.4% (Indonesia) and everywhere in between. Meanwhile, in Europe, the picture is not as dour as there are a few winners (Spain +0.9% and Italy +0.5%) although the rest of the continent is struggling to break even. The data point that is receiving the most press is Eurozone Negotiated Wage Growth (+4.12%) which rose less than in Q3 and has encouraged many to believe the ECB will be cutting rates next week. Interestingly, Joachim Nagel, Bundesbank president was on the tape telling the rest of the ECB to shut up about their expectations of future rate moves as there is still far too much uncertainty and decisions need to be made on a meeting-by-meeting basis. Apparently, oversharing is a general central bank affliction, not merely a Fed problem. As to US stocks, at this hour (6:50) they are little changed.

In the bond market, yields continue to slide, at least in the US, with Treasury yields down -6bps this morning and back to levels last seen in December. Apparently, some investors are beginning to believe Secretary Bessent regarding his goal to drive yields lower. As well, he has reconfirmed that there will be no major increase in the issuance of long-dated paper for now. European sovereigns, though, are little changed this morning with only UK gilts (-3bps) showing any movement after the CBI Trades report printed at -23, a bit less bad than expected.

In the commodity markets, oil (-0.15%) is little changed this morning after a very modest rally yesterday. But the reality here is that oil, like other markets, has been in a trading range rather than trending, although my take is that the longer-term view could be a bit lower. Gold (-0.35%), though lower this morning, is the one market that has shown a trend since Trump’s election, and truthfully since well before that as you can see in the chart below.

Source: tradingeconomics.com

Finally, the dollar is a touch softer this morning, with both the euro and pound rising 0.3% alongside the CHF (+0.3%) and JPY (+0.2%). Commodity currencies, though, are less robust with very minor losses seen in MXN, ZAR and CLP. Given the decline in 10-year yields, I am not that surprised at the dollar’s weakness although it is in opposition to the gut reaction that tariffs mean a higher dollar. This is of interest because yesterday President Trump confirmed that the 25% tariffs on Canada and Mexico were going into effect next week. As I explained above, it is very difficult to get a sense of short-term price action here although given the clear intent of the president to improve the competitiveness of US exporters, he would certainly like to see the dollar decline further.

It is very interesting to watch this president reduce the power of the Fed with words and not even have to attack the Chairman like he did in his first term. It will be very interesting to see how Chair Powell responds to the ongoing machinations.

On the data front, this morning brings only the Case-Shiller Home Price Index (exp +4.4%) and Consumer Confidence (102.5). We do hear from two Fed speakers, Barr and Barkin, but as I keep explaining, their words matter less each day. (It must be driving them crazy!)

It is hard to get excited about markets here. There is no directional bias right now and the lack of critical data adds to the lack of information. As well, given the mercurial nature of President Trump’s activities, we are always one tape bomb away from a complete reversal. While I don’t see the dollar collapsing, perhaps the next short-term wave is for further dollar weakness.