Right now, markets keep taking risk

And lately, the pace has been brisk

But coming next week

We could see a peak

If there’s no cash left in the fisc

A government shutdown would raise

Concerns about ‘nomic malaise

As well, what I see

Is Trump’s OMB

Is planning a RIF anyways

Volatility remains absent from most markets these days, metals excepted, and given the dearth of data until tomorrow’s PCE report, the focus is beginning to turn elsewhere. Perhaps the biggest story developing right now is the potential US government shutdown if no continuing resolution is passed by Congress. The government’s fiscal year runs from October 1 through September 30, and the rules are if Congress hasn’t passed appropriations bills by the end of the fiscal year, nonessential services are ended, and government employees are furloughed until that process is completed. As of right now, the House of Representatives has passed a clean bill, meaning it continues spending at the current rate, and we are all awaiting on the Senate. However, the Senate needs 60 votes to pass it to overcome the filibuster and right now, the Democratic Minority Leader, Chuck Schumer, claims they will not support the bill.

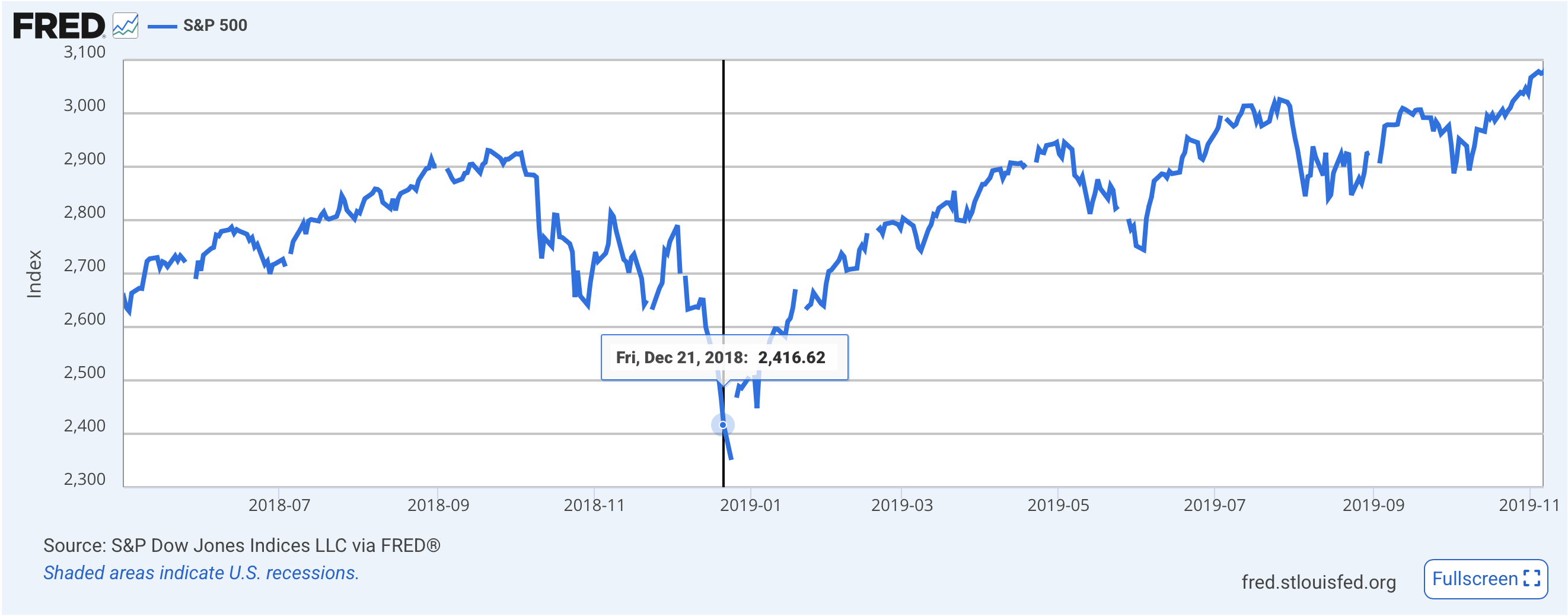

First, understand this is not unprecedented. In fact, according to Grok, it has happened 21 times since 1980 with the longest being 35 days in 2018-19 over funding for the border wall. Now, I ask you, can anyone remember the impact of any of those shutdowns, which in fairness typically last less than a week?

Next, it is worth understanding what actually happens during a shutdown. National Parks are closed, while passport services, HUD services, SBA services, scientific research and EPA inspections are the type of things that are put on hold. Also, the BLS will pause data collection and calculations, although given their recent track record, that may be seen as a benefit! But things like Social Security, Medicare, Medicaid and the Military are all unaffected.

Naturally, there is a lot of politicking ongoing with this process and apparently, President Trump has given marching orders for departments to begin a RIF if the government is shut down. So, when things reopen, there will be fewer federal employees, one of the goals of this administration, and something that is anathema to his opponents.

From a market perspective, the impact on equity markets during the December 2018 – January 2019 shutdown was actually a rally of just over 10%, although the market did decline in the month leading up to the shutdown. My point is, there is a lot more politics than economics in this process.

But away from that story, commodities remain the market with the most interest as oil (-0.5%) continues to trade within the range I highlighted earlier this week with a top at $65.50, but has made a technical break above its 50-day moving average, which has the bulls starting to get excited. As well, the backwardation of the curve is increasing, another bullish sign and much of this is being laid at the feet of President Trump’s seeming turn on the Russia/Ukraine war, where he is quite tired of President Putin’s dissembling. Certainly, a break above that range top would be at least short term bullish for crude.

Source: tradingeconomics.com

As to the precious metals, while gold continues to trade well, silver has taken the mantle and as you can see from the chart below, is accelerating higher at an even more impressive clip than the yellow metal. This is a common occurrence as silver historically outperforms gold, on a percentage basis, when both are in bull markets like this. Just wait until it reaches $50/oz, and makes new all-time highs, and you will see even more discussion of the metals and why they are rallying with inflation concerns a major part of that discussion.

Source: tradingeconomics.com

Meanwhile, financial instruments are far less exciting lately with equity markets stabilizing after their recent run and bond markets also doing little. Granted, we have seen two consecutive down days in US equity markets, but the magnitude of the decline was de minimis, so it is not really telling us very much. European markets appear more closely linked to the US, with all bourses there lower by between -0.1% and -0.5% this morning although we did see some modest gains in Asia (China +0.6%, Japan +0.3%). Net, it seems investors are not certain where to turn right now and are waiting for more clarity from the Fed as to whether more rate cuts are on the way.

The same is true of bond investors who apparently are unconcerned over the shutdown threats, with yields unchanged despite the increasingly combative rhetoric. We did hear from SF Fed president Daly yesterday, a known dove, who explained that she is coming around to the idea that more cuts are necessary, and they were simply waiting to see how tariffs were going to impact things. I might argue that she is anxious to cut rates but also doesn’t want to seem to support President Trump’s demands.

Finally, the dollar, after a pretty solid rally yesterday, is essentially unchanged this morning as well. (That seems to be the theme today, no change.). As I look across my screen, the largest move I see is 0.15%, which is how far CHF has declined on the session, otherwise things have been completely dead.

On the data front, this morning brings the weekly Initial (exp 235K) and Continuing (1930K) Claims data as well as Durable Goods (-0.5%, 0.0% ex-Transport) and the final Q2 GDP reading (3.3%) all at 8:30 with Existing Home Sales (3.96M) at 10:00. Yesterday saw New Home Sales rise dramatically more than expected at 800K although most analysts expect that number to be revised lower as the Census Bureau gets more information. Nonetheless, it is a sign that the economy is not collapsing, that’s for sure.

We also hear from four more Fed speakers today, Williams, Bowman, Barr and Daly again, and we will need to see how they all interpret the current situation. We learned from the dot plot that there are a lot of different opinions at the Fed right now, and personally, I am very glad to see that. Given the overall confusion, and the asynchronous nature of the economy right now, it would be more concerning if everyone was on the same page.

As far as the shutdown is concerned, you can be sure that this process will continue until next Tuesday night, at the earliest, if the Democrats cave, and if not, we will then be bombarded by both sides claiming it is the other side’s fault. Eventually a spending bill will be passed, and as we saw back in 2019, markets pretty much look through this stuff. Meanwhile, unless the data starts to really deteriorate and brings Fed comments along for that ride, I think the dollar is probably in a rough equilibrium space for now.

Good luck

Adf