The NFP data was weak

And President Trump did critique

The BLS head

But unlike the Fed

He axed her as pundits did freak

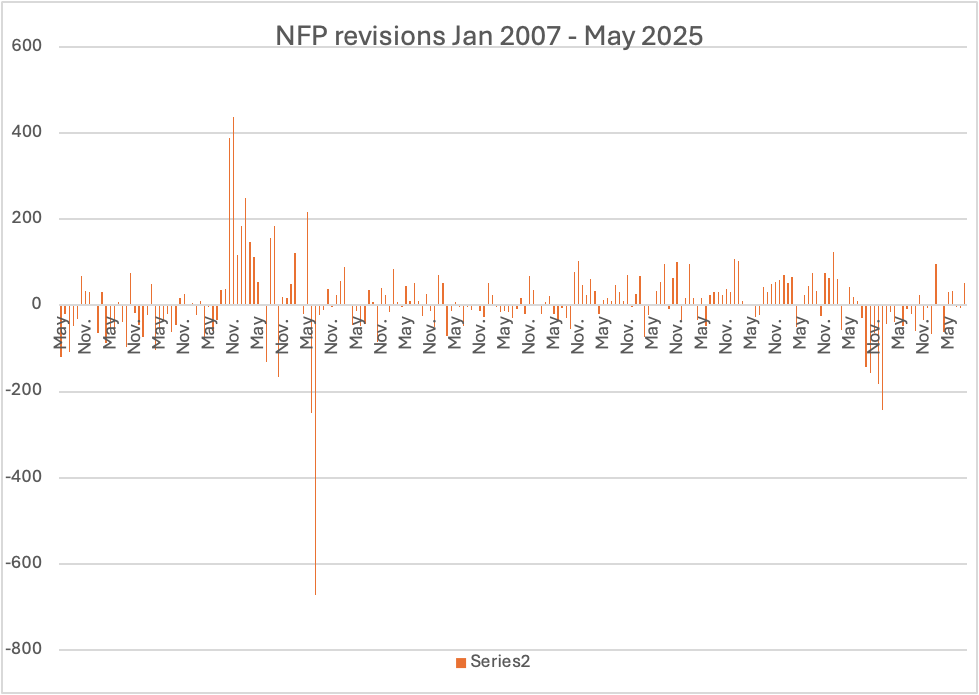

However, it is a fair question to ask if she was incompetent or politically motivated in her daily activities. After all, it is abundantly clear there are many government workers who are ostensibly non-partisan who are, in fact, highly partisan. As such, I took a look at the seasonally adjusted NFP data (the non-seasonally adjusted data is wildly volatile) to see if we could discern a pattern. I created the chart below from BLS data on revisions with May 2025, the latest month with the normal two revisions, on the left and January 2007, prior to the GFC, all the way on the right.

If you look on the left side of the chart, you can see a great many negative revisions. In fact, 21 of the last 29 months were revised lower from the original print. If we assume that the BLS models are unbiased, then one would expect a roughly equal distribution of both positive and negative revisions over time. It turns out, under the unbiased assumption, the probability of 21 out of 29 negative revisions is a very tiny 0.80%.

What conclusions can we draw from this? My first thought is that the BLS models are not very effective at modeling reality. I have raised this point many times in the past, the idea that the models that worked in the past, certainly pre-Covid, have been having trouble. This begs the question as to why an economist of Ms McEntarfer’s long experience didn’t seek to develop a more accurate model. As it is, there is no evidence that she did so. I imagine as a government employee, the idea that one should change something that exists within the government framework is quite alien. Thus, her competence could certainly be called into question, I think.

If we consider the alternative, that her actions were politically motivated, that will be more difficult to discern. However, given the predominance of Democrat voting members of the federal government and given the fact she was appointed to this position by President Biden, it is fair to assume she is not in favor of the current administration, at the very least. Now, during Mr Biden’s term, the initial NFP data was consistently better than expected, thus giving the impression that the economy was stronger than it may have otherwise been. After all, stories about revised data are usually on page 12 of the paper, not headline news. It is, therefore, possible that she was putting her proverbial thumb on the scale to flatter Biden’s economic performance. As to her likely distaste of Mr Trump, I expect that to the extent she had the ability to do so, weaker headlines and large negative revisions would be exactly her contribution.

However, the political issue is largely speculation on my part, although I would argue it is plausible. On the other hand, there is nothing in her background to suggest she is an especially thoughtful or creative economist and there is no indication that she examined the models she oversaw for flaws. In the end, I come down on incompetence driving a political motive. But I doubt we will ever know.

Now, it is not a very good look for a leader to proverbially kill the messenger, which is essentially what Trump did. Not surprisingly, much hair is on fire in the press and punditry, not because they though McEntarfer was particularly good at her job (I’m sure nobody had ever heard of her before) but because, as we have observed time and again, President Trump doesn’t follow their rules, and they don’t know what to do about it.

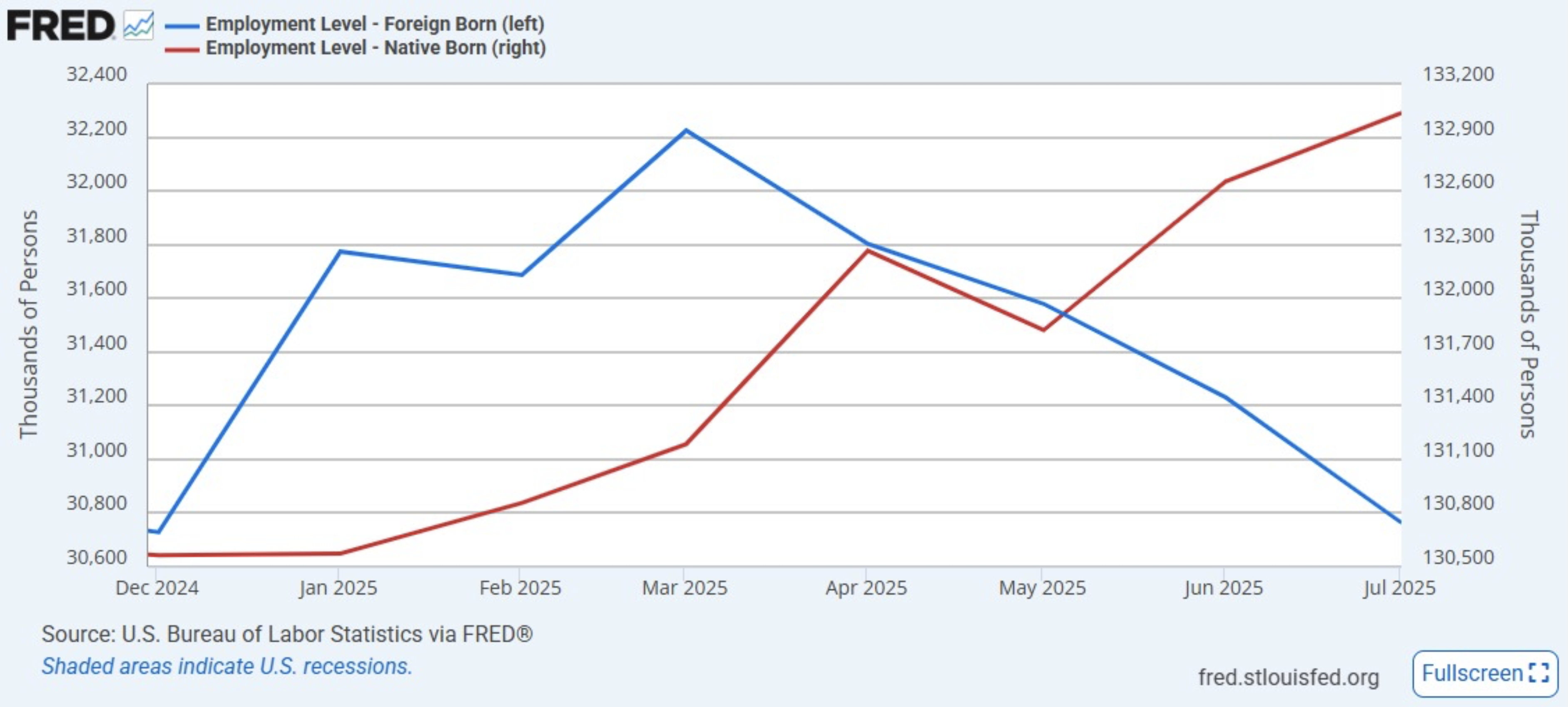

Will this matter in the end? This is merely the latest tempest in a teapot in my opinion and will do nothing to change the economy. However, there is one interesting feature of the employment situation that can be directly attributed to the immigration situation. As you can see in the FRED chart below, since March, the number of foreign-born workers has declined by 1.46 million while the number of US born workers has increased by more than 1.8 million. I would say that as long as American citizens are finding jobs, President Trump is likely to remain quite popular across the nation despite all the negative press.

The weak NFP report altered the narrative on Friday, with bond yields, equity markets and the dollar all tumbling and the probability of a September rate cut jumping to 80%. Perhaps President Trump is correct, and it is time to cut rates.

That’s all for this special Sunday night edition.

Good luck

Adf