Inflation has now been defeated

At least that’s the mantra repeated

By equity bulls

Who’re buying bagfuls

Of stocks which last week had depleted

But what if the data today

Does not show inflation’s at bay?

Will pundits still call

For Fed funds to fall

Or will cooler heads get their way?

As last week fades into the mists of memory, the narrative writers have been hard at work reimposing the soft-landing thesis and how the Fed is going to ride to the rescue of what seems to be slackening data across most aspects of the economy. The latest piece of information was yesterday’s PPI numbers that indicated, at the producer level, price pressures were ebbing further. In fact, the core PPI reading for July was 0.0%, a huge victory for the Fed as it continues to add to the story that their timely behavior and strength of will have been having the desired effects. And maybe they have been doing just that, although there is reason to believe that other things are happening.

Regardless, with the much more important CPI data set to be released this morning, if those PPI numbers are “confirmed” with lower than forecast CPI numbers, there will be no stopping the equity rebound/rally and expectations for a 50bp cut at the September meeting will run rampant. The current median forecasts, according to tradingeconomics.com are:

- Headline (0.2%, 3.0% Y/Y); and

- Core (0.2% (3.2% Y/Y).

Almost by definition, at least half of the punditry is looking for a headline print with a 2 handle, substantially closer to the Fed’s target than we have seen since March 2021. The basis of this view is that shelter costs are going to continue to trend lower and there is a growing expectation that used car prices are also destined to head lower. Given the way that shelter costs are implemented in the CPI calculations, I have no opinion on how recent activity will impact the overall results. However, the anecdata that comes from my neighborhood shows that homes continue to sell over asking prices in short order and that there is no sign of prices declining yet. I know that what happens here is not necessarily occurring elsewhere in the country, but it is unlikely to be entirely unique. I guess we’ll all see the answer at 8:30.

In the meantime, the market story has been twofold, equity bulls are basking in the glow of the rebound from last week’s dramatic declines and the interest rate doves are completely willing to ignore actual Fed commentary and are increasing their bets that the Fed starts this cutting cycle with a 50bp reduction.

As can be seen in the graphic below from the cmegroup.com website, the 50bp cut story is slightly more than a coin flip at the moment.

But the interesting thing is to see how this pricing has evolved over the past month. Looking at the table at the bottom of the graphic shows that last week, in the wake of the Japanese market selloff, the belief was much stronger that a 50bp cut was on the way (in fact, on July 5th, that probability was >90%), but a month ago, it was a very low probability event. Back then, it was only the true believers in an upcoming recession that were looking for 50bps. But now, it is mainstream thinking, at least among the punditry. Yesterday, Atlanta Fed president Raphael Bostic explained, “we want to be absolutely sure. It would be really bad if we started cutting rates and then had to turn around and raise them again.” However, he did acknowledge that he is likely to be ready to cut “by the end of the year.” While I have never met Mr Bostic, this does not sound like a man who is desperate to cut interest rates soon, narrative be damned.

Ok, away from all the huffing and puffing on US CPI, we did get some other important news overnight. The first thing was the RBNZ surprised many folks by cutting their Official Cash Rate by 25bps. Apparently, they are concerned with slowing growth and gratified that inflation appears to be slowing. The upshot was that the NZD (-1.0%) fell sharply and the local stock market rallied more than 2%.

Elsewhere, UK inflation was released at a lower than expected 2.2% for July. While that was an uptick from the June level of 2.0%, the fact that it was lower than both the BOE and Street expectations, and that services inflation rose “only” 5.2%, down from the 5.7% reading in June, has traders increasing their bets for a rate cut in September. The pound (-0.2%) did slip slightly on the report but remains modestly higher on the year. As to the FTSE 100, its 0.3% gain pales in comparison to the type of movements we have been seeing in equity markets elsewhere.

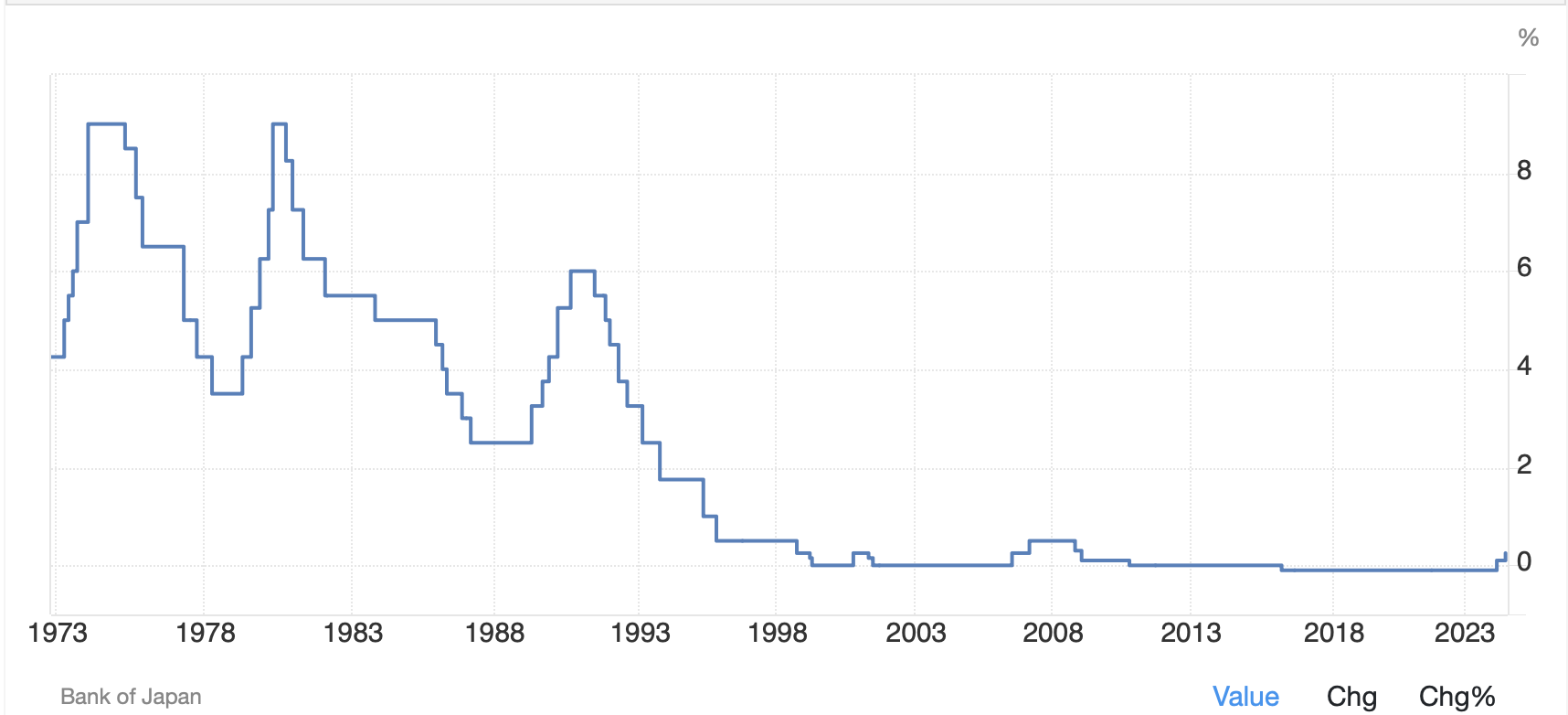

The zephyrs of change

Are blowing throughout Japan

Kishida’s leaving

One last piece of news is that Japanese PM, Fumio Kishida, has announced that he will not be running for LDP party leadership, the critical post to become (or in his case remain) Prime Minister. A series of fundraising scandals has dogged his entire administration, and his approval rating remains below 30%. The market take is that his leaving will enable the BOJ to act more aggressively, at least according to some local analysts and all depending on who wins the election. While several of the mooted candidates are on record as calling for more monetary policy normalization (i.e. rate hikes), they are not the leading candidates at this time. It seems early to make that case in my mind. In the meantime, while the BOJ may want to raise rates, I think they are going to wait for more rate cutting in the rest of the G10, specifically from the Fed, before considering their next move. Net, the yen’s response to this story has been nil, although we did see Japanese equities rally (Nikkei + 0.6%).

Elsewhere in equity markets, both the Hang Seng (-0.35%) and CSI 300 (-0.75%) continue to languish relative to other markets around the world as the prospects for the Chinese economy, and by extension its companies, remains lackluster, at best. The absence of any significant Chinese stimulus remains a weight on the economy and the markets there. However, most other markets in Asia rallied nicely overnight, following the US price action yesterday. As to European bourses, they are all green, but the movements have been modest, on the order of 0.3% or so, as Eurozone economic data continues to disappoint (IP -0.1% in June, exp +0.5%). As to US futures, ahead of the CPI data, they are essentially unchanged.

In the bond market, Treasury yields continue to grind lower, falling 7bps after the PPI data yesterday and down another basis point ahead of the CPI today. European sovereign yields, though, are slightly higher this morning, between 1bp and 2bps, which based on the data makes no sense. But the moves are small enough to be irrelevant. One outlier here is UK Gilt yields, which have declined 4bps on the softer inflation print.

Oil (-0.2%) which suffered yesterday has stopped falling for the moment as the market remains on tenterhooks regarding a possible Iranian attack on Israel. In the meantime, expectations are for a further draw of oil inventories in the US, although the industry continues to pump an extraordinary 13.4 million bpd despite all the efforts of the current administration to stifle it. As to the metals markets, gold (+0.4%) continues to find support and is pushing toward new highs yet again. This morning it is taking the rest of the metals complex with it, although that could be a result of the dollar’s modest weakness.

Finally, the dollar is a bit softer overall this morning, but there are several idiosyncratic stories. We’ve already mentioned NZD, GBP and JPY. However, the euro (+0.25%) is now at its highest level of 2024 and back above 1.10. Meanwhile, the commodity currencies are mostly firmer vs. the dollar this morning (ZAR +0.3%, MXN +0.3%, NOK +0.6%, SEK +0.5%) although Aussie (-0.2%) is bucking that trend. One other noteworthy mover is CNY (+0.2%) which has been showing far more volatility than normal in the past two weeks. It seems it is still coming to grips with the Japanese story as well.

And that’s really it for the day. There are no Fed speakers on the calendar, but we must always be aware of some unscheduled interview. Remember, they love to talk. Right now, I would say the market is looking for softer inflation data and is pricing accordingly. As such, if this data is even modestly warm, let alone hot, be ready for some quick reversals, at least early in the session. So, stocks lower with bonds while the dollar climbs. But based on the current zeitgeist, I have to believe that any dip will be bought with reckless abandon.

Good luck

Adf