Well, Jay and the Fed cooed like doves

And treated the bulls with kid gloves

But under the hood

Was it quite so good?

It’s clear number up’s what he loves!

The upshot is stocks really soared

As everyone’s sure Jay’s on board

To cut first in June

And thrice when Cold Moon

Is seen, near the birth of our Lord

Whatever the pundits thought about the hottish inflation readings in January and February, they clearly did not read the room properly, at least not the room in the Eccles Building. Despite raising their 2024 forecasts for GDP growth (2.1% from 1.4%) and Core PCE (2.6% from 2.4%), as well as maintaining their forecast for the Unemployment Rate to remain quiescent (4.0% to 4.1%), they are hell-bent on cutting rates this year, with June still the most likely starting point. I created a little table to show, however, that perhaps the consensus is not quite what the headlines would have you believe.

| Dec | Mar | |||

| Median | Avg | Median | Avg | |

| 2024 | 4.625 | 4.704 | 4.625 | 4.809 |

| 2025 | 3.625 | 3.612 | 3.875 | 3.783 |

| 2026 | 2.875 | 2.947 | 3.125 | 3.066 |

| Longer Term | 2.500 | 2.586 | 2.625 | 2.813 |

Source: Data FRB, calculations @fx_poet

The highlighted points show that while the median for 2024 remained the same, the average was nearly a full cut less. In fact, if one more member had adjusted their forecast higher, the median would have come out for just 2 cuts this year. But as I wrote yesterday, perhaps of more importance is the Longer Term view, where not only did the median rise by 12.5bps, but the average is substantially higher, a full 25bps higher than the December views.

However, the market has ignored this wonkish number crunching and accepted the numbers at face value; three cuts this year and three more next year helping drive equity prices to yet another set of new all-time highs.

Regarding the tapering of the balance sheet, Powell explained at the press conference that they had, indeed, discussed the topic as they were trying to determine the best way to continue the process without any untoward events, but that is not the issue. The issue is…BUY STONKS!!!

I would estimate that Chairman Powell is pretty happy with the outcome and am certain that Secretary Yellen is very happy with the outcome. After all, the equity rally continued while bond yields managed to drift lower by a couple of basis points. But the really happy campers are the holders of gold which rallied more than 1% and traded above $2200/oz for the first time ever. The market has reviewed this outcome and decided that the biggest risk going forward is a further devaluation of the dollar vs. stuff, although vs. other fiat currencies it is likely to hold its own. In other words, inflation ain’t dead. I expect the bond market to determine this is the case over the next several weeks and see yields rising further, especially if the PCE data next week is hot again.

While Jay may have had the most press

In Switzerland, Tom did aggress

He cut twenty-five

In order to drive

Their growth with a bit more largesse

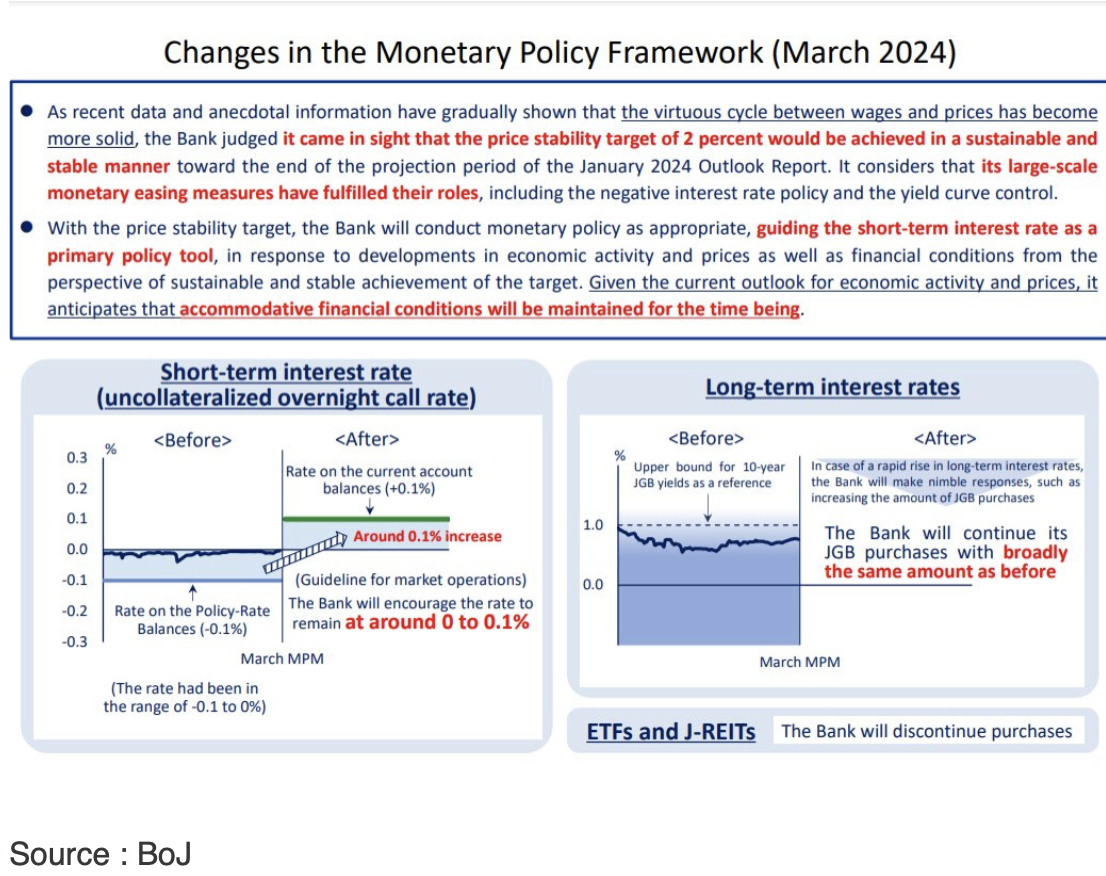

This morning, we have seen three more G10 central banks and the only surprise comes from Switzerland, where soon-to-retire President, Thomas Jordan, cut their base rate by 25bps to 1.50%. While there were several analysts who had suggested this might be the case (including this poet on Monday), the bulk of the market was in the no change camp. However, cut they did, and the result was an immediate 1.1% decline in the Swiss franc, arguably a key part of their goal. In the statement, they explained that inflation had been well within their target range, and they would have the tool of further currency intervention if they felt the franc was weakening too much.

One theory on the surprise cut is that the SNB wanted to get ahead of the pack as they only meet 4 times each year and their next meeting is after the June Fed and ECB meetings. As well, many pundits are now saying this is the “proof” that the Fed and ECB are going to cut in June. My take is that while I agree the ECB is a done deal come June, I think the Fed may have a tougher time as there is still no evidence that inflation is heading back to their 2% target. We have two more CPI and PCE reports before the June meeting, and if the recent price activity continues (and given energy prices remain buoyant I expect they will), it will be very difficult for Chair Powell to explain the need to cut rates unless Unemployment is surging. Perhaps that will be the case, but right now, the data does not indicate things are collapsing. The next three months should be quite interesting.

Ok, let’s see how other markets have responded to Powell and the SNB surprise. Equity markets are in a happy place right now after records fell in the US yesterday. The Nikkei (+2.0%) also set a new record and the Hang Seng (+1.9%) continued its recent rebound. In fact, only mainland Chinese stocks couldn’t muster a rally last night, with every other nation in APAC in the green, often by more than 1%. In Europe, though, the picture is a bit more mixed with more gainers than losers, but still several nations seeing modest pressure on their equity indices. It should be no surprise that Swiss stock markets are higher, but France and Denmark are suffering somewhat today. The best performer is the UK (+0.9%) which seems to be benefitting from a solid uptick in its Flash Manufacturing PMI (49.9, exp 47.8). Lastly, in what should not be a surprise at all, US futures are pointing higher across the board.

In the bond market, all is right with the world this morning as there are bids everywhere with yields declining correspondingly. Treasury yields slipped another 4bps overnight and throughout Europe, we are seeing declines between 3bps and 5bps with Swiss bonds lower by 7bps. In fact, Asia is where things were modestly different as JGB’s remain unchanged (tighter policy remains an idea not a reality yet) and Australian yields rose after much stronger than expected employment data was released last night.

In the commodity space, oil (-0.25%) is a touch softer after a decline of more than 1% during yesterday’s session. With all the focus on the Fed, there was not a lot of news driving things here specifically. But the real winner in the commodity space is gold (+1.0%) as the market appears to be calling BS on the Fed’s inflation and QT forecasts. The thing to remember about gold is it is not so much a good hedge for consumer inflation, but it is a very good hedge for monetary inflation (i.e. the excess printing of money). While those two inflations tend to be correlated, they are not tick for tick, so gold seems to be amiss at times. But the very idea that despite ongoing inflationary pressures, and the continued supplying of liquidity by the global central banking cast, is the right time to cut interest rates is a step too far for gold markets. I believe this has room to run higher. As well, copper (+0.7%) is also rebounding, and I expect that we will see most commodities continue to perform well going forward in this environment.

Finally, the dollar is under some pressure this morning, adding to yesterday’s declines in the wake of the Fed meeting. Recall, the dollar had rallied the first half of the week as the punditry was looking for the Fed to seem more hawkish. But that was not to be and this morning it is broadly, though not universally lower. AUD (+0.3%) and JPY (+0.2%) are the biggest gainers in the G10 while CHF (-0.65%) is the laggard after the rate cut, although has rebounded from its worst levels. In the EMG space, PHP (+0.4%), MYR (+0.5%) and IDR (+0.4%) are the leading gainers although we are seeing weakness in EEMEA with ZAR (-0.3%) and CZK (-0.3%) lagging.

On the data front, as it is Thursday, we see Initial (exp 215K) and Continuing (1815K) Claims as well as the Current Account deficit (-$209B) and Philly Fed (-2.3) all at 8:30. Then as the morning progresses, we see the Flash PMI data (51.7 Manufacturing, 52.0 Services), Existing Home Sales (3.94M) and Leading Indicators (-0.2%). As well, we get our first Fed speaker post the meeting, vice-chairman for regulation Michael Barr, this afternoon, but given my assessment that the Fed is happy with the market response, I don’t imagine he will say anything new.

Overall, the bulls and doves are walking hand in hand (what a terrible metaphor, sorry) and that means that risk assets are likely to continue to perform well for now and the dollar seems likely to come under a bit more pressure. I maintain that the bond market is going to figure out the inflation story is not great and react, but that is not today’s story.

Good luck

Adf