The ECI data’s designed

To help understand what’s enshrined

In hiring workers,

Including the shirkers,

With numbers quite nicely streamlined

The problem for Jay and the Fed

Is yesterday’s data brought dread

It rocketed higher

With wages on fire

And showing that rate cuts are dead

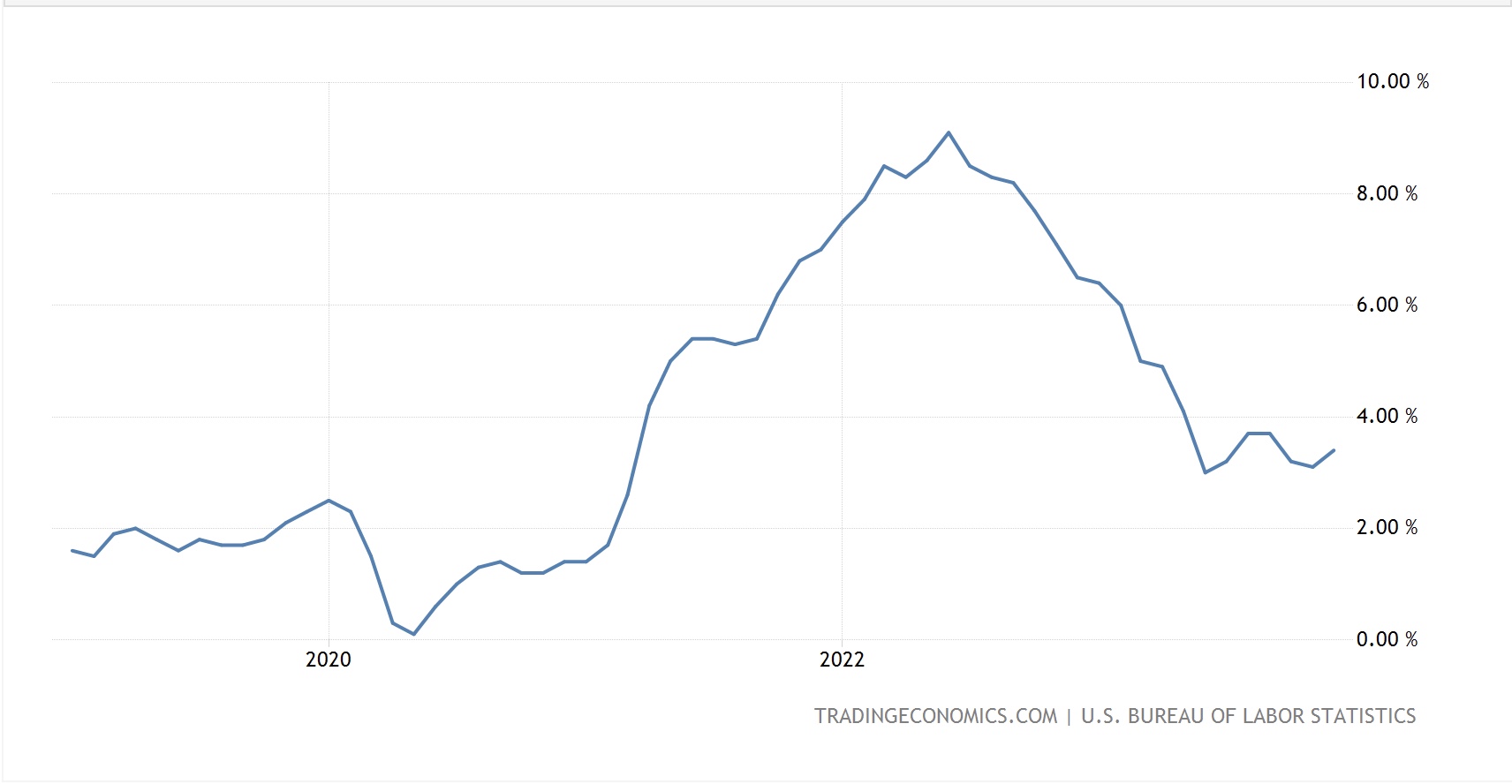

It’s funny the way things work. Historically, the number of people who paid attention to the Employment Cost Index (ECI), even in financial markets, could be counted on your fingers and toes. It was just not a meaningful datapoint in the scheme of the macro conversation. And yet, here we are in extraordinary times and suddenly it is a market mover! I have updated yesterday’s 10-year graph with the most recent print of 1.2% and it is now very evident that wage pressures are not dissipating at all. Rather, they seem to be accelerating and that is not going to help Jay achieve the 2.0% inflation goal.

Source: tradingeconomics.com

But in fairness, it wasn’t just the ECI. Yesterday’s data releases were lousy across the board. Case-Shiller Home prices rose more than expected, by 7.3% Y/Y. Chicago PMI fell sharply to 37.9, far below expectations and I guess we cannot be surprised that, given all that, Consumer Confidence fell to 97.0, its lowest reading since immediately after the pandemic. The upshot is rising prices and weakening growth, back to fears of stagflation. With that as backdrop, the fact that risk assets got slaughtered across the board yesterday seems par for the course.

And that is the setup for Jay and his merry band at the FOMC today. At this point, much ink has already been spilled trying to anticipate what the statement will say and how hawkish/dovish Powell will be at the press conference so there is very little I can add that will be new. I would contend the consensus is that the statement will be more hawkish, likely removing the line about “Inflation has eased over the past year but remains elevated,” or adjusting it. However, one of the things that has been pointed out lately is that Powell’s press conferences seem to have consistently been more dovish than the statement. Perhaps that happens again today, but I have to have some faith that Powell is actually trying to achieve the mandates and it is abundantly clear that right now the price side of the mandate is in jeopardy. As there are no dots or ‘official’ forecasts coming, my take is a slightly more hawkish statement and Powell backing that up later.

I guess the biggest question, especially after yesterday’s data, is how he will respond to questions regarding hiking rates further. If I were him, I would have that answer prepared to be as nondescript as possible. Because if he opens up that avenue of discussion, we are going to see a much more serious decline in risk assets.

One other thing of note yesterday was a comment by Secretary Yellen which was almost laughable when considering who is making the statement. Apparently, she is,” concerned about where we’re going with [the] US deficit.” Seriously? She is the Treasury Secretary in charge of spending plans and after pitching for ever more money to spend she is now concerned about the budget deficit? Then, apparently according to Axios, in a speech later today she is set to make a plea for the Fed’s independence! Again, seriously? The Fed is ostensibly already independent, yet I’m pretty certain she is bending Powell’s ear daily about what to do, i.e., commingling Treasury and the Fed. But suddenly she is concerned about its independence? It is things like this that make it so difficult to take certain players on the stage seriously. It doesn’t speak well of the current administration’s efforts to fix the problems that exist, many of which they have initiated.

Ok, enough ranting on my part. As it is May Day, much of Europe and some of Asia was closed last night but let’s recap the session as well as look ahead to the data before the FOMC. I’m pretty sure you know how poorly the equity markets behaved yesterday with -1.5%- to -2.0% losses in the US. In Asia, the markets that were open, Japan, Australia and New Zealand followed the same course, falling, albeit not quite as far, more on the order of -0.5% to -1.0%. in Europe, only the FTSE 100 is trading today, and it is flat on the session while US futures are pointing lower again, down -0.3% or so at this hour (7:00).

In the bond market, after yesterday’s Treasury selloff with yields jumping 8bps across the curve, markets are quiet with Europe on holiday so no change ahead of the NY opening. The rise in Treasury yields did drag European sovereign yields up as well, just not as far with most higher by 3bps-4bps yesterday and they are closed today. As to JGB yields, despite all the huffing and puffing in the FX market, they are essentially unchanged so far this week.

But the real fun yesterday was in the commodity markets with significant declines across the board. Oil prices fell on a combination of higher inventories according to the API as well as hopes of a ceasefire in Gaza helping to settle things down in the middle east. And they are lower by another -1.5% this morning. Meanwhile, metals markets, which had been exploding higher across the board until two days ago, had another wipeout yesterday with all the metals falling by 1% or more. This morning, though, they seem to have found some support with gold (+0.1%) and silver (+0.5%) bouncing slightly while copper (-0.8%) and aluminum (-0.3%) are still under pressure given the weaker economic data. Of course, underlying all this movement is concerns that interest rates are going to continue higher.

Which brings us to the dollar, which, not surprisingly given the rise in interest rates, rose sharply yesterday and is holding those gains this morning. On average, I would say the dollar gained 0.5% yesterday and it was broad based, rising against both G10 and EMG currencies as well as against financial and commodity currencies. For instance, CLP, which is closely linked to copper prices, fell -2.0% yesterday while ZAR was lower by -1.0%. But the euro (-0.6%) and pound (-0.4%) were also under pressure as traders started to anticipate an even more hawkish Fed today. I suspect things will be quiet until the FOMC this afternoon despite the data that is due.

Speaking of that data, first thing we get the ADP Employment report (exp 175K) then JOLTS Job Openings (8.69M) and ISM Manufacturing (50.0). A little later comes the EIA oil inventory data and then, of course, the FOMC statement at 2:00 with the press conference at 2:30. Since all eyes are focused on that, I would not expect much activity until it is released, and Powell speaks.

Good luck

Adf